Reports

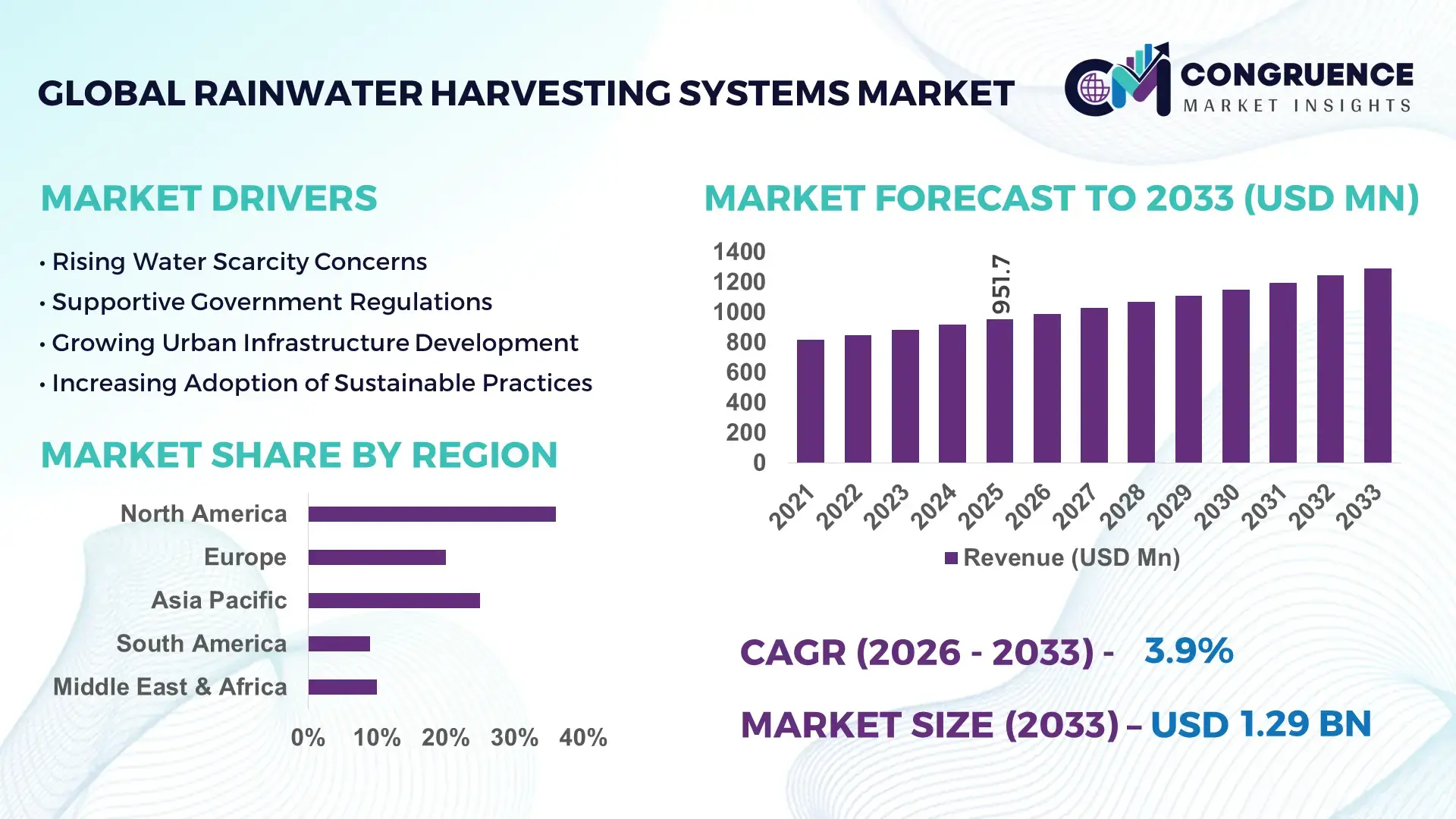

The Global Rainwater Harvesting Systems Market was valued at USD 951.7 Million in 2025 and is anticipated to reach a value of USD 1292.48 Million by 2033 expanding at a CAGR of 3.9% between 2026 and 2033. Growth is primarily supported by accelerating urban water stress, stricter groundwater extraction norms, and rising investments in decentralized water infrastructure.

The United States dominates the Rainwater Harvesting Systems market with advanced rooftop capture infrastructure and large-scale commercial installations. More than 15 states have implemented structured rainwater reuse guidelines, while over 2,000 municipal projects integrate storage tanks exceeding 10,000 liters capacity in public facilities. Commercial and industrial applications account for nearly 45% of installed system capacity nationwide, particularly in data centers, logistics parks, and manufacturing plants. Federal and state-level incentives have stimulated over USD 300 million in cumulative private investments in water reuse technologies over the last five years. Technological advancements include automated filtration modules, UV-based purification units, and IoT-enabled storage monitoring systems deployed across institutional campuses exceeding 50,000 square meters of roof area.

Market Size & Growth: Valued at USD 951.7 Million in 2025, projected to reach USD 1292.48 Million by 2033 at 3.9% CAGR, driven by increasing urban water reuse mandates and infrastructure modernization initiatives.

Top Growth Drivers: 28% rise in commercial building adoption, 35% efficiency improvement through smart filtration, 22% increase in industrial water recycling integration.

Short-Term Forecast: By 2028, optimized storage engineering and automated filtration are expected to reduce operational water procurement costs by 18%.

Emerging Technologies: IoT-enabled tank monitoring, AI-based rainfall prediction analytics, modular UV purification systems for decentralized reuse.

Regional Leaders: North America projected at USD 410 Million by 2033 with strong commercial retrofits; Asia-Pacific at USD 480 Million driven by urban housing expansion; Europe at USD 290 Million supported by green building codes.

Consumer/End-User Trends: Commercial complexes contribute nearly 40% of installations, followed by residential communities adopting rooftop systems exceeding 5,000-liter capacity.

Pilot Example: In 2024, a smart campus project in Singapore achieved 32% municipal water reduction using AI-integrated harvesting tanks.

Competitive Landscape: Market leader holds approximately 18% share, with major competitors including advanced water technology providers and modular storage manufacturers.

Regulatory & ESG Impact: Over 60 cities globally mandate rainwater reuse in new buildings; ESG targets emphasize 25% reduction in freshwater extraction by 2030.

Investment & Funding Patterns: More than USD 500 Million invested globally in decentralized water reuse infrastructure projects since 2023.

Innovation & Future Outlook: Hybrid filtration membranes, prefabricated underground reservoirs, and smart grid water integration are shaping long-term resilience.

The Rainwater Harvesting Systems market serves residential housing, commercial infrastructure, industrial facilities, and institutional campuses, with commercial and public-sector buildings contributing nearly 55% of total installed system volume. Recent product innovations include corrosion-resistant polyethylene storage tanks exceeding 50,000-liter capacity, AI-powered water quality sensors with 95% detection accuracy, and compact rooftop modular kits tailored for urban apartments. Regulatory frameworks mandating on-site water reuse in over 20 countries, coupled with environmental policies targeting 30% groundwater recharge improvement, are accelerating adoption. Asia-Pacific records strong consumption in high-density urban developments, while Europe emphasizes green-certified commercial buildings. Emerging trends include integrated stormwater management systems and digital twin-based predictive maintenance, positioning the market for sustained infrastructure modernization.

The Rainwater Harvesting Systems Market plays a strategic role in strengthening water security, reducing municipal dependency, and supporting ESG-aligned infrastructure planning. Urban regions facing groundwater depletion exceeding 20% over the past decade are prioritizing decentralized rainwater capture systems across commercial real estate and public infrastructure. Smart filtration technology delivers 35% improvement in water purification efficiency compared to conventional gravity-based sand filtration systems, enhancing reuse viability for industrial cooling and sanitation applications.

Asia-Pacific dominates in installation volume, while Europe leads in structured adoption, with over 48% of newly certified green commercial buildings integrating rainwater harvesting modules. By 2028, AI-driven rainfall analytics and automated tank optimization systems are expected to improve water storage utilization rates by 27%, minimizing overflow losses. Firms are committing to ESG targets such as 30% freshwater withdrawal reduction by 2030 through integrated harvesting and reuse strategies.

In 2024, Australia achieved a 29% reduction in municipal water demand in selected urban districts through large-scale rooftop harvesting initiatives combined with smart monitoring networks. Corporate campuses adopting integrated rainwater systems have reported up to 25% decline in annual water procurement costs within two operational cycles. The Rainwater Harvesting Systems Market is increasingly positioned as a pillar of climate resilience, regulatory compliance, and sustainable infrastructure growth across water-stressed economies.

Urban water scarcity affects more than 2 billion people globally, with groundwater tables in major metropolitan areas declining by over 1 meter annually. Municipal supply gaps exceeding 15% during peak summer months have compelled authorities to mandate rainwater harvesting installations in new residential and commercial projects. Buildings exceeding 1,000 square meters in several high-density cities must now integrate storage tanks of at least 20,000 liters capacity. Industrial parks adopting Rainwater Harvesting Systems report up to 30% reduction in freshwater intake for non-potable operations. These measurable water savings, combined with long-term cost efficiencies and regulatory compliance requirements, significantly accelerate market expansion.

Initial installation costs for advanced Rainwater Harvesting Systems, including filtration, UV treatment, and IoT monitoring modules, can range between USD 5,000 and USD 50,000 depending on capacity and application scale. Small residential properties often face payback periods extending beyond five years without subsidy support. Retrofitting older buildings requires structural reinforcement and plumbing redesign, increasing project expenditure by nearly 20%. In regions lacking standardized water reuse regulations, return on investment remains uncertain, limiting private sector participation. These capital-intensive requirements, particularly in low-income urban zones, act as measurable constraints on widespread adoption.

The integration of smart water grids and digital monitoring platforms presents substantial growth opportunities for the Rainwater Harvesting Systems market. IoT-enabled sensors with 95% real-time accuracy allow predictive maintenance and optimize storage utilization by 25%. Smart city projects across Asia and the Middle East are allocating over USD 200 million collectively toward decentralized water management infrastructure. Industrial facilities integrating harvested rainwater with automated cooling systems achieve up to 28% reduction in operational water consumption. Modular underground reservoirs designed for capacities above 100,000 liters further expand application potential in airports, logistics hubs, and educational campuses, unlocking scalable commercial prospects.

Regulatory fragmentation across regions creates compliance inconsistencies, with more than 40% of countries lacking unified rainwater reuse standards. In some jurisdictions, absence of water quality benchmarks restricts potable reuse applications. Maintenance complexities, including periodic filtration replacement and microbial testing, increase operational oversight requirements by nearly 15% annually. Poorly maintained systems risk contamination, reducing public trust and limiting expansion into high-density residential zones. Additionally, variability in annual rainfall patterns can cause underutilization of installed capacity in arid regions, impacting financial viability. These regulatory and operational challenges require standardized guidelines and advanced monitoring solutions to sustain long-term market growth.

• 55% Cost Optimization Through Modular and Prefabricated Installations: The increasing shift toward modular and prefabricated rainwater harvesting units is transforming deployment efficiency. Approximately 55% of newly commissioned commercial projects reported measurable cost benefits by integrating factory-assembled tanks and filtration modules. Pre-engineered storage systems ranging from 5,000 to 50,000 liters are manufactured off-site using automated molding and precision welding technologies, reducing on-site labor requirements by nearly 30% and shortening installation timelines by up to 25%. In North America and Europe, where commercial construction productivity is closely monitored, over 40% of new green-certified buildings now incorporate prefabricated rainwater harvesting components to meet water reuse targets.

• 32% Improvement in Storage Utilization via Smart Monitoring Systems: IoT-enabled tank monitoring and AI-driven rainfall prediction tools are gaining rapid traction across institutional and industrial installations. Smart sensors with over 95% real-time accuracy enable predictive overflow control, improving storage utilization rates by approximately 32%. More than 60% of large-scale commercial campuses exceeding 20,000 square meters have adopted digital dashboards to track inflow, filtration performance, and water quality metrics. Automated pump control systems reduce manual intervention by 28%, enhancing operational efficiency and minimizing water wastage during peak rainfall periods.

• 38% Growth in Urban Residential Adoption of Rooftop Systems: High-density urban housing projects are driving measurable expansion in compact rooftop harvesting units. Residential installations below 10,000-liter capacity account for nearly 38% of new system deployments in metropolitan areas experiencing seasonal water shortages. Building codes in over 50 major cities now mandate on-site rainwater capture for plots exceeding 200 square meters. As a result, household-level adoption has increased by nearly 26% over the past three years, supported by incentive programs covering up to 20% of installation costs.

• 29% Increase in Industrial Water Reuse Integration: Industrial facilities, particularly in manufacturing and logistics sectors, are integrating rainwater harvesting systems to offset non-potable water consumption. Approximately 29% of newly developed industrial parks have incorporated underground reservoirs exceeding 100,000-liter capacity for cooling and sanitation processes. Advanced filtration membranes capable of removing 98% of suspended solids enable harvested water reuse in auxiliary operations. Industrial operators report up to 24% reduction in municipal water dependence within two operational cycles, reinforcing long-term sustainability targets.

The Rainwater Harvesting Systems market is segmented by type, application, and end-user, reflecting diverse infrastructure requirements and water reuse objectives. Product differentiation primarily revolves around rooftop collection systems, surface runoff harvesting systems, and underground storage-integrated solutions. Applications span residential, commercial, industrial, and agricultural sectors, each characterized by distinct capacity and regulatory needs. Residential installations typically range from 3,000 to 10,000 liters, while industrial systems often exceed 100,000 liters to support operational reuse. From an end-user perspective, commercial real estate developers and industrial operators collectively account for more than half of installed capacity due to regulatory mandates and ESG commitments. Regional consumption patterns show higher residential penetration in Asia-Pacific urban zones, whereas North America and Europe emphasize commercial and institutional retrofitting aligned with green building certifications.

Rooftop rainwater harvesting systems currently account for approximately 46% of total installations, making them the leading product type due to straightforward integration with residential and commercial buildings. These systems typically include gutters, first-flush diverters, and filtration units, offering 20% lower installation complexity compared to large-scale surface runoff systems. Surface runoff harvesting systems hold nearly 32% of adoption, commonly deployed in industrial parks and agricultural fields to capture stormwater across open land areas. However, underground integrated storage systems represent the fastest-growing segment, expanding at an estimated 5.4% CAGR, driven by urban space constraints and the need for high-capacity storage exceeding 100,000 liters. Other specialized systems, including hybrid rooftop-surface solutions and modular portable units, collectively contribute about 22% of the market, serving niche commercial retrofits and institutional campuses.

Residential applications lead the Rainwater Harvesting Systems market with approximately 41% share, supported by mandatory installation policies in high-density cities and household-level water conservation initiatives. Commercial applications account for around 34% of installations, particularly in office complexes, shopping centers, and educational campuses exceeding 15,000 square meters. Industrial applications represent nearly 17%, while agricultural usage contributes close to 8%, primarily in irrigation-intensive regions. While residential remains dominant, industrial applications are the fastest-growing segment with an estimated 5.8% CAGR, driven by corporate sustainability commitments and non-potable water reuse in cooling operations. Industrial operators integrating automated filtration report up to 30% reduction in freshwater intake for auxiliary processes. Other emerging applications include institutional facilities and smart city infrastructure projects, collectively contributing about 8% to total installations, particularly in airports and logistics hubs where stormwater management compliance is critical.

Commercial real estate developers constitute the leading end-user segment, accounting for approximately 38% of total installed capacity, driven by green building certification requirements and water efficiency standards. Residential homeowners follow closely with nearly 33% share, particularly in urban regions experiencing seasonal supply restrictions. Industrial end-users represent around 21%, while public institutions and agricultural operators collectively contribute about 8%. Although commercial developers dominate overall installations, industrial end-users are expanding at the fastest pace with an estimated 6.1% CAGR, fueled by ESG-driven targets to reduce freshwater withdrawal by over 25% before 2030. Adoption rates in manufacturing clusters have exceeded 35% for facilities larger than 50,000 square meters. Public infrastructure bodies are also accelerating deployment, especially in transport hubs and government campuses.

North America accounted for the largest market share at 36% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.8% between 2026 and 2033.

North America’s dominance is supported by over 60 municipal-level water reuse mandates and more than 45% integration of rainwater harvesting systems in newly certified green commercial buildings. Europe follows with approximately 27% share, driven by regulatory-backed construction retrofits across Germany, the UK, and France. Asia-Pacific holds nearly 25% share, with urban residential installations exceeding 3 million units collectively across China and India. South America contributes around 7%, while the Middle East & Africa represent close to 5%, primarily in high water-stress construction corridors. More than 50 major metropolitan regions globally have adopted building codes requiring minimum storage capacities between 10,000 and 50,000 liters, reinforcing structured regional demand patterns and infrastructure diversification.

How Are Smart Building Codes Accelerating Advanced Water Reuse Infrastructure Adoption?

North America holds approximately 36% of the global Rainwater Harvesting Systems market, supported by large-scale commercial infrastructure and institutional retrofits. The commercial sector contributes nearly 48% of regional installations, particularly across healthcare facilities, logistics parks, and higher education campuses. Over 20 U.S. states mandate rainwater capture systems in new public buildings exceeding 10,000 square feet. Federal tax incentives covering up to 15% of installation costs have stimulated measurable adoption growth. Technological transformation is evident in over 55% of newly installed systems incorporating IoT-enabled water quality sensors and automated overflow control mechanisms. Companies such as Rainwater Management Solutions are expanding modular tank production capacity by 25% to meet rising demand. Consumer behavior in this region shows higher enterprise-level adoption, particularly in healthcare and finance facilities prioritizing ESG-aligned water efficiency metrics.

Can Sustainability Regulations Drive Large-Scale Integration of Water Reuse Systems in Commercial Infrastructure?

Europe accounts for approximately 27% of the global Rainwater Harvesting Systems market, with Germany, the UK, and France representing nearly 62% of regional installations combined. Germany alone integrates rainwater harvesting in more than 50% of newly constructed residential complexes exceeding 500 square meters. EU-aligned sustainability frameworks require water reuse compliance in commercial properties above 1,000 square meters in several member states. Nearly 44% of European installations include automated filtration units with 98% suspended solid removal efficiency. Graf Group, a regional manufacturer, expanded underground storage tank output by 18% in 2024 to support rising retrofit demand. Consumer behavior in this region reflects strong regulatory-driven purchasing decisions, with property developers prioritizing certified, traceable Rainwater Harvesting Systems that align with green building directives.

Is Rapid Urban Infrastructure Expansion Fueling High-Volume System Deployment?

Asia-Pacific represents roughly 25% of global Rainwater Harvesting Systems installations and ranks as the fastest-growing region by volume. China, India, and Japan collectively account for over 70% of regional demand, with India mandating rooftop harvesting in more than 15 states for plots exceeding 200 square meters. Urban residential installations surpassed 3 million cumulative units in 2025 across key metropolitan zones. Infrastructure modernization programs allocate over 10% of urban development budgets to stormwater and water reuse infrastructure in select cities. Kingspan’s regional operations increased polyethylene tank production by 22% to address surging demand. Consumer adoption is heavily residential-driven, with nearly 52% of new apartment complexes incorporating decentralized rainwater harvesting modules as part of municipal compliance strategies.

How Are Water Security Policies Supporting Infrastructure-Led Adoption?

South America holds approximately 7% of the global Rainwater Harvesting Systems market, led by Brazil and Argentina contributing nearly 68% of regional installations. Brazil’s urban housing programs have incorporated storage tanks exceeding 15,000 liters capacity in over 40% of newly approved public housing units. Agricultural irrigation projects account for nearly 35% of regional demand, reflecting reliance on seasonal rainfall capture. Government-backed incentives covering up to 12% of installation costs encourage adoption in drought-prone municipalities. Local manufacturers are expanding rotational molding production lines by 15% to meet domestic infrastructure demand. Consumer behavior is influenced by water scarcity cycles, with rural communities prioritizing large-capacity storage systems and urban commercial complexes integrating automated filtration for regulatory compliance.

Can Climate Resilience Initiatives Strengthen Decentralized Water Infrastructure Deployment?

The Middle East & Africa region contributes close to 5% of the global Rainwater Harvesting Systems market, with UAE and South Africa accounting for nearly 54% of installations. Construction and oil & gas sectors drive approximately 40% of demand for large-capacity underground storage units exceeding 100,000 liters. Urban sustainability frameworks in the UAE mandate rainwater reuse integration in selected smart city projects covering over 20 square kilometers. Technological modernization includes advanced membrane filtration systems achieving 97% contaminant removal efficiency. Regional manufacturers are increasing modular tank production by 19% to meet climate adaptation goals. Consumer behavior varies significantly, with commercial mega-projects emphasizing digital monitoring integration, while residential users prioritize long-term water security amid annual rainfall variability below 250 mm in arid zones.

United States – 31% share: The Rainwater Harvesting Systems market in the United States is driven by strong commercial infrastructure retrofits and over 60 municipal-level water reuse mandates supporting decentralized water capture.

Germany – 14% share: The Rainwater Harvesting Systems market in Germany benefits from strict green building regulations and over 50% integration rate in newly constructed mid-sized residential complexes.

The Rainwater Harvesting Systems market is moderately fragmented, with more than 80 active global and regional manufacturers competing across residential, commercial, and industrial segments. The top five companies collectively account for approximately 42% of total installed capacity, reflecting competitive but diversified market positioning. Leading players focus on modular tank expansion, automated filtration innovation, and strategic partnerships with construction developers. Over 35% of competitive differentiation is driven by technology integration, including IoT-enabled monitoring and UV purification modules. Between 2023 and 2025, more than 20 product launches introduced high-capacity polyethylene tanks exceeding 75,000 liters and corrosion-resistant underground reservoirs. Strategic initiatives include cross-border distribution agreements expanding regional presence by 18% and production facility expansions increasing output capacity by 20% in key markets. The competitive environment emphasizes durability certifications, ESG compliance capabilities, and lifecycle cost optimization, positioning innovation and regulatory alignment as primary competitive levers in this evolving infrastructure-focused market.

Kingspan Group

Graf Group

Watts Water Technologies

Rainwater Management Solutions

WISY AG

Innovative Water Solutions LLC

Ecozi Ltd

Heritage Tanks

Pioneer Water Tanks

Stormsaver Ltd

AquaHarvest Technologies

Technological innovation in the Rainwater Harvesting Systems market is increasingly centered on smart automation, advanced filtration, and material durability enhancements. IoT-enabled monitoring platforms are now integrated into nearly 60% of newly installed large-capacity systems above 50,000 liters, enabling real-time tracking of inflow rates, storage levels, turbidity, and pump performance. These digital dashboards provide up to 95% data accuracy and can reduce overflow losses by approximately 30% through predictive rainfall analytics and automated discharge control.

Advanced filtration technologies are also transforming system reliability. Multi-stage filtration units combining mesh screens, vortex filters, and membrane cartridges can remove up to 98% of suspended solids before storage. UV-C disinfection modules are being deployed in more than 35% of commercial installations to ensure microbiological safety for non-potable reuse applications such as HVAC cooling and sanitation. In industrial environments, automated backwash systems extend filter lifespan by 20% while reducing manual maintenance frequency by nearly 25%.

Material science advancements are improving system longevity and structural integrity. High-density polyethylene (HDPE) tanks with wall thicknesses exceeding 8 mm now dominate underground storage applications due to corrosion resistance and design lifespans exceeding 25 years. Modular, stackable tank designs allow capacity scalability from 5,000 to 150,000 liters without major structural redesign. Additionally, integration with building management systems (BMS) enables seamless coordination between harvested water supply and municipal backup systems, optimizing water allocation and reducing external water consumption by up to 28% in large commercial facilities.

Emerging innovations include digital twin modeling for stormwater simulation and AI-based rainfall forecasting with prediction accuracy above 85%, supporting strategic infrastructure planning in water-stressed urban zones. These technologies collectively position the Rainwater Harvesting Systems market at the intersection of smart infrastructure and climate-resilient water management.

• In March 2024, Kingspan Group announced the expansion of its water and energy division manufacturing capacity in Europe, increasing rotational molding output for large-capacity rainwater storage tanks by approximately 20% to support rising demand in sustainable construction projects. Source: www.kingspan.com

• In September 2024, Graf Group introduced an upgraded Carat XXL underground rainwater tank system with storage capacities exceeding 76,000 liters, designed for commercial and municipal stormwater management projects, enhancing installation flexibility through modular extension units. Source: www.graf.info

• In February 2025, Watts Water Technologies launched an enhanced rainwater harvesting control panel integrating smart pump automation and remote monitoring compatibility, enabling facility managers to track system performance with digital dashboards and automated alerts.

• In May 2025, Stormsaver Ltd secured multiple large-scale commercial contracts across the UK for integrated rainwater harvesting systems in logistics and warehouse developments exceeding 50,000 square meters, reinforcing adoption in industrial real estate projects.

The Rainwater Harvesting Systems Market Report provides a comprehensive assessment of system types, applications, technologies, and regional demand patterns across residential, commercial, industrial, and agricultural sectors. The scope encompasses rooftop collection systems, surface runoff harvesting infrastructure, and underground integrated storage units with capacities ranging from 3,000 liters to more than 150,000 liters. The report evaluates filtration technologies, including mesh-based pre-filters, vortex separators, membrane filtration systems, and UV disinfection modules, as well as digital monitoring solutions integrated with building management systems.

Geographically, the analysis covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with detailed country-level insights for key markets such as the United States, Germany, China, India, Brazil, UAE, and South Africa. The report examines regulatory frameworks mandating on-site water reuse in over 50 metropolitan jurisdictions and assesses installation mandates for commercial properties exceeding 1,000 square meters.

Industry focus areas include green building certification compliance, stormwater management integration, ESG-driven freshwater reduction targets, and smart city infrastructure projects. The report further explores niche segments such as modular prefabricated systems, portable harvesting units for rural applications, and AI-driven rainfall analytics platforms. It provides quantitative insights into installation volume distribution, end-user adoption rates exceeding 40% in commercial segments, and storage capacity trends supporting decentralized water resilience strategies for infrastructure planners and corporate decision-makers.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

3.9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Kingspan Group, Graf Group, Watts Water Technologies, Rainwater Management Solutions, WISY AG, Innovative Water Solutions LLC, Ecozi Ltd, Heritage Tanks, Pioneer Water Tanks, Stormsaver Ltd, AquaHarvest Technologies |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |