Reports

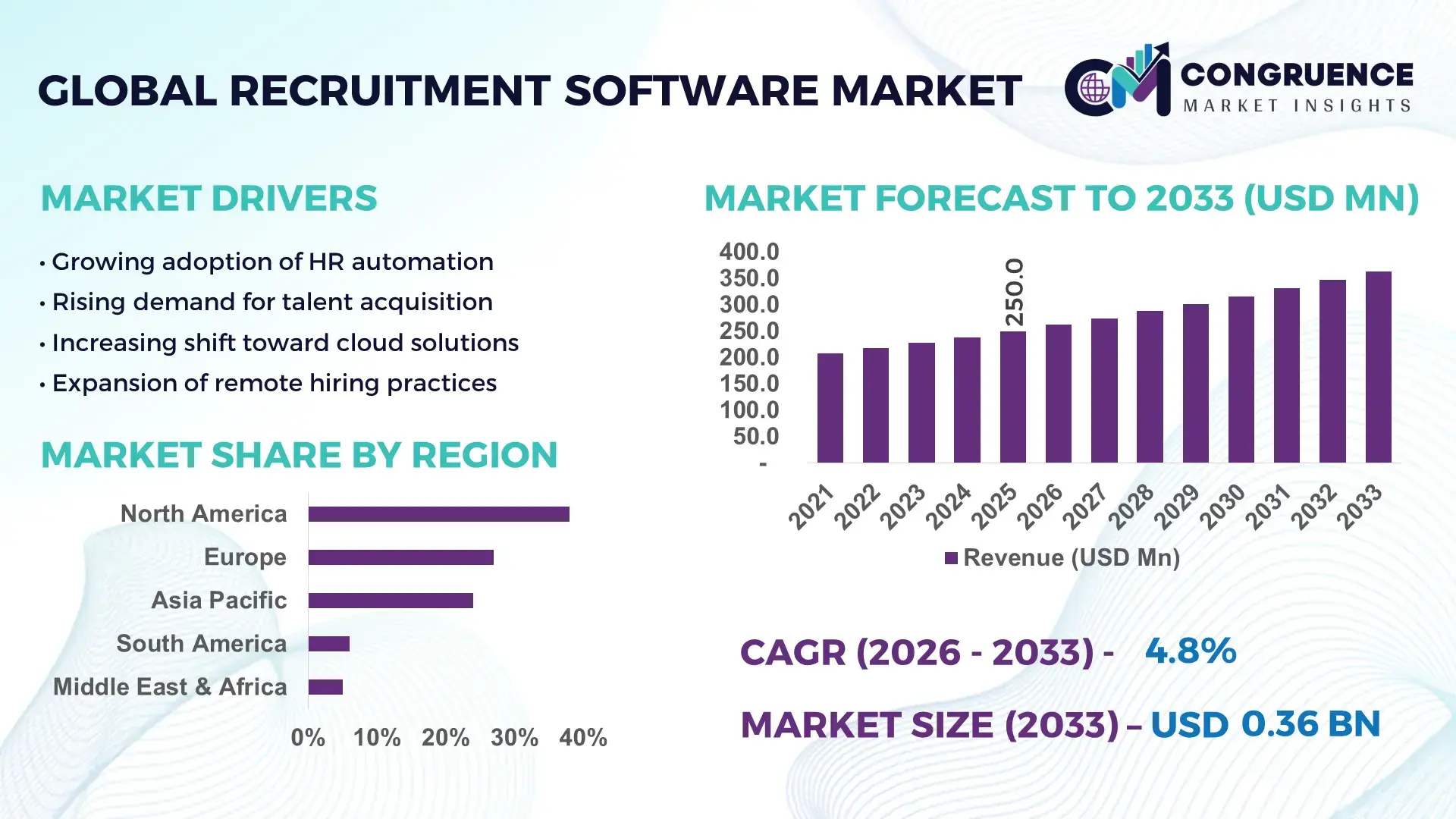

The Global Recruitment Software Market was valued at USD 250.0 Million in 2025 and is anticipated to reach a value of USD 363.8 Million by 2033 expanding at a CAGR of 4.8% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is primarily driven by increasing enterprise demand for automated hiring, AI-based candidate screening, and data-driven talent acquisition strategies.

The United States continues to dominate the Recruitment Software Market with over 42% enterprise-level adoption of cloud-based hiring platforms across Fortune 1000 companies. More than 65% of large enterprises in the country have integrated AI-enabled applicant tracking systems (ATS), while nearly 48% of SMEs are transitioning toward SaaS-based recruitment tools. The country hosts over 300+ recruitment technology vendors and attracts annual investments exceeding USD 1.2 billion in HR tech innovations. Key applications span BFSI, healthcare, and IT sectors, collectively accounting for over 58% of total software usage. Additionally, over 70% of hiring workflows in large corporations now include automation features such as resume parsing, chatbot screening, and predictive analytics, reflecting strong technological advancement and large-scale deployment.

Market Size & Growth: Valued at USD 250.0 Million in 2025, projected to reach USD 363.8 Million by 2033, growing at 4.8% CAGR driven by AI-led hiring automation and digital HR transformation.

Top Growth Drivers: AI adoption in hiring (68%), automation efficiency improvement (55%), cloud deployment expansion (61%).

Short-Term Forecast: By 2028, recruitment process costs are expected to reduce by 27% due to automation and analytics integration.

Emerging Technologies: AI-powered candidate matching, NLP-based resume parsing, predictive workforce analytics.

Regional Leaders: North America (USD 140 Million by 2033, high enterprise adoption), Europe (USD 95 Million, regulatory-driven digital hiring), Asia-Pacific (USD 82 Million, SME cloud adoption surge).

Consumer/End-User Trends: Over 62% of enterprises prefer integrated HR suites, while 49% SMEs rely on mobile-first recruitment platforms.

Pilot or Case Example: In 2025, a global IT firm reduced hiring time by 34% using AI screening tools.

Competitive Landscape: Market leader holds ~18% share, followed by SAP, Oracle, Workday, iCIMS, and ADP.

Regulatory & ESG Impact: 52% firms aligning hiring tools with data privacy laws and diversity hiring metrics.

Investment & Funding Patterns: Over USD 2.3 billion invested globally in HR tech startups between 2023–2025.

Enterprise HR solutions contribute approximately 46% of demand, followed by staffing agencies at 28% and SMEs at 26%. AI-driven tools such as automated interview scheduling and candidate scoring systems have improved recruiter productivity by over 30%. Regulatory compliance with data protection laws is influencing vendor design strategies, while Asia-Pacific markets are witnessing over 40% growth in mobile recruitment adoption, indicating strong future expansion potential.

The Recruitment Software Market is strategically positioned at the intersection of digital transformation and workforce optimization, enabling enterprises to streamline hiring processes, reduce operational inefficiencies, and enhance talent acquisition outcomes. Organizations leveraging AI-driven recruitment platforms have reported up to 35% improvement in candidate matching accuracy compared to traditional manual screening methods. Advanced analytics and automation tools are now integral to workforce planning, reducing time-to-hire by nearly 30% across large enterprises.

AI-based recruitment systems deliver 40% faster processing compared to legacy applicant tracking systems, demonstrating clear performance advantages. North America dominates in volume due to high enterprise penetration, while Asia-Pacific leads in adoption with over 54% of SMEs actively implementing cloud-based recruitment platforms. This divergence highlights a shift toward scalable and cost-effective hiring solutions in emerging economies.

By 2028, AI-powered recruitment tools are expected to reduce hiring costs by 25% while improving candidate experience scores by 32%. Firms are also committing to ESG metrics, with over 48% targeting diversity hiring improvements and 20% reduction in hiring bias through algorithmic transparency by 2030. In 2025, a leading European HR technology firm achieved a 28% reduction in hiring cycle time through AI-enabled candidate ranking systems.

The future pathway of the Recruitment Software Market is closely aligned with automation, compliance, and sustainability. As organizations increasingly adopt integrated HR ecosystems, recruitment software is evolving into a critical pillar supporting operational resilience, regulatory adherence, and long-term workforce strategy.

The Recruitment Software Market is experiencing steady transformation driven by digitalization, automation, and increasing reliance on data-driven decision-making in talent acquisition. Enterprises across industries are transitioning from manual hiring processes to automated systems, with over 60% of organizations globally implementing some form of recruitment technology. The rise of remote and hybrid work models has further accelerated demand for cloud-based platforms, enabling recruiters to manage geographically dispersed talent pools efficiently. Additionally, the growing importance of employer branding and candidate experience is influencing software capabilities, including chatbot integration and real-time communication tools. SMEs are rapidly adopting cost-effective SaaS solutions, contributing to broader market penetration. Meanwhile, integration with HR analytics platforms and enterprise resource planning systems is becoming a key differentiator, enhancing the strategic value of recruitment software in workforce planning and management.

AI-driven automation is significantly enhancing recruitment efficiency by reducing manual workload and improving candidate screening accuracy. Over 68% of organizations now use AI-based tools for resume parsing and candidate matching, enabling recruiters to process applications up to 5 times faster. Automated chatbots are handling nearly 45% of initial candidate interactions, improving engagement rates and reducing response times. Additionally, predictive analytics tools are helping companies identify high-potential candidates with up to 30% greater accuracy compared to traditional methods. Industries such as IT and BFSI have reported a 25–35% improvement in hiring efficiency due to AI integration. The ability to minimize human bias and standardize evaluation criteria is further driving adoption, particularly among large enterprises focused on diversity hiring initiatives.

Data privacy concerns and integration complexities remain critical challenges impacting market expansion. Approximately 52% of organizations report difficulties in ensuring compliance with global data protection regulations such as GDPR and similar frameworks. Handling sensitive candidate data across multiple jurisdictions requires robust security measures, increasing implementation complexity. Additionally, nearly 40% of enterprises face challenges integrating recruitment software with existing HR systems, leading to operational inefficiencies. Legacy infrastructure in large organizations often limits seamless adoption, requiring significant upgrades. Concerns around algorithmic bias and lack of transparency in AI decision-making are also affecting trust among users. These factors collectively slow down adoption rates, particularly among regulated industries such as healthcare and finance.

Cloud-based recruitment solutions are opening new growth avenues by offering scalability, cost efficiency, and remote accessibility. Over 61% of SMEs globally are adopting SaaS-based recruitment platforms due to lower upfront costs and flexible deployment models. Cloud solutions enable real-time collaboration among hiring teams, reducing recruitment cycle times by approximately 20%. Emerging markets, particularly in Asia-Pacific, are witnessing over 40% growth in mobile-enabled recruitment platforms, driven by increasing internet penetration and smartphone usage. Integration with AI and analytics tools further enhances functionality, enabling data-driven hiring decisions. Additionally, subscription-based pricing models are making advanced recruitment technologies accessible to smaller organizations, expanding the overall addressable market.

The evolving nature of job roles and persistent talent shortages are posing challenges for recruitment software effectiveness. Over 58% of organizations report difficulties in finding candidates with required digital skills, particularly in emerging fields such as AI and cybersecurity. Recruitment platforms must continuously update algorithms to match evolving skill sets, requiring ongoing investment in technology upgrades. Additionally, candidate expectations have shifted, with over 65% prioritizing personalized and seamless application experiences. Failure to meet these expectations can lead to high drop-off rates. The need for multilingual capabilities and cultural adaptability further complicates software development, especially for global enterprises. These challenges require continuous innovation to maintain relevance and effectiveness.

• AI-driven candidate matching improving hiring accuracy by 35%: Organizations are increasingly deploying AI algorithms that analyze over 100+ candidate data points, improving hiring accuracy by nearly 35%. Around 68% of enterprises now use AI tools for screening, significantly reducing manual intervention and enhancing recruitment precision.

• Mobile-first recruitment platforms rising with 45% adoption growth: Mobile recruitment applications are witnessing rapid growth, with over 45% increase in usage among SMEs. More than 52% of job seekers now prefer mobile-based applications, driving vendors to prioritize mobile optimization and app-based hiring interfaces.

• Integration with HR analytics improving decision-making by 30%: Approximately 60% of enterprises have integrated recruitment software with HR analytics platforms, enabling data-driven decisions. This integration has resulted in a 30% improvement in hiring efficiency and workforce planning accuracy.

• Automation reducing time-to-hire by up to 40%: Automated interview scheduling and chatbot interactions have reduced hiring cycle times by up to 40%. Nearly 50% of large enterprises now rely on automation tools to streamline recruitment workflows and enhance candidate engagement.

The Recruitment Software Market is segmented based on type, application, and end-user, each playing a critical role in shaping demand patterns and adoption trends. Cloud-based solutions dominate due to their scalability and ease of deployment, while on-premise systems continue to hold relevance in highly regulated industries. Application-wise, large enterprises lead adoption due to complex hiring needs, whereas SMEs are rapidly transitioning toward cost-effective SaaS models. End-user segmentation highlights strong demand from IT, BFSI, and healthcare sectors, collectively contributing over 60% of total usage. The increasing integration of AI and analytics across all segments is enhancing functionality and driving innovation in recruitment platforms.

Cloud-based recruitment software accounts for approximately 64% of total adoption due to its scalability, cost efficiency, and remote accessibility. On-premise solutions hold around 36%, primarily preferred by organizations with stringent data security requirements. However, hybrid models are emerging rapidly, expected to grow at a CAGR of 6.5%, driven by demand for flexible deployment options. Other niche solutions, including open-source and customized platforms, collectively contribute nearly 18% of the market, catering to specific enterprise needs. Cloud solutions are widely adopted across SMEs, with over 61% preferring SaaS-based platforms for recruitment operations.

• In 2025, a global technology consortium reported that over 70% of enterprises migrating to cloud recruitment systems achieved improved hiring workflow efficiency and reduced system downtime.

Large enterprises dominate with approximately 48% share due to high-volume hiring requirements and complex workforce management needs. SMEs account for around 32%, while staffing agencies contribute nearly 20%. Recruitment software adoption in large enterprises is driven by the need for automation and analytics, improving hiring efficiency by over 30%. The fastest-growing segment is staffing agencies, expanding at a CAGR of 6.9%, supported by increasing demand for outsourced recruitment services. Over 38% of enterprises globally reported piloting recruitment software for customer-facing roles in 2025, while 60% of Gen Z job seekers prefer AI-enabled hiring platforms.

• In 2025, a global HR research organization highlighted that AI-powered recruitment tools were deployed across more than 150 enterprise organizations, significantly improving early candidate screening outcomes.

The IT sector leads with approximately 34% share, driven by high demand for skilled professionals and continuous hiring cycles. BFSI follows with 26%, while healthcare accounts for 18%. Other sectors, including retail and manufacturing, collectively contribute around 22%. The fastest-growing end-user segment is healthcare, expanding at a CAGR of 6.7%, supported by increasing demand for specialized talent. Over 42% of enterprises in developed economies are testing AI-based recruitment tools, while 58% of organizations report improved hiring efficiency through automation.

• In 2025, a global technology advisory firm reported that over 500 companies implemented AI-driven recruitment systems, improving workforce analytics and talent acquisition strategies significantly.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2026 and 2033.

North America benefits from high enterprise adoption and advanced HR tech ecosystems, while Europe holds approximately 27% share driven by regulatory compliance requirements. Asia-Pacific accounts for nearly 24% share, with rapid SME adoption and mobile-first recruitment solutions. South America contributes around 6%, and Middle East & Africa hold approximately 5%, supported by gradual digital transformation. Over 65% of enterprises in developed regions have adopted AI-based recruitment tools, compared to 40% in emerging markets, highlighting regional disparities in technology penetration.

North America holds approximately 38% market share, driven by strong adoption across IT, BFSI, and healthcare sectors. Over 70% of large enterprises use AI-powered recruitment tools, while regulatory frameworks emphasize data protection and fair hiring practices. Technological advancements such as predictive analytics and automation are widely implemented. A leading regional player has introduced AI copilots improving recruiter productivity by 30%. Consumer behavior indicates higher adoption among enterprises seeking efficiency and compliance.

Europe accounts for around 27% market share, with key markets including Germany, the UK, and France. Regulatory bodies enforce strict data protection laws, influencing software design and adoption. Over 58% of enterprises prioritize compliance-driven recruitment tools. Emerging technologies such as AI and NLP are gaining traction. A regional vendor has launched GDPR-compliant recruitment solutions, enhancing trust and adoption. Consumer behavior reflects demand for transparent and ethical hiring systems.

Asia-Pacific ranks among the fastest-growing regions, with strong demand from China, India, and Japan. Over 45% of SMEs are adopting cloud-based recruitment tools, supported by increasing digital infrastructure. Innovation hubs are driving AI integration, with mobile-first platforms gaining popularity. A regional company has developed mobile recruitment apps used by over 2 million users. Consumer behavior shows preference for cost-effective and scalable solutions.

South America accounts for approximately 6% market share, with Brazil and Argentina leading adoption. Infrastructure improvements and government incentives are supporting digital transformation. Over 35% of enterprises are adopting recruitment software to improve hiring efficiency. A local provider has introduced AI-based hiring tools improving candidate matching accuracy. Consumer behavior highlights demand for localized and language-specific solutions.

Middle East & Africa hold around 5% market share, driven by demand in UAE and South Africa. Key sectors include oil & gas and construction. Technological modernization and trade partnerships are supporting adoption. Over 30% of enterprises are implementing digital hiring tools. A regional company has launched cloud-based recruitment platforms improving hiring efficiency. Consumer behavior reflects gradual adoption with focus on cost optimization.

United States – 38% Market share: Strong enterprise adoption and advanced HR technology infrastructure

China – 18% Market share: Rapid SME digitalization and growing demand for cloud-based recruitment tools

The Recruitment Software Market is moderately fragmented, with over 150 active global and regional players competing across various segments. The top five companies collectively account for approximately 45% of the total market share, indicating a competitive yet evolving landscape. Leading players are focusing on AI integration, cloud-based solutions, and strategic partnerships to strengthen their market position. Mergers and acquisitions have increased by over 20% between 2023 and 2025, reflecting consolidation trends.

Product innovation remains a key differentiator, with over 60% of vendors introducing AI-driven features such as predictive analytics and chatbot integration. Startups are gaining traction by offering niche solutions targeting SMEs, while established players focus on enterprise-grade platforms. The competitive environment is characterized by continuous technological advancements, customer-centric solutions, and expanding global footprints.

Oracle

Sap

ADP, Inc.

iCIMS, Inc.

Cornerstone OnDemand, Inc.

Greenhouse Software, Inc.

Lever, Inc.

Jobvite, Inc.

SmartRecruiters, Inc.

BambooHR LLC

Zoho Corporation

Ultimate Software Group

ClearCompany, Inc.

The Recruitment Software Market is undergoing rapid technological transformation, driven by advancements in artificial intelligence, machine learning, and data analytics. AI-powered candidate matching systems are now capable of analyzing over 150 data points, improving hiring accuracy by nearly 35%. Natural language processing (NLP) is widely used for resume parsing and candidate communication, enabling automation of up to 60% of initial screening tasks. Predictive analytics tools are helping organizations forecast hiring needs with up to 28% greater accuracy, enhancing workforce planning. Cloud computing remains a key enabler, with over 65% of enterprises adopting SaaS-based recruitment platforms for scalability and flexibility.

Integration with HR management systems and enterprise resource planning tools is improving operational efficiency by approximately 30%. Emerging technologies such as AI copilots and blockchain-based credential verification are gaining traction, enhancing transparency and security in hiring processes. Additionally, mobile-first platforms are supporting remote recruitment, with over 50% of job applications now submitted via mobile devices. These technological advancements are reshaping the recruitment landscape, making it more efficient, data-driven, and candidate-centric.

• In March 2025, Workday announced its Spring 2025 Release with over 350 new features, including AI-powered talent rediscovery and integrated candidate sourcing tools that enable recruiters to identify qualified candidates from existing talent pools in real time, improving hiring efficiency and candidate experience. Source: www.workday.com

• In August 2025, Workday signed a definitive agreement to acquire Paradox, an AI recruitment platform known for its conversational assistant “Olivia,” which automates screening, interview scheduling, and candidate communication, enhancing high-volume hiring processes across enterprises.

• In September 2024, Workday introduced new AI-powered recruiting agents as part of its “Illuminate” platform, including Recruiter Agent capabilities designed to streamline hiring workflows, automate repetitive tasks, and improve decision-making across HR functions.

• In August 2024, Workday expanded its recruitment capabilities through the integration of HiredScore AI, enabling advanced talent mobility and recruiting solutions that enhance recruiter productivity and support data-driven hiring decisions across enterprise environments.

The Recruitment Software Market Report provides a comprehensive analysis of key industry segments, including type, application, and end-user categories. The report covers cloud-based, on-premise, and hybrid deployment models, highlighting their adoption patterns across enterprises and SMEs. It evaluates applications across large enterprises, staffing agencies, and small businesses, offering insights into usage trends and operational efficiencies. The report also examines end-user industries such as IT, BFSI, healthcare, retail, and manufacturing, which collectively drive significant demand for recruitment solutions.

Geographically, the report analyzes market trends across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, providing detailed insights into regional adoption patterns and technological advancements. It highlights key factors influencing demand, including digital transformation, regulatory compliance, and workforce dynamics. The scope further includes emerging technologies such as AI, machine learning, NLP, and predictive analytics, which are shaping the future of recruitment processes.

Additionally, the report explores competitive dynamics, innovation trends, and strategic initiatives undertaken by key market players. It identifies growth opportunities in underserved markets and niche segments, including mobile recruitment and AI-driven hiring tools. The comprehensive scope ensures actionable insights for decision-makers, enabling informed strategic planning and investment decisions across the recruitment software ecosystem.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 250.0 Million |

| Market Revenue (2033) | USD 363.8 Million |

| CAGR (2026–2033) | 4.8% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Workday; Oracle; SAP; ADP; iCIMS; Cornerstone OnDemand; Greenhouse Software; Lever; Jobvite; SmartRecruiters; BambooHR; Zoho Corporation; Ultimate Software; ClearCompany |

| Customization & Pricing | Available on Request (10% Customization Free) |