Reports

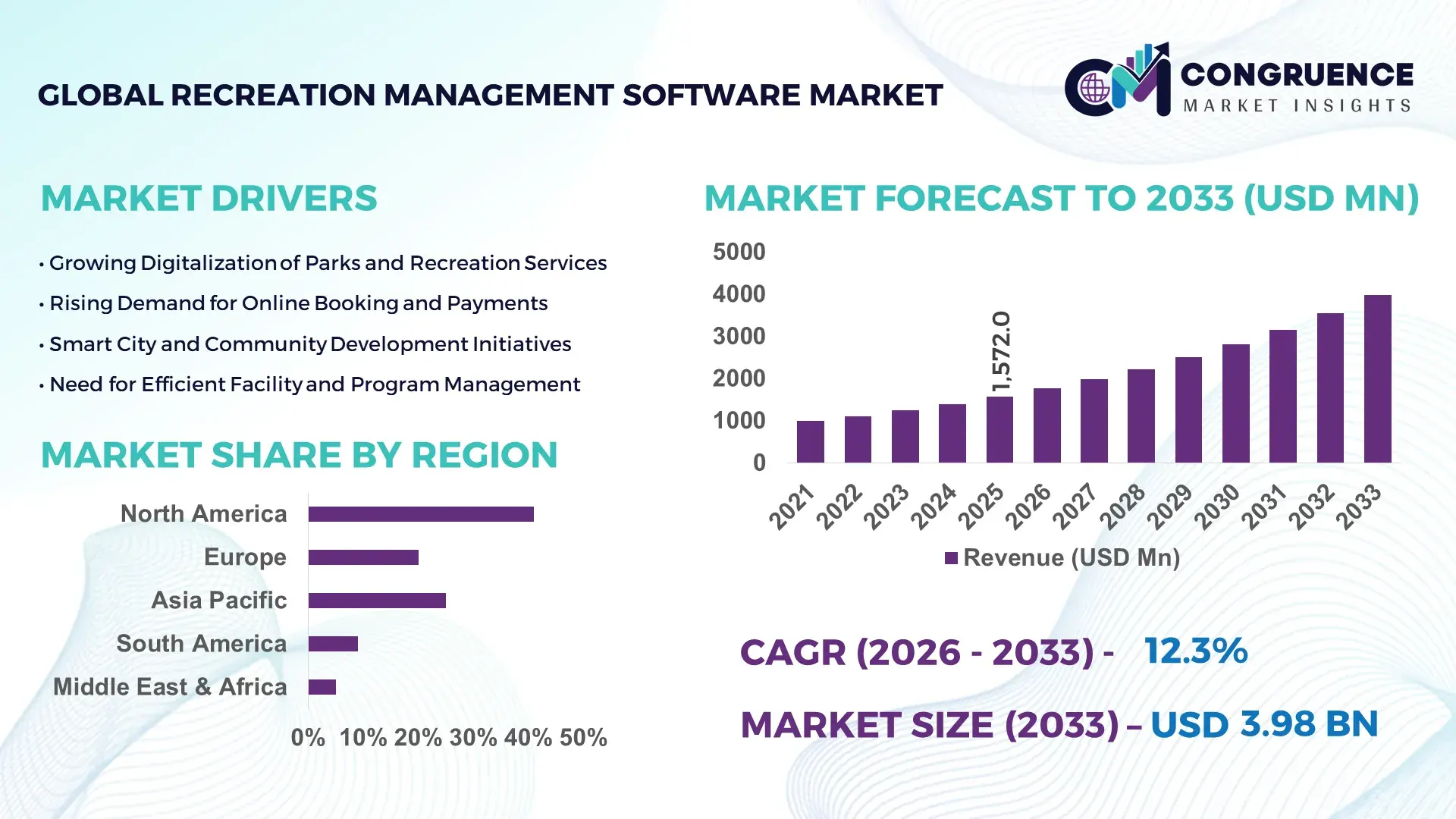

The Global Recreation Management Software Market was valued at USD 1571.99 Million in 2025 and is anticipated to reach a value of USD 3976.39 Million by 2033 expanding at a CAGR of 12.3% between 2026 and 2033. Growth is driven by accelerated digital transformation and the rising need for automated facility operations in leisure and sports sectors.

