Reports

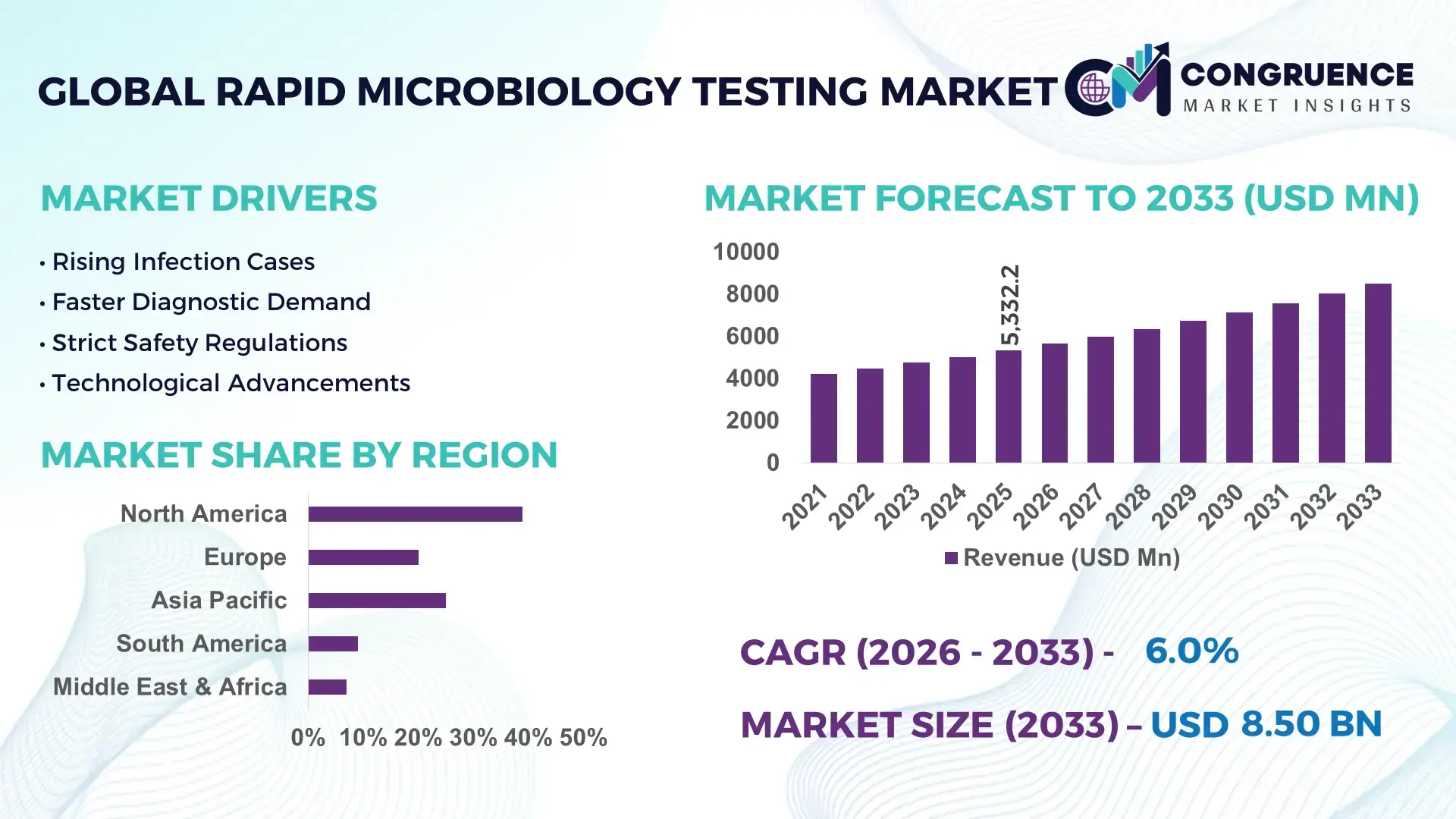

The Global Rapid Microbiology Testing Market was valued at USD 5332.17 Million in 2025 and is anticipated to reach a value of USD 8498.68 Million by 2033 expanding at a CAGR of 6% between 2026 and 2033. Growth is being driven by accelerated pharmaceutical batch-release requirements, stricter contamination-control protocols in biopharmaceutical manufacturing, rising adoption of rapid sterility testing platforms, and expanded food safety monitoring programs.

The United States remains the dominant country, accounting for approximately 34% of global market activity, supported by over USD 2 billion in annual investments across biopharmaceutical manufacturing and advanced quality-control infrastructure. More than 65% of large pharmaceutical production facilities utilize rapid microbial detection technologies to reduce product release timelines. In comparison, Germany represents nearly 8% of global demand, driven by high-value biologics production and automated laboratory adoption. Ongoing supply-chain resilience initiatives and pharmaceutical reshoring efforts following geopolitical disruptions continue to strengthen deployment across North America.

Organizations investing in automated rapid microbiology platforms gain faster release cycles, stronger compliance performance, and measurable operational efficiency advantages across regulated production environments.

Market Size & Growth: USD 5332.17 Million in 2025 rising to USD 8498.68 Million by 2033 at 6% CAGR, supported by rapid sterility testing and pharmaceutical automation.

Top Growth Drivers: Pharmaceutical quality control (+28%), biologics manufacturing (+24%), and food safety monitoring (+19%) remain primary growth catalysts.

Short-Term Forecast: By 2028, microbial testing turnaround times decline by 35% while laboratory productivity improves by nearly 30%.

Emerging Technologies: AI-assisted result interpretation, automated sample preparation, and ATP bioluminescence platforms improve testing efficiency by 20–40%.

Regional Leaders: North America exceeds USD 3.0 Billion, Europe approaches USD 2.2 Billion, and Asia-Pacific surpasses USD 1.9 Billion with expanding laboratory automation adoption.

Consumer/End-User Trends: Over 60% of pharmaceutical manufacturers prioritize rapid testing systems to accelerate batch release and compliance workflows.

Pilot/Case Example: In 2026, automated microbial monitoring deployments reduced contamination investigation times by approximately 45% across selected manufacturing sites.

Competitive Landscape: Leading suppliers collectively control nearly 48% market share, with major participation from global diagnostics and laboratory technology providers.

Regulatory & ESG Impact: Advanced testing programs reduce product waste by 15–20% while supporting stricter quality assurance and sustainability objectives.

Investment & Funding: More than USD 1.1 Billion in expansion projects, strategic partnerships, and laboratory modernization initiatives support global capacity growth.

Innovation & Future Outlook: Next-generation real-time microbial detection and digital quality-management integration improve decision accuracy by over 30% while supporting regional manufacturing expansion.

Rapid microbiology testing has become a critical component across pharmaceutical production, biotechnology research, food processing, and healthcare laboratories where contamination risks directly affect product quality and regulatory compliance. Recent innovation centers on automated microbial detection, AI-enabled analytics, and real-time monitoring systems that shorten testing cycles by nearly 40%. Growing biologics manufacturing activity and increased focus on resilient supply chains are accelerating deployment of advanced testing platforms, setting the stage for deeper strategic evaluation of competitive positioning and investment priorities.

Rapid microbiology testing is becoming a strategic priority as pharmaceutical manufacturers, biologics producers, and food processing companies face increasing pressure to shorten product-release timelines while maintaining compliance standards. The market is benefiting from laboratory digitalization, stricter contamination-control frameworks, and supply-chain restructuring that favors localized production and faster quality assurance workflows. More than 60% of large pharmaceutical facilities now integrate some level of automated microbial testing, reflecting a shift from reactive quality control toward predictive manufacturing operations.

Modern rapid testing platforms deliver results 50–70% faster than conventional culture-based methods while reducing manual laboratory interventions by nearly 40%. The United States leads deployment through advanced biopharmaceutical infrastructure and high automation intensity, whereas India is emerging as a cost-efficient expansion hub supported by growing vaccine, biosimilar, and contract manufacturing activities. A practical example is the adoption of automated sterility testing systems that enable manufacturers to accelerate batch-release decisions and improve production scheduling accuracy across multiple facilities.

Over the next two to three years, digital laboratory integration and real-time contamination monitoring are expected to expand across regulated production environments. Companies are increasing investments in automation partnerships, laboratory modernization programs, and AI-enabled analytics platforms. Organizations that establish scalable rapid microbiology capabilities will secure stronger compliance performance, faster commercialization cycles, and a sustainable competitive advantage in quality-driven industries.

The strongest market driver is the transition toward high-value biologics, cell therapies, and advanced pharmaceutical manufacturing, where rapid contamination detection directly influences production efficiency. More than 65% of large pharmaceutical facilities have accelerated automation investments, while rapid microbial testing can reduce product-release timelines by up to 70% and lower investigation workloads by approximately 35%. Regulatory emphasis on data integrity and contamination prevention is further reinforcing adoption. In the United States, biomanufacturing expansion projects are incorporating advanced microbial monitoring as a core infrastructure component. The operational impact is significant: faster batch disposition improves facility utilization and inventory management. Companies are responding through laboratory automation investments, technology partnerships, and deployment of integrated microbial detection platforms that transform quality assurance from a compliance function into a strategic productivity driver.

Implementation complexity remains a major structural limitation, particularly for mid-sized manufacturers and testing laboratories. Validation processes can account for 15–25% of deployment expenditures, while integration with legacy laboratory information systems often extends implementation timelines by more than 30%. Dependence on specialized reagents, sensors, and analytical components creates procurement challenges during supply-chain disruptions. In Germany and Japan, highly regulated production environments require extensive performance verification before technology transitions can occur. These constraints directly affect deployment speed, operational scalability, and return-on-investment realization. To mitigate risk, companies are diversifying supplier networks, localizing critical component sourcing, and adopting phased implementation models. A key strategic insight is that validation efficiency increasingly determines adoption speed as much as technological performance itself.

The most significant opportunity lies in combining rapid microbiology testing with artificial intelligence, predictive analytics, and connected laboratory ecosystems. AI-assisted interpretation can improve result-processing efficiency by approximately 30%, while automated workflows reduce manual intervention by more than 40%. India's pharmaceutical manufacturing sector and Singapore's advanced life-science infrastructure are creating attractive deployment environments for next-generation testing solutions. Emerging regulatory acceptance of digital quality-management frameworks is accelerating investment in connected laboratory architectures. Beyond faster testing, organizations gain opportunities to optimize staffing, reduce batch-hold durations, and improve production planning accuracy. Companies are expanding R&D programs, forming software partnerships, and building integrated platforms that combine microbial detection, analytics, and compliance management. The non-obvious advantage is the creation of operational intelligence datasets that enhance broader manufacturing decision-making.

Long-term market expansion depends on successful integration of advanced testing technologies into increasingly digital production environments. Approximately 40% of laboratories report shortages of personnel skilled in automated microbiology workflows, while system integration projects can exceed planned deployment schedules by 20–30%. As facilities adopt cloud-connected laboratory platforms and real-time monitoring architectures, maintaining data consistency across multiple systems becomes more challenging. In the United States and the United Kingdom, manufacturers face pressure to harmonize quality data across geographically distributed operations. These execution barriers affect scalability, deployment consistency, and long-term competitiveness. Companies must invest in workforce development, interoperability standards, and digital infrastructure modernization while strengthening technology partnerships. The organizations that solve integration complexity fastest will establish durable operational advantages as testing environments become increasingly automated and data-centric.

• AI-Driven Laboratory Intelligence AI-enabled interpretation platforms are transforming microbiology workflows by reducing result review times by 30–45% and lowering manual verification workloads by nearly 25%. Pharmaceutical facilities in the United States are increasingly integrating analytics engines with laboratory information management systems, improving contamination trend detection and process consistency. Companies are expanding software partnerships and embedding predictive algorithms into testing platforms to improve operational visibility while addressing skilled labor shortages.

• Real-Time Manufacturing Monitoring Expansion Continuous microbial monitoring is replacing periodic testing across high-value biologics and sterile manufacturing environments. Deployment of real-time contamination detection systems increased by approximately 35% across advanced production facilities during the past two years, while batch release timelines have shortened by up to 60%. Stricter manufacturing quality requirements and production continuity objectives are accelerating adoption. Suppliers are scaling sensor portfolios and automated monitoring solutions to support uninterrupted manufacturing operations.

• Automation Beyond Central Laboratories Decentralized and automated testing workflows are gaining traction as enterprises seek faster decision-making across multiple sites. Automated sample preparation adoption has increased by over 40%, while hands-on technician time has declined by nearly 30%. A non-obvious shift is the movement of testing capabilities closer to production lines rather than central laboratories. Companies are restructuring quality-control networks and investing in modular testing platforms to improve responsiveness and reduce operational bottlenecks.

• Supply-Chain Resilience Priorities Pharmaceutical and food manufacturers are prioritizing testing infrastructure as part of broader supply-chain risk management strategies. More than 50% of large enterprises have expanded quality-monitoring investments following recent raw-material sourcing disruptions. Faster contamination detection reduces inventory hold periods by approximately 20% and strengthens production scheduling accuracy. Companies are increasing regional testing capacity, forming technology alliances, and standardizing quality systems across manufacturing networks to improve operational resilience.

PCR-Based Testing remains the leading segment due to its high sensitivity, rapid turnaround, and seamless integration into pharmaceutical quality-control workflows. The technology accounts for an estimated 35–40% of advanced rapid microbiology deployments because it can identify microbial contamination significantly faster than traditional culture-based approaches. Pharmaceutical manufacturers increasingly favor PCR systems to support biologics production and sterility assurance programs. ATP Bioluminescence and Microbial Culture Systems continue to maintain strong positions in routine quality monitoring, particularly where cost efficiency and established validation frameworks remain critical purchasing factors.

Flow Cytometry represents the fastest-growing segment, supported by its ability to deliver near real-time microbial analysis and automated cell characterization. Adoption rates have increased by roughly 20% in advanced pharmaceutical facilities seeking greater process visibility. Immunoassay Testing remains strategically relevant for targeted detection applications where specificity is essential. Companies are expanding product portfolios, enhancing automation compatibility, and developing multiplex testing capabilities to strengthen differentiation. Investment priorities are gradually shifting toward platforms that combine speed, scalability, and digital connectivity, creating competitive advantages in regulated production environments.

Pharmaceutical Testing is the dominant application segment due to stringent contamination-control requirements across biologics, vaccines, sterile injectables, and advanced therapeutics manufacturing. Nearly 40% of rapid microbiology testing deployments are linked directly to pharmaceutical quality assurance activities. Faster microbial detection supports accelerated batch release, improved facility utilization, and stronger regulatory compliance. Clinical Diagnostics remains a major application area as healthcare providers seek quicker identification of microbial threats to improve treatment decisions and laboratory efficiency.

Food Safety Testing is emerging as the fastest-growing application, supported by expanding food traceability programs and heightened contamination monitoring requirements. Adoption of rapid microbial testing in food production environments has increased by approximately 25% as manufacturers focus on reducing recall risks and production interruptions. Environmental Monitoring and Water Testing are also gaining strategic importance, particularly in industrial facilities requiring continuous contamination surveillance. Companies are scaling automation investments, integrating testing data into enterprise quality systems, and expanding deployment across distributed operational networks. Demand is increasingly concentrated in applications where testing speed directly affects production continuity and risk management outcomes.

Diagnostic Laboratories represent the largest end-user segment due to their high testing volumes, centralized infrastructure, and broad deployment of advanced analytical technologies. Approximately 30–35% of rapid microbiology testing activity is concentrated within laboratory networks supporting healthcare, pharmaceutical, and industrial clients. Their operational dependence on throughput optimization and turnaround-time reduction continues to drive investment in automated microbial detection systems. Hospitals remain important adopters, particularly for infection-control monitoring and clinical microbiology applications requiring faster diagnostic support.

Pharmaceutical Companies constitute the fastest-growing end-user segment as biologics manufacturing, sterile production, and quality-assurance modernization initiatives expand globally. Adoption of automated microbial testing within pharmaceutical environments has increased by nearly 30% over recent years. Food and Beverage Companies are also increasing deployments to strengthen contamination prevention and supply-chain quality controls. Research Institutes and Environmental Agencies continue to expand usage for surveillance, validation, and environmental assessment programs. Vendors are responding through customized workflow solutions, long-term service agreements, and integrated digital platforms tailored to different operational requirements. Future demand is increasingly shifting toward organizations where testing outcomes directly influence production efficiency and compliance performance.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 7.4% between 2026 and 2033.

Biopharmaceutical Automation Driving Deployment Leadership

North America maintains the leading position through its concentration of biopharmaceutical manufacturing facilities, advanced laboratory infrastructure, and extensive adoption of automated quality-control systems. The region represents approximately 38% of global market activity, supported by large-scale biologics production and contamination-control requirements. More than 65% of major pharmaceutical manufacturing sites utilize rapid microbial detection technologies within critical production workflows. Enterprise investment is increasingly focused on integrating automated microbiology platforms with digital quality-management systems to improve operational efficiency. Recent facility modernization initiatives have reduced batch-release timelines by up to 50%, strengthening deployment momentum across pharmaceutical, healthcare, and food safety applications.

United States Market Outlook: The United States remains the region’s strategic center due to its extensive biopharmaceutical production capacity, advanced regulatory framework, and strong laboratory automation ecosystem. Large pharmaceutical manufacturers continue expanding microbial monitoring capabilities across biologics and sterile manufacturing operations. More than 70% of newly commissioned pharmaceutical quality-control laboratories incorporate molecular testing technologies. Ongoing investments in advanced manufacturing, coupled with increasing adoption of AI-supported laboratory workflows, position the country as the primary innovation hub for rapid microbiology testing deployment.

Regulatory Modernization Accelerating Advanced Testing Adoption

Europe holds a significant market position through stringent quality standards, strong pharmaceutical production capabilities, and increasing laboratory digitalization initiatives. The region accounts for approximately 29% of global demand, with adoption concentrated across pharmaceutical manufacturing, food safety monitoring, and environmental testing programs. Regulatory emphasis on contamination prevention and process validation continues to encourage migration toward rapid microbial detection platforms. Recent laboratory modernization projects have increased automated testing utilization by nearly 30% across selected manufacturing clusters. Companies are strengthening partnerships with technology providers to improve workflow standardization and compliance efficiency while reducing operational complexity.

Germany Market Outlook: Germany serves as the region’s primary market due to its advanced pharmaceutical manufacturing base, biotechnology expertise, and highly automated industrial infrastructure. The country continues expanding investments in quality-control technologies to support biologics production and export-oriented manufacturing. Approximately 60% of large pharmaceutical facilities have implemented advanced rapid microbiology solutions within contamination-monitoring programs. Strong engineering capabilities and established industrial partnerships continue supporting deployment of next-generation testing systems across regulated production environments.

Manufacturing Expansion Supporting Rapid Adoption

Asia-Pacific is emerging as the fastest-expanding market due to pharmaceutical manufacturing growth, laboratory capacity expansion, and increasing investments in healthcare infrastructure. The region contributes approximately 24% of global demand and continues strengthening its role in vaccine production, biosimilars, and contract manufacturing services. Pharmaceutical testing deployments have increased by more than 35% across major manufacturing hubs during the past three years. Companies are expanding testing capacity through automation projects, facility upgrades, and strategic technology partnerships. The combination of cost-efficient manufacturing and growing regulatory requirements is accelerating adoption of advanced microbial testing platforms.

China Market Outlook: China remains the largest market within Asia-Pacific due to its extensive pharmaceutical production network, biotechnology investments, and manufacturing scale. The country continues expanding high-value biologics production facilities that require advanced contamination-control systems. More than 50% of newly established pharmaceutical quality laboratories incorporate rapid testing technologies as part of modernization programs. Government-backed industrial development initiatives and expanding domestic innovation capabilities are strengthening the country's position as a major deployment center for advanced microbiology testing solutions.

Food Safety and Pharmaceutical Demand Expansion

South America is experiencing steady market development driven by pharmaceutical quality-control requirements and growing food safety testing activities. The region accounts for approximately 5% of global market demand, with adoption concentrated in industrial production centers and regulated manufacturing environments. Investments in laboratory modernization and contamination-control infrastructure are improving testing capabilities across multiple industries. Automated testing deployments have increased by nearly 20% among large food processing facilities seeking stronger quality assurance performance. While infrastructure disparities remain across certain markets, enterprise demand for faster testing workflows continues to support gradual adoption.

Brazil Market Outlook: Brazil represents the region’s largest opportunity due to its pharmaceutical production scale, food processing industry, and expanding laboratory infrastructure. Regulatory emphasis on product quality and export competitiveness is encouraging investment in advanced testing technologies. Large manufacturers increasingly deploy rapid microbial monitoring systems to reduce production delays and improve compliance outcomes. The country's growing contract manufacturing sector and modernization initiatives are strengthening demand for scalable and automated microbiology testing solutions.

Healthcare and Industrial Modernization Investments

The Middle East & Africa market is benefiting from healthcare infrastructure expansion, industrial diversification programs, and increasing quality-control requirements across pharmaceutical and food production sectors. The region contributes approximately 4% of global demand, with deployment activity concentrated in countries investing heavily in laboratory modernization. Recent healthcare and biotechnology infrastructure initiatives have increased advanced testing capacity by nearly 25% in selected markets. Companies are partnering with international technology providers to improve laboratory capabilities and accelerate adoption of automated microbial detection systems. Investment-led modernization remains the primary catalyst for market development.

Saudi Arabia Market Outlook: Saudi Arabia leads regional adoption through large-scale healthcare transformation programs, pharmaceutical manufacturing investments, and advanced laboratory infrastructure projects. The country continues strengthening domestic production capabilities as part of broader industrial diversification strategies. More than 40% of newly developed pharmaceutical quality facilities include advanced microbiology testing technologies. Government-backed investment programs, combined with growing biotechnology ambitions, are supporting deployment of automated testing systems and creating long-term opportunities for technology suppliers.

The market is led by Merck KGaA, bioMérieux, Danaher Corporation, Thermo Fisher Scientific, and Sartorius, which collectively account for approximately 58% of global market activity. Competition primarily occurs between global technology leaders offering integrated rapid microbiology platforms and specialized innovators focusing on automation, molecular diagnostics, and contamination-monitoring solutions. Technology performance, validation speed, and workflow efficiency represent the primary competitive factors. Advanced automated systems reduce testing turnaround times by 50–70%, while digital workflow integration improves laboratory productivity by nearly 30%. Leading players are expanding through biopharmaceutical partnerships, laboratory automation investments, product portfolio enhancements, and strategic acquisitions. Regional suppliers compete through cost-efficient deployment models and localized service capabilities. The current competitive shift centers on AI-enabled analytics, real-time microbial monitoring, and integrated quality-management ecosystems. Validation requirements and regulatory compliance remain significant entry barriers. Success increasingly depends on delivering scalable automation, regulatory confidence, operational efficiency, and seamless digital integration across quality-control environments.

Merck KGaA

bioMérieux

Thermo Fisher Scientific

Danaher Corporation

Sartorius AG

Charles River Laboratories

BD (Becton, Dickinson and Company)

Neogen Corporation

Shimadzu Corporation

Agilent Technologies

Rapid Micro Biosystems

Bruker Corporation

QIAGEN N.V.

Lonza Group AG

Rapid microbiology testing is increasingly centered on PCR-based detection, ATP bioluminescence, and automated microbial monitoring platforms that shorten contamination detection cycles across pharmaceutical and biotechnology facilities. PCR systems can improve microbial identification speed by nearly 60% compared with conventional culture methods, while automated incubation and imaging technologies reduce manual laboratory intervention by approximately 35%. More than 65% of large pharmaceutical quality-control laboratories now utilize at least one automated rapid microbiology workflow. The operational advantage is faster batch disposition, improved production scheduling, and stronger contamination-control performance in regulated manufacturing environments.

Emerging technologies are shifting toward AI-assisted result interpretation, flow cytometry-based microbial analysis, and integrated laboratory informatics platforms. AI-enabled analytics improve data review efficiency by nearly 30%, while advanced flow cytometry systems enhance microbial detection throughput by approximately 25%. Adoption is accelerating among biologics manufacturers where contamination risks directly affect production continuity. Companies are investing in software integration, digital quality-management ecosystems, and predictive contamination-monitoring capabilities to create operational differentiation and reduce quality-related delays.

Between 2026 and 2028, disruptive technologies such as real-time microbial sensing, cloud-connected laboratory platforms, and autonomous testing workflows are expected to gain broader deployment. New-generation automated systems deliver up to 70% faster results than legacy culture-based methods. Global pharmaceutical manufacturers and contract development organizations benefit most through faster product release, improved compliance consistency, and stronger competitive positioning. Organizations delaying modernization risk slower decision cycles and reduced manufacturing agility.

May 2025 – Rapid Micro Biosystems announced a global distribution and collaboration agreement with Merck KGaA’s Life Science business (MilliporeSigma) to expand Growth Direct system commercialization. The agreement included minimum purchase commitments exceeding USD 20 million, strengthening global deployment and market reach.

November 2025 – Rapid Micro Biosystems secured its largest multi-system order from a Top 20 global biopharmaceutical manufacturer to automate microbiology quality control across multiple facilities. Recurring revenue increased 32% year-over-year, demonstrating accelerating enterprise adoption and validation of automated testing workflows. Source: investors.rapidmicrobio.com

June 2025 – bioMérieux acquired Day Zero Diagnostics solutions and technologies to strengthen next-generation microbiology and pathogen identification capabilities. The transaction expanded advanced diagnostic innovation capacity and enhanced competitive positioning in automated microbiology testing applications. Source: rapidmicrobiology.com

March 2026 – Rapid Micro Biosystems reported expansion of Growth Direct deployments through follow-on orders from major biopharmaceutical manufacturers, including Samsung Biologics. The company reached 190 cumulative system placements globally, supporting broader automation adoption and faster microbial quality-control processes. Source: investors.rapidmicrobio.com

The report provides comprehensive coverage of rapid microbiology testing technologies across PCR-Based Testing, Immunoassay Testing, Flow Cytometry, ATP Bioluminescence, and Microbial Culture Systems. Analysis extends across key applications including Clinical Diagnostics, Pharmaceutical Testing, Food Safety Testing, Environmental Monitoring, and Water Testing, while evaluating adoption patterns among hospitals, diagnostic laboratories, pharmaceutical companies, food and beverage enterprises, research institutes, and environmental agencies. More than 60% of advanced pharmaceutical quality-control facilities have incorporated automated testing workflows, making technology deployment trends a central area of assessment.

The study delivers detailed regional intelligence covering North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. It evaluates laboratory automation, digital quality-management integration, AI-enabled analytics, real-time microbial monitoring, and emerging contamination-control technologies. Strategic insights support investment prioritization, market-entry planning, competitive benchmarking, partnership evaluation, and expansion decisions. Particular attention is given to deployment acceleration between 2026 and 2033, evolving enterprise purchasing behavior, innovation pipelines, and operational factors shaping long-term competitive positioning.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 5332.17 Million |

|

Market Revenue in 2033 |

USD 8498.68 Million |

|

CAGR (2026 - 2033) |

6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Merck KGaA, bioMérieux, Thermo Fisher Scientific, Danaher Corporation, Sartorius AG, Charles River Laboratories, BD (Becton, Dickinson and Company), Neogen Corporation, Shimadzu Corporation, Agilent Technologies, Rapid Micro Biosystems, Bruker Corporation, QIAGEN N.V., Lonza Group AG |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |