Reports

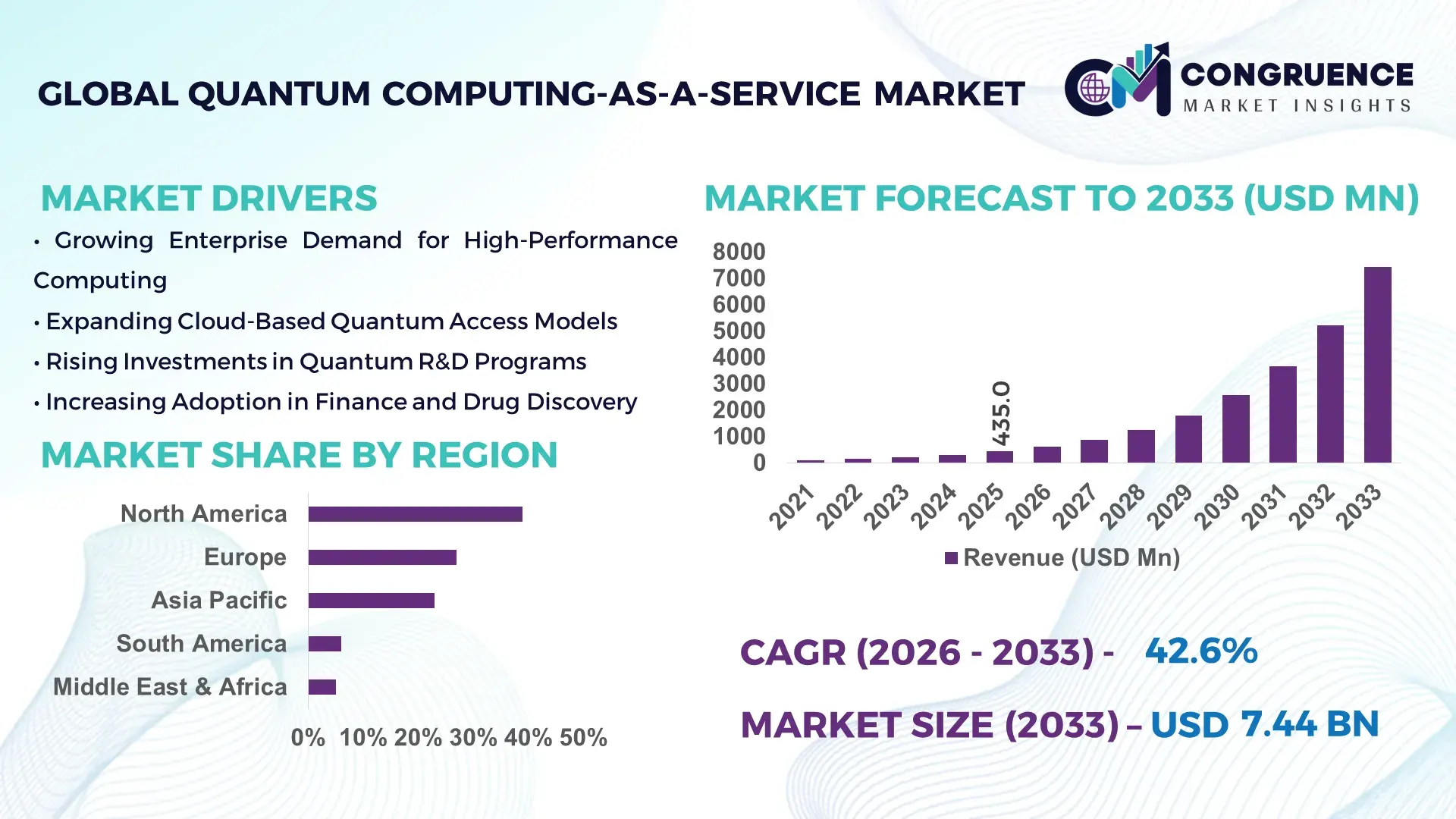

The Global Quantum Computing-as-a-Service Market was valued at USD 435.0 Million in 2025 and is anticipated to reach a value of USD 7,437.8 Million by 2033 expanding at a CAGR of 42.6% between 2026 and 2033, according to an analysis by Congruence Market Insights. The growth is primarily driven by rising enterprise experimentation in quantum algorithms, increasing cloud-based quantum access models, and expanding public–private investments in advanced computing infrastructure.

The United States represents the dominant country in the Quantum Computing-as-a-Service Market, supported by over USD 3.5 billion in federal quantum research funding allocated under the National Quantum Initiative Act and complementary state-level programs. The country hosts more than 60% of globally accessible cloud-based quantum processors, including superconducting and trapped-ion systems exceeding 100 qubits. Major technology providers operate quantum data centers integrated with hyperscale cloud platforms, enabling enterprise pilots across pharmaceuticals, aerospace, and financial services. Over 45% of Fortune 500 companies in the U.S. are actively testing quantum algorithms for optimization, cryptography, and materials science applications, reflecting strong industrial integration and advanced R&D commercialization capabilities.

Market Size & Growth: Valued at USD 435.0 Million in 2025, projected to reach USD 7,437.8 Million by 2033, expanding at 42.6% CAGR; growth driven by enterprise-grade quantum cloud access and hybrid HPC integration.

Top Growth Drivers: 58% enterprise pilot adoption increase, 35% optimization efficiency improvement in logistics simulations, 42% faster molecular modeling versus classical-only environments.

Short-Term Forecast: By 2028, hybrid quantum-classical workflows are expected to reduce complex simulation runtimes by 30% across financial and pharmaceutical workloads.

Emerging Technologies: Fault-tolerant qubit architectures, quantum error mitigation software, and hybrid quantum-HPC orchestration platforms.

Regional Leaders: North America projected at USD 3,120.0 Million by 2033 with strong cloud integration; Europe at USD 2,050.0 Million driven by sovereign quantum initiatives; Asia-Pacific at USD 1,780.0 Million supported by semiconductor-backed quantum R&D.

Consumer/End-User Trends: BFSI and pharmaceuticals account for over 48% of pilot deployments, focusing on risk modeling and drug discovery acceleration.

Pilot or Case Example: In 2024, a U.S.-based pharmaceutical firm achieved 27% faster compound simulation cycles using hybrid quantum services.

Competitive Landscape: IBM holds approximately 32% platform usage share, followed by Google Quantum AI, Microsoft Azure Quantum, Amazon Braket, and D-Wave.

Regulatory & ESG Impact: National quantum strategies across 17+ countries and 20% energy-efficiency improvements in cryogenic systems influence adoption.

Investment & Funding Patterns: Over USD 2.8 billion in venture and public funding allocated to quantum startups in 2024, emphasizing scalable qubit stability and cloud delivery models.

Innovation & Future Outlook: Integration with AI accelerators, post-quantum cryptography migration programs, and 1,000+ qubit roadmaps are shaping enterprise-ready deployments.

Quantum Computing-as-a-Service Market demand is primarily driven by BFSI (22%), pharmaceuticals (18%), aerospace & defense (15%), and energy (12%) applications. Advances in 100+ qubit processors, quantum error mitigation tools, and hybrid cloud orchestration platforms are accelerating enterprise pilots. Regulatory emphasis on post-quantum cryptography, regional sovereign quantum programs, and AI-quantum integration initiatives are strengthening adoption pipelines across North America, Europe, and Asia-Pacific markets.

Quantum Computing-as-a-Service (QCaaS) has emerged as a strategic enabler for enterprises seeking computational advantage without investing in capital-intensive quantum hardware infrastructure. By offering cloud-based access to superconducting, trapped-ion, and annealing systems, QCaaS reduces infrastructure deployment costs by nearly 40% compared to on-premise quantum experimentation models. Hybrid quantum-classical computing frameworks are increasingly embedded into enterprise workflows, particularly in portfolio optimization, cryptographic resilience testing, and molecular simulations.

From a performance perspective, hybrid quantum algorithms deliver up to 35% improvement compared to classical-only high-performance computing (HPC) environments in combinatorial optimization problems. North America dominates in volume of quantum cloud deployments, while Europe leads in structured enterprise adoption, with approximately 41% of large enterprises engaged in at least one quantum pilot initiative. Asia-Pacific is expanding rapidly through semiconductor-driven quantum hardware ecosystems and government-backed research clusters.

By 2028, AI-driven quantum error mitigation systems are expected to improve qubit stability metrics by 25%, significantly enhancing algorithm reliability. Firms are committing to ESG targets, including 30% reduction in data-center energy intensity by 2030 through advanced cryogenic cooling efficiency and renewable-powered facilities. In 2025, a U.S.-based aerospace consortium achieved a 22% optimization improvement in flight-path simulations using cloud-accessible quantum algorithms.

Looking forward, the Quantum Computing-as-a-Service Market is positioned as a pillar of digital resilience, regulatory compliance in post-quantum security transitions, and sustainable computational growth, enabling enterprises to future-proof mission-critical workloads.

The Quantum Computing-as-a-Service Market is characterized by accelerated cloud integration, cross-industry experimentation, and strong government-backed research funding. Increasing digital transformation across BFSI, life sciences, aerospace, and energy sectors is expanding demand for advanced optimization and simulation tools. More than 70% of quantum deployments currently operate under hybrid quantum-classical models, reflecting the transitional state of hardware maturity. Technological advances in qubit coherence times, which have improved by nearly 15% annually in leading labs, are enhancing system reliability. Simultaneously, hyperscale cloud providers are embedding quantum development kits (QDKs) into existing AI and HPC frameworks, simplifying enterprise adoption. Strategic alliances between semiconductor manufacturers and quantum startups are accelerating fabrication precision below 10 nanometers for superconducting circuits, supporting scalability and industrialization.

Enterprises facing exponential data complexity are increasingly leveraging QCaaS for combinatorial optimization, fraud detection, and secure communications. Over 52% of global banks are testing quantum algorithms for risk modeling and derivative pricing simulations. In pharmaceuticals, quantum-enhanced molecular modeling has demonstrated up to 30% faster compound interaction analysis compared to classical simulations. Additionally, the transition toward post-quantum cryptography—anticipated to affect nearly 75% of existing encryption protocols—has intensified demand for quantum testing environments. Cloud-based access removes infrastructure barriers, enabling mid-sized enterprises to participate in pilot programs without multimillion-dollar hardware investments, thereby broadening adoption across multiple verticals.

Despite rapid innovation, current quantum systems remain in the Noisy Intermediate-Scale Quantum (NISQ) phase, with error rates ranging between 0.1% and 1% per gate operation. Most commercially accessible systems operate below 500 qubits, limiting execution of highly complex algorithms. Cryogenic cooling requirements reaching temperatures near −273°C increase operational energy intensity and infrastructure complexity. Additionally, quantum programming expertise remains scarce, with fewer than 5,000 specialized quantum developers globally. These constraints slow enterprise-wide deployment and extend pilot validation cycles, restricting broader industrial scalability.

Hybrid quantum-HPC orchestration platforms present significant scalability opportunities, enabling enterprises to offload specific optimization tasks to quantum processors while retaining classical systems for data preprocessing. Approximately 68% of QCaaS users are integrating quantum APIs into existing cloud workflows. Emerging 1,000+ qubit development roadmaps and modular processor architectures are expanding industrial feasibility. Furthermore, defense and aerospace sectors are allocating over 20% of advanced R&D budgets toward quantum simulation research, signaling long-term institutional adoption potential. As error mitigation algorithms improve stability by up to 25%, broader commercial deployment scenarios are expected.

Quantum technologies introduce complex regulatory and cybersecurity considerations, particularly in cross-border data transfers and cryptographic transitions. Nearly 60% of enterprises cite uncertainty in post-quantum compliance standards as a deployment barrier. Migration from legacy encryption frameworks requires infrastructure upgrades across financial and government institutions. Additionally, intellectual property protection remains a concern, as quantum algorithms may expose proprietary modeling frameworks within shared cloud environments. Addressing these challenges requires harmonized regulatory frameworks and standardized security protocols across regions.

Rapid Expansion of 100+ Qubit Commercial Systems: Over 65% of cloud-accessible quantum processors now exceed 100 qubits, compared to less than 30% three years ago. Gate fidelity rates have improved by 18%, enhancing algorithm execution stability. Enterprise pilot projects increased by 40% year-over-year as larger qubit systems enabled more complex optimization modeling.

Hybrid Quantum-Classical Integration Accelerating: Approximately 72% of QCaaS deployments operate within hybrid HPC frameworks. Enterprises report 28% reduction in simulation runtime when combining classical preprocessing with quantum back-end optimization. Cloud-native quantum SDK downloads have grown by 35%, reflecting developer ecosystem expansion.

Surge in Post-Quantum Cryptography Testing: Around 55% of financial institutions initiated post-quantum encryption trials in 2025. Quantum-resilient algorithm implementation testing environments have increased by 33%, driven by regulatory preparedness initiatives. Governments in over 20 countries launched national cryptographic transition roadmaps.

Increased Venture and Public Funding in Scalable Architectures: More than 48% of recent quantum startup funding targets error correction and modular qubit scaling technologies. Public-private partnerships expanded by 37%, focusing on achieving 1,000+ qubit systems. Semiconductor fabrication precision improvements of 12% are enhancing superconducting circuit yields and hardware consistency.

The Quantum Computing-as-a-Service Market is segmented by type, application, and end-user, reflecting the evolving maturity of quantum hardware, software abstraction layers, and industry-specific use cases. From a type perspective, superconducting qubit platforms and quantum annealing systems dominate early-stage commercialization due to cloud-based accessibility and integration with classical HPC environments. Application-wise, optimization and simulation workloads account for the majority of deployments, particularly in finance, pharmaceuticals, and logistics. End-user segmentation highlights strong uptake among large enterprises and research institutions, where over 60% of pilot programs are concentrated. Increasing hybrid quantum-classical orchestration, improved qubit coherence times (up 15% in leading labs), and growing post-quantum cryptography initiatives are reshaping deployment patterns. Decision-makers are prioritizing use cases with measurable efficiency gains above 20%, ensuring practical ROI alignment while hardware scalability advances toward 1,000+ qubit thresholds.

The market is broadly categorized into Superconducting Qubit Platforms, Trapped-Ion Quantum Systems, Quantum Annealing Systems, and Photonic/Other Emerging Architectures. Superconducting qubit platforms currently account for approximately 46% of total QCaaS adoption due to compatibility with existing semiconductor fabrication techniques and integration with hyperscale cloud ecosystems. Quantum annealing systems hold around 28%, particularly favored for combinatorial optimization problems in logistics and manufacturing. However, trapped-ion systems are rising fastest, expanding at an estimated CAGR of 45%, driven by superior qubit coherence times and lower error rates below 0.1% in controlled environments.

Photonic and other niche architectures collectively contribute nearly 26% of deployments, primarily in research-intensive simulations and secure communications experimentation. While superconducting systems dominate enterprise pilot programs, trapped-ion advancements are gaining traction for complex algorithm execution requiring longer stability windows.

In 2025, the U.S. National Institute of Standards and Technology (NIST) reported achieving improved two-qubit gate fidelity above 99.5% in trapped-ion systems, reinforcing their viability for enterprise-grade quantum cloud services.

Optimization applications lead the Quantum Computing-as-a-Service Market, accounting for nearly 38% of total deployments, particularly in portfolio optimization, supply chain routing, and risk modeling. Simulation applications follow with approximately 29%, largely driven by pharmaceutical molecular modeling and materials science research. Cryptography and cybersecurity testing represent 18%, while machine learning and AI-enhanced quantum research contribute the remaining 15%.

Although optimization remains dominant, cryptography testing is the fastest-growing application segment, expanding at an estimated CAGR of 47%, fueled by global migration toward post-quantum encryption standards. In 2025, more than 42% of global banks reported testing quantum-safe encryption frameworks. Additionally, approximately 35% of pharmaceutical enterprises are piloting hybrid quantum simulations for compound discovery acceleration.

Emerging AI-quantum integration is enhancing predictive analytics by nearly 25% in early-stage pilots. Defense agencies and aerospace firms are also increasing adoption for secure communications and trajectory optimization models.

In 2025, the U.S. Department of Energy confirmed the deployment of quantum simulation tools across multiple national laboratories, supporting advanced materials research and complex system modeling initiatives.

Large enterprises dominate the Quantum Computing-as-a-Service Market, accounting for nearly 54% of total adoption due to substantial R&D budgets and established cloud partnerships. Research institutions and government laboratories represent approximately 26%, leveraging QCaaS platforms for advanced physics and materials experimentation. Small and medium enterprises (SMEs) contribute around 20%, primarily accessing quantum platforms through public cloud subscriptions.

While large enterprises lead in deployment volume, SMEs are the fastest-growing end-user group, expanding at an estimated CAGR of 48%, driven by subscription-based quantum access models and pay-per-use pricing structures. In 2025, over 38% of global enterprises reported active quantum pilot programs integrated into AI or analytics workflows. Additionally, around 44% of aerospace and defense organizations indicated ongoing quantum experimentation for secure communications and optimization tasks.

Financial institutions demonstrate strong uptake, with nearly 52% exploring quantum algorithms for derivative pricing and fraud analytics. Pharmaceutical companies account for about 18% of enterprise usage focused on molecular modeling and drug discovery simulations.

According to a 2025 OECD policy brief, more than 30 national governments have launched structured quantum adoption frameworks supporting enterprise and academic end-users through funding incentives and infrastructure grants.

North America accounted for the largest market share at 39% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 45% between 2026 and 2033.

North America’s leadership is supported by more than 60% of globally accessible cloud-based quantum processors hosted within the region and over 45% of Fortune 500 enterprises running pilot quantum programs. Europe follows with approximately 27% market share, driven by over 20 national quantum initiatives and coordinated public funding exceeding USD 7 billion equivalent in long-term commitments. Asia-Pacific holds nearly 23% share, with China and Japan collectively accounting for over 70% of regional quantum patent filings. South America and the Middle East & Africa together contribute around 11%, with adoption concentrated in energy optimization, financial modeling, and public research institutions. Cross-regional enterprise pilot participation increased by 38% in 2025, reflecting accelerated global experimentation and hybrid HPC integration.

North America accounts for approximately 39% of the global Quantum Computing-as-a-Service Market share, supported by deep integration between hyperscale cloud providers and quantum hardware innovators. The region hosts over 65% of commercial quantum cloud endpoints exceeding 100 qubits. Key industries driving demand include BFSI (over 25% of regional deployments), pharmaceuticals (18%), aerospace & defense (16%), and energy optimization (14%). Federal frameworks such as the National Quantum Initiative have allocated more than USD 3.5 billion in coordinated R&D programs, strengthening commercialization pathways. Technological advancements include superconducting qubit systems surpassing 400 qubits and AI-assisted error mitigation improving algorithm reliability by nearly 20%. IBM, a leading regional player, continues expanding cloud-based quantum access through its 1,000+ qubit roadmap and enterprise subscription platforms. Regional consumer behavior reflects higher enterprise adoption in healthcare and financial analytics, with over 52% of banks conducting quantum-safe cryptography testing pilots.

Europe represents nearly 27% of the global Quantum Computing-as-a-Service Market, with Germany, the United Kingdom, and France contributing more than 60% of regional deployments. Over 20 coordinated national strategies under EU-aligned quantum programs emphasize sovereign infrastructure and cross-border collaboration. The region prioritizes explainable and secure quantum integration, especially in financial services and industrial manufacturing. More than 40% of large enterprises in Western Europe have initiated at least one structured quantum pilot. Regulatory focus on post-quantum cryptography compliance is influencing early adoption across telecom and defense sectors. Technological efforts include photonic quantum research hubs and trapped-ion system scaling initiatives. A notable regional player, IQM (Finland), is deploying on-premise and cloud-integrated superconducting quantum systems across European research institutions. Consumer behavior trends indicate that regulatory oversight drives higher demand for secure and auditable quantum workloads, particularly in Germany and France.

Asia-Pacific holds approximately 23% of the Quantum Computing-as-a-Service Market and ranks as the fastest-growing region in enterprise pilot expansion. China, Japan, and India are the leading consuming countries, together accounting for over 75% of regional deployments. China leads in quantum patent filings with more than 3,000 active quantum-related patents, while Japan has invested heavily in superconducting circuit fabrication below 10 nm precision. Infrastructure growth includes advanced semiconductor manufacturing clusters and national quantum laboratories. Over 35% of regional enterprises are integrating hybrid quantum-HPC platforms within AI and analytics workflows. Toshiba and Fujitsu are actively developing quantum-inspired optimization services targeting logistics and telecom industries. Regional behavior reflects strong alignment with mobile AI ecosystems and digital transformation initiatives, with 48% of technology enterprises testing quantum algorithms for supply chain and e-commerce optimization.

South America contributes approximately 6% of the global Quantum Computing-as-a-Service Market, with Brazil and Argentina representing nearly 70% of regional activity. Adoption is concentrated in financial risk modeling, commodity trading optimization, and energy grid simulations. Over 30% of regional quantum pilot programs are linked to public research universities. Government-backed digital transformation initiatives in Brazil include incentives for high-performance computing collaborations and innovation tax credits. Infrastructure investments in renewable energy optimization are encouraging quantum experimentation in grid balancing and load forecasting. Regional consumer behavior indicates demand tied to financial analytics modernization and language-specific algorithm development. Brazilian research institutions are collaborating with global cloud providers to expand quantum workforce training programs exceeding 5,000 participants annually.

The Middle East & Africa account for roughly 5% of the global Quantum Computing-as-a-Service Market. The UAE and Saudi Arabia lead regional adoption, with quantum pilot programs integrated into smart city and oil & gas optimization projects. South Africa is expanding research collaborations through national science foundations and HPC modernization efforts. Energy and infrastructure sectors drive nearly 40% of regional quantum use cases, particularly in reservoir modeling and predictive maintenance simulations. Government-led digital transformation strategies allocate over USD 500 million equivalent toward advanced computing research initiatives. Local trade partnerships with global technology providers are accelerating skill development and infrastructure deployment. Consumer behavior trends indicate rising enterprise experimentation in fintech and energy analytics, with approximately 28% of large regional firms piloting quantum-compatible optimization tools.

United States – 36% Market Share: It leads due to extensive cloud infrastructure, over 60% of global commercial quantum processors, and strong enterprise adoption across BFSI and pharmaceuticals.

China – 18% Market Share: It is driven by high patent concentration, state-backed quantum laboratories, and large-scale semiconductor manufacturing capabilities supporting scalable qubit development.

The Quantum Computing-as-a-Service Market is moderately consolidated, with the top five companies accounting for approximately 58% of total platform usage and enterprise subscriptions. The competitive landscape comprises more than 40 active global participants, including hyperscale cloud providers, specialized quantum hardware firms, and quantum software orchestration startups. Market leaders differentiate through qubit scalability, cloud integration depth, hybrid quantum-classical orchestration capabilities, and enterprise-grade security frameworks.

Superconducting and trapped-ion hardware providers are competing to surpass the 1,000-qubit milestone, while several players have already demonstrated systems exceeding 400–1,000 qubits in controlled environments. Over 65% of competitive differentiation currently centers on error mitigation software, algorithm libraries, and developer ecosystem expansion rather than raw qubit count alone. Strategic initiatives include multi-year government contracts, cross-border research alliances, and partnerships with financial institutions and pharmaceutical firms.

In 2024–2025, more than 25 strategic collaborations were announced globally, targeting hybrid HPC integration and post-quantum cryptography readiness. Product launches increasingly emphasize modular quantum processors and AI-assisted calibration systems, improving gate fidelity above 99%. The market remains innovation-driven, with over 48% of competitive investments directed toward fault-tolerant architectures and scalable cryogenic infrastructure. Competitive intensity is expected to increase as Asia-Pacific players accelerate semiconductor-backed quantum fabrication capabilities and European firms expand sovereign quantum cloud deployments.

Amazon Braket

D-Wave Systems

Rigetti Computing

IonQ

Quantinuum

Xanadu

IQM Quantum Computers

Fujitsu

Toshiba

Alibaba Cloud Quantum Laboratory

Pasqal

Atos (Eviden Quantum)

The Quantum Computing-as-a-Service Market is driven by rapid advancements in qubit architecture, hybrid orchestration software, and quantum error correction frameworks. Superconducting qubits currently dominate commercial deployments, with gate fidelities exceeding 99% and coherence times improving by nearly 15% annually in leading systems. Trapped-ion architectures demonstrate lower error rates below 0.1% per gate in laboratory conditions, supporting high-precision algorithm experimentation.

Hybrid quantum-classical computing frameworks now represent over 70% of enterprise deployments, integrating quantum processing units (QPUs) with classical HPC clusters through API-based orchestration. AI-driven calibration systems are reducing system downtime by approximately 20%, improving operational stability for enterprise pilots.

Emerging fault-tolerant quantum computing research focuses on logical qubit construction using surface code error correction, where thousands of physical qubits may be required to create a single stable logical qubit. More than 45% of R&D investment in 2025 is directed toward scalable cryogenic systems operating below 20 millikelvin to maintain qubit coherence.

Photonic quantum computing platforms are gaining traction due to room-temperature operation capabilities, potentially reducing infrastructure energy intensity by up to 30%. Quantum-safe cryptography testing environments are also expanding, with over 50% of global financial institutions piloting post-quantum encryption validation systems. Collectively, these technological shifts are transitioning QCaaS from experimental research environments toward enterprise-grade computational acceleration.

• In May 2025, IBM introduced the IBM Quantum Flex Plan — a new access model that lets organizations pre-purchase project-based quantum compute time on IBM’s entire fleet of quantum systems, allowing flexible research and experiment execution without long-term subscription commitments. This plan provides premium access and is priced starting at an entry point for high-impact research. Source: www.ibm.com

• In May 2025, D-Wave Quantum announced the general availability of its Advantage2 system, its most advanced quantum annealing computer with over 4,400 qubits and enhanced connectivity and coherence. The system is accessible via D-Wave’s Leap cloud service with enterprise-grade uptime and security, and also supports on-premises deployments for large-scale optimization applications. Source: www.dwavequantum.com

• In June 2025, Microsoft Quantum advanced quantum error correction by developing a novel family of four-dimensional error-correction codes designed to dramatically reduce error rates — up to 1,000-fold in certain scenarios — bringing logical qubits closer to practical reliability for hybrid quantum workloads. Source: www.azure.microsoft.com

• In November 2025, IBM unveiled major progress on fault-tolerant and high-performance quantum processors, showcasing new IBM Quantum Nighthawk and Loon processors aimed at supporting larger gate counts and more connected qubit architectures as part of its roadmap to deliver practical quantum advantage by 2026 and beyond. Source: www.newsroom.ibm.com

The Quantum Computing-as-a-Service Market Report provides a comprehensive analysis of cloud-accessible quantum computing platforms segmented by hardware type, application domain, end-user industry, and geographic region. The report evaluates superconducting, trapped-ion, quantum annealing, and photonic architectures, highlighting their respective deployment footprints and performance benchmarks such as qubit counts exceeding 100–1,000 and gate fidelities above 99%.

Industry coverage spans BFSI, pharmaceuticals, aerospace & defense, energy, telecommunications, and government research institutions, collectively representing more than 80% of enterprise pilot programs. Application focus areas include optimization (38% deployment share), simulation (29%), cryptography testing (18%), and quantum-enhanced AI research (15%).

Geographically, the report analyzes five major regions—North America (39% share), Europe (27%), Asia-Pacific (23%), South America (6%), and Middle East & Africa (5%)—detailing infrastructure readiness, regulatory frameworks, and innovation clusters.

The study further assesses competitive positioning of over 40 active market participants, innovation trends such as fault-tolerant logical qubits and hybrid HPC orchestration, and investment flows where nearly half of R&D funding targets error correction and scalable hardware systems. The scope extends to emerging segments including quantum networking, secure communications pilots, and AI-integrated quantum development toolkits, providing decision-makers with a structured, forward-looking assessment of technology readiness and industrial deployment potential.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 435.0 Million |

| Market Revenue (2033) | USD 7,437.8 Million |

| CAGR (2026–2033) | 42.6% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | IBM; Google Quantum AI; Microsoft Azure Quantum; Amazon Braket; D-Wave Systems; Rigetti Computing; IonQ; Quantinuum; Xanadu; IQM Quantum Computers; Fujitsu; Toshiba; Alibaba Cloud Quantum Laboratory; Pasqal; Atos (Eviden Quantum) |

| Customization & Pricing | Available on Request (10% Customization Free) |