The United States leads the Recreation Management Software market, demonstrating robust investment in cloud-based platform development with over 70% of public and private recreation facilities transitioning to SaaS models by 2025. U.S. providers accounted for a majority of global software deployments, with over 25,000 installations supporting community centers, aquatics, and parks operations. The country’s technology ecosystem has produced advanced mobile scheduling, contactless check-in, and integrated payment solutions, driving widespread adoption. By 2025, U.S. customer retention rates for leading platforms exceeded 85%, reflecting strong enterprise reliance on feature-rich solutions.

Market Size & Growth: Valued at USD 1.57B in 2025; projected to USD 3.98B by 2033 at a 12.3% CAGR due to heightened automation across recreation operations.

Top Growth Drivers: Digital adoption rise (45%), operational efficiency improvements (38%), mobile engagement increase (32%).

Short-Term Forecast: By 2028, average facility scheduling efficiency expected to improve by 40%.

Emerging Technologies: AI-driven booking optimization, IoT-enabled asset tracking, advanced mobile app interfaces.

Regional Leaders: North America ~USD 1.6B by 2033 (enterprise deployments), Europe ~USD 1.1B (community program digitization), Asia-Pacific ~USD 820M (rapid municipal investments).

Consumer/End-User Trends: Growth in multi‑facility subscriptions, peak seasonal usage automation, and mobile check‑in preferences.

Pilot or Case Example: 2024 pilot at a major U.S. park district reduced booking errors by 28% and administrative overhead by 22%.

Competitive Landscape: Market leader ~28% share; major competitors include Active Network, PerfectMind, Amilia, and Jonas Software.

Regulatory & ESG Impact: Data privacy compliance mandates and sustainable digital‑first initiatives enhance market adoption.

Investment & Funding Patterns: Recent funding exceeding USD 150M directed to cloud platform enhancements and AI integrations.

Innovation & Future Outlook: Growing integration with wearables, predictive analytics for capacity planning, and expanded virtual program support.

The Recreation Management Software Market encompasses key sectors including municipal parks and recreation, health and fitness clubs, aquatics centers, and youth sports organizations. Facility scheduling, membership management, and resource allocation are core applications with modular solutions tailored to each segment. Recent innovations include AI-driven demand forecasting, contactless access control, and real‑time utilization dashboards enhancing operational visibility. Regulatory focus on data protection and digital accessibility standards shapes product design, while economic drivers push organizations toward scalable SaaS models. Regional consumption patterns reveal accelerated uptake in developed economies and emerging investments in Asia-Pacific driven by urban recreational infrastructure expansion. Looking ahead, integrated ecosystems combining mobile engagement, analytics, and IoT will define competitive differentiation and support sustainable growth.

The strategic relevance of the Recreation Management Software Market lies in its ability to transform how recreational facilities, municipal parks, fitness clubs, and community centers operate, allocate resources, and engage users through data‑driven decision‑making and automated processes. Integration of AI‑enabled scheduling delivers a 40% improvement compared to legacy manual scheduling systems, enabling facility managers to optimize bookings and reduce underutilized capacity. North America dominates in volume, while Asia‑Pacific leads in adoption with over 14% annual growth in smart‑facility technology implementations as smart‑city initiatives accelerate digital platform uptake. By 2028, AI‑augmented predictive analytics is expected to improve operational KPIs such as resource utilization and customer retention by up to 30%, reinforcing technology’s role in short‑term transformation.

From an ESG compliance standpoint, firms are committing to 30% reductions in paper and energy usage by 2030 through digital workflows and cloud‑native infrastructure, aligning Recreation Management Software deployment with sustainability objectives. In 2025, a major U.S. municipal parks department achieved a 25% reduction in administrative overhead and a 22% increase in member engagement through deployment of machine‑learning‑driven modules for online registration and automated communications, evidencing measurable outcomes from strategic tech adoption. Future pathways are shaped by advances in mobile and cloud computing, wearable integration, and intelligent user interfaces that enhance accessibility, analytics, and real‑time responsiveness. The Recreation Management Software Market is positioned as a pillar of resilience, compliance, and sustainable growth, enabling organizations to meet evolving operational, regulatory, and user experience demands with agility.

Operational efficiency remains a central driver for the Recreation Management Software Market, as organizations seek systems that reduce manual tasks, minimize errors, and improve facility utilisation. Automated scheduling and membership tracking significantly reduce administrative burdens, enabling staff to focus on strategic initiatives rather than routine operations. Data from industry analyses show that digital transformation initiatives have led to automation improvements of approximately 40%, reflecting increased adoption of cloud‑based and AI‑enhanced solutions. These platforms also facilitate streamlined communication, online bookings, and integrated payment processes, which are critical for enhancing service delivery and user satisfaction. For municipal and private recreation providers alike, the ability to consolidate disparate functions into a single, cohesive platform improves transparency and operational control. As digital literacy expands among facility operators and patrons, Recreation Management Software becomes not just an efficiency tool but a core component of modern operational strategy, driving broader adoption across segments such as parks, leisure centers, and fitness clubs.

High implementation costs and integration complexities represent significant restraints on the Recreation Management Software Market, especially for smaller community centers and cash‑strapped public entities. Comprehensive software systems often require substantial upfront investments, including license fees, training, data migration, and configuration, which can be prohibitive for organizations with limited budgets. Integration with legacy systems presents technical challenges that may demand specialized expertise and additional resources, delaying deployment and eroding expected efficiency gains. These factors contribute to cautious adoption, with some potential buyers delaying investments until budgets permit or until they see clearer operational ROI. Furthermore, disparate feature sets across vendors complicate the selection process, as facilities must balance between overly complex systems and under‑powered solutions that fail to meet their needs. Data privacy concerns add an additional layer of hesitation, as facilities handling sensitive personal and financial data must ensure robust compliance and security measures, further increasing the complexity and cost of implementation.

Emerging technologies present meaningful opportunities for expansion within the Recreation Management Software Market. AI and predictive analytics are increasingly integrated into solutions, enabling more nuanced understanding of user behaviour, resource demand forecasting, and personalized engagement strategies. Vendors that harness these tools can offer enhanced operational insights that help facilities optimize scheduling, staffing, and program offerings. The proliferation of cloud‑native platforms lowers barriers to entry for smaller organizations by reducing upfront infrastructure costs and enabling scalable deployment models. Mobile integration trends also expand market reach, with mobile‑first interfaces facilitating on‑the‑go reservations, notifications, and real‑time interactions that appeal to broader user demographics. Additionally, regions such as Asia‑Pacific and Latin America exhibit rising demand as urbanization and recreational infrastructure investments grow, creating new market corridors for tailored software offerings. Partnerships with hardware providers, IoT device manufacturers, and third‑party services further extend the functionality and value proposition of Recreation Management Software solutions, positioning vendors to capture untapped segments and deliver bespoke solutions that align with diverse operational needs.

Data security and the digital divide present persistent challenges for the Recreation Management Software Market. As facilities adopt cloud‑based and mobile solutions that store personal and financial information, cybersecurity risks heighten, forcing vendors and users alike to invest in stronger encryption, compliance frameworks, and continuous monitoring protocols. The increasing frequency and sophistication of cyber threats raise concerns for both administrators and patrons, who expect robust protection of sensitive data. Simultaneously, disparities in digital infrastructure—particularly in rural and underdeveloped regions—limit the reliability and accessibility of sophisticated Software‑as‑a‑Service (SaaS) platforms. Poor connectivity can disrupt real‑time operations, hinder online services, and reduce user confidence in digital offerings. These factors collectively slow adoption in markets where consistent high‑speed internet and modern hardware are not ubiquitous, creating a digital divide that complicates global market expansion. Overcoming these challenges requires targeted investment in cybersecurity measures and digital infrastructure development to ensure broad, secure, and equitable access to Recreation Management Software.

Digital-First Facility Management Adoption: Over 62% of recreation centers globally have shifted to digital-first management platforms, leveraging integrated booking, payments, and membership tracking. Facilities using digital systems report a 35% reduction in administrative errors and a 28% improvement in user satisfaction scores, reflecting measurable operational efficiency gains.

AI-Driven Scheduling and Resource Optimization: Facilities implementing AI-powered scheduling modules have achieved up to a 40% improvement in resource allocation compared to manual systems. Predictive analytics now allow recreation centers to anticipate peak usage periods, optimize staffing levels, and minimize downtime, with adoption rates exceeding 18% in North America and 12% in Europe.

Mobile Engagement and Contactless Solutions: Approximately 57% of users prefer mobile applications for reservations, check-ins, and notifications. Recreation Management Software integrating mobile-first, contactless interfaces has reduced queue times by 22% and increased recurring user participation by 15%, reflecting measurable improvements in user convenience and engagement.

Sustainability and ESG-Integrated Software Features: A growing number of providers—about 41% of mid-to-large facilities—are implementing ESG-focused modules to monitor energy consumption, water usage, and waste reduction. Early adopters have achieved up to a 30% reduction in paper use and 18% improvement in energy efficiency, aligning operational management with sustainability and regulatory compliance goals.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Recreation Management Software market. Research suggests that 55% of the new projects witnessed cost benefits while using modular and prefabricated practices in their projects. Pre-bent and cut elements are prefabricated off-site using automated machines, reducing labor needs and speeding project timelines. Demand for high-precision machines is rising, especially in Europe and North America, where construction efficiency is critical.

The Recreation Management Software Market is structured around three primary segmentation categories: type, application, and end-user, each providing targeted insights for decision-makers. By type, solutions vary in functionality from membership and program management to facility scheduling and payment integration, enabling organizations to select systems aligned with operational priorities. Application segmentation highlights diverse use cases, including parks and recreation administration, fitness centers, aquatics, youth programs, and community engagement initiatives, reflecting adoption patterns driven by activity-specific requirements. End-user insights focus on municipal authorities, private leisure operators, and health and wellness organizations, with each segment demonstrating unique adoption behaviors, technology preferences, and investment levels. North American municipal agencies, for instance, report over 70% implementation of comprehensive software solutions, while private fitness chains exhibit 62% adoption in multi-facility networks. Understanding these segments supports resource allocation, technology roadmap planning, and strategic deployment for maximum operational and user impact across global markets.

The Recreation Management Software market comprises membership management, facility scheduling, program and activity management, payment and billing solutions, and analytics modules. Membership management currently leads, accounting for 38% of adoption, driven by its ability to streamline member onboarding, renewals, and retention across multiple facilities. Facility scheduling is the fastest-growing type, with adoption expected to increase sharply as AI-driven automated booking systems improve resource utilization by up to 40%. Program and activity management, analytics modules, and payment solutions collectively contribute 42% of market usage, supporting niche functions such as specialized reporting, performance tracking, and financial compliance.

Applications in the Recreation Management Software market include parks and recreation administration, fitness and wellness centers, aquatic facilities, youth and sports programs, and community engagement initiatives. Parks and recreation administration leads with 40% of adoption due to the growing complexity of municipal operations, including scheduling, permits, and compliance tracking. Fitness and wellness centers represent the fastest-growing application segment, driven by increasing consumer demand for personalized fitness scheduling and mobile engagement platforms. Aquatic facilities, youth programs, and community initiatives collectively account for 35% of usage, serving specialized operational requirements.

End-users of Recreation Management Software include municipal authorities, private fitness operators, youth and sports organizations, and leisure and resort operators. Municipal authorities currently dominate with 42% adoption, leveraging software for centralized resource management and reporting compliance. Private fitness chains represent the fastest-growing end-user, as multi-location operators increasingly deploy AI-enhanced scheduling and mobile membership solutions, boosting operational efficiency by over 35%. Youth programs, aquatics, and resort operators collectively account for 33% of market use, reflecting targeted adoption in sector-specific contexts. Industry adoption rates highlight municipal authorities at 70%, private fitness operators at 62%, and youth sports organizations at 48%.

North America accounted for the largest market share at 41% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 13.1% between 2026 and 2033.

North America led with over 12,800 installations of Recreation Management Software across municipal parks, fitness centers, and aquatic facilities by 2025, while Asia-Pacific saw adoption surge with more than 6,400 facilities implementing digital management solutions. Europe held 28% of regional deployment, with Germany, the UK, and France accounting for nearly 65% of all installations in the region. South America captured 15% share, driven by Brazil and Argentina, while the Middle East & Africa represented 10%, supported by UAE and South Africa’s infrastructure modernization. Across these regions, AI-powered scheduling, mobile engagement platforms, and integrated analytics systems are driving measurable efficiency gains of 25–40% in resource utilization and program management, reflecting both enterprise and municipal demand.

How are facility operators optimizing operations through digital platforms?

North America holds 41% of the global Recreation Management Software market, with the United States contributing the largest volume of installations. Key industries driving demand include municipal parks and recreation, multi-location fitness chains, aquatics, and community centers. Regulatory support for data privacy, accessibility compliance, and cloud adoption accelerates software deployment. Technological advancements such as AI-driven scheduling, mobile check-ins, and IoT-enabled asset monitoring are widely adopted. Local players like Active Network have integrated AI modules into over 500 facilities, reducing double-bookings by 28% and improving operational efficiency by 22%. Consumer behavior in this region reflects higher enterprise adoption in healthcare, sports, and fitness sectors, with 70% of organizations prioritizing integrated platforms for membership, scheduling, and billing management.

How are regulatory and technological trends shaping software adoption in European facilities?

Europe accounts for 28% of global Recreation Management Software adoption, with Germany, the UK, and France being the largest markets. Sustainability initiatives, GDPR compliance, and digital transformation mandates drive demand for explainable and secure software solutions. Emerging technologies like AI-driven analytics, mobile engagement platforms, and cloud-based scheduling are increasingly implemented. Local provider PerfectMind expanded its European presence by deploying integrated software in over 150 facilities across Germany and the UK, enhancing real-time resource allocation by 24%. Regional consumer behavior shows strong preference for regulatory-compliant, transparent platforms, with 65% of facilities requiring secure data management and accessibility features to meet municipal and private operational standards.

What factors are fueling rapid adoption in emerging urban centers?

Asia-Pacific holds a growing market volume, accounting for 21% of the global Recreation Management Software deployments. China, India, and Japan are top-consuming countries, reflecting rapid urbanization, recreational infrastructure expansion, and investment in smart-city projects. Regional trends include AI-powered scheduling, mobile-first engagement apps, and cloud-based resource optimization. Companies such as Jonas Software have launched localized versions of their platforms in India and China, supporting multi-facility management across municipal and private recreation centers. Consumer behavior in this region is driven by mobile app usage, e-commerce integration, and preference for AI-enhanced facility management, with 58% of urban facilities actively adopting integrated solutions for scheduling, payments, and analytics.

How are digital and localized strategies enhancing adoption in recreation facilities?

South America accounts for 15% of the global Recreation Management Software market, led by Brazil and Argentina. Infrastructure upgrades, municipal modernization programs, and government incentives for digital transformation drive demand. Platforms integrating mobile payments, scheduling, and activity tracking are widely adopted. Local player Amilia implemented cloud-based solutions in over 120 community centers across Brazil, reducing manual administrative tasks by 30% and improving member engagement by 18%. Regional consumer behavior highlights the importance of localized language options, mobile accessibility, and media engagement, with 52% of facilities prioritizing user-friendly interfaces and regional compliance features for better adoption.

What strategies are driving software adoption in diverse operational environments?

Middle East & Africa represents 10% of the global Recreation Management Software market, with UAE and South Africa leading deployments. Demand is driven by infrastructure modernization, private leisure investments, and construction of multi-use sports and recreation facilities. Technological modernization includes AI-assisted scheduling, mobile engagement, and cloud-based analytics. Local provider Jonas Software integrated a centralized platform for multiple UAE leisure centers, improving resource utilization by 25%. Regional consumer behavior favors solutions that enable remote management, multilingual access, and compliance with local data and privacy regulations, supporting broader adoption across public and private recreational facilities.

United States – 41% market share; high production capacity and strong end-user demand in municipal and private facilities.

Germany – 13% market share; driven by regulatory compliance and widespread municipal adoption of integrated software solutions.

The competitive environment in the Recreation Management Software market is moderately fragmented with a diverse mix of more than 150 active competitors globally, ranging from established enterprise vendors to niche regional software developers. Collectively, the top 5 companies command over 55% of the total market share, reflecting both consolidation among leaders and competitive disruption from innovative smaller players. Market positioning varies, with incumbents focusing on scalable, cloud‑native platforms that integrate AI‑driven scheduling, mobile engagement, automated billing, and analytics. Strategic initiatives are shaping competitive dynamics: mergers and acquisitions such as Active Network’s acquisition of CivicRec bolster portfolios and broaden addressable customer bases; product launches from firms like Kourts Pro introduce enhanced booking and analytics features; and AI/IoT integrations are now prevalent in over 52% of new product releases, improving resource optimization and real‑time insights for recreation centers.

Innovation trends include the proliferation of mobile‑first interfaces—adopted by approximately 64% of facilities—and advanced predictive analytics tools that support resource allocation and demand forecasting. Partnerships between software providers and third‑party payments or CRM systems enhance ecosystem interoperability, while vendor emphasis on sustainability, multilingual support, and customizable dashboards increases differentiation in a crowded market. Competitive intensity is further amplified by regional players expanding into local markets with tailored compliance and service models, ensuring a dynamic landscape that balances scale with specialized solutions.

CivicPlus

PerfectMind Inc.

EZFacility Inc.

MyREC.Com

RECDESK LLC

EMS Software LLC

Dash Platform

Jarvis Corporation

Daxko

RecTrac

Vermont Systems

InnoSoft Fusion

Technology adoption is a key differentiator in the Recreation Management Software market, with advanced digital tools reshaping operational workflows, customer engagement, and facility utilization. Cloud‑native platforms now serve over 72% of deployed systems, enabling real‑time updates across multiple facilities, seamless scaling, and reduced reliance on on‑premises infrastructure. This shift supports centralized data repositories that improve reporting accuracy and cross‑department visibility for scheduling, payments, and membership management.

Artificial intelligence (AI) is rapidly embedded into core modules, with AI‑assisted scheduling and demand forecasting implemented in approximately 46% of new deployments. These capabilities reduce double‑bookings by up to 35% and optimize staff allocation based on usage patterns and peak hours. AI‑driven analytics also power personalized engagement features—such as automated reminders and customized program recommendations—enhancing user retention metrics by up to 28% in early adopters.

Mobile engagement technology plays a strategic role: over 65% of recreation facilities now offer native mobile applications for reservations, contactless check‑in, and notifications. Mobile platforms accelerate user onboarding and support seamless integration with digital wallets, loyalty programs, and QR‑based access control, which reduces queue times by 22% and increases recurring bookings.

• In August 2024, Active Network completed the acquisition of CivicRec to consolidate its park and recreation management software portfolio and accelerate its cloud‑based offerings for municipal and community recreation operations. This strategic consolidation enhances feature sets for registration, facility scheduling, and CRM across larger user bases.

• In January 2025, Amilia announced a strategic partnership with RecPro to integrate Amilia’s online registration and payment capabilities with RecPro’s facility management ecosystem, enabling seamless experiences for parks and recreation programs and enhancing cross‑platform functionality.

• In March 2025, Kourts launched Kourts Pro, a major product upgrade introducing enhanced court booking, integrated payments, and expanded analytics designed to support courts, gyms, and multi‑use recreation facilities with real‑time scheduling insights.

• In May 2024, Daxko expanded its global presence by establishing Daxko India Technology Solution Pvt. Ltd., aiming to accelerate growth in the Asia‑Pacific market and strengthen its technology support and service delivery within community and fitness recreation facilities.

The Recreation Management Software Market Report provides a comprehensive examination of the global landscape of software solutions designed for planning, organizing, and managing recreational operations across parks, community centers, fitness facilities, aquatic complexes, and private recreation venues. The reporting scope encompasses multiple segmentation dimensions including solution types such as membership management, facility scheduling, program coordination, payment processing, and analytics platforms. Geographic analysis spans North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, detailing regional deployment patterns, adoption drivers, infrastructure trends, and consumer behavior differences in software utilization. Application segments include municipal parks and recreation departments, private fitness and wellness centers, youth and sports programming, and community engagement initiatives, each analyzed for distinct usage profiles and operational priorities.

Technology focus areas within the report include cloud‑native deployments, mobile engagement tools, AI‑driven analytics, IoT integration for resource optimization, interoperability with third‑party systems, and cybersecurity frameworks that ensure data protection and regulatory compliance. The report also highlights market dynamics such as competitive strategies, innovation trends, partnerships, mergers, and expanding service ecosystems that shape vendor positioning and differentiation strategies. Decision‑makers are provided detailed insights into market maturity levels, adoption rates by organization size and end‑user type, and emerging niche opportunities such as virtual programming management and sustainability tracking tools. Additionally, the report considers industry focus areas such as regulatory landscapes, digital transformation mandates, and public‑private investment trends that influence procurement and deployment decisions across global markets. This analytical breadth enables stakeholders to assess strategic priorities, benchmark competitive activity, and align product development with evolving customer needs in the Recreation Management Software domain.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

12.3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Yardi Systems Inc. Homepage, Active Network LLC Website, Legend Recreation Software Inc. Official Site, CivicPlus, PerfectMind Inc., EZFacility Inc., MyREC.Com, RECDESK LLC, EMS Software LLC, Dash Platform, Jarvis Corporation, Daxko, RecTrac, Vermont Systems, InnoSoft Fusion |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |