Reports

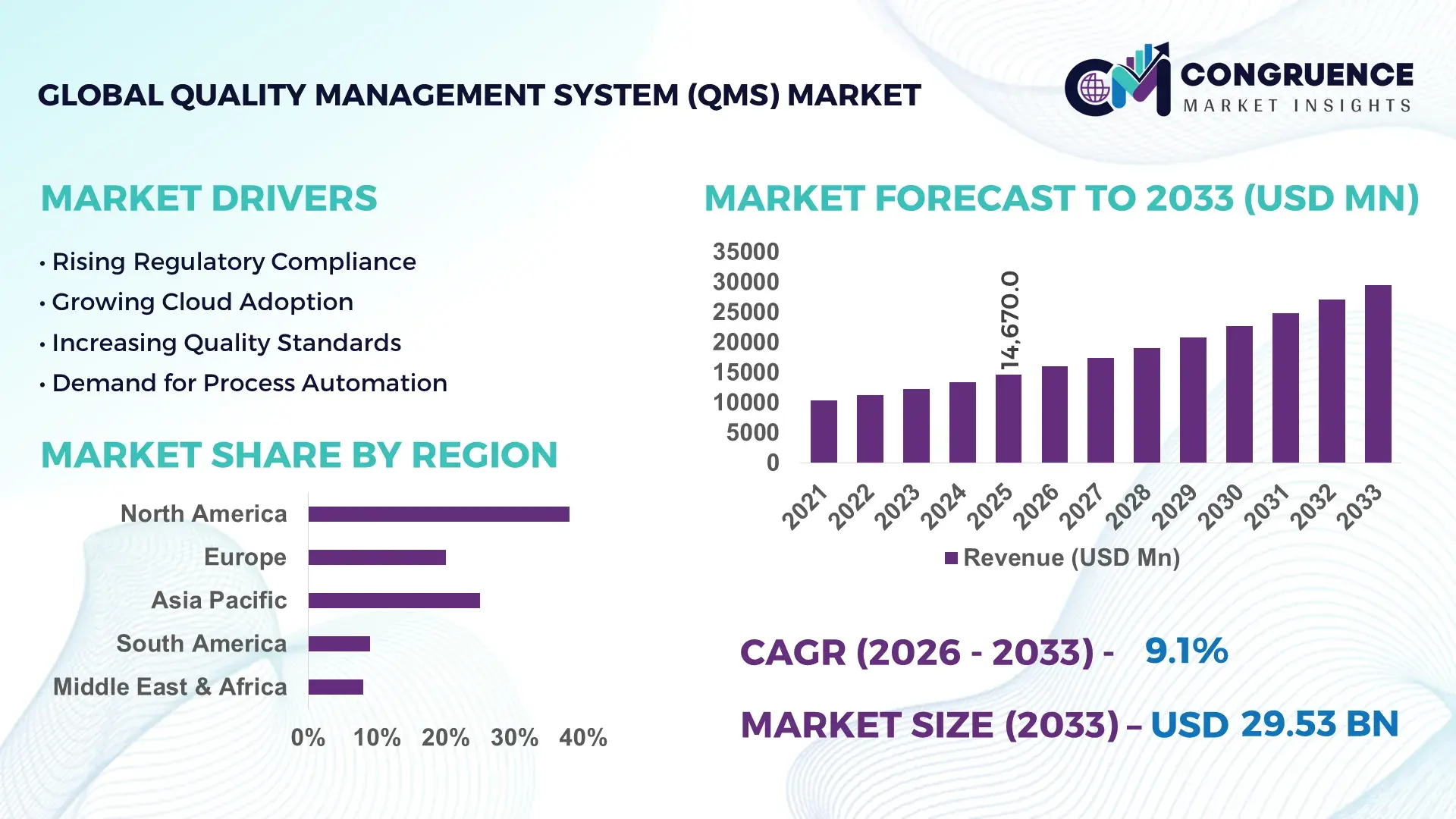

The Global Quality Management System (QMS) Market was valued at USD 14670 Million in 2025 and is anticipated to reach a value of USD 29532.6 Million by 2033 expanding at a CAGR of 9.14% between 2026 and 2033. Growth is being accelerated by digital compliance mandates, AI-enabled quality monitoring, pharmaceutical validation requirements, and manufacturing traceability programs across highly regulated industries.

The United States remains the dominant country, accounting for approximately 34% of global QMS platform adoption, supported by over USD 12 billion in annual digital manufacturing and compliance technology investments across healthcare, aerospace, and advanced manufacturing sectors. More than 68% of large enterprises have integrated cloud-based quality workflows, compared with nearly 52% in Germany. Ongoing supply-chain restructuring following global trade realignments has further increased enterprise spending on supplier quality visibility, while industrial AI deployment rates exceed 40% across major U.S. manufacturing operations.

Organizations prioritizing scalable, compliance-driven QMS platforms with AI and supplier integration capabilities are positioned to strengthen operational resilience and regulatory readiness through 2033.

Market Size & Growth: USD 14670 Million in 2025, reaching USD 29532.6 Million by 2033 at 9.14% CAGR, driven by AI-enabled quality assurance and digital compliance transformation.

Top Growth Drivers: Cloud deployment adoption exceeds 60%, automated audit processes improve productivity by 25%, and supplier quality integration reduces non-conformance events by 18%.

Short-Term Forecast: By 2028, enterprises are expected to reduce compliance management costs by 22% and improve quality reporting efficiency by 30%.

Emerging Technologies: AI analytics, predictive quality management, and industrial IoT integration improve defect detection accuracy by up to 35%.

Regional Leaders: North America surpasses USD 10 Billion, Europe exceeds USD 8 Billion, and Asia-Pacific approaches USD 7 Billion, supported by rapid digital quality adoption.

Consumer/End-User Trends: More than 70% of regulated manufacturers are shifting toward cloud-native QMS environments for centralized governance.

Pilot/Case Example: In 2026, a multinational medical device deployment achieved a 28% reduction in audit preparation time through automated documentation workflows.

Competitive Landscape: Leading vendors collectively control approximately 45% of market activity, with major competition focused on cloud and AI capabilities among 3–5 global providers.

Regulatory & ESG Impact: Digital compliance frameworks have lowered documentation errors by nearly 20% while strengthening ESG reporting transparency.

Investment & Funding: Annual enterprise investment exceeds USD 5 Billion, with strategic partnerships and platform modernization driving expansion.

Innovation & Future Outlook: Generative AI quality assistants, autonomous corrective-action systems, and real-time supplier intelligence are reshaping advanced quality operations.

Quality Management System (QMS) solutions are seeing strong demand across pharmaceuticals, medical devices, aerospace, automotive, and food manufacturing, where compliance accuracy and traceability remain critical. AI-powered quality analytics and automated corrective-action workflows are reducing review cycles by nearly 30%. An emerging trend is the integration of supplier quality intelligence into enterprise platforms as organizations respond to evolving regulatory requirements and supply-chain risk exposure, setting the stage for broader strategic quality transformation.

Quality Management System (QMS) platforms have become a strategic enterprise layer as manufacturers, healthcare providers, and regulated industries prioritize operational resilience, compliance visibility, and supplier accountability. Supply-chain restructuring and tighter digital recordkeeping requirements are accelerating adoption beyond traditional quality departments into enterprise-wide operations. Organizations increasingly view QMS investments as a competitive differentiator because quality failures can directly affect production continuity, customer retention, and regulatory performance.

Technology modernization is reshaping deployment models. AI-enabled QMS platforms can reduce audit preparation time by nearly 30% compared with legacy document-centric systems while improving deviation detection accuracy by more than 20%. The United States leads large-scale cloud QMS deployment across pharmaceutical and aerospace industries, while Germany emphasizes Industry 4.0-integrated quality architectures linked with production systems. A practical example is medical device manufacturers deploying automated corrective and preventive action workflows, reducing manual review cycles and strengthening traceability across global supplier networks.

Over the next two to three years, enterprise adoption of cloud-native quality platforms is expected to exceed 70% among large regulated organizations, supported by expanded software partnerships and compliance-focused digital transformation programs. Companies are increasing investments in AI analytics, supplier quality integration, and predictive risk monitoring to secure stronger operational control. Organizations that establish connected quality ecosystems will gain measurable advantages in compliance readiness, manufacturing consistency, and long-term competitive positioning.

The primary growth driver is the rapid digitization of compliance and quality operations across regulated industries. More than 68% of large manufacturers now utilize cloud-based quality workflows, while automated audit management systems reduce administrative effort by approximately 25%. Pharmaceutical and medical device companies are expanding digital validation programs as regulatory scrutiny over product traceability increases. In the United States, growing adoption of AI-powered quality analytics is enabling organizations to identify non-conformance patterns up to 20% faster than traditional review methods. This shift improves operational consistency, reduces remediation costs, and strengthens inspection readiness. Companies are responding through platform modernization initiatives, strategic software partnerships, and expanded investment in integrated supplier quality management, creating a more connected and proactive quality ecosystem.

Legacy infrastructure remains a significant barrier to efficient QMS deployment. Nearly 45% of industrial enterprises continue to operate multiple disconnected quality databases, while system integration projects can increase implementation timelines by 20–30%. Manufacturing organizations in Japan and parts of Europe frequently face interoperability challenges between older production systems and modern cloud-based quality platforms. The resulting fragmentation limits data visibility, delays corrective actions, and increases operational overhead. Regulatory requirements for validated system transitions further extend deployment cycles and resource commitments. To reduce risk, companies are adopting phased migration strategies, localized implementation models, and middleware integration solutions. A critical operational insight is that integration readiness increasingly determines deployment success more than software functionality alone.

The emergence of predictive quality intelligence creates a high-value opportunity beyond conventional compliance management. AI-driven risk prediction tools can improve defect forecasting accuracy by over 30%, while real-time analytics platforms reduce investigation cycles by nearly 25%. Manufacturers in India are expanding digital factory initiatives that connect quality, production, and supplier performance data into unified operational environments. The growing use of digital twins and machine-learning-based root-cause analysis is enabling earlier intervention and lower quality-related waste. Companies are accelerating R&D investment, ecosystem partnerships, and cloud platform expansion to capture these benefits. A particularly valuable opportunity lies in supplier quality intelligence, where predictive monitoring can identify disruption risks before they affect production schedules or regulatory outcomes.

As QMS platforms become increasingly interconnected, cybersecurity and data governance have emerged as major execution challenges. More than 60% of enterprise quality environments now exchange information across multiple operational systems, increasing exposure to cyber vulnerabilities and data integrity risks. Cloud-based deployments require continuous validation, access control management, and compliance monitoring to maintain trusted records. In the United States, growing reliance on AI-generated quality insights is creating additional governance requirements around model transparency and auditability. These pressures can slow deployment consistency and increase operational complexity across multinational organizations. Companies must invest in secure architecture, workforce training, and advanced governance frameworks while strengthening technology partnerships. Long-term competitiveness will depend on balancing scalable innovation with rigorous control of quality-critical data assets.

AI-Powered Quality Workflows: Enterprises are embedding AI into audit management, deviation tracking, and corrective-action processes, with automated quality reviews reducing investigation time by 25% and improving issue detection rates by over 20%. Regulatory scrutiny across pharmaceuticals and medical devices is accelerating deployment, while large manufacturers are integrating AI with operational systems. Companies are expanding technology partnerships and scaling analytics capabilities to improve compliance efficiency and reduce quality-related disruptions.

Supplier Visibility Expansion: Supply-chain restructuring is driving stronger demand for supplier quality management capabilities. More than 60% of multinational manufacturers now require digital supplier performance monitoring, while supplier-related quality incidents have declined by nearly 15% among organizations using integrated oversight platforms. U.S. and German industrial firms are extending quality controls beyond internal operations, prompting software vendors to prioritize supplier collaboration modules and ecosystem integrations.

Cloud-Native Platform Migration: Cloud-based QMS adoption has surpassed 70% among large regulated enterprises, driven by faster deployment cycles and approximately 30% lower infrastructure management requirements. Organizations are replacing fragmented on-premise environments with centralized quality architectures that improve data accessibility and audit readiness. Vendors are responding through subscription-based delivery models, industry-specific configurations, and accelerated migration services.

Connected Compliance Ecosystems: Quality management is increasingly linked with enterprise resource planning, manufacturing execution, and risk management systems. Integrated deployments have improved process visibility by nearly 35% while reducing duplicate documentation activities by 20%. A notable shift is the movement from departmental quality oversight to enterprise-wide governance models, encouraging companies to invest in unified digital platforms that support operational consistency and strategic decision-making.

Document Control remains the leading segment due to its foundational role in regulatory compliance, audit readiness, and enterprise-wide information governance. More than 65% of regulated organizations prioritize document control modernization as the first stage of quality digitization because it supports scalability, standardization, and cross-functional integration. The segment benefits from lower implementation complexity and direct alignment with compliance mandates in healthcare, manufacturing, and aerospace industries. Audit Management and Supplier Management continue to hold strategic importance as organizations strengthen oversight across increasingly distributed operational environments.

CAPA Management is emerging as the fastest-growing segment as enterprises shift from reactive quality correction toward predictive issue resolution. Automated CAPA workflows have reduced investigation cycles by approximately 28% and improved closure efficiency by nearly 22% in advanced deployments. Complaint Management is also gaining traction in customer-focused industries where product feedback data is increasingly linked with quality systems. Vendors are responding through AI-enabled root-cause analysis, workflow automation, and integrated quality platforms, while investment priorities increasingly favor corrective intelligence capabilities that improve operational performance and regulatory responsiveness.

Quality Assurance remains the dominant application segment because it serves as the operational backbone for compliance, product consistency, and manufacturing performance. Nearly 70% of enterprise QMS deployments continue to prioritize quality assurance functions, particularly in pharmaceutical, automotive, and aerospace environments where quality deviations carry substantial operational consequences. Compliance Management maintains strong demand as digital recordkeeping requirements intensify, while Product Quality applications are increasingly integrated with manufacturing and customer feedback systems to strengthen lifecycle oversight.

Risk Management is the fastest-growing application area as organizations seek earlier identification of operational, supplier, and compliance-related disruptions. Advanced risk analytics deployments have improved issue prediction accuracy by over 30%, while integrated monitoring frameworks have reduced quality-related incident response times by approximately 20%. Supplier Quality and Process Improvement applications are also expanding as companies focus on operational resilience and productivity optimization. Vendors are investing in predictive analytics, automation tools, and connected quality ecosystems to address shifting enterprise priorities and strengthen long-term quality performance.

Manufacturing remains the largest end-user segment due to its extensive dependence on standardized processes, supplier coordination, and regulatory compliance. More than 40% of enterprise QMS deployments are concentrated within manufacturing environments where quality performance directly influences production efficiency and customer satisfaction. Automotive and Aerospace & Defense continue to represent mature adoption segments because of stringent traceability and documentation requirements. Food & Beverage companies are also increasing investments in digital quality monitoring to address product safety and operational transparency requirements.

Healthcare is the fastest-growing end-user segment as hospitals, medical device manufacturers, and pharmaceutical organizations accelerate digital quality transformation initiatives. Automated compliance and validation workflows have improved documentation efficiency by nearly 30%, while cloud-based quality systems have reduced manual administrative workloads by approximately 20%. Consumer Goods companies are increasingly deploying integrated quality platforms to manage product consistency across global operations. Vendors are targeting these sectors through industry-specific solutions, strategic partnerships, and configurable deployment models that address evolving compliance and operational requirements.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 11.2% between 2026 and 2033.

Enterprise-Wide Quality Digitalization Leadership

North America maintains the largest share of the Quality Management System (QMS) market due to high software adoption across pharmaceuticals, aerospace, healthcare, and advanced manufacturing. The region represents approximately 38% of global deployment activity, supported by mature cloud infrastructure and stringent compliance requirements. More than 70% of large regulated enterprises utilize integrated quality platforms linked with operational and supplier systems. Organizations are increasingly deploying AI-enabled quality analytics and automated audit management tools, reducing compliance preparation workloads by nearly 25%. Strategic partnerships between software providers and industrial enterprises continue to accelerate enterprise-wide quality transformation and operational standardization.

United States Market Outlook: The United States remains the primary market driver due to its concentration of pharmaceutical manufacturing, medical device production, and aerospace operations. Over 68% of large enterprises have adopted cloud-based quality management environments, while increasing investment in AI-supported compliance monitoring is strengthening deployment activity. Federal regulatory oversight and digital traceability requirements continue to encourage enterprise modernization programs focused on quality governance, supplier accountability, and operational resilience.

Industry 4.0 and Regulatory Integration Momentum

Europe represents a major QMS deployment hub supported by advanced manufacturing infrastructure and strong regulatory alignment. The region accounts for approximately 29% of global market activity, with Germany, France, and the United Kingdom leading implementation across automotive, industrial equipment, and life sciences sectors. Industry 4.0 initiatives are encouraging deeper integration between manufacturing execution systems and quality platforms. Nearly 60% of large industrial organizations have expanded digital quality oversight programs to improve traceability and production consistency. Sustainability reporting requirements are also driving investments in centralized compliance and documentation management capabilities.

Germany Market Outlook: Germany leads European adoption through its advanced industrial ecosystem and extensive smart manufacturing investments. Automotive and industrial manufacturers increasingly connect quality management platforms with factory automation systems to improve operational visibility. More than half of large manufacturing facilities have implemented digitally integrated quality controls, supporting stronger defect management, process standardization, and supplier performance monitoring throughout complex production networks.

Manufacturing Scale and Cloud Adoption Expansion

Asia-Pacific is emerging as the fastest-growing regional market due to large-scale industrial expansion, digital manufacturing initiatives, and increasing regulatory modernization. The region accounts for nearly 24% of global deployment activity, supported by strong demand from electronics, automotive, pharmaceutical, and industrial manufacturing sectors. Cloud-based QMS adoption has increased by over 30% across major enterprises during recent years as organizations seek scalable compliance and quality management capabilities. Continued investment in industrial digitalization and export-focused production facilities is strengthening enterprise demand for integrated quality platforms.

China Market Outlook: China remains the largest country market within Asia-Pacific due to its manufacturing scale and rapid enterprise digitization efforts. Large exporters are expanding quality automation programs to meet international compliance standards and strengthen supplier oversight. More than 55% of major manufacturers have accelerated deployment of digital quality monitoring systems, while government-backed industrial modernization initiatives continue to support advanced quality infrastructure and operational standardization.

Compliance Modernization Driving Adoption

South America is experiencing gradual QMS expansion as manufacturers and regulated industries modernize quality processes and strengthen compliance frameworks. The region contributes approximately 5% of global market activity, with adoption concentrated in pharmaceutical production, food processing, and industrial manufacturing. Enterprise demand is increasing as organizations seek better audit readiness and operational transparency. Digital quality deployments have improved process documentation efficiency by nearly 20% among early adopters. However, infrastructure disparities and budget constraints continue to influence implementation speed across several markets.

Brazil Market Outlook: Brazil represents the region's most significant market due to its industrial base and pharmaceutical manufacturing presence. Large enterprises are investing in cloud-based quality platforms to improve regulatory compliance and production consistency. Expanding modernization initiatives across healthcare, food processing, and manufacturing sectors are increasing demand for integrated quality workflows. Enterprise deployments have accelerated as organizations prioritize operational standardization and stronger supplier quality governance.

Industrial Diversification and Digital Transformation Investments

The Middle East & Africa market is benefiting from industrial diversification strategies, digital transformation programs, and infrastructure modernization initiatives. The region accounts for roughly 4% of global market activity, with adoption concentrated in energy, healthcare, manufacturing, and government-regulated sectors. Organizations are increasingly implementing centralized quality frameworks to improve compliance consistency and operational control. Several large-scale industrial modernization projects have incorporated digital quality systems, contributing to deployment growth. Enterprise demand is also supported by expanding investments in cloud infrastructure and smart industrial operations.

Saudi Arabia Market Outlook: Saudi Arabia leads regional adoption through industrial diversification programs and large-scale digital transformation investments. Manufacturing, healthcare, and energy operators are expanding quality management deployments to support operational excellence objectives. More than 40% of major industrial organizations have accelerated digital governance initiatives linked to quality and compliance management. Ongoing infrastructure modernization and technology investment programs continue to strengthen enterprise demand for advanced quality management solutions.

The market is led by MasterControl, ETQ, Sparta Systems, Intelex Technologies, Arena Solutions, and AssurX, with global platform providers competing against specialized compliance-focused vendors. The top five players collectively account for approximately 42% of market activity. Competition centers on AI-enabled quality analytics, deployment speed, regulatory functionality, and enterprise integration capabilities. Advanced automation features can reduce audit preparation time by 25%, while integrated quality ecosystems improve process visibility by nearly 30%, creating clear differentiation. Global leaders compete through cloud platform expansion, strategic partnerships with manufacturing and healthcare enterprises, and continuous product innovation. Specialized vendors focus on industry-specific workflows and faster implementation cycles to challenge larger providers. The competitive landscape is shifting toward connected quality architectures that integrate supplier management, risk monitoring, and compliance automation. High validation requirements, integration complexity, and regulatory expertise create significant entry barriers. Success increasingly depends on delivering scalable, intelligent, and compliance-ready platforms that generate measurable operational improvements.

MasterControl

ETQ

Sparta Systems

Intelex Technologies

Arena Solutions

AssurX

Qualio

Greenlight Guru

Veeva Systems

SAP

Oracle

Dassault Systèmes

Siemens Digital Industries Software

QT9 Software

Cloud-native QMS platforms remain the core technology foundation, with more than 70% of large regulated enterprises deploying centralized quality environments to replace fragmented legacy systems. Modern cloud architectures reduce infrastructure administration costs by approximately 25% while improving audit readiness and document accessibility. Integrated workflow automation is also accelerating adoption, reducing manual quality review effort by nearly 20%. Organizations benefit through faster compliance execution, improved traceability, and standardized quality governance across global operations.

Emerging technologies are centered on artificial intelligence, predictive analytics, and connected quality ecosystems. AI-powered quality intelligence tools improve defect prediction accuracy by over 30% and reduce investigation cycles by approximately 25%. More than 45% of advanced manufacturers have begun integrating quality data with production, supplier, and operational systems. Compared with legacy rule-based quality monitoring, AI-enabled platforms deliver roughly 35% faster root-cause identification. This shift enables proactive quality management while improving production consistency and supplier performance visibility.

Disruptive innovation is increasingly driven by digital twins, generative AI assistants, and real-time supplier quality intelligence. Between 2026 and 2028, enterprise adoption of predictive quality automation is expected to exceed 50% among highly regulated industries. Global platform leaders and AI-focused software innovators are competing to deliver intelligent, closed-loop quality ecosystems. Organizations acting now gain operational advantages through faster compliance execution, lower remediation costs, stronger supplier oversight, and more resilient quality-driven decision making.

August 2024 – ETQ launched its Inspection Management application within the ETQ Reliance NXG platform, enabling automated quality inspections and real-time operational visibility. The solution supports 100% integration with existing Reliance workflows, helping manufacturers accelerate defect identification and compliance execution across production environments. Source: etq.com

October 2024 – ETQ introduced ETQ Reliance Predictive Quality Analytics through a partnership with Acerta Analytics, bringing AI-driven defect prediction and shop-floor quality intelligence. ETQ reported that 73% of surveyed manufacturers experienced product recalls within five years, highlighting the solution’s value in reducing quality-related operational risk. Source: etq.com

January 2025 – Veeva Systems partnered with Zifo to accelerate quality control modernization by integrating Veeva LIMS with qcKen data-management technology. The initiative streamlines laboratory master-data configuration and site deployment processes, reducing implementation complexity while helping life sciences companies transition away from legacy quality systems. Source: veeva.com

January 2026 – ETQ unveiled Reliance AI, introducing native AI capabilities including Form Field Advisor and Complaint & Feedback Advisor. Built on more than 30 years of automated quality management expertise, the platform enables faster investigation workflows, contextual decision support, and improved quality intelligence for manufacturing organizations.

This report provides comprehensive analysis of the Quality Management System (QMS) market across key solution categories including Document Control, Audit Management, CAPA Management, Supplier Management, and Complaint Management. It evaluates demand across Quality Assurance, Compliance Management, Risk Management, Supplier Quality, Product Quality, and Process Improvement applications while assessing adoption trends within Manufacturing, Healthcare, Automotive, Aerospace & Defense, Food & Beverage, and Consumer Goods industries. The study covers more than 10 major market participants and examines cloud deployment patterns, AI integration levels, and enterprise digital transformation strategies.

The report delivers regional assessment across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting deployment concentration, technology adoption, and industry-specific quality modernization initiatives. Coverage includes emerging areas such as predictive quality analytics, AI-driven compliance automation, supplier intelligence platforms, and connected quality ecosystems. With enterprise cloud adoption exceeding 70% in several regulated sectors, the report supports investment prioritization, expansion planning, competitive benchmarking, partnership evaluation, and long-term strategic positioning between 2026 and 2033.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 14670 Million |

|

Market Revenue in 2033 |

USD 29532.6 Million |

|

CAGR (2026 - 2033) |

9.14% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

MasterControl, ETQ, Sparta Systems, Intelex Technologies, Arena Solutions, AssurX, Qualio, Greenlight Guru, Veeva Systems, SAP, Oracle, Dassault Systèmes, Siemens Digital Industries Software, QT9 Software |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |