Reports

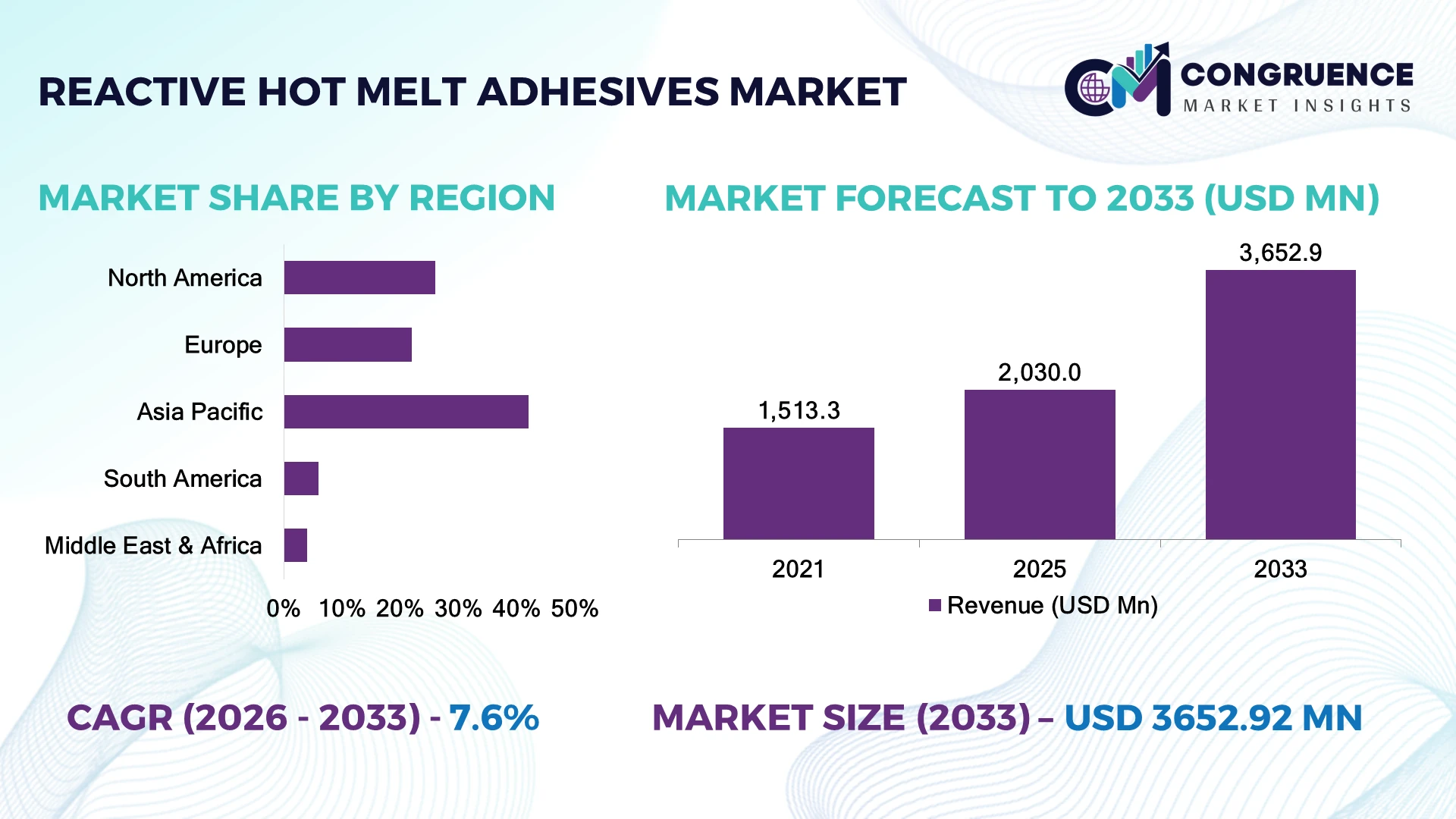

The Global Reactive Hot Melt Adhesives Market was valued at USD 2,030.0 Million in 2025 and is anticipated to reach a value of USD 3,652.9 Million by 2033 expanding at a CAGR of 7.62% between 2026 and 2033. Growth is driven by rising adoption of moisture-curing polyurethane hot melts in automotive lightweighting, electronics assembly, and sustainable packaging applications requiring stronger bonding performance with reduced solvent emissions.

China dominates the market with approximately 32% share, supported by large-scale packaging, automotive, and electronics manufacturing capacity, while investments in advanced adhesive production facilities exceeded USD 1 billion across chemical clusters. The country’s electronics sector uses reactive hot melts in over 40% of new high-performance assembly applications, compared with Europe’s higher adoption in sustainable packaging and construction solutions.

The European Union’s stricter VOC regulations are accelerating solvent-free adhesive transitions, creating strategic opportunities for manufacturers to expand advanced formulation capabilities and regional production networks.

Market Size & Growth: USD 2.03 Billion (2025) to USD 3.65 Billion (2033) at 7.62% CAGR, driven by solvent-free bonding technologies and lightweight material adoption.

Top Growth Drivers: Automotive lightweighting (35%), sustainable packaging conversion (30%), electronics miniaturization (25%) are leading demand catalysts.

Short-Term Forecast: By 2028, automated adhesive dispensing systems improve production efficiency by 20% and reduce material waste by 15%.

Emerging Technologies: Advanced polyurethane formulations, AI-controlled adhesive application, and smart curing technologies are reshaping industrial bonding.

Regional Leaders: Asia Pacific reaches USD 1.8 Billion with electronics expansion; Europe reaches USD 950 Million with ESG-driven adoption; North America reaches USD 720 Million through automotive innovation.

Consumer/End-User Trends: Over 45% of packaging manufacturers prioritize solvent-free adhesive solutions for recyclable product designs.

Pilot/Case Example: A 2024 automotive bonding project achieved 18% weight reduction and improved assembly cycle efficiency through reactive hot melt integration.

Competitive Landscape: Henkel leads with approximately 20% share, followed by H.B. Fuller, Arkema, 3M, and Sika in global adhesive markets.

Regulatory & ESG Impact: EU sustainability policies are accelerating adoption, with solvent-free technologies reducing VOC emissions by more than 90%.

Investment & Funding: Over USD 800 Million invested in adhesive innovation, regional plants, and sustainable material partnerships.

Innovation & Future Outlook: Next-generation bio-based polymers, recyclable bonding systems, and digital manufacturing integration are becoming strategic priorities.

Reactive Hot Melt Adhesives are gaining importance across automotive interiors, flexible packaging, footwear, electronics, and construction sectors due to their rapid curing capability and high durability. Manufacturers are increasingly developing bio-based and recyclable formulations, with more than 30% of new adhesive product launches focusing on sustainability improvements. Supply-chain diversification after recent global disruptions is encouraging regional production expansion and localized chemical manufacturing strategies.

Reactive Hot Melt Adhesives are becoming strategically important as industries transition toward lightweight materials, faster manufacturing cycles, and environmentally responsible bonding technologies. Automotive, electronics, and packaging manufacturers are restructuring supply chains to secure advanced adhesive materials closer to production hubs, while regulatory pressure on VOC reduction is accelerating solvent-free technology adoption.

Compared with traditional solvent-based adhesives, modern reactive hot melts provide up to 40% faster processing speeds and significantly lower emissions while maintaining strong adhesion on complex substrates. Asia Pacific leads in manufacturing scale, particularly through China, Japan, and South Korea’s electronics and automotive ecosystems, whereas Europe emphasizes sustainable formulations driven by regulatory frameworks and circular economy initiatives.

Over the next 2–3 years, manufacturers are expected to increase automated adhesive application systems, improving production consistency and reducing operational losses. Automotive suppliers are deploying reactive hot melts for lightweight interior components, battery assemblies, and composite structures to enhance efficiency. Companies are prioritizing strategic partnerships, regional manufacturing expansion, and material innovation to strengthen competitive positioning. Long-term success will depend on balancing performance, sustainability, and supply-chain resilience in high-value industrial applications.

The transition toward lightweight materials, recyclable packaging, and solvent-free manufacturing is accelerating reactive hot melt adhesive adoption across automotive, electronics, and industrial applications. Automotive manufacturers in Germany and China are increasing polyurethane hot melt usage as composite component adoption rises by over 25%, improving bonding strength and assembly efficiency. More than 60% of new packaging developments prioritize low-emission adhesive systems due to sustainability regulations. Companies are responding through expanded production capacity, bio-based formulation investments, and partnerships with material suppliers to support faster curing, reduced energy consumption, and improved production reliability across advanced manufacturing environments.

Reactive hot melt adhesive manufacturers face pressure from fluctuating polyurethane, isocyanate, and polymer feedstock costs, with raw material price swings exceeding 15% during recent supply disruptions. Dependence on specialized chemical suppliers in China, Germany, and South Korea creates procurement risks for global manufacturers. Regulatory compliance requirements for chemical handling and formulation safety increase operational complexity, particularly in Europe where stricter chemical policies influence product development. These constraints impact margins and production scalability, prompting companies to diversify suppliers, establish localized manufacturing networks, and secure long-term material contracts to stabilize costs and improve supply continuity.

Growing demand for recyclable packaging, electric vehicle components, and automated assembly systems is creating new opportunities for reactive hot melt adhesive producers. Bio-based adhesive formulations are gaining traction, with sustainable material adoption increasing by nearly 30% among packaging innovators. Japan and South Korea are expanding advanced electronics manufacturing, creating demand for precision bonding solutions with improved thermal resistance. Digital dispensing technologies and automated quality monitoring systems are improving adhesive utilization efficiency by approximately 20%. Companies are strengthening R&D pipelines, forming technology partnerships, and developing customized formulations for high-growth applications such as battery systems, medical devices, and lightweight composite structures.

Scaling reactive hot melt adhesive technologies across diverse industrial environments remains challenging due to formulation complexity, equipment compatibility issues, and skilled workforce requirements. Approximately 35% of manufacturers report difficulties integrating advanced adhesive systems into existing production lines without process modifications. Battery manufacturing and electronics assembly require tighter performance controls, with temperature and curing consistency becoming critical operational factors. Companies in the United States and China are investing in automation, application engineering teams, and collaborative testing facilities to overcome deployment barriers. Long-term competitiveness depends on improving process standardization, reducing integration complexity, and ensuring reliable performance across evolving industrial applications.

Bio-Based Adhesive Transition: Manufacturers are accelerating development of bio-derived reactive hot melts as sustainability targets reshape industrial procurement. Adoption of low-emission adhesive systems has increased by around 30% among packaging innovators, while over 40% of European manufacturers are evaluating renewable raw material options. Companies are expanding green chemistry partnerships and reformulating products to meet stricter environmental requirements, particularly after the European Union’s circular economy initiatives increased pressure on material suppliers.

Automated Bonding Integration: Advanced dispensing automation is transforming adhesive application workflows, with smart monitoring systems improving material utilization by approximately 20% and reducing production inconsistencies by nearly 15%. Automotive and electronics manufacturers in Germany, Japan, and China are integrating robotic adhesive systems to address labor shortages and improve precision. Companies are investing in connected equipment, digital process controls, and customized application solutions to optimize high-volume manufacturing.

Battery Assembly Expansion: Electric vehicle production is creating new demand patterns for reactive hot melts in battery modules, thermal management components, and lightweight interiors. Battery manufacturers are increasing adhesive-based assembly approaches, with over 25% growth in advanced bonding applications for EV-related components. Companies are forming partnerships with automotive suppliers to develop heat-resistant formulations that support safer and more efficient vehicle production.

Regional Production Localization: Supply-chain restructuring is encouraging adhesive producers to establish localized manufacturing and storage facilities closer to industrial customers. Nearly 35% of global chemical manufacturers have increased regional sourcing strategies following logistics disruptions. Companies are expanding plants in China, India, and the United States to reduce dependency risks, shorten delivery timelines, and improve responsiveness for customized industrial applications.

Polyurethane reactive hot melt adhesives represent the leading segment, accounting for approximately 65% of market adoption due to superior bonding strength, moisture resistance, and compatibility with diverse substrates. Their extensive use in automotive interiors, furniture, packaging, and electronics manufacturing has strengthened their position as the preferred high-performance adhesive solution. Silicone-based and other reactive hot melt variants maintain niche relevance in specialized applications requiring extreme temperature resistance and flexibility, collectively supporting around 20% of industrial demand. The fastest-growing shift is toward bio-based and advanced polyurethane formulations, supported by sustainability requirements and demand for recyclable materials. Adoption of environmentally optimized formulations is increasing by nearly 30% among packaging and consumer goods manufacturers. Companies are prioritizing R&D investments, expanding formulation capabilities, and partnering with chemical suppliers to improve curing speed, reduce emissions, and develop customized adhesive systems for next-generation manufacturing.

Packaging remains the largest application segment, contributing approximately 38% of reactive hot melt adhesive consumption due to demand from flexible packaging, labeling, and carton sealing operations. Rapid curing, improved line speeds, and compatibility with recyclable substrates make reactive hot melts increasingly important for modern packaging workflows. Automotive assembly and electronics manufacturing represent significant growth areas, together accounting for nearly 35% of demand as lightweight materials and precision bonding requirements increase. The fastest-growing application area is electric vehicle and electronics assembly, where advanced adhesives support miniaturization, thermal management, and structural bonding requirements. Adoption in EV-related applications is expanding by more than 25% as manufacturers replace mechanical fastening methods. Companies are adapting through automation integration, application-specific formulations, and partnerships with OEMs to strengthen positioning in high-value industrial segments.

Industrial manufacturers represent the dominant end-user segment, holding approximately 45% market share due to large-scale consumption across automotive, packaging, furniture, and electronics production facilities. Their demand concentration is driven by continuous manufacturing operations, strict quality requirements, and the need for efficient bonding solutions. Packaging companies and automotive suppliers remain established buyers, while electronics and EV manufacturers are emerging as faster-growing users due to advanced material integration. The fastest-growing end-user group is electric vehicle and electronics manufacturers, with adoption increasing by nearly 30% as companies shift toward lightweight assemblies and automated production. Small and medium manufacturers are also adopting reactive hot melts to improve productivity and reduce process complexity. Adhesive producers are responding through customized solutions, technical support programs, and strategic partnerships with equipment manufacturers to expand industrial adoption.

Asia-Pacific accounted for the largest market share at 42% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 8.1% between 2026 and 2033.

North America holds approximately 26% of the global reactive hot melt adhesives market, supported by strong automotive, electronics, packaging, and construction manufacturing bases. The United States remains the primary contributor due to rising adoption of solvent-free bonding technologies and automated production systems. Automotive suppliers are increasingly integrating reactive hot melts into lightweight component assembly, while packaging manufacturers are transitioning toward recyclable materials. More than 35% of large manufacturers in the region are increasing investments in automated adhesive application equipment to improve production consistency. Companies are expanding local production capacity, developing customized formulations, and partnering with OEMs to strengthen supply reliability and application expertise.

United States Market Outlook: The United States leads regional adoption through advanced automotive, aerospace, electronics, and packaging industries. The country accounts for a significant share of North American demand, with over 40% of industrial adhesive users prioritizing high-performance bonding solutions for automated manufacturing processes. Strong R&D capabilities and investments in domestic chemical production are supporting innovation in polyurethane reactive hot melt technologies.

Europe represents around 22% of the global reactive hot melt adhesives market, driven by stringent environmental regulations, circular economy initiatives, and advanced manufacturing standards. Germany, France, and Italy are major contributors due to strong automotive production, industrial equipment manufacturing, and sustainable packaging adoption. The European Union’s focus on reducing volatile organic compound emissions is encouraging manufacturers to replace traditional adhesive systems with reactive hot melt alternatives. More than 40% of packaging companies are evaluating low-emission adhesive solutions to improve sustainability performance. Companies are investing in bio-based formulations, regional manufacturing facilities, and partnerships with material innovators to meet evolving regulatory requirements.

Germany Market Outlook: Germany remains the leading European market due to its automotive engineering strength and advanced manufacturing ecosystem. The country’s automotive sector represents a major application base, with more than 30% of new vehicle component programs incorporating lightweight bonding solutions. Industrial automation expertise and sustainability-focused production strategies continue to support reactive hot melt adhesive adoption.

Asia-Pacific dominates the global reactive hot melt adhesives market with approximately 42% share, supported by large-scale manufacturing activities across China, Japan, South Korea, and India. The region benefits from strong electronics production, automotive manufacturing, packaging expansion, and export-oriented industrial ecosystems. China accounts for the largest regional contribution due to extensive chemical production capacity and high-volume manufacturing operations. More than 50% of new electronics assembly facilities in major Asian manufacturing hubs are integrating advanced adhesive dispensing systems. Companies are expanding production facilities, strengthening supplier networks, and developing application-specific solutions to support growing demand from high-precision industries.

China Market Outlook: China maintains leadership through its extensive electronics, automotive, and packaging manufacturing infrastructure. The country contributes over 30% of global electronics manufacturing output, creating strong demand for reactive hot melt adhesives in precision assembly applications. Domestic chemical companies are increasing investments in advanced polymer technologies and localized adhesive production capabilities.

South America accounts for approximately 6% of the global reactive hot melt adhesives market, with demand concentrated in Brazil and Argentina’s packaging, automotive, and consumer goods industries. Industrial modernization and increasing investment in manufacturing efficiency are encouraging companies to adopt faster and cleaner bonding technologies. Brazil represents the largest market due to its automotive production base and expanding packaging sector. Nearly 25% of regional manufacturers are improving production processes through automation and material optimization initiatives. Companies are focusing on localized distribution partnerships, application support services, and cost-efficient adhesive solutions to address infrastructure limitations and improve market penetration.

Brazil Market Outlook: Brazil leads South American demand due to its automotive manufacturing, food packaging, and industrial production capabilities. The country’s packaging sector represents a major application area, with increasing adoption of recyclable materials and efficient bonding systems. Local and international suppliers are strengthening partnerships to improve product availability and technical support.

Middle East & Africa represents nearly 4% of the global reactive hot melt adhesives market, supported by construction activity, packaging growth, and industrial diversification programs. Countries including Saudi Arabia, the United Arab Emirates, and South Africa are increasing investments in manufacturing infrastructure and advanced production capabilities. The region is experiencing higher adoption of reactive hot melts in furniture, packaging, and construction applications due to improved processing efficiency. Industrial investment programs have increased demand for locally available adhesive solutions, with more than 20% of manufacturers exploring production modernization initiatives. Companies are expanding distribution networks, forming regional partnerships, and introducing customized adhesive systems for local industrial requirements.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as a strategically important market due to industrial diversification initiatives and infrastructure development projects. The country’s expanding construction and manufacturing sectors are increasing demand for advanced bonding materials. Investments in local industrial capacity and supply-chain development are supporting broader adoption of reactive hot melt adhesive technologies.

The Reactive Hot Melt Adhesives market features competition between global adhesive leaders such as Henkel, H.B. Fuller, 3M, Sika, and Arkema against regional formulation specialists and cost-focused chemical suppliers. The top five players collectively control approximately 55% of the market, creating a moderately consolidated structure. Competition is defined by polyurethane formulation expertise, curing performance, supply reliability, customization capability, and production scalability. Premium suppliers compete through advanced materials and sustainability solutions, while regional manufacturers target price-sensitive customers with localized supply chains. Over 35% of buyers prioritize customized adhesive performance, while nearly 30% emphasize delivery reliability and technical support. Companies are expanding manufacturing facilities, forming OEM partnerships, and integrating raw material capabilities to strengthen positioning. Increasing regulatory pressure and specialized formulation requirements create entry barriers. Winning requires technological differentiation, dependable supply networks, and the ability to deliver application-specific adhesive solutions faster than established competitors.

H.B. Fuller Company

3M Company

Sika AG

Arkema Group

Jowat SE

Beardow Adams

Avery Dennison Corporation

Dow Inc.

Bostik

Covestro AG

Evonik Industries AG

Reactive hot melt adhesive technology is advancing through polyurethane innovations, automated dispensing systems, and sustainable formulation development. Modern moisture-curing polyurethane adhesives improve bonding performance by approximately 25% compared with conventional hot melts, while automated application systems reduce material waste by 15–20%. Automotive and electronics manufacturers are increasing deployment of precision dispensing technologies to improve consistency and production speed.

Emerging technologies include bio-based polymers, low-temperature reactive hot melts, and digitally controlled adhesive application platforms. More than 30% of new adhesive development programs emphasize sustainable chemistry, enabling companies to reduce emissions and meet evolving environmental requirements. Compared with older solvent-based systems, reactive hot melts deliver faster processing cycles and up to 40% lower VOC emissions, creating advantages for manufacturers focused on efficiency and compliance.

Between 2026 and 2028, companies investing in smart manufacturing integration, recyclable adhesive solutions, and application-specific formulations will gain competitive advantages. Global suppliers with strong R&D capabilities benefit most, while smaller manufacturers face pressure to improve technical specialization and production flexibility.

May 2025 Henkel partnered with Sasol to integrate lower-carbon wax technology into its TECHNOMELT® hot melt adhesive portfolio. The collaboration uses SASOLWAX LC materials delivering a 35% reduction in product carbon footprint while maintaining adhesive performance. The initiative strengthens sustainable packaging solutions and supports low-emission manufacturing transitions. Source: www.henkel.com

March 2025 H.B. Fuller launched Millennium PG-1 EF ECO₂ commercial roofing adhesive using ECO₂ Driven™ technology, replacing high-impact propellants with naturally occurring gases. The innovation eliminates high-GWP blowing agents while maintaining bonding performance. The launch improves environmental compliance and expands sustainable adhesive adoption in construction applications. Source: www.newsroom.hbfuller.com

2025 Bostik (Arkema) introduced bio-based specialty hot melt adhesives containing up to 90% bio-based content for automotive interiors, technical textiles, electronics, and footwear applications. The product expansion improves sustainability performance while maintaining durability and processing flexibility. The move strengthens Bostik’s position in renewable adhesive solutions and advanced manufacturing markets. Source: www.bostik.com

September 2025 Henkel opened its Inspiration Center Shanghai for Adhesive Technologies with an investment exceeding €60 million. The 33,000-square-meter facility brings together more than 500 scientists and technical experts to accelerate adhesive innovation. The expansion strengthens regional collaboration, application development, and sustainable technology deployment across Asia-Pacific markets.

The Reactive Hot Melt Adhesives Market Report covers comprehensive analysis across types, applications, end-users, technologies, and major geographic markets including North America, Europe, Asia-Pacific, South America, and Middle East & Africa. The study evaluates polyurethane reactive hot melts, specialized formulations, packaging, automotive, electronics, construction, and industrial bonding applications.

The report examines adoption patterns, manufacturing trends, competitive positioning, innovation strategies, and emerging opportunities across established and developing markets. With analysis of leading companies, technology advancements, sustainability transitions, and supply-chain developments, the report supports investment planning, market expansion strategies, product development decisions, and competitive positioning from 2026 to 2033. It highlights evolving demand areas including automated bonding systems, recyclable materials, and advanced manufacturing applications.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 2,030.0 Million |

| Market Revenue (2033) | USD 3,652.9 Million |

| CAGR (2026–2033) | 7.62% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | Henkel AG & Co. KGaA; H.B. Fuller Company; 3M Company; Sika AG; Arkema Group; Jowat SE; Beardow Adams; Avery Dennison Corporation; Dow Inc.; Bostik; Covestro AG; Evonik Industries AG |

| Customization & Pricing | Available on Request (10% Customization Free) |