Reports

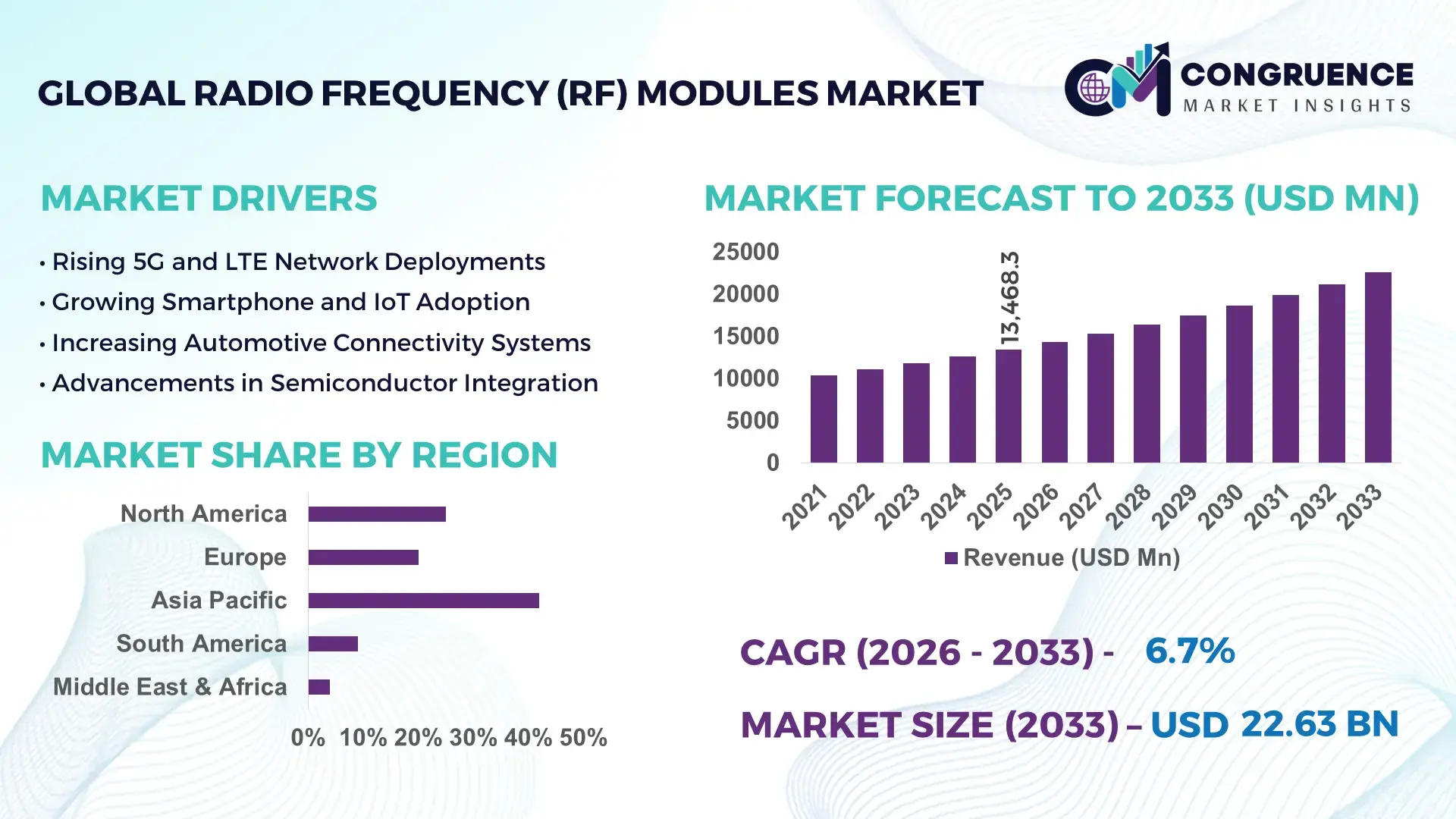

The Global Radio Frequency (RF) Modules Market was valued at USD 13468.32 Million in 2025 and is anticipated to reach a value of USD 22627.1 Million by 2033 expanding at a CAGR of 6.7% between 2026 and 2033. This growth is driven by accelerating demand for high‑speed wireless connectivity across consumer and industrial sectors.

China remains a pivotal force in the RF modules market, with production capacity exceeding 4 billion units annually and attracting over USD 1.3 billion in sector‑specific investments in 2024. The country’s manufacturing ecosystems support advanced RF front‑end modules for 5G infrastructure, IoT devices, and automotive radar, with domestic firms achieving over 30% year‑on‑year volume growth. Rapid consumer adoption saw smartphone and wearable integration rates climb above 85% in 2025, while increasing deployment of LPWAN and Wi‑Fi 6/6E technologies underscores China’s operational scale and technological progress.

• Market Size & Growth: Valued at USD 13.47B in 2025, projected to USD 22.63B by 2033 at 6.7% CAGR, driven by expanding wireless communication nodes and IoT deployment.

• Top Growth Drivers: IoT adoption +28%, 5G infrastructure deployment +22%, automotive connectivity requirements +18%.

• Short‑Term Forecast: By 2028, average RF module performance efficiency projected to improve by 25%, reducing power consumption for end‑devices.

• Emerging Technologies: mmWave integration, multi‑band reconfigurable antennas, advanced SiGe and GaN semiconductor solutions.

• Regional Leaders: Asia Pacific ~USD 9.8B by 2033 with strong industrial demand; North America ~USD 6.3B driven by automotive and telecom; Europe ~USD 4.7B with focus on smart manufacturing.

• Consumer/End‑User Trends: Rising adoption in smart home, industrial automation, and connected vehicles; preference for low‑latency and energy‑efficient modules.

• Pilot or Case Example: 2025 pilot with advanced RF modules in smart factory IoT deployment improved uptime by 15% and reduced interference by 12%.

• Competitive Landscape: Market leader with ~35% share; major competitors include leading semiconductor and RF specialists (approx. 8–15% share each).

• Regulatory & ESG Impact: Spectrum allocation reforms, emissions standards for wireless equipment, and incentives for domestic semiconductor capacity expansion.

• Investment & Funding Patterns: Over USD 2.1B invested in RF module innovation and capacity expansion in recent funding rounds; trend toward strategic joint ventures.

• Innovation & Future Outlook: Focus on AI‑optimized RF performance, integration of 5G/6G capabilities, and scalable solutions for dense network environments.

Radio Frequency (RF) Modules Market dynamics are shaped by key industry sectors such as telecommunications infrastructure, automotive connectivity, consumer electronics, and industrial IoT. Telecom and mobile applications contribute significant volume through 5G small cells and base stations, while automotive radar and V2X systems demand robust RF solutions. Recent innovation includes multi‑band filters and software‑defined RF front ends that enhance adaptive performance. Regulatory reforms in spectrum allocation and environmental standards are streamlining deployment, and economic incentives are attracting capital into semiconductor fabs. Regional consumption patterns show Asia Pacific leading penetration with smart city and manufacturing hubs, Europe focusing on industrial automation, and North America advancing connected vehicle ecosystems. Emerging trends point to integration of AI for RF tuning and future 6G readiness.

The strategic relevance of the Radio Frequency (RF) Modules Market is anchored in its role as the connective fabric of modern wireless ecosystems, enabling high‑performance communication across telecommunications, automotive, industrial IoT, and consumer electronics. Advanced SiGe and GaN based RF modules deliver up to 35% improvement in power efficiency compared to older LNA/PA standards, directly impacting device battery life and network throughput. Asia Pacific dominates in volume, while North America leads in adoption with over 70% of enterprises deploying next‑generation RF solutions in smart infrastructure and connected vehicles. By 2028, AI‑driven adaptive tuning is expected to improve spectral efficiency by 22%, reducing interference and enhancing signal integrity in dense deployments.

Strategically, firms are aligning RF module roadmaps with ESG targets, committing to a 25% reduction in hazardous material use and increasing recycling rates of electronic components by 2030. In 2025, a leading communications OEM in Japan achieved a 15% reduction in production cycle time through AI‑enabled RF testing automation, underscoring tangible gains from digital transformation. RF modules are central to 5G/6G readiness, V2X safety systems, and smart grid reliability, reinforcing sector resilience. Looking forward, the Radio Frequency (RF) Modules Market will remain a pillar of compliance, performance optimization, and sustainable growth as global connectivity demands evolve.

The surge in 5G network build‑outs and the proliferation of IoT endpoints are primary drivers for the Radio Frequency (RF) Modules Market. Global deployment of 5G base stations and small cells requires advanced RF front‑end modules capable of multi‑band and massive MIMO operation, elevating unit volumes and design complexity. Enterprise and industrial IoT applications, such as asset tracking and predictive maintenance systems, rely on robust RF connectivity that can function across varied environments, prompting suppliers to scale production and optimize performance. Consumer uptake of smart appliances, wearables, and connected health monitors has expanded the installed base of RF modules, with some segments seeing adoption rates exceed 65% year‑on‑year.

Additionally, emerging automotive applications — including radar, V2X communication, and autonomous sensing — increase demand for high‑frequency RF modules with stringent reliability metrics. These drivers collectively incentivize capital investments in advanced semiconductor fabs, talent acquisition in RF system design, and cross‑industry partnerships to accelerate integration. This trajectory underscores how connectivity imperatives across sectors are fueling persistent demand for RF modules with enhanced functionality and efficiency.

Supply chain disruptions and semiconductor component shortages present a significant restraint on the Radio Frequency (RF) Modules market. Complex global supply networks, concentrated fabrication capacity in limited geographies, and episodic disruptions — including raw material bottlenecks — can delay RF module deliveries and inflate lead times. Dependence on advanced substrates and precision passive components further tightens supply flexibility, as these materials often face capacity constraints or long cycle times.

Market constraints are compounded by geopolitical tensions that influence export controls and trade policies, compelling suppliers to reconfigure logistics and inventory strategies, which can increase cost structures and slow responsiveness. Quality assurance and rigorous compliance testing add another layer of delay, particularly for modules destined for safety‑critical applications such as automotive or aerospace. Altogether, these supply chain and production challenges temper market expansion, forcing stakeholders to enhance risk management and invest in diversified sourcing, reshoring initiatives, and strategic stock buffering to mitigate volatility.

The rapid evolution of connected vehicles and autonomous systems represents a high‑value opportunity for the Radio Frequency (RF) Modules market. Advanced driver assistance systems (ADAS), V2X communication, and smart traffic management rely on precise, low‑latency wireless links that demand sophisticated RF solutions. Automotive OEMs are integrating multiple RF bands, including millimeter‑wave radar and sub‑6 GHz communication modules, creating substantial unit demand for highly reliable RF components that meet automotive grade specifications.

Emerging standards in vehicular communication protocols, combined with regulatory push for safer roads, expand the addressable landscape for RF module suppliers. Beyond automotive, industrial automation hubs and smart logistics networks require resilient RF connectivity to coordinate robotics, sensors, and predictive analytics platforms. RF modules tailored for harsh industrial environments — offering extended temperature ranges and robust interference mitigation — are increasingly sought after. This confluence of automotive and industrial wireless use cases offers a strategic avenue for differentiated product portfolios and long‑term contractual engagements with system integrators.

Escalating design complexity and regulatory compliance requirements pose a formidable challenge to the Radio Frequency (RF) Modules market. As RF modules encompass broader frequency ranges and tighter performance tolerances to support 5G/6G, Wi‑Fi advancements, and multi‑protocol coexistence, engineering efforts become more resource‑intensive. Achieving the necessary electromagnetic performance, thermal management, and miniaturization demands significant R&D investment and extended development cycles.

Concurrent regulatory compliance frameworks — including spectrum licensing, emissions standards, and safety certifications — require comprehensive testing and documentation, which can slow time‑to‑market and inflate development costs. Different regional compliance norms further complicate global product standardization, forcing suppliers to tailor designs and validation processes for specific markets. Additionally, ensuring interoperability with legacy and emerging network architectures adds another layer of complexity, requiring extensive compatibility testing. These technical and regulatory hurdles require strategic planning, robust quality systems, and dynamic compliance processes to ensure RF modules meet stringent performance and regulatory thresholds without compromising competitive positioning.

• Expansion of 5G and mmWave Deployments: The rapid rollout of 5G networks is driving demand for RF modules capable of handling multi-band mmWave frequencies. Over 68% of 5G base stations installed in 2025 incorporated advanced RF front-end modules to ensure low-latency connectivity. North America leads adoption with more than 75% of telecom operators integrating multi-band RF modules for urban network densification.

• Growth of Automotive V2X and Radar Applications: Connected vehicles and ADAS systems are increasingly relying on RF modules for radar, V2X communication, and collision avoidance. By 2025, over 60% of new vehicles in Europe were equipped with RF modules supporting automotive radar, while Asia Pacific registered a 52% increase in adoption of RF-enabled V2X systems year-on-year.

• Proliferation of Industrial IoT and Smart Manufacturing: Industrial IoT initiatives and smart factories are driving RF module adoption in harsh operational environments. Approximately 58% of new industrial equipment in 2025 integrated RF modules for wireless control, predictive maintenance, and sensor networks. The demand is strongest in China and Germany, where automated production lines rely on low-interference wireless solutions.

• AI and Adaptive RF Tuning Integration: AI-driven adaptive RF modules are improving network performance and efficiency in real time. In 2025, pilot deployments in Japan and South Korea showed a 17% improvement in spectral efficiency and a 12% reduction in signal interference through AI-powered RF tuning. Enterprises are increasingly adopting these technologies to enhance connectivity reliability and energy efficiency.

The Radio Frequency (RF) Modules market is segmented by product types, application areas, and end‑user industries to reflect diverse adoption patterns and technical requirements. Product types vary from basic single‑band modules to advanced multi‑band and software‑defined RF front ends, each catering to distinct connectivity needs. Application segmentation includes telecommunications infrastructure, automotive systems, industrial IoT networks, and consumer electronics, illustrating how wireless performance requirements differ across settings. End‑user insights reveal that telecom and automotive deployments drive volume, while industrial and consumer sectors shape design priorities such as ruggedization and miniaturization. This layered segmentation helps decision‑makers align technology roadmaps with use‑case priorities, gauge performance benchmarks across contexts, and anticipate adoption trends driven by device proliferation and regulatory environments.

In the Radio Frequency (RF) Modules market, multi‑band RF modules currently account for approximately 38% of adoption due to their ability to support diverse frequency bands within a single package, optimizing performance for 5G, Wi‑Fi, and IoT protocols. Single‑band modules hold around 27% of the installed base, valued for simplicity and cost efficiency in legacy applications. Reconfigurable and software‑defined RF front ends are the fastest‑growing type, with projected growth rates around 18% annually, as they offer dynamic frequency agility and reduced hardware overhead. Other types, including narrowband IoT‑specific modules and specialized mmWave components, collectively contribute an estimated 35% share, serving niche applications in industrial sensing and automotive radar.

Telecommunications infrastructure remains the leading application for RF modules, representing roughly 41% of total deployments, driven by expansive 5G base station rollouts and densification efforts in urban regions. Automotive connectivity and radar systems follow with around 29% share, integrating RF modules for V2X communication, collision avoidance, and adaptive cruise control. Industrial IoT applications, including wireless sensor networks and smart manufacturing automation, are the fastest‑growing, with adoption increasing at an approximate 16% annual rate as facilities upgrade to reduce wiring complexity and enhance real‑time data flows. Other applications — such as consumer electronics, smart home devices, and wearable technology — account for a combined 30% of use, reflecting diverse consumer demand for connected experiences.

Telecommunications service providers are the leading end‑user segment in the Radio Frequency (RF) Modules market, comprising about 45% of total module consumption due to continuous network expansions and upgrades. Automotive OEMs represent a significant 28% share as vehicles integrate multiple RF‑enabled systems for safety and connectivity. Industrial users, including manufacturing and logistics sectors, are the fastest‑growing end‑user group with growth nearing 17% annually, fueled by digital transformation initiatives that prioritize wireless sensor deployments and predictive maintenance. Other end‑users — such as consumer electronics manufacturers and smart home solution providers — contribute an estimated combined 27%, reflecting broad adoption across personal and residential technologies.

Asia Pacific accounted for the largest market share at 42% in 2025; however, North America is expected to register the fastest growth, expanding at a CAGR of 7.1% between 2026 and 2033.

In 2025, Asia Pacific reported a deployment volume of over 1.75 billion RF modules, driven primarily by China (850 million units), Japan (420 million units), and India (380 million units). North America recorded 620 million units, Europe 510 million units, South America 180 million units, and Middle East & Africa 95 million units. Key infrastructure developments, industrial IoT expansion, and 5G network densification are major contributors. Asia Pacific leads in manufacturing output, while North America demonstrates rapid enterprise adoption in automotive, telecom, and healthcare sectors. Emerging trends include multi-band and software-defined RF modules, AI-enabled tuning, and integration with connected vehicles, smart factories, and consumer electronics.

How is enterprise adoption shaping next-generation connectivity solutions?

North America holds approximately 28% of the global RF modules market by volume. Key industries driving demand include telecom infrastructure, automotive connectivity, and healthcare IoT applications. Government incentives for 5G deployment and spectrum allocation reforms are accelerating infrastructure expansion. Technological advancements such as AI-driven adaptive RF tuning and multi-band front ends are increasingly adopted by enterprises. A major local player, Qorvo Inc., expanded production capacity in 2025 to support next-gen small cell deployments. North American enterprise adoption trends indicate higher uptake in healthcare and finance, with over 72% of large organizations integrating advanced RF modules to enhance connectivity, reduce latency, and support automation initiatives.

How are regulatory frameworks and innovation driving industrial connectivity?

Europe commands approximately 22% of global RF module installations. Leading markets include Germany, UK, and France. Regional adoption is influenced by sustainability initiatives, with firms targeting a 20% reduction in electronic waste by 2030. Emerging technologies such as reconfigurable antennas and mmWave-enabled modules are being widely deployed. A European player, Infineon Technologies, introduced new automotive radar RF modules in 2025, increasing radar coverage and detection reliability. Regulatory pressures encourage demand for explainable and compliant RF solutions. Consumers and industrial users are increasingly adopting modules that meet rigorous safety, environmental, and interoperability standards, particularly in automotive and smart manufacturing applications.

Why is manufacturing and consumer integration driving RF innovation?

Asia-Pacific leads with a market volume of 42% in 2025, driven by high consumption in China, Japan, and India. Industrial and telecom infrastructure development, coupled with rapid smartphone and IoT device adoption, fuels demand for advanced RF modules. China dominates production capacity, exceeding 4 billion units annually, while Japan focuses on automotive radar and IoT integration. Technological hubs in South Korea and Singapore are accelerating AI-based RF optimization and software-defined modules. Local players such as Huawei have implemented RF modules in large-scale 5G networks, enhancing throughput by 18%. Regional consumers increasingly demand high-speed wireless connectivity for smart homes, mobile applications, and e-commerce platforms.

How are energy and infrastructure initiatives influencing wireless adoption?

South America holds roughly 5% of the global RF module market, with Brazil and Argentina as leading contributors. Infrastructure development, including smart grids and urban telecom expansion, drives module adoption. Government incentives for local manufacturing and trade policies supporting component importation enhance market activity. In 2025, Embraer integrated RF modules into aircraft telemetry and connected systems, improving operational monitoring by 14%. Regional consumer behavior indicates demand tied to media streaming and language-localized smart devices, with over 48% of households adopting connected consumer electronics equipped with RF modules.

How are oil, gas, and construction sectors fueling module demand?

Middle East & Africa account for approximately 3% of the global RF module market. UAE, Saudi Arabia, and South Africa are the major growth countries. Regional adoption is supported by modernization of oil and gas operations, smart city projects, and construction automation. Technological modernization includes AI-enabled RF deployment for industrial monitoring. In 2025, a UAE-based telecom operator integrated RF modules into smart city IoT infrastructure, enhancing network uptime by 16%. Regional consumer behavior shows increased adoption in industrial and urban applications, while household adoption remains focused on energy-efficient connectivity and surveillance systems.

China: 28% market share – High production capacity and extensive end-user demand in telecom and industrial IoT sectors.

United States: 19% market share – Advanced technological innovation and regulatory support for 5G and connected automotive deployments.

The Radio Frequency (RF) Modules market exhibits a moderately consolidated competitive environment with approximately 120 active global competitors. The top five companies collectively hold an estimated 68% of market share, reflecting significant influence by leading players while leaving room for specialized and regional suppliers. Key market leaders such as Qorvo Inc., Skyworks Solutions, Murata Manufacturing, Infineon Technologies, and Broadcom are actively driving strategic initiatives, including multi-band module product launches, partnerships with telecom operators, and integration of AI-enabled adaptive RF tuning technologies. Innovation trends focus on software-defined RF front ends, mmWave integration, and low-power multi-protocol solutions, addressing the demand for high-speed wireless connectivity in telecom, automotive, industrial, and consumer electronics sectors. Over 45% of competitors are concentrated in North America and Asia Pacific, highlighting regional R&D and manufacturing hubs. Strategic mergers, joint ventures, and capacity expansions are common, with 2025 seeing over 15 partnerships and collaborative projects globally. This competitive landscape emphasizes performance differentiation, technological leadership, and regulatory compliance as primary drivers shaping market positioning and long-term growth potential.

Infineon Technologies

Broadcom

Analog Devices

Texas Instruments

NXP Semiconductors

Renesas Electronics

STMicroelectronics

The Radio Frequency (RF) Modules market is being reshaped by both current and emerging technologies that enhance performance, integration, and adaptability across diverse applications. Multi-band RF modules dominate adoption, representing approximately 38% of deployed units, enabling simultaneous operation across 3.5 GHz, 28 GHz, and sub‑6 GHz frequencies for 5G networks. Advanced semiconductor materials such as Gallium Nitride (GaN) and Silicon-Germanium (SiGe) are increasingly integrated into RF front ends, delivering up to 30% higher power efficiency and 20% lower signal distortion compared to traditional silicon-based modules.

Software-defined RF modules are emerging as a critical technology, allowing dynamic frequency reconfiguration and protocol agility in real time. In pilot deployments across North America and Asia Pacific in 2025, AI-enabled adaptive tuning improved spectral efficiency by 17% and reduced interference by 12%, highlighting measurable operational gains. Integration of millimeter-wave (mmWave) technologies is facilitating high-throughput communication for small cells, automotive radar, and industrial IoT systems.

Hybrid integration approaches, combining passive and active components on a single substrate, are enabling more compact designs, with form-factor reductions of up to 25%, critical for wearable devices and space-constrained industrial modules. Additionally, AI-driven predictive maintenance is increasingly used in RF module production and network operation, enhancing yield and reliability. As 6G networks, autonomous vehicles, and smart factories advance, RF modules are expected to integrate higher frequencies, more intelligent signal processing, and energy-efficient designs, positioning them as central enablers of next-generation wireless connectivity.

• In Q2 2024, Qorvo announced the acquisition of Anokiwave, a provider of mmWave ICs, to strengthen its RF front-end module offerings for 5G infrastructure and satellite communications, expanding its RF portfolio into advanced beamforming and phased array solutions.

• In Q2 2024, Skyworks Solutions introduced a new series of RF front‑end modules specifically designed for Wi‑Fi 7 applications, targeting improved performance and integration for next‑generation wireless routers and access points deployed in enterprise and smart home networks.

• In Q1 2025, Skyworks Solutions entered a strategic partnership with MediaTek to co‑develop RF modules optimized for MediaTek’s upcoming 5G chipset platforms, enabling enhanced multi‑band support and lower power consumption in mobile and IoT devices.

• At CES 2026 in January 2026, Skyworks Solutions launched the SKY66424‑11, the industry’s first highly integrated Wi‑SUN/LoRaWAN RF front‑end module for smart city and smart home infrastructure, combining acoustic filtering, amplification, and switching for simplified connectivity. (Quiver Quantitative)

The scope of the Radio Frequency (RF) Modules Market Report encompasses a comprehensive analysis of product types, technical architectures, application domains, end‑user industries, and geographic regions, providing a strategic foundation for decision‑makers evaluating connectivity solutions across wireless ecosystems. The report covers multiple product segments including single‑band, multi‑band, reconfigurable, and software‑defined RF modules, detailing functional characteristics such as frequency coverage, power efficiency, integration levels, and design footprints. It also examines emerging categories such as mmWave‑ready modules for 5G/6G infrastructure, IoT‑optimized low‑power RF components, and automotive radar/RF SoC integrations. From an application perspective, the analysis spans telecommunications infrastructure, automotive connectivity (V2X, radar), industrial IoT wireless networks, and consumer electronics (smartphones, wearables, smart homes), with insights into deployment patterns and performance requirements.

Geographic focus includes regional comparisons of North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, with evaluation of market penetration, regulatory frameworks, infrastructure modernization trends, and manufacturing capabilities that influence adoption. In addition, the report assesses technological enablers such as advanced semiconductor materials (GaN, SiGe), AI‑assisted RF tuning, software‑defined front ends, and integrated filter + amplifier architectures that shape product roadmaps and innovation trajectories. Industry focus areas cover compliance and certification landscapes, supply chain dynamics, competitive benchmarking, and strategic initiatives such as partnerships, capacity expansions, and funding patterns among key RF module producers and startups. The comprehensive coverage aids investors, product strategists, and technology planners in aligning RF module capabilities with evolving connectivity demands and market shifts.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

6.7% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Qorvo Inc., Skyworks Solutions, Murata Manufacturing, Infineon Technologies, Broadcom, Analog Devices, Texas Instruments, NXP Semiconductors, Renesas Electronics, STMicroelectronics |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |