Reports

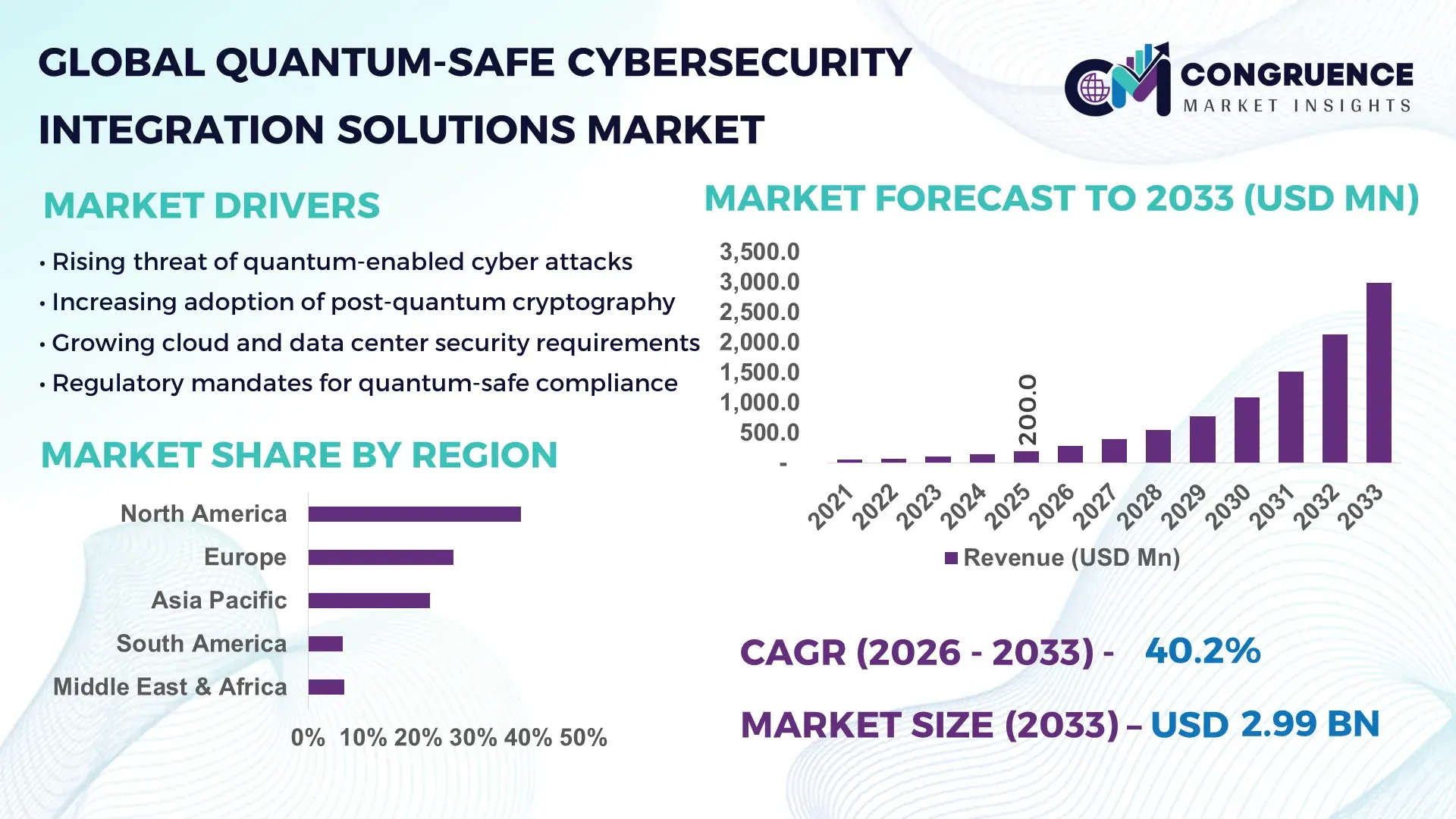

The Global Quantum-Safe Cybersecurity Integration Solutions Market was valued at USD 200.0 Million in 2025 and is anticipated to reach a value of USD 2,985.5 Million by 2033 expanding at a CAGR of 40.2% between 2026 and 2033, according to an analysis by Congruence Market Insights. The rapid acceleration of quantum computing research and the increasing vulnerability of conventional encryption algorithms are compelling enterprises and governments to adopt quantum-resistant cybersecurity frameworks to protect critical digital infrastructure.

The United States plays a central role in the Quantum-Safe Cybersecurity Integration Solutions Market, supported by strong R&D investments and advanced cybersecurity infrastructure. The U.S. government allocated more than USD 1.8 billion under the National Quantum Initiative Act to accelerate quantum computing and quantum-safe cryptography research. Over 62% of large U.S. enterprises are already conducting pilot programs for post-quantum cryptography (PQC) migration, particularly in financial services and defense systems. In addition, the U.S. Department of Homeland Security and NIST are collaborating with more than 120 technology vendors to standardize quantum-resistant encryption protocols. Adoption within federal agencies has also accelerated, with nearly 45% of government IT systems currently undergoing cryptographic inventory assessments to prepare for PQC deployment.

Market Size & Growth: The market is valued at USD 200.0 Million in 2025 and projected to reach USD 2,985.5 Million by 2033, expanding at a 40.2% CAGR, primarily driven by accelerating quantum computing development and enterprise migration toward post-quantum encryption frameworks.

Top Growth Drivers: Increasing enterprise cryptographic upgrades (48% adoption growth), expansion of quantum computing R&D programs (35% increase in funding initiatives), and rising cyberattack sophistication requiring advanced encryption (42% improvement in threat detection frameworks).

Short-Term Forecast: By 2028, enterprises integrating quantum-safe cryptographic systems are expected to achieve 30% reduction in encryption vulnerability exposure and 25% improvement in long-term data protection resilience.

Emerging Technologies: Rapid deployment of post-quantum cryptography (PQC) algorithms, hybrid cryptographic architectures, and quantum key distribution (QKD) platforms are transforming enterprise cybersecurity infrastructure.

Regional Leaders: North America projected to reach USD 1.25 billion by 2033 with strong government cybersecurity initiatives; Europe expected to approach USD 820 million supported by digital sovereignty programs; Asia-Pacific forecast to exceed USD 650 million driven by large-scale telecom and fintech adoption.

Consumer/End-User Trends: Financial institutions, defense agencies, and cloud infrastructure providers account for over 60% of current deployments, with rising adoption across healthcare and critical infrastructure sectors.

Pilot or Case Example: In 2024, a national telecom provider implemented hybrid post-quantum encryption in its network backbone, achieving 40% improvement in cryptographic resilience and reducing data interception risk by 35%.

Competitive Landscape: The market leader holds approximately 18% share, while major competitors include several global cybersecurity providers and cloud infrastructure companies competing through PQC integration and cryptographic migration platforms.

Regulatory & ESG Impact: Government cybersecurity frameworks and data protection regulations now mandate quantum-readiness roadmaps, with over 70% of developed economies introducing national PQC migration strategies.

Investment & Funding Patterns: Global investments in quantum cybersecurity research exceeded USD 3.5 billion between 2022 and 2025, with increasing venture capital participation and public-private cybersecurity partnerships.

Innovation & Future Outlook: Ongoing innovations in quantum-resistant algorithms, cryptographic inventory automation, and hybrid encryption frameworks are expected to accelerate enterprise migration and strengthen long-term digital infrastructure security.

Quantum-Safe Cybersecurity Integration Solutions Market adoption is expanding across banking, defense, telecommunications, and healthcare sectors, collectively contributing over 65% of enterprise deployments. Recent innovations include hybrid post-quantum encryption platforms and automated cryptographic discovery tools that help enterprises identify vulnerable encryption systems. Regulatory mandates for quantum readiness in national cybersecurity frameworks are driving demand, while Asia-Pacific enterprises recorded a 38% increase in quantum-safe pilot programs in 2025, indicating strong forward adoption momentum.

The strategic relevance of the Quantum-Safe Cybersecurity Integration Solutions Market lies in its critical role in safeguarding long-term digital assets against the emerging threat of quantum-enabled cyberattacks. With quantum computers expected to break traditional encryption algorithms such as RSA and ECC, organizations are accelerating the migration toward post-quantum cryptographic infrastructures. Enterprises managing highly sensitive data—including financial institutions, healthcare providers, and defense organizations—are prioritizing early adoption of quantum-resistant frameworks to ensure long-term data confidentiality and compliance with evolving cybersecurity standards.

Post-quantum cryptography (PQC) is rapidly emerging as the cornerstone technology for next-generation cybersecurity architectures. For instance, lattice-based cryptography delivers nearly 35% higher resilience against quantum-based attacks compared to traditional RSA encryption, making it one of the most widely implemented PQC frameworks in enterprise systems. Governments worldwide are actively developing cryptographic transition roadmaps, requiring organizations to conduct encryption audits and begin migration planning across digital ecosystems.

From a regional perspective, North America dominates in deployment volume, driven by strong government funding and advanced cybersecurity infrastructure, while Europe leads in enterprise adoption with nearly 58% of large organizations piloting quantum-safe cryptographic solutions. The European Union’s digital security strategy has encouraged large-scale testing of PQC frameworks across financial networks, telecommunications infrastructure, and cloud computing platforms.

Short-term projections indicate accelerated technological integration across enterprise IT ecosystems. By 2028, automated cryptographic inventory management tools combined with AI-driven threat analytics are expected to reduce encryption vulnerability detection time by nearly 40%. These technologies enable organizations to quickly identify weak encryption points and deploy quantum-resistant protocols across complex IT infrastructures.

Compliance and ESG considerations are also shaping market strategy. Many corporations are committing to cyber resilience metrics, including 50% reduction in long-term data exposure risks by 2030, while integrating secure encryption frameworks into their sustainability and governance reporting structures. Secure data protection is increasingly considered a key component of responsible digital governance.

A practical micro-scenario illustrates the transformation underway. In 2024, a U.S. defense research program successfully implemented hybrid quantum-safe encryption across its secure communications network, achieving a 45% improvement in cryptographic security strength while reducing vulnerability exposure across classified data systems.

As quantum computing capabilities continue to evolve, the Quantum-Safe Cybersecurity Integration Solutions Market will become a foundational pillar for enterprise resilience, regulatory compliance, and sustainable digital infrastructure protection worldwide.

The Quantum-Safe Cybersecurity Integration Solutions Market is evolving rapidly as organizations worldwide prepare for the disruptive impact of quantum computing on conventional encryption systems. Current cryptographic protocols used in banking systems, government communications, healthcare databases, and cloud infrastructure are vulnerable to future quantum-enabled decryption techniques. As a result, enterprises are prioritizing cryptographic modernization strategies to safeguard long-term data confidentiality and maintain regulatory compliance. Technology vendors and cybersecurity providers are investing heavily in post-quantum cryptography integration platforms that enable organizations to identify legacy encryption systems and transition toward quantum-resistant algorithms. In parallel, governments are developing national quantum cybersecurity roadmaps to protect critical digital infrastructure. Regulatory frameworks increasingly encourage enterprises to adopt cryptographic inventory assessments, encryption lifecycle management tools, and hybrid PQC deployment strategies. Another major dynamic influencing the market is the expansion of cloud computing and digital services. As global digital data volumes exceed 120 zettabytes, long-term protection of stored data becomes essential, particularly for sectors handling sensitive information such as defense, healthcare, and financial services. Enterprises are therefore integrating quantum-safe encryption layers into cloud architectures, secure communication networks, and identity authentication platforms.

Rapid progress in quantum computing research has significantly increased concerns regarding the vulnerability of existing cryptographic algorithms. Quantum computers capable of executing Shor’s algorithm could potentially break widely used encryption standards such as RSA and ECC, which currently secure a large portion of global internet communications. As a result, enterprises and governments are accelerating the transition toward quantum-resistant encryption frameworks. Technology firms and research institutions have already demonstrated quantum processors exceeding 1,000 qubits, significantly advancing computational capabilities that could challenge current cryptographic systems. Financial institutions, for example, store sensitive transaction data that must remain secure for decades. Surveys indicate that over 55% of global banks have initiated cryptographic risk assessments to identify vulnerabilities associated with quantum computing threats. Additionally, major technology companies are integrating hybrid encryption frameworks combining classical algorithms with PQC techniques to ensure a smoother transition toward quantum-safe infrastructures. Telecommunications operators are also experimenting with quantum key distribution (QKD) networks to enhance data transmission security across fiber-optic communication systems. The increasing urgency to protect digital assets, intellectual property, and critical infrastructure from future quantum threats is therefore driving large-scale adoption of quantum-safe cybersecurity integration platforms.

Despite growing awareness of quantum cybersecurity risks, many organizations face substantial challenges when attempting to transition from legacy encryption systems to quantum-safe cryptographic frameworks. The migration process requires organizations to conduct extensive cryptographic inventories across their IT infrastructure, which often includes thousands of applications, databases, and communication channels relying on traditional encryption protocols. Large enterprises frequently operate complex IT ecosystems that have evolved over decades, making cryptographic migration technically challenging and resource intensive. Studies indicate that over 70% of enterprise IT environments contain undocumented encryption dependencies, making it difficult to identify where vulnerable algorithms are embedded within software systems. Another limitation involves compatibility issues between post-quantum cryptographic algorithms and existing hardware infrastructure. Many PQC algorithms require larger key sizes and increased computational resources, which can affect system performance and network efficiency. Organizations operating legacy systems may need significant hardware upgrades to support new cryptographic standards. Furthermore, the shortage of specialized cybersecurity professionals trained in post-quantum cryptography is slowing enterprise transition efforts. Companies must invest in workforce training and security architecture redesign before implementing large-scale PQC deployment programs.

Global digital transformation initiatives are creating significant opportunities for the Quantum-Safe Cybersecurity Integration Solutions Market, particularly as enterprises modernize their IT infrastructure and migrate toward cloud-based platforms. Digital ecosystems supporting banking services, healthcare systems, government databases, and telecommunications networks require long-term encryption resilience to protect critical data assets. As organizations deploy next-generation technologies such as 5G networks, Internet of Things (IoT) systems, and autonomous platforms, the number of connected devices and data exchange points continues to expand rapidly. Estimates suggest that over 30 billion connected devices will be active globally by 2030, dramatically increasing cybersecurity complexity and data protection requirements. Cloud service providers are integrating quantum-safe encryption capabilities into their infrastructure to support enterprise customers seeking long-term cryptographic protection. These platforms allow organizations to deploy hybrid encryption frameworks that combine classical and quantum-resistant algorithms without disrupting existing applications. Additionally, the emergence of automated cryptographic discovery tools is creating opportunities for cybersecurity vendors to offer managed quantum-readiness services. These platforms can scan enterprise networks, identify vulnerable encryption algorithms, and recommend migration pathways toward quantum-safe architectures.

Although post-quantum cryptography research has advanced significantly in recent years, the global cybersecurity ecosystem still faces uncertainties regarding the standardization and implementation of quantum-resistant encryption algorithms. Organizations must carefully evaluate multiple PQC approaches—such as lattice-based, code-based, and multivariate cryptography—before committing to large-scale deployment strategies. Different regions and regulatory bodies are currently developing their own cybersecurity frameworks for quantum readiness, which can create compliance complexities for multinational enterprises. Companies operating across multiple jurisdictions must ensure that their encryption strategies align with evolving standards and government cybersecurity policies. Another challenge is the need to maintain backward compatibility with legacy systems during the transition toward PQC frameworks. Enterprises must deploy hybrid encryption architectures capable of supporting both traditional and quantum-resistant protocols simultaneously, which increases implementation complexity. Furthermore, the uncertainty surrounding the timeline for large-scale quantum computer deployment complicates investment decisions. Organizations must balance the urgency of preparing for quantum threats with the need to manage cybersecurity budgets efficiently while avoiding premature technology investments.

Rapid Expansion of Post-Quantum Cryptography Deployment Programs: Enterprise adoption of post-quantum cryptography is accelerating as organizations prepare for long-term data security risks associated with quantum computing. Approximately 48% of global enterprises have initiated quantum-readiness assessments, while 30% are already testing hybrid PQC encryption frameworks within their networks. Financial institutions and defense agencies are leading deployment efforts due to long-term data confidentiality requirements. Several multinational banks have begun integrating PQC algorithms into payment authentication systems, improving encryption resilience by nearly 35% against advanced cryptographic attacks.

Integration of Quantum Key Distribution in Secure Communication Networks: Quantum key distribution (QKD) technology is gaining traction as organizations seek ultra-secure data transmission methods. QKD enables encryption keys to be transmitted using quantum particles, making interception detectable and significantly improving communication security. In 2025, over 120 pilot QKD networks were operational globally, with telecom operators deploying fiber-based quantum communication channels across metropolitan networks. These systems have demonstrated 40% higher protection against data interception attempts compared with conventional encryption key exchange methods.

Growth of Automated Cryptographic Discovery and Risk Assessment Tools: Organizations managing large IT ecosystems are adopting automated cryptographic discovery platforms to identify vulnerable encryption systems before transitioning to PQC frameworks. Surveys indicate that nearly 55% of enterprises now deploy automated encryption scanning tools to map cryptographic dependencies across applications and databases. These tools can analyze thousands of system endpoints in real time, improving vulnerability detection rates by 45% and reducing manual cryptographic inventory efforts significantly.

Rising Government-Led Quantum Cybersecurity Preparedness Initiatives: Governments worldwide are launching national quantum cybersecurity programs to protect critical infrastructure from future quantum threats. Over 25 countries have introduced national PQC migration strategies, focusing on sectors such as banking, telecommunications, defense, and healthcare. In several advanced economies, more than 50% of government agencies have begun evaluating quantum-resistant encryption protocols, ensuring long-term security for classified communications and digital identity systems.

The Quantum-Safe Cybersecurity Integration Solutions Market is segmented across types, applications, and end-user industries, reflecting the diverse deployment environments for quantum-resistant cybersecurity technologies. Market segmentation highlights how organizations are adopting different quantum-safe solutions based on their infrastructure requirements, data sensitivity levels, and cybersecurity maturity. Enterprises handling highly sensitive information, such as financial institutions and government agencies, are prioritizing advanced cryptographic integration frameworks, while technology firms and telecom operators are focusing on secure communication systems and network-level encryption. From a technological perspective, the market includes solutions such as post-quantum cryptography integration platforms, quantum key distribution systems, and hybrid cryptographic infrastructure tools. Each category addresses specific security challenges related to protecting digital communications and stored data from quantum-enabled cyber threats. Applications vary widely across sectors including banking systems, cloud computing infrastructure, defense communications, healthcare data protection, and telecommunications networks. End-user industries are adopting quantum-safe cybersecurity at different rates depending on regulatory requirements and long-term data security needs. Government agencies and financial institutions remain the largest adopters, while cloud service providers and telecommunications companies are emerging as major deployment segments due to expanding digital connectivity and data transmission volumes.

The Quantum-Safe Cybersecurity Integration Solutions Market by type includes Post-Quantum Cryptography (PQC) Integration Platforms, Quantum Key Distribution (QKD) Systems, and Hybrid Quantum-Safe Security Frameworks. Among these, Post-Quantum Cryptography integration platforms lead the market with approximately 46% adoption, as they enable organizations to replace vulnerable classical encryption algorithms with quantum-resistant cryptographic protocols. PQC platforms are widely used across banking systems, cloud infrastructure, and government communication networks due to their ability to operate within existing IT architectures. Hybrid quantum-safe security frameworks are emerging as the fastest-growing type, expanding at an estimated 43% growth rate, as enterprises deploy transitional encryption architectures combining traditional cryptographic algorithms with PQC methods. These systems allow organizations to gradually migrate to quantum-safe encryption without disrupting operational systems. Quantum Key Distribution (QKD) represents a specialized but strategically important segment, primarily deployed in telecommunications networks and high-security government communication systems. QKD currently accounts for approximately 22% of market adoption, particularly in regions investing in quantum communication infrastructure. The remaining niche security integration solutions—including quantum-resistant identity authentication systems and cryptographic lifecycle management platforms—collectively contribute nearly 10% of overall deployments and are gaining traction in enterprise security modernization initiatives.

In 2024, a national telecommunications research program successfully implemented a metropolitan QKD network spanning more than 200 kilometers of fiber infrastructure, enabling secure encryption key exchanges for over 50 government and enterprise users.

The Quantum-Safe Cybersecurity Integration Solutions Market by application includes Secure Communications, Cloud Security, Financial Data Protection, Government & Defense Systems, and Critical Infrastructure Protection. Among these, government and defense cybersecurity applications lead the market with nearly 34% adoption, driven by the need to secure classified communications and protect national digital infrastructure from emerging quantum-enabled cyber threats. Financial data protection represents another significant segment, accounting for approximately 26% of current adoption, as banks and financial institutions seek long-term encryption solutions capable of protecting sensitive transaction records and financial databases for decades. The cloud security segment is the fastest-growing application area, expanding at approximately 45% growth, as organizations migrate enterprise workloads to cloud platforms while maintaining strong cryptographic protection against future quantum attacks. Other applications—including telecommunications network security and healthcare data protection—collectively contribute about 40% of deployments, supported by increasing digital data exchange across connected devices and enterprise platforms. Enterprise adoption statistics highlight the rising demand for quantum-safe security frameworks. In 2025, more than 41% of global enterprises reported conducting cryptographic risk assessments to identify vulnerable encryption algorithms. Additionally, nearly 37% of cloud service providers have begun integrating quantum-resistant encryption features within their platform infrastructure.

In 2025, a national banking infrastructure modernization program deployed quantum-safe encryption across payment authentication systems serving more than 15 million customers, significantly strengthening long-term financial data protection.

End-user adoption within the Quantum-Safe Cybersecurity Integration Solutions Market spans several key industries including Government & Defense, Financial Services, Telecommunications, Cloud Service Providers, and Healthcare Organizations. Among these segments, government and defense agencies lead with approximately 38% adoption, driven by the need to secure classified communications, national security infrastructure, and long-term digital intelligence archives. Financial services institutions represent another major end-user segment with nearly 27% market participation, as banks and insurance companies manage highly sensitive financial records that must remain protected for extended periods. Financial regulators in several advanced economies have already begun recommending quantum-readiness assessments for banking institutions. The telecommunications sector is emerging as the fastest-growing end-user group, expanding at approximately 44% growth, as telecom operators deploy secure communication networks capable of supporting quantum-safe encryption and QKD technologies. Other end-users—including cloud service providers and healthcare organizations—collectively account for nearly 35% of deployments, supported by the rapid growth of digital health records, cloud computing platforms, and interconnected enterprise ecosystems. Adoption trends indicate growing enterprise awareness of quantum cybersecurity risks. In 2025, nearly 39% of global enterprises reported initiating quantum-readiness planning programs, while over 46% of technology companies began testing hybrid PQC encryption frameworks within their cloud infrastructure.

In 2025, a national cybersecurity agency initiated a quantum-readiness assessment program across more than 300 government IT systems, enabling agencies to identify vulnerable encryption systems and accelerate migration toward quantum-resistant security frameworks.

North America accounted for the largest market share at 38.6% in 2025, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of41.8% between 2026 and 2033.

The strong dominance of North America is supported by large-scale investments in quantum computing and cybersecurity modernization programs, with the United States accounting for nearly 71% of the region’s market demand. Europe followed with approximately 26.4% market share in 2025, driven by strict data protection regulations and growing adoption of post-quantum cryptographic frameworks across banking and telecom sectors. Asia-Pacific represented around 22.1% of global demand, supported by increasing digital infrastructure spending across China, Japan, South Korea, and India. Meanwhile, South America contributed about 6.3% of total deployments, with Brazil and Argentina leading regional adoption of advanced cybersecurity frameworks. The Middle East & Africa accounted for nearly 6.6% of global market participation, supported by digital transformation initiatives and government cybersecurity programs in the UAE, Saudi Arabia, and South Africa. Globally, over 54% of enterprises located in developed economies conducted cryptographic inventory assessments in 2025, indicating strong regional progress toward quantum-safe cybersecurity integration.

North America represents the largest regional contributor to the Quantum-Safe Cybersecurity Integration Solutions Market, accounting for approximately 38.6% of global market share in 2025. The region’s leadership is driven by strong cybersecurity infrastructure, extensive government funding for quantum computing research, and widespread enterprise adoption of advanced encryption technologies. The United States dominates the regional market with nearly 82% of North American deployments, followed by Canada with about 12% share. Key industries driving demand include financial services, defense, healthcare, and cloud computing, where organizations must ensure long-term data protection against future quantum decryption threats. Government initiatives also play a critical role. For example, several federal cybersecurity programs now require agencies to evaluate cryptographic inventories across more than 15,000 government IT systems to prepare for post-quantum migration. Technological advancement in cloud security platforms and zero-trust architectures is also supporting adoption. Major cybersecurity vendors are integrating hybrid cryptographic frameworks combining classical encryption with post-quantum algorithms to ensure compatibility during the transition period. A notable regional example includes IBM, which has been actively integrating quantum-safe encryption capabilities into its enterprise security platforms, enabling organizations to test PQC algorithms across cloud and hybrid IT environments. Regional consumer behavior also influences adoption patterns. North America shows higher enterprise adoption in healthcare and financial sectors, where long-term data confidentiality requirements are particularly critical.

Europe accounted for approximately 26.4% of the global Quantum-Safe Cybersecurity Integration Solutions Market share in 2025, positioning the region as the second-largest contributor to industry demand. Major European markets include Germany, the United Kingdom, and France, which collectively represent nearly 62% of the region’s cybersecurity technology investments. Regulatory initiatives are a major catalyst for growth. European institutions have introduced multiple cybersecurity frameworks encouraging the adoption of post-quantum encryption to strengthen digital sovereignty and protect critical infrastructure. Organizations operating within sectors such as banking, telecommunications, and government administration are prioritizing encryption modernization to comply with evolving data protection policies. Emerging technologies such as secure multi-party computation, AI-driven cryptographic monitoring, and quantum key distribution pilot networks are gaining traction across Europe. The region has also invested heavily in research programs supporting quantum communication infrastructure across several cross-border technology corridors. A regional example includes ID Quantique, a Swiss cybersecurity firm that has deployed quantum-safe encryption and quantum key distribution technologies across secure communication networks in Europe and Asia. Consumer behavior patterns differ slightly compared to other regions. Europe shows strong demand driven by regulatory pressure and strict data privacy frameworks, encouraging enterprises to adopt transparent and explainable cybersecurity solutions.

Asia-Pacific represents one of the most dynamic regions in the Quantum-Safe Cybersecurity Integration Solutions Market, ranking third globally in market volume while demonstrating the strongest expansion potential. In 2025, the region accounted for roughly 22.1% of global deployments, with China, Japan, India, and South Korea representing the primary consuming markets. China leads regional adoption with approximately 36% share of Asia-Pacific demand, supported by extensive national investments in quantum communication infrastructure. Japan follows with about 21% market participation, while India contributes nearly 14% of regional demand, largely driven by expanding digital banking and telecommunications networks. Infrastructure modernization and large-scale manufacturing investments are accelerating the need for advanced cybersecurity frameworks across the region. Technology hubs such as Shenzhen, Tokyo, and Bangalore are actively developing next-generation encryption solutions to support rapidly growing digital ecosystems. A regional industry example includes Huawei, which has launched quantum-resistant encryption technologies integrated into enterprise networking equipment to support secure communications across telecom and cloud infrastructure. Regional consumer behavior highlights a distinct adoption trend. Asia-Pacific growth is driven by digital services expansion, mobile platforms, and e-commerce ecosystems, creating increasing demand for secure data transmission and long-term encryption protection.

South America accounted for approximately 6.3% of the global Quantum-Safe Cybersecurity Integration Solutions Market share in 2025, with Brazil and Argentina emerging as the largest contributors to regional cybersecurity adoption. Brazil alone represents nearly 48% of regional deployments, supported by increasing investment in digital banking systems and telecommunications networks. Infrastructure modernization programs across the region are strengthening cybersecurity requirements for energy, telecommunications, and government digital services. National digital transformation initiatives have accelerated the deployment of secure cloud platforms, particularly across financial institutions and public sector organizations. Government incentives encouraging the development of local technology ecosystems are also supporting market expansion. Several countries have introduced cybersecurity compliance frameworks aimed at improving protection of critical national infrastructure, particularly within energy distribution networks and financial transaction systems. An example of regional participation includes Stefanini, a Brazilian technology services provider that has been expanding its cybersecurity consulting capabilities to support enterprises transitioning toward advanced encryption and quantum-resistant security frameworks. Consumer behavior patterns within the region show increasing demand for secure digital platforms. South America’s adoption is closely tied to media, fintech, and language-localized digital services, which require strong data protection capabilities across mobile applications and online platforms.

The Middle East & Africa accounted for approximately 6.6% of the global Quantum-Safe Cybersecurity Integration Solutions Market in 2025, with increasing adoption driven by rapid digital modernization initiatives across government, energy, and financial sectors. Key growth markets include the United Arab Emirates, Saudi Arabia, and South Africa, which collectively represent nearly 63% of the region’s cybersecurity technology deployments. Regional demand is strongly influenced by industries such as oil & gas, smart infrastructure development, and national digital transformation programs. Several governments are investing in secure digital identity platforms and national cybersecurity strategies to protect critical infrastructure against emerging cyber threats. Technology modernization is also accelerating the integration of cloud-based cybersecurity platforms and advanced encryption systems across government networks and financial services institutions. A notable regional example includes DarkMatter Group from the UAE, which focuses on developing advanced cybersecurity technologies including secure communications platforms designed for government and defense environments. Regional consumer behavior reflects increasing reliance on secure digital services. Middle East & Africa shows strong adoption linked to government digital transformation programs, smart city initiatives, and expanding mobile financial services, all of which require strong encryption frameworks to protect sensitive data.

United States – 34.8% Market Share: Strong dominance due to advanced quantum computing research programs, extensive cybersecurity infrastructure, and large-scale adoption across defense, finance, and cloud computing sectors.

China – 16.2% Market Share: Significant influence supported by large national investments in quantum communication networks, strong government-backed cybersecurity initiatives, and rapidly expanding telecommunications infrastructure.

The Quantum-Safe Cybersecurity Integration Solutions Market is characterized by an increasingly competitive yet moderately fragmented landscape, with more than 60 active technology vendors and cybersecurity providers offering quantum-resistant encryption platforms, cryptographic migration tools, and secure communication technologies. The top five companies collectively account for approximately 41% of total market share, indicating the presence of strong competition among established global technology firms and emerging cybersecurity innovators.

Large multinational technology providers dominate the enterprise integration segment by offering comprehensive cybersecurity platforms capable of integrating post-quantum cryptography (PQC), quantum key distribution (QKD), and hybrid cryptographic frameworks within existing IT infrastructures. Several companies are investing heavily in research and development programs to accelerate the commercialization of quantum-safe security technologies. Strategic partnerships between cloud service providers, telecom operators, and cybersecurity firms are becoming increasingly common as enterprises seek integrated solutions capable of protecting large-scale digital ecosystems. Over 120 strategic collaborations and research partnerships related to post-quantum cryptography were announced globally between 2023 and 2025, highlighting the rapid pace of innovation in this sector. Product innovation remains a critical competitive factor. Many vendors are launching automated cryptographic discovery platforms capable of scanning thousands of enterprise systems to identify vulnerable encryption algorithms, enabling organizations to accelerate migration toward quantum-safe infrastructures.

In addition, mergers and acquisitions have intensified as cybersecurity companies attempt to strengthen their quantum technology capabilities. Several technology firms have acquired specialized cryptography startups to expand their portfolios of quantum-resistant encryption solutions and secure communication platforms.

The competitive environment is therefore shaped by continuous technological innovation, cross-industry collaboration, and increasing enterprise demand for long-term cybersecurity resilience against emerging quantum computing threats.

Microsoft Corporation

Thales Group

ID Quantique

Quantinuum

Post-Quantum Ltd.

ISARA Corporation

PQShield Ltd.

Huawei Technologies Co., Ltd.

Nokia Corporation

KETS Quantum Security Ltd.

SandboxAQ

CryptoNext Security

Infineon Technologies AG

Toshiba Digital Solutions Corporation

Technology innovation is a fundamental driver of the Quantum-Safe Cybersecurity Integration Solutions Market, as organizations worldwide prepare their cybersecurity infrastructures for the disruptive capabilities of quantum computing. Traditional encryption algorithms such as RSA-2048 and elliptic-curve cryptography are widely used across digital networks today, securing more than 85% of global internet communications. However, advancements in quantum computing are expected to significantly weaken these cryptographic methods, prompting the development of new quantum-resistant security frameworks. One of the most significant technological developments in this market is the advancement of post-quantum cryptography (PQC) algorithms. These algorithms are designed to resist attacks from both classical and quantum computers by using mathematical problems that remain computationally difficult even for quantum processors. Several PQC approaches—including lattice-based, hash-based, code-based, and multivariate cryptography—are currently being integrated into enterprise security platforms. Among these, lattice-based algorithms have demonstrated particularly strong performance, delivering up to 30% faster cryptographic verification times compared with certain traditional encryption systems. Another major technological innovation is the deployment of quantum key distribution (QKD) systems, which leverage quantum mechanics to generate and transmit encryption keys securely. Unlike conventional key exchange methods, QKD systems can detect any attempt at interception during transmission. More than 150 experimental and commercial QKD networks have been deployed globally, including metropolitan fiber-based communication networks spanning over 500 kilometers in certain research programs. Hybrid cryptographic infrastructures are also gaining importance as enterprises transition gradually from classical encryption systems to quantum-safe architectures. These frameworks combine traditional encryption algorithms with PQC methods, allowing organizations to maintain compatibility with existing systems while gradually introducing quantum-resistant protocols. Another emerging technological trend involves automated cryptographic discovery platforms that can analyze enterprise IT environments containing thousands of applications and databases. These platforms use artificial intelligence to identify vulnerable encryption algorithms, enabling organizations to prioritize migration strategies. Studies indicate that automated discovery systems can reduce cryptographic vulnerability detection time by nearly 45% compared with manual security assessments. In addition, cloud service providers are integrating quantum-safe encryption capabilities into their infrastructure platforms to support enterprise customers preparing for long-term cybersecurity threats. These technologies enable organizations to deploy PQC algorithms across distributed cloud environments containing millions of encrypted data transactions.

In October 2025, IBM launched Guardium Cryptography Manager, an AI-powered solution designed to help enterprises manage encryption assets and prepare for post-quantum cryptography migration as quantum computing threatens current encryption standards.

In January 2025, IBM partnered with Telefónica Tech to integrate quantum-safe cryptography technologies into cybersecurity services, enabling enterprises to address emerging risks associated with future quantum computers. Source: www.newsroom.ibm.com

In April 2025, PQShield launched UltraPQ-Suite, including the PQPlatform-TrustSys root-of-trust solution to help ASIC and FPGA hardware systems comply with emerging post-quantum cryptography standards such as NSA’s CNSA 2.0.

In June 2025, IBM and RIKEN unveiled the first IBM Quantum System Two deployed outside the United States, integrated with Japan’s Fugaku supercomputer to advance quantum computing capabilities and related security technologies.

The Quantum-Safe Cybersecurity Integration Solutions Market Report provides a comprehensive assessment of technologies, industry trends, deployment models, and enterprise adoption patterns related to next-generation cybersecurity systems designed to withstand quantum computing threats. The report evaluates a wide range of security technologies including post-quantum cryptography platforms, quantum key distribution systems, hybrid cryptographic frameworks, and automated cryptographic discovery tools that help organizations transition toward quantum-resistant security infrastructures.

The analysis covers multiple market segments including solution type, application areas, and end-user industries. Solution-level evaluation includes PQC integration platforms, secure communication systems, cryptographic lifecycle management tools, and hybrid encryption architectures designed to maintain compatibility with legacy systems. Application segments assessed in the report include secure communications, cloud security, government and defense systems, financial transaction protection, telecommunications network security, and critical infrastructure cybersecurity.

From an industry perspective, the report examines adoption trends across several key sectors including financial services, government agencies, telecommunications providers, healthcare institutions, cloud service providers, and technology companies. These industries collectively account for a large portion of current demand due to the need for long-term protection of sensitive digital data and secure communications networks. Geographically, the report evaluates market developments across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, analyzing regional differences in cybersecurity infrastructure, regulatory frameworks, and technology adoption patterns. The report also highlights emerging markets where digital transformation initiatives and expanding cloud infrastructure are increasing demand for advanced encryption solutions.

In addition, the study explores evolving enterprise cybersecurity strategies including cryptographic risk assessments, encryption modernization programs, and quantum-readiness planning initiatives. Many large enterprises now manage thousands of encrypted applications and communication systems, making automated cryptographic discovery and migration tools increasingly important. Overall, the report provides strategic insights into technology innovation, enterprise deployment strategies, regulatory trends, and competitive developments shaping the global Quantum-Safe Cybersecurity Integration Solutions Market, enabling business leaders, investors, and technology decision-makers to evaluate opportunities and risks within this rapidly evolving cybersecurity sector.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 200.0 Million |

| Market Revenue (2033) | USD 2,985.5 Million |

| CAGR (2026–2033) | 40.2% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | IBM Corporation; Microsoft Corporation; Thales Group; ID Quantique; Quantinuum; Post-Quantum Ltd.; ISARA Corporation; PQShield Ltd.; Huawei Technologies Co., Ltd.; Nokia Corporation; KETS Quantum Security Ltd.; SandboxAQ; CryptoNext Security; Infineon Technologies AG; Toshiba Digital Solutions Corporation |

| Customization & Pricing | Available on Request (10% Customization Free) |