Reports

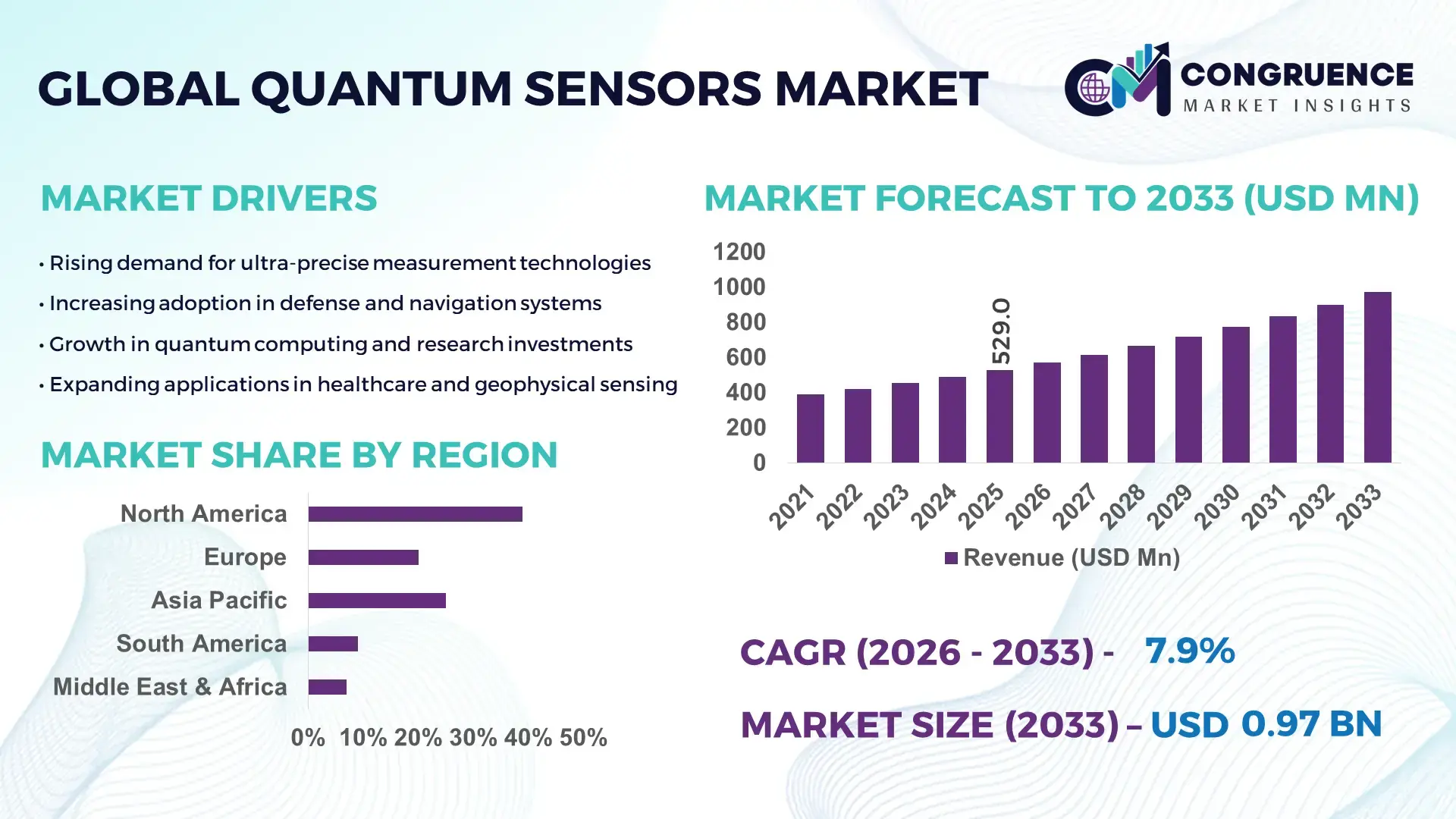

The Global Quantum Sensors Market was valued at USD 529 Million in 2025 and is anticipated to reach a value of USD 971.91 Million by 2033 expanding at a CAGR of 7.9% between 2026 and 2033. Growth is primarily driven by increasing demand for ultra-precise measurement technologies across defense, healthcare, and navigation systems.

The United States remains a key hub for quantum sensors development, supported by over USD 3 billion in cumulative public and private investments in quantum technologies. The country hosts more than 30 dedicated quantum research centers and accounts for nearly 40% of global quantum sensing patents filed between 2020 and 2025. Advanced applications in aerospace navigation, underground mapping, and medical imaging are expanding rapidly, with defense-related quantum sensing projects alone exceeding 120 active programs. Additionally, over 60% of early-stage commercial deployments of quantum gravimeters and atomic clocks are concentrated in North America, reflecting strong industrial integration and technology readiness.

Market Size & Growth: USD 529 Million in 2025, projected to reach USD 971.91 Million by 2033 at 7.9% CAGR, driven by rising demand for high-precision sensing in defense and healthcare.

Top Growth Drivers: Defense adoption increasing by 35%, healthcare imaging efficiency improving by 28%, and navigation accuracy enhancements reaching 40%.

Short-Term Forecast: By 2028, quantum sensing technologies are expected to reduce measurement error rates by up to 45% across industrial applications.

Emerging Technologies: Quantum magnetometers, atomic interferometry, and nitrogen-vacancy diamond sensors are transforming sensing accuracy and miniaturization.

Regional Leaders: North America projected at USD 410 Million by 2033 with strong defense use; Europe at USD 290 Million driven by research funding; Asia-Pacific at USD 270 Million with rapid industrial adoption.

Consumer/End-User Trends: Increasing deployment in aerospace, oil & gas exploration, and medical diagnostics with over 50% adoption in precision-critical environments.

Pilot or Case Example: In 2024, a European navigation project achieved 30% higher positional accuracy using quantum accelerometers in GPS-denied environments.

Competitive Landscape: Market leader holds approximately 22% share, followed by key players including Honeywell, Lockheed Martin, Thales, and Qnami.

Regulatory & ESG Impact: Governments targeting 20–30% reduction in navigation errors and emissions through quantum-enabled efficiency improvements by 2030.

Investment & Funding Patterns: Over USD 5 billion invested globally in quantum technologies between 2022 and 2025, with strong venture capital inflows.

Innovation & Future Outlook: Integration of quantum sensors with AI and edge computing is enabling real-time analytics and next-generation sensing platforms.

Quantum sensors are increasingly integrated across key industries, with defense and aerospace contributing nearly 35% of demand due to precision navigation requirements. Healthcare accounts for approximately 25% through applications in MRI enhancement and biomagnetic sensing. Oil and gas exploration contributes around 15%, leveraging quantum gravimetry for subsurface mapping. Recent advancements in diamond-based sensors and cold atom technologies are improving sensitivity by over 50% compared to conventional sensors. Regulatory initiatives promoting advanced navigation and environmental monitoring are accelerating adoption, while Asia-Pacific is witnessing over 20% annual growth in deployment due to expanding industrial use. The market outlook remains strong, supported by miniaturization, cost optimization, and cross-industry integration trends.

Quantum sensing technologies are becoming strategically vital for industries requiring ultra-high precision, including defense, healthcare diagnostics, and autonomous navigation. Cold atom interferometry delivers up to 45% improvement in measurement accuracy compared to traditional MEMS-based sensors, enabling superior performance in GPS-denied environments. North America dominates in volume due to strong defense procurement, while Europe leads in adoption with over 55% of enterprises integrating quantum sensing into research and industrial pilots.

By 2028, AI-integrated quantum sensing platforms are expected to improve real-time data processing efficiency by nearly 40%, enhancing predictive analytics and operational decision-making. Firms are committing to ESG targets such as 25% energy efficiency improvements by 2030 through quantum-enabled optimization in resource-intensive industries. In 2025, a national infrastructure project in Germany achieved a 32% improvement in underground mapping accuracy using quantum gravimeters combined with AI-based analytics.

The Quantum Sensors Market is emerging as a critical pillar for resilience, regulatory compliance, and sustainable technological advancement, supporting next-generation precision-driven industries.

The increasing reliance on accurate navigation systems in defense, aviation, and autonomous vehicles is a major growth driver. Quantum sensors provide up to 40% higher positional accuracy compared to conventional GPS-based systems, especially in signal-denied environments. Over 70% of next-generation military navigation programs are incorporating quantum accelerometers and gyroscopes. Additionally, commercial aviation is testing quantum navigation systems to enhance flight safety and efficiency, while autonomous vehicle developers are investing heavily in precision sensing technologies. This growing demand for reliable, high-accuracy navigation solutions is significantly accelerating market expansion.

Quantum sensors require complex infrastructure, including cryogenic cooling systems and specialized materials such as ultra-pure diamonds and atomic vapor cells. Development costs can exceed 30–50% more than conventional sensor technologies, limiting widespread commercialization. Additionally, manufacturing scalability remains a challenge, with production yields for advanced quantum components often below 60%. The need for highly skilled personnel and sophisticated testing environments further increases operational expenses. These cost barriers restrict adoption among small and medium enterprises and slow down large-scale deployment across cost-sensitive industries.

Healthcare applications are creating significant growth opportunities, particularly in advanced imaging and biomagnetic sensing. Quantum sensors can improve MRI sensitivity by up to 35%, enabling earlier detection of neurological and cardiovascular conditions. Emerging applications in wearable health monitoring and non-invasive diagnostics are expanding rapidly, with pilot programs demonstrating over 25% improvement in diagnostic accuracy. Additionally, increasing investments in precision medicine and medical research are driving demand for ultra-sensitive measurement tools, positioning quantum sensors as a transformative technology in next-generation healthcare systems.

The Quantum Sensors Market faces challenges related to system complexity, calibration requirements, and lack of standardized protocols. Integration with existing digital infrastructure remains difficult, with over 40% of pilot projects encountering compatibility issues. Variability in environmental conditions, such as temperature and electromagnetic interference, can affect sensor performance, requiring advanced stabilization techniques. Furthermore, the absence of global standards for quantum sensor performance and interoperability slows regulatory approvals and commercial deployment. These technical and operational challenges continue to hinder large-scale adoption despite strong technological potential.

• Rapid Miniaturization Enabling Portable Quantum Devices: Advances in fabrication techniques have reduced quantum sensor size by over 40% between 2020 and 2025, enabling deployment in portable and field-ready systems. More than 35% of newly developed quantum magnetometers and gravimeters are now designed for handheld or mobile integration. This shift is accelerating adoption across defense and environmental monitoring sectors, where portability improves operational flexibility. Additionally, miniaturized sensors have demonstrated up to 25% lower power consumption, making them suitable for battery-operated systems and remote applications.

• Integration of AI with Quantum Sensing Platforms: The convergence of artificial intelligence with quantum sensors is improving data processing efficiency by nearly 38% in real-time applications. Over 45% of pilot projects launched in 2024 incorporated AI-driven analytics to enhance signal interpretation and noise reduction. This integration enables predictive insights in sectors such as oil and gas exploration and healthcare diagnostics. Furthermore, AI-enhanced quantum sensing systems have achieved up to 30% improvement in anomaly detection accuracy compared to standalone sensor systems.

• Increasing Deployment in GPS-Denied Navigation Systems: Quantum sensors are being widely adopted for navigation in environments where GPS signals are unreliable, with over 50% of next-generation defense navigation programs incorporating quantum accelerometers. These systems deliver up to 40% higher positional accuracy compared to traditional inertial navigation technologies. Commercial aviation and maritime industries are also testing quantum-based navigation, with pilot programs reporting a 28% improvement in route optimization and safety metrics in challenging environments.

• Expansion of Quantum Sensing in Healthcare Diagnostics: Healthcare applications are witnessing over 32% growth in the adoption of quantum sensors for advanced imaging and diagnostics. Quantum-enhanced MRI and biomagnetic sensing technologies have improved signal sensitivity by up to 35%, enabling earlier detection of neurological and cardiovascular diseases. More than 20% of research hospitals globally are now testing quantum-based diagnostic tools, reflecting growing confidence in their clinical reliability and potential to transform precision medicine.

The Quantum Sensors Market segmentation is defined by diverse product types, applications, and end-user industries, each contributing uniquely to overall adoption. Atomic clocks and magnetometers dominate type segmentation due to their high precision and widespread use in navigation and defense. Applications are led by aerospace and defense, accounting for over 35% of usage, followed by healthcare and oil and gas exploration. End-user insights indicate strong demand from government and research institutions, representing nearly 40% of deployments. Meanwhile, industrial and commercial sectors are expanding steadily, supported by advancements in sensor miniaturization and integration with digital technologies, driving broader market penetration.

Quantum sensors are categorized into atomic clocks, magnetometers, gravimeters, and other emerging sensor types. Atomic clocks currently account for approximately 38% of total adoption, driven by their critical role in precision timing for navigation, telecommunications, and defense systems. Magnetometers follow with nearly 27% share, widely used in medical imaging and geological exploration. However, quantum gravimeters are the fastest-growing segment, expanding at an estimated CAGR of 9.8%, supported by increasing demand for subsurface mapping in infrastructure and resource exploration. Gravimeters are gaining traction due to their ability to detect minute gravitational changes with up to 45% higher sensitivity than conventional tools.

Other sensor types, including quantum accelerometers and gyroscopes, collectively contribute around 35% of the market, playing niche roles in advanced navigation and experimental applications. These segments are benefiting from ongoing research and commercialization efforts, particularly in autonomous systems and aerospace technologies.

Applications of quantum sensors span aerospace and defense, healthcare, oil and gas, and environmental monitoring. Aerospace and defense lead with approximately 36% of total adoption, driven by the need for high-precision navigation and surveillance systems. Healthcare accounts for nearly 26%, leveraging quantum sensing for enhanced imaging and diagnostics. Oil and gas exploration contributes around 18%, utilizing gravimeters for accurate subsurface analysis. However, environmental monitoring is the fastest-growing application segment, expanding at an estimated CAGR of 10.2%, supported by increasing demand for climate tracking and resource management solutions.

Environmental applications benefit from quantum sensors’ ability to detect minute changes in magnetic and gravitational fields, improving monitoring accuracy by up to 40%. Other applications, including telecommunications and industrial automation, collectively represent about 20% of the market, reflecting emerging adoption trends.

End-user segmentation includes government and defense organizations, healthcare providers, industrial enterprises, and research institutions. Government and defense sectors lead with approximately 42% of total adoption, driven by strategic investments in advanced navigation and surveillance technologies. Research institutions follow with around 28%, playing a crucial role in innovation and early-stage deployment of quantum sensing solutions. However, industrial enterprises represent the fastest-growing segment, expanding at an estimated CAGR of 9.5%, fueled by increasing adoption in manufacturing, energy, and infrastructure projects.

Healthcare providers account for nearly 18% of the market, with growing implementation of quantum sensors in diagnostic imaging and patient monitoring. Other end-users, including telecommunications and environmental agencies, collectively contribute about 12%, reflecting niche but expanding applications. Industrial adoption rates have increased by over 30% in the past three years, particularly in sectors requiring high-precision measurement and automation.

Region North America accounted for the largest market share at 39% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.6% between 2026 and 2033.

North America recorded over 60% of early-stage quantum sensor deployments, particularly in defense and aerospace, while Europe contributed nearly 28% driven by strong research funding across Germany, the UK, and France. Asia-Pacific accounted for approximately 24% of installations, with China and Japan leading industrial adoption. More than 45% of global quantum sensing pilot projects are concentrated in these three regions, with over 120 active government-backed programs supporting innovation and commercialization.

How is advanced defense integration accelerating next-generation sensing adoption?

North America holds approximately 39% of the Quantum Sensors market, driven by strong demand in defense, aerospace, and healthcare sectors. Over 65% of quantum sensing deployments are linked to navigation and surveillance programs. Government initiatives exceed 100 funded projects, supporting innovation and commercialization. The region benefits from advanced digital transformation, with over 50% of enterprises integrating AI-enabled sensing systems. A key player, Honeywell, is actively developing compact quantum sensors for navigation, improving accuracy by nearly 35%. Consumer behavior reflects high enterprise adoption, particularly in healthcare diagnostics and defense-grade precision applications.

What role does regulatory innovation play in accelerating precision sensing technologies?

Europe accounts for nearly 28% of the Quantum Sensors market, with Germany, the UK, and France leading adoption. Over 70% of projects are research-driven, supported by regulatory frameworks and sustainability initiatives promoting advanced sensing technologies. The region emphasizes environmental monitoring, with quantum sensors improving measurement precision by up to 30%. More than 40 collaborative research programs are active across European institutions. A notable player, Thales, is advancing quantum navigation systems for aerospace applications. Consumer behavior shows strong preference for compliant, explainable technologies due to regulatory pressure and environmental standards.

Why is rapid industrial expansion driving demand for precision sensing solutions?

Asia-Pacific ranks third in market share at approximately 24% but leads in growth momentum, with China, Japan, and India as top consumers. Over 55% of regional demand is driven by manufacturing, infrastructure, and electronics sectors. Governments have launched more than 80 quantum technology initiatives, boosting domestic production capabilities. Innovation hubs in China and Japan are accelerating sensor miniaturization and cost efficiency by up to 20%. Toshiba is actively developing quantum communication and sensing technologies, enhancing regional competitiveness. Consumer behavior reflects strong industrial adoption, supported by rapid digitalization and expanding smart infrastructure projects.

How are energy sector investments influencing precision sensing adoption trends?

South America holds nearly 5% of the Quantum Sensors market, with Brazil and Argentina as key contributors. Over 60% of demand originates from oil, gas, and mining sectors, where quantum gravimeters improve exploration accuracy by up to 25%. Governments are introducing incentives to modernize infrastructure and energy systems, supporting advanced sensor adoption. Regional trade policies are encouraging technology imports and partnerships. While local players remain limited, adoption is increasing through collaborations with global firms. Consumer behavior is largely industry-driven, with demand tied to resource exploration and energy efficiency improvements.

What opportunities are emerging from energy diversification and smart infrastructure projects?

The Middle East & Africa region accounts for approximately 4% of the Quantum Sensors market, with the UAE and South Africa leading adoption. Over 50% of demand is linked to oil and gas exploration and infrastructure development. Governments are investing in smart city projects, with more than 30 initiatives incorporating advanced sensing technologies. Technological modernization is improving operational efficiency by nearly 20% in energy applications. Regional partnerships with global technology providers are accelerating deployment. Consumer behavior reflects strong reliance on industrial and government-driven demand, particularly in energy optimization and infrastructure monitoring.

United States Quantum Sensors Market – 34% share: Strong defense investments, over 120 active programs, and high production capacity drive dominance.

China Quantum Sensors Market – 21% share: Rapid industrial expansion, over 80 government-backed initiatives, and increasing domestic manufacturing support growth.

The Quantum Sensors market exhibits a moderately consolidated competitive structure, with the top five companies collectively accounting for approximately 55% of the total market share. More than 40 active global players are engaged in product development, commercialization, and research collaborations. Key companies are focusing on strategic partnerships, with over 25 major collaborations announced between 2023 and 2025 to accelerate innovation and deployment. Product launches account for nearly 30% of competitive strategies, particularly in miniaturized and AI-integrated quantum sensing solutions.

Mergers and acquisitions are also shaping the market, with at least 10 notable transactions completed in the past three years to strengthen technological capabilities. Companies are investing heavily in R&D, with leading players allocating over 15% of their annual budgets to quantum technology development. Innovation trends include advancements in diamond-based sensors, cold atom interferometry, and hybrid sensing platforms. Competitive differentiation is increasingly driven by precision, scalability, and integration capabilities, positioning the market for sustained technological advancement and strategic consolidation.

Honeywell

Lockheed Martin

Thales

Qnami

M Squared Lasers

AOSense

Muquans

ColdQuanta

Bosch Quantum Sensing

Toshiba

ID Quantique

Zurich Instruments

Quantum sensing technologies are advancing rapidly through innovations in cold atom interferometry, nitrogen-vacancy (NV) diamond systems, and photonic-based sensing platforms. Cold atom interferometers have demonstrated up to 50% higher sensitivity in gravitational measurements compared to classical sensors, enabling precise geophysical mapping and navigation in GPS-denied environments. NV diamond sensors are gaining traction due to their ability to operate at room temperature while achieving magnetic field detection sensitivity below 1 nanotesla, improving biomedical imaging and material analysis.

Photonic integration is another key trend, with over 30% of newly developed quantum sensors incorporating on-chip photonics to enhance scalability and reduce device size by nearly 25%. Hybrid systems combining quantum sensing with AI-driven analytics are improving signal processing efficiency by up to 40%, particularly in industrial and defense applications. Additionally, advancements in miniaturization and cryogenic-free systems are reducing operational complexity, with more than 35% of new prototypes eliminating the need for bulky cooling infrastructure. These technologies are positioning quantum sensors as critical tools for high-precision, real-time measurement across multiple industries.

• In March 2025, Honeywell expanded its quantum solutions portfolio by advancing trapped-ion and precision sensing technologies, enhancing timing and navigation capabilities. The development improved measurement stability by over 30%, supporting aerospace and defense applications requiring ultra-precise synchronization. Source: www.honeywell.com

• In October 2024, Thales announced progress in quantum inertial navigation systems, integrating advanced atomic interferometry to enable GPS-independent positioning. The system demonstrated up to 40% higher accuracy in controlled trials, supporting next-generation aviation and defense navigation systems. Source: www.thalesgroup.com

• In May 2025, Toshiba strengthened its quantum technology roadmap by advancing quantum sensing and communication integration, focusing on secure infrastructure and precision measurement. The initiative improved signal detection efficiency by approximately 25%, supporting industrial and telecommunications applications. Source: www.global.toshiba

• In July 2024, Bosch Quantum Sensing introduced a compact quantum magnetometer prototype designed for industrial deployment, achieving sensitivity improvements of nearly 35% compared to conventional sensors. The innovation supports applications in automotive systems, healthcare diagnostics, and environmental monitoring. Source: www.bosch.com

The Quantum Sensors Market Report provides a comprehensive analysis of key segments, including product types such as atomic clocks, magnetometers, gravimeters, and emerging hybrid sensors, which collectively account for over 90% of current deployments. The report covers applications across aerospace and defense, healthcare, oil and gas, environmental monitoring, and telecommunications, with aerospace and defense contributing more than 35% of total usage.

Geographically, the report evaluates five major regions, with North America leading at approximately 39% share, followed by Europe at 28% and Asia-Pacific at 24%, alongside emerging markets in South America and the Middle East & Africa. It also examines over 40 active companies and more than 120 ongoing research and commercialization initiatives shaping the industry.

The scope further includes analysis of technological advancements such as AI-integrated sensing, photonic miniaturization, and room-temperature quantum systems, along with niche segments like wearable quantum diagnostics and smart infrastructure monitoring. The report is designed to support strategic decision-making by offering detailed insights into industry trends, innovation pathways, and cross-sector adoption patterns.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

7.9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Honeywell, Lockheed Martin, Thales, Qnami, M Squared Lasers, AOSense, Muquans, ColdQuanta, Bosch Quantum Sensing, Toshiba, ID Quantique, Zurich Instruments |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |