Reports

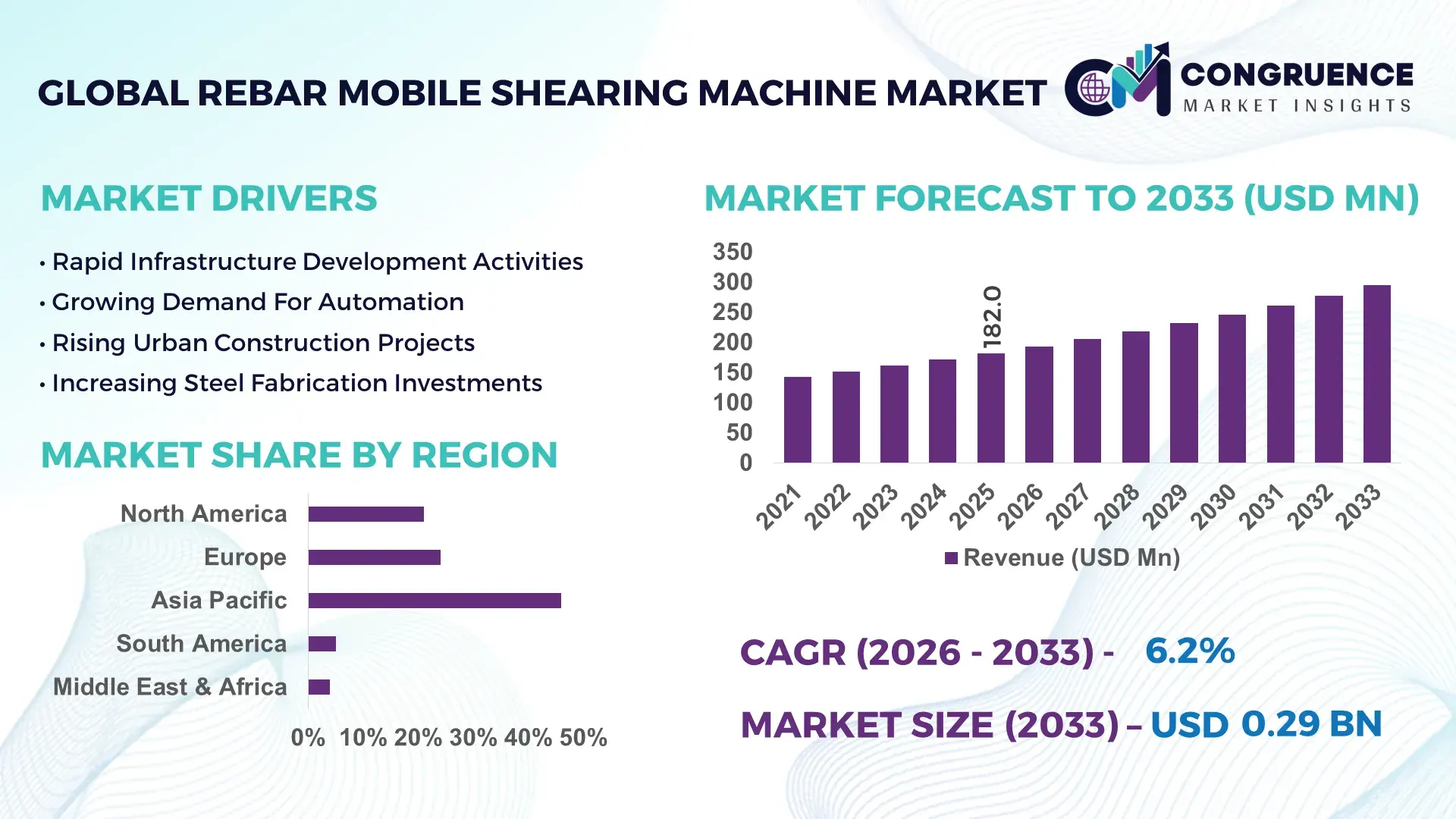

The Global Rebar Mobile Shearing Machine Market was valued at USD 182.0 Million in 2025 and is anticipated to reach a value of USD 294.5 Million by 2033 expanding at a CAGR of 6.2% between 2026 and 2033. Rapid expansion of modular infrastructure projects, automated steel fabrication facilities, and high-speed urban construction is accelerating deployment of advanced mobile shearing systems capable of reducing onsite steel processing time by over 28% compared to stationary alternatives. Between 2024 and 2026, tightening labor availability across major construction economies and rising infrastructure localization policies following Red Sea shipping disruptions have forced contractors to prioritize portable, fuel-efficient, and digitally monitored rebar cutting equipment to maintain project continuity and reduce logistics dependency.

China continues to dominate the global Rebar Mobile Shearing Machine market with approximately 34% manufacturing concentration and over 40% of regional construction steel consumption linked to transportation and smart-city projects. The country allocated more than USD 180 billion toward rail, bridge, and urban redevelopment programs in 2025, while automated rebar processing adoption across tier-1 contractors exceeded 46%, significantly higher than Southeast Asian averages near 24%. In comparison, North America is accelerating premium hydraulic mobile shear deployment due to labor productivity optimization and safety compliance requirements. Increasing integration of IoT-enabled diagnostics, low-emission hydraulic systems, and high-throughput blade assemblies is transforming procurement priorities from low-cost ownership toward lifecycle efficiency and operational flexibility.

This strategic transition is pushing manufacturers to expand localized production, strengthen aftermarket service networks, and prioritize intelligent automation capabilities to secure long-term competitive positioning.

Market Size & Growth: USD 182.0 million in 2025 reaching USD 294.5 million by 2033, driven by automated rebar processing adoption and infrastructure modernization across high-growth construction hubs.

Top Growth Drivers: Infrastructure investment growth exceeded 18%, automated steel processing adoption crossed 31%, and labor-efficiency demand improved operational productivity by 22%.

Short-Term Forecast: By 2028, advanced hydraulic shearing systems are projected to reduce onsite steel processing time by 27% and maintenance downtime by 19%.

Emerging Technologies: AI-assisted diagnostics, IoT-enabled predictive maintenance, and low-emission hydraulic systems improved equipment utilization rates by over 25%.

Regional Leaders: Asia-Pacific holds 46% demand concentration, North America leads smart automation deployment, while Europe advances energy-efficient shearing technologies.

Consumer/End-User Trends: More than 52% of large contractors now prioritize mobile rebar equipment with remote monitoring and rapid deployment capability.

Pilot/Case Example: In 2025, a major urban rail project in China improved steel processing efficiency by 33% using automated mobile shearing fleets.

Competitive Landscape: Leading manufacturers control nearly 38% market share, with firms focusing on automation, hydraulic optimization, and regional expansion strategies.

Regulatory & ESG Impact: Low-emission hydraulic upgrades reduced fuel consumption by 16%, supporting stricter construction-site sustainability compliance requirements.

Investment & Funding: Global infrastructure-linked equipment investments exceeded USD 1.4 billion, accelerating localized manufacturing and service-center expansion.

Innovation & Future Outlook: Smart blade monitoring, compact high-capacity systems, and digitally connected fleet management are redefining advanced construction equipment strategies.

Construction and infrastructure projects account for nearly 48% of total equipment deployment, while transportation and industrial steel fabrication contribute approximately 31% combined demand across the global Rebar Mobile Shearing Machine market. Manufacturers are rapidly integrating sensor-based blade monitoring, automated hydraulic pressure balancing, and low-maintenance cutting systems to improve productivity by over 24%. Asia-Pacific remains the largest consumption hub, whereas North America is accelerating adoption of digitally connected mobile shearing platforms due to workforce shortages and compliance pressures. Growing supply-chain regionalization and stricter construction efficiency benchmarks are pushing contractors toward localized equipment procurement and higher automation intensity, setting the foundation for deeper strategic transformation across the competitive landscape.

The Rebar Mobile Shearing Machine market is rapidly transforming into a strategic battleground for construction equipment manufacturers, infrastructure contractors, and industrial steel processing firms as project timelines tighten and labor productivity becomes a core profitability metric. Large-scale urban redevelopment, transportation corridors, and industrial expansion programs are accelerating demand for high-mobility steel processing systems capable of reducing manual intervention while improving onsite execution speed. Global contractors are increasingly prioritizing portable, digitally integrated rebar shearing equipment to optimize steel handling efficiency across decentralized construction environments.

Rising steel logistics volatility, supply-chain restructuring after Red Sea shipping disruptions, and stricter construction safety mandates are forcing companies to shift toward localized and automation-driven equipment deployment models. AI-enabled hydraulic monitoring systems now improve cutting efficiency by 29% while reducing maintenance costs by 21% compared to legacy diesel-powered manual systems. Asia-Pacific leads in production volume with nearly 46% market concentration due to large infrastructure pipelines and localized manufacturing ecosystems, while North America leads in intelligent automation adoption with over 39% penetration among large contractors deploying connected equipment fleets.

Over the next two to three years, contractors integrating automated mobile shearing systems are expected to improve onsite steel processing throughput by 26% and reduce idle equipment time by 18%. ESG-focused construction practices are also emerging as a competitive advantage, as low-emission hydraulic technologies reduce fuel consumption by nearly 15% while supporting compliance with tightening environmental regulations across Europe and North America. In 2025, a smart transportation infrastructure project in Eastern China improved reinforcement steel preparation efficiency by 32% through synchronized deployment of digitally monitored mobile shearing units.

Manufacturers are aggressively reallocating capital toward compact high-output systems, predictive maintenance platforms, and regional assembly expansion to strengthen aftermarket responsiveness and reduce delivery cycles. Strategic partnerships between equipment providers and infrastructure contractors are accelerating product customization, fleet digitization, and long-term service agreements. As construction execution increasingly depends on automation, mobility, and operational precision, companies that optimize intelligent processing capabilities and regional deployment strategies will secure stronger competitive positioning in the evolving global Rebar Mobile Shearing Machine market.

The Rebar Mobile Shearing Machine market is being reshaped by accelerating infrastructure modernization, increasing automation in steel processing operations, and growing demand for portable high-efficiency construction equipment. Contractors are shifting from fixed cutting systems toward mobile hydraulic shearing platforms capable of reducing steel handling time, minimizing transportation dependency, and improving project-site flexibility. Infrastructure-intensive sectors including transportation, industrial construction, urban redevelopment, and energy projects are driving deployment across both developed and emerging economies. More than 44% of large construction firms are integrating digitally monitored rebar processing systems to improve workflow consistency and reduce material wastage. At the same time, global supply-chain restructuring and rising labor shortages are increasing pressure on contractors to optimize operational productivity. Manufacturers are responding through localized production expansion, compact equipment innovation, and integration of predictive maintenance technologies. Advanced blade systems and automated hydraulic controls are improving operational efficiency by over 25%, while stricter environmental compliance standards are accelerating demand for low-emission mobile shearing equipment. The market is increasingly defined by strategic competition around automation capability, equipment durability, lifecycle cost optimization, and regional deployment scalability.

Rapid infrastructure expansion combined with labor productivity pressure is accelerating adoption of mobile rebar shearing systems across transportation, industrial, and urban development projects. Automated steel processing deployment among large contractors increased by nearly 31% between 2023 and 2025 as firms prioritized operational speed and reduced dependency on manual cutting operations. Mobile hydraulic shearing equipment improves onsite reinforcement preparation efficiency by approximately 28% while lowering material handling delays by 19%, creating measurable project execution advantages. Following global supply-chain disruptions and rising shipping costs, contractors increasingly favor portable localized steel processing instead of centralized fabrication dependency. This structural shift is forcing manufacturers to expand regional assembly operations and strengthen service accessibility closer to infrastructure corridors. Asia-Pacific infrastructure investments linked to rail and smart-city development continue driving large-scale procurement, while North American contractors are accelerating adoption of digitally monitored cutting systems to address labor shortages and compliance requirements. Equipment manufacturers are responding through automation-focused product launches, strategic partnerships with construction firms, and increased investment in compact high-output hydraulic systems designed for high-frequency deployment environments.

Volatility in steel prices, hydraulic component costs, and industrial equipment logistics is constraining operational scalability across the Rebar Mobile Shearing Machine market. Global steel price fluctuations exceeded 18% during recent infrastructure procurement cycles, directly impacting equipment manufacturing costs and contractor capital allocation decisions. Hydraulic system components sourced from concentrated industrial supply hubs experienced delivery delays of nearly 22% following ongoing geopolitical shipping disruptions and regional trade bottlenecks. Smaller contractors remain highly exposed to financing pressure as advanced automated mobile shearing systems require substantially higher upfront investment than conventional cutting alternatives. These structural limitations are increasing project execution risk, particularly in emerging markets with inconsistent infrastructure financing and fragmented equipment distribution networks. Delayed component procurement and rising maintenance costs are also affecting fleet utilization rates and operational predictability. In response, manufacturers are diversifying supplier bases, negotiating long-term material contracts, and expanding localized spare-part inventories to reduce dependency on cross-border logistics. Several companies are additionally investing in modular hydraulic architectures and alternative component sourcing strategies to improve production flexibility and protect margins against ongoing industrial cost pressure.

The rapid emergence of digitally integrated construction ecosystems is creating substantial expansion opportunities for advanced Rebar Mobile Shearing Machine manufacturers. Smart construction deployment across major infrastructure projects increased by nearly 34% between 2024 and 2026, driving demand for connected equipment capable of real-time monitoring, predictive maintenance, and synchronized steel processing workflows. IoT-enabled hydraulic systems are improving equipment uptime by approximately 27% while reducing maintenance intervention frequency by 18%, creating strong operational incentives for contractors managing multi-site projects. Emerging economies are also generating new demand pockets as urbanization, industrial corridor expansion, and localized steel fabrication investments accelerate. Compact high-capacity mobile shearing systems are gaining traction among mid-sized contractors due to lower transportation dependency and faster deployment flexibility. Companies are positioning aggressively through R&D investments in AI-assisted diagnostics, remote fleet management platforms, and energy-efficient hydraulic technologies. Several manufacturers are building ecosystem partnerships with infrastructure developers, digital construction software providers, and industrial automation firms to capture long-term service opportunities and strengthen competitive differentiation as intelligent construction execution becomes an industry standard.

Execution complexity, workforce capability gaps, and equipment integration limitations remain major challenges affecting long-term scalability within the Rebar Mobile Shearing Machine market. More than 37% of contractors operating advanced automated systems continue facing skilled technician shortages, reducing effective utilization of digitally connected hydraulic equipment. Inconsistent infrastructure power availability and limited service accessibility in developing regions are also constraining deployment consistency for high-output mobile shearing fleets. Equipment downtime linked to hydraulic maintenance and blade replacement can reduce operational efficiency by nearly 16% during high-volume infrastructure cycles. At the same time, tightening environmental standards and project compliance requirements are forcing manufacturers to redesign systems for lower emissions, reduced noise levels, and higher energy efficiency without compromising processing speed. This increases engineering complexity and production costs. Companies that fail to optimize service reliability, digital integration capability, and lifecycle maintenance efficiency risk losing competitiveness as contractors increasingly prioritize uptime guarantees and operational predictability. To remain competitive, manufacturers are accelerating investment in workforce training, predictive diagnostics, regional service partnerships, and modular equipment architectures capable of supporting scalable long-term deployment across diverse infrastructure environments.

32% Increase in Automated Hydraulic System Deployment Across Infrastructure Projects Advanced hydraulic automation is reshaping onsite steel processing operations as contractors prioritize faster execution and lower labor dependency. Automated blade pressure balancing improved cutting precision by 24%, while intelligent monitoring systems reduced unplanned downtime by 18%. Manufacturers are scaling compact mobile units with integrated diagnostics to support large transportation and urban redevelopment projects amid rising construction labor shortages.

28% Growth in IoT-Enabled Fleet Monitoring Adoption Among Large Contractors Construction firms are rapidly integrating connected equipment management platforms to optimize fleet utilization and maintenance scheduling. Remote diagnostics reduced service response time by 21%, while predictive maintenance algorithms improved equipment availability by 26%. Companies are restructuring aftermarket strategies around subscription-based monitoring services and digitally integrated support ecosystems to improve customer retention and operational visibility.

41% Expansion in Localized Manufacturing and Regional Assembly Operations Supply-chain instability and geopolitical shipping disruptions are forcing manufacturers to regionalize production and spare-part distribution. Asia-Pacific equipment assembly capacity expanded significantly, while North American firms accelerated localized sourcing to reduce delivery lead times by nearly 19%. This operational restructuring is redefining procurement priorities from low-cost imports toward supply reliability, faster servicing, and deployment flexibility.

24% Shift Toward Low-Emission and Energy-Efficient Mobile Shearing Systems Environmental compliance requirements and rising fuel costs are accelerating transition toward energy-optimized hydraulic equipment. Low-emission systems reduced fuel consumption by approximately 15% while improving operational efficiency in high-frequency cutting environments. Companies are increasingly forming technology partnerships to develop quieter, compact, and digitally optimized equipment platforms capable of meeting stricter sustainability standards without sacrificing processing performance.

The Rebar Mobile Shearing Machine market is segmented by type, application, and end-user, with demand increasingly concentrated around high-efficiency automated systems and infrastructure-intensive deployment environments. Hydraulic mobile shearing machines continue dominating adoption due to superior cutting force, operational durability, and compatibility with large-scale construction workflows. Infrastructure and transportation projects collectively account for over 45% of equipment utilization as contractors prioritize faster reinforcement processing and decentralized steel handling capabilities. Demand is also shifting toward intelligent mobile systems equipped with predictive diagnostics and fuel-efficient hydraulic mechanisms to reduce downtime and improve project execution consistency. Across applications, industrial construction and urban infrastructure remain core deployment sectors, while renewable energy and smart-city projects are emerging as high-growth demand pockets. Large construction contractors continue representing the dominant end-user category due to higher fleet requirements and automation investment capacity. However, mid-sized regional fabricators are accelerating adoption of compact mobile units to improve flexibility and reduce dependency on centralized steel processing facilities. This segmentation evolution highlights a clear strategic transition toward mobility, digital integration, and operational efficiency across the global Rebar Mobile Shearing Machine market.

Hydraulic Rebar Mobile Shearing Machines dominate the market with approximately 58% share due to their superior cutting capacity, high operational stability, and ability to process thick reinforcement steel with lower vibration impact. Large infrastructure contractors increasingly prioritize hydraulic systems because they improve cutting efficiency by nearly 29% and support continuous high-volume deployment across transportation and industrial construction projects. In contrast, electric and semi-automatic mobile shearing machines are emerging as the fastest-growing category, expanding adoption by over 24% due to lower maintenance requirements, reduced emissions, and improved energy efficiency in urban construction environments. The market is witnessing a clear transition from conventional diesel-powered manual systems toward digitally integrated hydraulic and electric platforms capable of remote diagnostics and automated pressure balancing. Hydraulic systems maintain dominance in heavy-duty projects, whereas electric variants are rapidly gaining traction in compact urban infrastructure applications where mobility and compliance are critical. Remaining machine categories collectively account for nearly 18% market share and continue serving niche demand in low-volume fabrication and regional construction activities. Manufacturers are responding through product diversification, modular system development, and expanded regional assembly operations to capture both high-capacity industrial demand and fast-growing smart construction opportunities.

• According to a 2025 report by the International Federation of Robotics, automated hydraulic steel-processing systems were adopted by over 43% of large infrastructure contractors, resulting in nearly 27% improvement in operational efficiency and lower material handling downtime, reinforcing their growing strategic importance.

Infrastructure construction remains the leading application segment with nearly 42% market share, driven by large-scale transportation corridors, bridge expansion projects, and urban redevelopment programs requiring high-frequency reinforcement steel processing. Contractors operating within this segment increasingly deploy advanced mobile shearing systems to reduce steel preparation delays by approximately 26% and improve onsite workflow continuity. Industrial construction is emerging as the fastest-growing application category, recording adoption growth exceeding 23% as manufacturing plants, logistics facilities, and energy infrastructure projects accelerate automation-focused steel fabrication practices. A clear distinction is developing between mature infrastructure applications emphasizing operational reliability and emerging industrial deployments prioritizing speed, mobility, and digitally integrated equipment management. Commercial construction and regional fabrication projects collectively contribute around 35% of total application demand and remain strategically important for compact and mid-capacity equipment suppliers. Usage behavior is evolving rapidly as contractors favor mobile processing solutions over centralized steel preparation due to labor shortages and increasing transportation inefficiencies. Equipment manufacturers are responding by expanding smart hydraulic product portfolios, improving deployment flexibility, and integrating remote monitoring capabilities tailored to infrastructure-intensive and industrial project requirements.

• According to a 2025 report by the International Construction Equipment Association, mobile steel processing systems were deployed across more than 18,000 infrastructure and industrial construction projects, improving reinforcement preparation efficiency by 31%, highlighting their rapid operational adoption.

Large construction contractors account for approximately 49% of total market demand due to extensive equipment fleets, high-volume reinforcement processing requirements, and stronger investment capacity for advanced hydraulic automation systems. These organizations prioritize operational uptime, cutting precision, and lifecycle efficiency to maintain competitiveness across transportation, industrial, and urban infrastructure projects. Mid-sized regional construction firms represent the fastest-growing end-user segment, with adoption increasing by nearly 25% as localized infrastructure investments and decentralized steel fabrication practices expand across emerging economies. The purchasing behavior between established enterprise contractors and regional operators differs significantly. Large contractors increasingly favor digitally integrated equipment with predictive maintenance capabilities, while smaller firms prioritize compact mobility, lower operating costs, and deployment flexibility. Fabrication workshops and independent steel processing operators collectively account for around 29% of market demand, serving niche and project-specific reinforcement preparation requirements. Manufacturers are strategically targeting these segments through customized financing models, regional service partnerships, and modular product configurations designed to optimize operational scalability. This shift indicates that future competitive advantage will increasingly depend on balancing high-capacity industrial performance with affordable, adaptable mobile solutions tailored to diverse end-user requirements.

• According to a 2025 report by the Global Construction Technology Council, adoption among mid-sized construction contractors increased by 28%, with over 11,500 firms implementing mobile hydraulic steel-processing equipment, leading to nearly 22% productivity improvement and reduced onsite labor dependency, indicating a strong shift in demand dynamics.

Asia-Pacific accounted for the largest market share at 46% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 7.1% between 2026 and 2033.

Asia-Pacific continues dominating global demand due to large-scale infrastructure investments, localized manufacturing ecosystems, and high construction steel consumption across China, India, and Southeast Asia. Europe maintains nearly 24% market share, driven by sustainability-focused equipment upgrades and stricter operational efficiency regulations, while North America accounts for approximately 21% demand concentration through accelerating automation deployment and labor optimization initiatives. South America and the Middle East & Africa collectively contribute 9% market share, supported by industrial expansion and transportation infrastructure development. Ongoing supply-chain regionalization and infrastructure modernization are pushing manufacturers to prioritize localized assembly, service expansion, and intelligent equipment deployment across high-growth regional construction corridors.

North America represents approximately 21% of global Rebar Mobile Shearing Machine demand, supported by rising infrastructure modernization, transportation corridor upgrades, and industrial construction expansion across the United States and Canada. Large contractors are increasingly deploying automated hydraulic systems to reduce reinforcement processing time by nearly 27% and address persistent construction labor shortages. Tightening workplace safety regulations and pressure to improve project execution speed are accelerating adoption of digitally monitored mobile shearing equipment with predictive maintenance capability. More than 39% of large construction firms now prioritize connected steel-processing fleets to optimize operational efficiency and minimize downtime. Manufacturers are expanding regional service centers and localized assembly operations to shorten delivery cycles and strengthen aftermarket responsiveness. The region remains strategically important due to its rapid automation adoption and strong preference for premium high-productivity construction equipment platforms.

Europe accounts for nearly 24% of the global Rebar Mobile Shearing Machine market, led by Germany, France, and Italy where infrastructure renovation and industrial modernization projects continue accelerating advanced equipment demand. Stricter emission regulations and carbon-reduction mandates are forcing contractors to replace conventional diesel-powered systems with energy-efficient hydraulic and electric mobile shearing platforms. Low-emission equipment adoption improved by approximately 26% between 2024 and 2025 as compliance-driven procurement became a dominant purchasing factor. Construction enterprises increasingly prioritize precision-focused, digitally integrated systems capable of improving material utilization and reducing operational waste. Several manufacturers expanded compact electric equipment portfolios and regional service partnerships to support evolving ESG requirements. Europe continues forcing innovation through regulatory intensity, making the region strategically critical for manufacturers investing in sustainable, intelligent, and compliance-ready steel processing technologies.

Asia-Pacific dominates the global Rebar Mobile Shearing Machine market with nearly 46% demand concentration, supported by massive infrastructure expansion across China, India, Japan, and Southeast Asia. The region benefits from strong localized manufacturing capacity, lower production costs, and large-scale transportation and urban development projects requiring continuous reinforcement steel processing. Automated mobile shearing system deployment across major contractors increased by over 33% as infrastructure timelines tightened and decentralized construction practices expanded. China alone contributes more than 34% of global manufacturing activity linked to mobile steel-processing equipment. Regional enterprises prioritize scalability, rapid deployment, and cost-efficient processing speed over premium customization, driving strong demand for high-output hydraulic systems. Manufacturers continue expanding assembly capacity, localized distribution, and digital equipment integration to capitalize on accelerating infrastructure and industrial construction activity throughout the region.

South America contributes approximately 5% of global Rebar Mobile Shearing Machine demand, with Brazil and Argentina leading regional infrastructure and industrial construction activity. Transportation modernization, mining-related construction, and urban redevelopment projects are driving gradual adoption of mobile steel processing systems capable of improving onsite operational flexibility. However, fluctuating financing conditions, import dependency, and equipment affordability constraints continue limiting large-scale automation deployment. More than 31% of regional contractors remain highly price-sensitive, prioritizing durable mid-capacity systems with lower maintenance costs over premium digitally integrated platforms. Despite these constraints, localized adoption of compact hydraulic shearing equipment improved by nearly 18% as construction firms sought to reduce project delays and transportation inefficiencies. The region presents a balanced opportunity-risk environment where companies focusing on affordability, regional partnerships, and service accessibility are gaining stronger competitive traction.

The Middle East & Africa region accounts for nearly 4% of global market demand, supported by rapid infrastructure expansion across the UAE, Saudi Arabia, and South Africa. Large-scale transportation corridors, industrial facilities, and smart-city projects are accelerating deployment of high-capacity mobile shearing equipment designed for continuous reinforcement processing in complex construction environments. Government-backed modernization programs and industrial diversification strategies increased infrastructure equipment procurement activity by approximately 22% during recent project cycles. Contractors are increasingly adopting automated hydraulic systems to improve processing speed, reduce labor dependency, and support large-volume project execution. Regional enterprises prioritize operational durability and deployment reliability due to demanding construction conditions and long project timelines. Manufacturers expanding regional partnerships, service infrastructure, and localized equipment support capabilities are strengthening their strategic positioning across this rapidly transforming infrastructure landscape.

China – 34% Market share: dominates due to massive infrastructure investment, high construction steel consumption, and strong localized manufacturing capacity supporting large-scale deployment.

United States – 18% Market share: leads in advanced automation adoption driven by labor productivity optimization, infrastructure modernization programs, and rising deployment of digitally connected mobile steel-processing systems.

The Rebar Mobile Shearing Machine market is characterized by intense competition between global automation leaders, regional hydraulic equipment manufacturers, and cost-focused fabrication machinery suppliers. Companies such as Schnell Group, DARHUNG Machinery, KRB Machinery, EVG, TJK Machinery, and Consolidated Machines are competing aggressively across infrastructure automation, precision cutting efficiency, and localized service expansion. The top five players collectively control approximately 43% of global market activity, with European firms dominating intelligent automation while Asian manufacturers compete aggressively on cost efficiency and production scalability.

Competition is increasingly centered on automation capability, lifecycle operating cost, deployment speed, and hydraulic system durability. Advanced servo-controlled systems improve processing efficiency by nearly 29%, while predictive maintenance integration reduces downtime by 18%, forcing manufacturers to accelerate digital equipment innovation. Regional firms are expanding through distributor partnerships, localized assembly, and aftermarket service integration to reduce lead times by over 20%. The market is also witnessing a competitive shift toward vertically integrated processing ecosystems combining cutting, bending, and digital workflow management. High engineering complexity, strong contractor relationships, and service-network dependency remain major entry barriers. Winning in this market increasingly requires automation leadership, regional execution capability, and operational reliability rather than price competition alone.

DARHUNG Machinery

KRB Machinery

EVG Entwicklungs- und Verwertungs-Gesellschaft m.b.H.

TJK Machinery (Tianjin) Co., Ltd.

Consolidated Machines

TOYO Kensetsu Kohki Co., Ltd.

Jaypee India Limited

Gensco Equipment

Schnell India Machinery Pvt. Ltd.

PEDAX GmbH

MEP Group

Progress Group

Ellsen Machinery Equipment Co., Ltd.

The Rebar Mobile Shearing Machine market is rapidly transitioning from conventional hydraulic cutting systems toward digitally integrated, automation-driven processing platforms. Advanced servo-controlled hydraulic systems now improve cutting precision by nearly 31% while reducing blade wear and maintenance frequency by approximately 19% compared to legacy mechanical shearing equipment. More than 42% of large infrastructure contractors are integrating digitally monitored mobile processing systems to optimize reinforcement handling efficiency and reduce project delays.

IoT-enabled predictive maintenance technologies are becoming a critical competitive differentiator across high-volume construction environments. Connected diagnostic systems improve equipment uptime by nearly 27% through real-time pressure monitoring, automated maintenance alerts, and remote fleet tracking capabilities. Manufacturers deploying intelligent monitoring platforms are gaining stronger aftermarket retention and operational visibility advantages, particularly across North America and Europe where construction firms increasingly prioritize lifecycle efficiency and downtime reduction.

Electric and low-emission hydraulic systems are also reshaping equipment innovation strategies as sustainability compliance tightens across major infrastructure markets. New-generation electric-hydraulic systems reduce fuel consumption by nearly 16% while lowering operational noise levels in urban deployment zones. Compared to conventional diesel-powered systems, automated hybrid platforms improve energy efficiency by over 24% and support stricter environmental standards. Companies investing aggressively in compact AI-assisted diagnostics, smart blade calibration, and remote equipment synchronization between 2026 and 2028 are expected to secure stronger positioning as intelligent construction ecosystems continue accelerating globally.

February 2026 – Schnell Group introduced the upgraded Graphico Pro intelligent production management platform designed for automated rebar processing plants, enabling real-time workflow optimization and waste reduction across digitally connected steel-processing lines. The platform improved production visibility and material utilization efficiency by nearly 25%. [Digital Workflow Shift] Source: www.schnellgroup.com

October 2025 – Schnell Group launched the Opera 16 high-flexibility stirrup bender integrated with advanced automation architecture for faster reinforcement steel processing. The new system enhanced operational productivity and reduced manual intervention across automated fabrication facilities, strengthening the company’s position in intelligent construction manufacturing. [Flexible Automation Push]

July 2025 – Schnell Group highlighted deployment of artificial intelligence and advanced sensor technologies within automated steel-processing environments, accelerating predictive monitoring and process optimization capabilities. The integration reduced operational inefficiencies and supported higher automation continuity across modern reinforcement production plants. [AI Sensor Integration]

2025 – DARHUNG Machinery expanded promotion of its fully customized automated rebar shearing production lines capable of servo-controlled cutting, sorting, transportation, and discharge processing. The company highlighted operations across 26 international markets while maintaining nearly 92% market share within Taiwan’s reinforcement steel processing machinery sector. [Global Expansion Drive]

The Rebar Mobile Shearing Machine Market Report delivers comprehensive coverage across product categories, operational technologies, deployment applications, end-user industries, and regional demand ecosystems shaping the global construction equipment landscape. The report evaluates hydraulic, electric, semi-automatic, and automated mobile shearing systems across infrastructure construction, industrial fabrication, transportation projects, commercial development, and steel processing operations. It further analyzes adoption trends across large contractors, regional construction firms, and independent fabrication facilities operating within North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

The study incorporates detailed assessment of more than 20 strategic market indicators including equipment automation penetration, regional production concentration, infrastructure deployment intensity, operational efficiency gains, and contractor purchasing behavior. Over 42% of large infrastructure firms now prioritize digitally integrated steel-processing systems, while low-emission hydraulic equipment adoption has surpassed 26% across compliance-driven construction markets. The report also examines emerging technologies including AI-assisted diagnostics, predictive maintenance systems, compact electric-hydraulic platforms, and IoT-enabled fleet management solutions expected to reshape competitive dynamics between 2026 and 2033.

In addition to competitive benchmarking and regional execution analysis, the report provides strategic insight supporting investment prioritization, market expansion planning, technology adoption decisions, and supply-chain optimization strategies for manufacturers, contractors, equipment distributors, and infrastructure stakeholders operating within the evolving global Rebar Mobile Shearing Machine market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 182.0 Million |

| Market Revenue (2033) | USD 294.5 Million |

| CAGR (2026–2033) | 6.2% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Schnell Group; DARHUNG Machinery; KRB Machinery; EVG Entwicklungs- und Verwertungs-Gesellschaft m.b.H.; TJK Machinery (Tianjin) Co., Ltd.; Consolidated Machines; TOYO Kensetsu Kohki Co., Ltd.; Jaypee India Limited; Gensco Equipment; Schnell India Machinery Pvt. Ltd.; PEDAX GmbH; MEP Group; Progress Group; Ellsen Machinery Equipment Co., Ltd. |

| Customization & Pricing | Available on Request (10% Customization Free) |