Reports

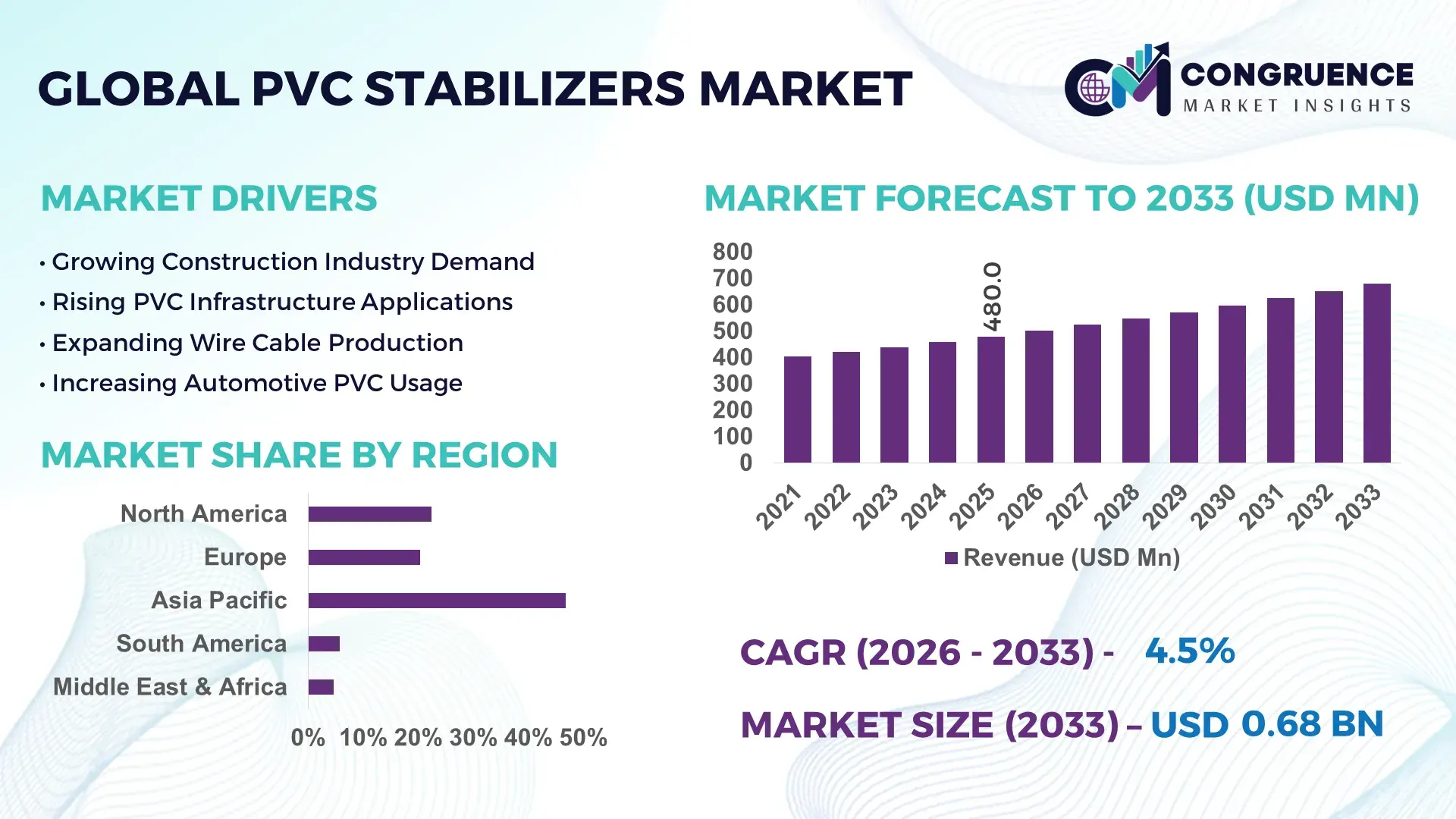

The Global PVC Stabilizers Market was valued at USD 480.0 Million in 2025 and is anticipated to reach a value of USD 681.0 Million by 2033 expanding at a CAGR of 4.47% between 2026 and 2033. Growth is being propelled by accelerating replacement of lead-based additives with calcium-zinc and organotin stabilizers across construction, wire & cable, and potable water pipe manufacturing under tightening environmental compliance frameworks.

China remains the dominant country in the global PVC stabilizers landscape, accounting for approximately 38% of global PVC production capacity and supporting over 30 million tons of annual PVC output through large-scale construction, infrastructure, and electrical manufacturing industries. Investments in advanced additive formulations and non-toxic stabilizer technologies have increased by nearly 20% across major producers. Compared with Germany’s specialty-focused production ecosystem, China maintains significantly larger volume deployment and downstream integration. Ongoing industrial policy support and post-supply-chain diversification initiatives continue strengthening domestic adoption efficiency.

Strategic implication: Suppliers with strong non-toxic stabilizer portfolios and localized manufacturing networks are positioned to secure long-term procurement contracts across infrastructure and utility value chains.

Market Size & Growth: USD 480.0 Million in 2025, reaching USD 681.0 Million by 2033 at 4.47% CAGR, supported by rapid transition toward lead-free PVC formulations and stricter compliance standards.

Top Growth Drivers: Lead-free stabilizer adoption up 28%, infrastructure PVC pipe demand up 18%, and wire & cable applications expanding by 14%.

Short-Term Forecast: By 2028, production efficiency is expected to improve by 12% through process optimization and automated additive dosing systems.

Emerging Technologies: AI-driven formulation development, advanced calcium-zinc chemistry, and automated quality monitoring are reducing formulation cycles by nearly 20%.

Regional Leaders: Asia Pacific exceeds USD 290 Million, Europe approaches USD 155 Million, and North America surpasses USD 125 Million, driven by sustainable material adoption.

Consumer/End-User Trends: More than 65% of new PVC pipe projects increasingly specify low-toxicity stabilizer systems for compliance and durability performance.

Pilot/Case Example: In 2024, multiple Chinese PVC compounders reported up to 15% improvement in processing stability after adopting advanced calcium-zinc formulations.

Competitive Landscape: Top manufacturers collectively control roughly 40% of market activity, led by Baerlocher, Songwon, Adeka, Galata Chemicals, and Valtris Specialty Chemicals.

Regulatory & ESG Impact: Lead-based stabilizer utilization declined by nearly 22% across regulated markets following stricter environmental compliance requirements.

Investment & Funding: More than USD 350 Million has been directed toward capacity expansions, sustainability upgrades, and specialty additive development initiatives.

Innovation & Future Outlook: High-performance hybrid stabilizers and circular-economy PVC solutions are reshaping competitive differentiation amid global supply-chain realignment.

PVC Stabilizers Market demand continues to strengthen across pipes, fittings, profiles, wire insulation, and medical-grade PVC applications where durability and thermal stability are critical. Recent innovations focus on advanced calcium-zinc systems, hybrid organic stabilizers, and low-VOC formulations capable of improving processing performance by over 15%. Regulatory migration away from heavy-metal additives and ongoing manufacturing localization strategies are encouraging investment in sustainable product portfolios, setting the stage for broader strategic transformation across the industry.

PVC stabilizers have become strategically important as manufacturers balance performance requirements, environmental compliance, and supply-chain resilience. The industry is undergoing a structural shift from legacy lead-based systems toward advanced calcium-zinc and organotin formulations as governments tighten material safety standards and infrastructure modernization programs accelerate demand for durable PVC products. This transition is influencing procurement strategies, product development priorities, and competitive positioning across the value chain.

Advanced calcium-zinc stabilizers deliver up to 15% better thermal stability and reduce formulation-related processing losses by nearly 10% compared with several legacy alternatives. China continues to dominate large-volume deployment through extensive PVC manufacturing capacity, while Germany and Japan emphasize specialty formulations and high-performance applications. Over the next two to three years, adoption of automated formulation management platforms is expected to increase by more than 20% among large compounders seeking consistency, quality control, and operational efficiency.

A practical example is the deployment of lead-free stabilizer systems in municipal water pipe manufacturing, where producers are expanding certified product portfolios to meet evolving regulatory requirements. Companies are strengthening partnerships with PVC compounders, investing in localized production facilities, and accelerating specialty additive development. Organizations that combine sustainable formulations, manufacturing flexibility, and application-specific expertise will establish stronger competitive advantages and long-term relevance in the evolving PVC materials ecosystem.

Environmental compliance requirements and infrastructure-grade material specifications are rapidly accelerating adoption of advanced PVC stabilizers. More than 65% of newly approved municipal piping projects increasingly favor lead-free PVC formulations, while calcium-zinc stabilizer utilization has expanded by approximately 25% over the last several years. China's large PVC processing sector and India's growing water infrastructure investments are driving substantial demand for compliant additive systems. The transition creates a direct performance advantage through improved thermal stability, regulatory acceptance, and export eligibility. In response, manufacturers are expanding specialty production lines, investing in formulation R&D, and entering strategic partnerships with PVC compounders. A notable operational insight is that suppliers capable of delivering customized stabilizer packages are securing stronger positions in long-term infrastructure and utility procurement programs.

Fluctuations in metal-based intermediates, specialty chemicals, and energy inputs continue creating cost uncertainty for PVC stabilizer manufacturers. Prices for several critical additive inputs have experienced periodic swings exceeding 15%, while logistics and transportation expenses remain elevated compared with pre-disruption levels. Germany and other manufacturing-intensive economies face additional pressure from higher industrial operating costs. These conditions directly affect pricing consistency, procurement planning, and margin performance throughout the value chain. To mitigate exposure, companies are diversifying supplier networks, negotiating longer-term sourcing agreements, and increasing regional production footprints. A significant strategic insight is that procurement resilience has become nearly as important as formulation performance when competing for large industrial and infrastructure contracts.

Next-generation stabilizer technologies are creating opportunities beyond traditional compliance-driven demand. Advanced hybrid stabilizers can improve processing efficiency by approximately 10–15% while reducing additive loading requirements by nearly 8%. India and Southeast Asian manufacturing hubs are emerging as attractive markets as industrial output and PVC conversion capacity expand. Innovation focused on recyclable PVC systems, low-VOC formulations, and digitally optimized additive design is reshaping product differentiation. Manufacturers are increasing investment in application-specific solutions for medical products, electrical infrastructure, and potable water systems. A less obvious opportunity lies in premium stabilizer packages that reduce downtime and quality variability, delivering measurable operational savings for processors while strengthening supplier-customer integration across the production ecosystem.

The industry faces increasing complexity in balancing regulatory compliance, performance consistency, and application-specific requirements across global markets. More than 30% of processors continue operating mixed production environments that require compatibility with multiple stabilizer technologies, creating formulation and qualification challenges. Certification timelines for specialized applications can extend beyond 12 months, delaying commercialization efforts. China, Europe, and North America often maintain differing compliance frameworks, increasing development complexity for multinational suppliers. Companies must invest in advanced testing capabilities, application engineering expertise, and collaborative customer validation programs to maintain competitiveness. A critical operational challenge is achieving consistent performance across recycled and virgin PVC streams while meeting evolving sustainability expectations without compromising processing efficiency or product durability.

Lead-Free Chemistry Acceleration Regulatory tightening and procurement reforms are rapidly shifting demand toward calcium-zinc and organotin stabilizers. Lead-free formulations now represent nearly 62% of new PVC compound approvals in developed markets, while adoption across water infrastructure applications has increased by 18% over the past two years. Manufacturers are restructuring product portfolios, expanding specialty additive capacity, and forming formulation partnerships with compounders. The transition is reducing compliance risks, shortening certification cycles, and improving export competitiveness for processors serving regulated end-use sectors.

Localized Supply Chain Expansion Supply-chain disruptions and geopolitical trade realignments have encouraged stabilizer producers to localize production and sourcing. More than 30% of major suppliers have expanded regional manufacturing footprints, while procurement diversification initiatives have increased by approximately 22%. India and Southeast Asia are attracting new blending and compounding investments as customers seek shorter lead times and improved supply security. The result is greater operational resilience, lower logistics exposure, and improved responsiveness to infrastructure and industrial project demand.

Advanced Processing Optimization PVC processors are increasingly adopting automated dosing systems, digital quality controls, and real-time formulation monitoring. Facilities deploying these technologies report up to 15% reductions in material variability and nearly 12% improvements in production consistency. Companies are integrating process analytics with additive management platforms to reduce waste and optimize stabilizer utilization. This operational shift is improving throughput efficiency while helping manufacturers maintain tighter performance specifications across diverse PVC applications.

Hybrid Stabilizer Innovation Growth Demand is rising for hybrid stabilizer systems that combine thermal performance, processing efficiency, and sustainability advantages. New formulations have reduced additive loading requirements by nearly 8% while improving heat stability by more than 10% in high-performance applications. In response, suppliers are increasing R&D investments, licensing specialty technologies, and collaborating with PVC converters. A notable emerging trend is the development of formulations specifically optimized for recycled PVC streams, addressing circular-economy objectives without compromising processing reliability.

Calcium-Based Stabilizers remain the leading segment, accounting for approximately 42% of global demand due to their strong regulatory acceptance, cost competitiveness, and suitability for pipes, profiles, and wire applications. Their compatibility with lead-free manufacturing strategies has accelerated deployment across China, India, and Europe. Manufacturers continue expanding production capacities and introducing enhanced calcium-zinc formulations to improve thermal stability and processing performance. Lead-Based Stabilizers still maintain relevance in selected cost-sensitive applications, although their share continues to decline due to environmental restrictions and changing procurement standards. Tin-Based Stabilizers represent the fastest-growing segment, supported by increasing adoption in transparent rigid PVC, medical-grade products, and potable water systems where superior clarity and heat resistance are critical. Demand for tin-based solutions has increased by nearly 14% in specialty applications. Barium-Zinc Stabilizers retain strategic importance in flexible PVC formulations, while other specialty stabilizers support niche industrial requirements. Companies are prioritizing innovation, application-specific product development, and compliance-focused formulations to capture premium-value opportunities and strengthen differentiation.

Pipes & Fittings remain the dominant application segment, representing approximately 45% of stabilizer consumption due to extensive deployment in water distribution, sewage infrastructure, irrigation systems, and utility networks. The segment benefits from long service-life requirements and stringent thermal stability standards. Municipal infrastructure projects across India and China continue supporting volume demand, while manufacturers are scaling production capabilities and optimizing formulations for pressure-resistant PVC systems. Profiles & Tubing also maintain substantial demand through construction and industrial applications requiring weatherability and dimensional stability. Wires & Cables constitute the fastest-growing application category, supported by expanding electrification projects, renewable energy installations, and data infrastructure investments. Adoption within this segment has increased by nearly 16% as producers prioritize fire performance and processing consistency. Coatings & Flooring applications continue expanding through commercial construction activity, while other niche applications benefit from specialized formulation requirements. Companies are increasingly integrating automated quality control systems and advanced additive packages to support high-performance operational requirements across evolving end-use environments.

Construction remains the largest end-user segment, accounting for nearly 48% of stabilizer consumption through extensive use of PVC pipes, window profiles, fittings, flooring systems, and structural components. Demand concentration is driven by infrastructure modernization, urban development programs, and utility expansion projects. Large-scale deployment requirements make performance consistency and regulatory compliance critical purchasing criteria. Manufacturers increasingly offer customized stabilizer packages and technical support programs tailored to construction-grade PVC processors. Electrical & Electronics is the fastest-growing end-user segment, supported by rising cable production, renewable energy installations, and digital infrastructure investments. Demand from this segment has expanded by approximately 15% as electrical performance requirements become more stringent. Packaging continues to represent a mature but stable market, while Automotive applications increasingly utilize specialty PVC components requiring advanced stabilization technologies. Healthcare demand is strengthening through medical tubing and specialized PVC products. Suppliers are pursuing strategic partnerships, application-focused innovation, and targeted pricing strategies to strengthen competitive positioning across these evolving customer groups.

Asia-Pacific accounted for the largest market share at 46.8% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 5.9% between 2026 and 2033.

North America represented approximately 22.4% of global PVC stabilizer demand in 2025, supported by advanced PVC processing capacity, infrastructure rehabilitation projects, and stringent material compliance standards. The region continues shifting toward calcium-zinc and organotin formulations as water infrastructure upgrades and electrical grid modernization programs increase demand for high-performance PVC compounds. More than 70% of newly specified municipal PVC pipe projects now prioritize lead-free stabilizer systems. Manufacturers are investing in automated formulation technologies and expanding specialty additive production capabilities to improve product consistency and regulatory alignment. Strategic partnerships between compounders and additive suppliers are accelerating product qualification cycles and strengthening supply security across industrial applications.

United States Market Outlook: The United States remains the dominant market due to its extensive construction sector, large PVC conversion industry, and ongoing infrastructure investment programs. More than 55% of regional stabilizer consumption is concentrated within water infrastructure, electrical cable, and construction-grade PVC applications. Domestic manufacturers continue investing in specialty formulation development and advanced production technologies to meet evolving environmental standards. Strong procurement activity from utility and municipal projects is supporting sustained demand for compliant, high-performance stabilizer solutions.

Europe accounted for nearly 20.3% of global market demand, supported by mature PVC processing industries and highly regulated material standards. The region remains at the forefront of lead-free stabilizer adoption, with sustainability objectives influencing procurement and formulation strategies across construction and industrial applications. More than 85% of newly certified PVC construction products utilize non-lead stabilizer technologies. Producers are focusing on circular-economy initiatives, recycled PVC compatibility, and advanced additive systems that support long-term compliance requirements. Investments in sustainable compounding technologies and collaborative product development programs continue reshaping competitive dynamics throughout the regional value chain.

Germany Market Outlook: Germany serves as Europe's most influential PVC stabilizer market due to its advanced manufacturing base, specialty chemical expertise, and strong industrial infrastructure. The country accounts for a significant share of regional specialty stabilizer production and remains a center for formulation innovation. German manufacturers increasingly focus on high-performance calcium-zinc and hybrid stabilizer systems, while investments in sustainable material technologies continue supporting next-generation PVC processing applications across industrial and construction sectors.

Asia-Pacific led the global PVC stabilizers market with approximately 46.8% market share in 2025, supported by extensive PVC production capacity, large-scale infrastructure development, and expanding industrial activity. The region accounts for more than half of global PVC processing output, creating substantial demand for stabilizers across pipes, fittings, profiles, and wire applications. Government-backed infrastructure investments and manufacturing expansion programs continue driving consumption. Several producers have expanded blending and compounding facilities by over 20% in recent years to meet increasing domestic demand. Strong integration between raw material suppliers, compounders, and end-use manufacturers provides a significant operational advantage.

China Market Outlook: China remains the largest country-level market globally, accounting for roughly 38% of worldwide PVC production capacity. Massive construction activity, water infrastructure deployment, and electrical manufacturing demand continue supporting stabilizer consumption. Domestic producers are increasingly investing in advanced lead-free formulations and automated production systems to improve processing efficiency and regulatory compliance. Strong downstream integration and export-oriented manufacturing capabilities position China as the most strategically important market for stabilizer suppliers seeking scale and long-term volume growth.

South America represented approximately 5.8% of global demand, supported by growing investments in water distribution networks, housing development, and industrial construction. PVC pipe and fitting applications remain the primary consumption driver as governments prioritize infrastructure modernization and utility expansion. The region benefits from increasing adoption of modern PVC processing technologies, although supply-chain efficiency and import dependency continue influencing operational performance. Several industrial projects have expanded domestic PVC processing capacity by nearly 10%, improving regional manufacturing capabilities. Producers are focusing on localized distribution networks and strategic sourcing initiatives to strengthen supply reliability.

Brazil Market Outlook: Brazil dominates regional demand through its large construction industry, expanding infrastructure investments, and established PVC processing sector. The country accounts for more than 45% of South American PVC consumption across key end-use industries. Domestic manufacturers continue modernizing production facilities and increasing utilization of advanced stabilizer technologies to improve product quality and operational efficiency. Infrastructure-focused procurement programs and urban development projects remain important demand generators for stabilizer suppliers operating in the Brazilian market.

Middle East & Africa accounted for approximately 4.7% of global market activity in 2025 and is emerging as the fastest-expanding regional opportunity. Large-scale infrastructure development, water management projects, industrial diversification initiatives, and construction investments are strengthening PVC demand across multiple sectors. Countries across the Gulf region are increasing deployment of advanced piping systems and utility infrastructure, creating new requirements for durable PVC formulations. Several industrial development programs have increased local manufacturing investment by more than 15%, encouraging broader adoption of specialty stabilizer technologies and reducing import dependency.

Saudi Arabia Market Outlook: Saudi Arabia is the most strategically significant market within the region due to extensive infrastructure development programs, industrial diversification initiatives, and growing petrochemical integration. Major utility, housing, and water distribution projects continue supporting strong PVC consumption. Domestic industrial expansion and downstream manufacturing investments are strengthening local demand for advanced stabilizer systems. The country's focus on large-scale infrastructure modernization and industrial localization provides a favorable environment for suppliers seeking long-term participation in emerging PVC value chains.

The PVC Stabilizers Market is characterized by competition between global formulation leaders such as Baerlocher, SONGWON, ADEKA Corporation, Valtris Specialty Chemicals, and Galata Chemicals versus regional suppliers competing primarily on cost and localized supply. The top five players collectively control approximately 38–42% of global market activity, creating a moderately consolidated structure. Competition is increasingly centered on regulatory-compliant formulations, supply reliability, and application-specific performance rather than price alone. Lead-free stabilizer adoption exceeds 60% in newly developed formulations, while premium calcium-zinc systems deliver up to 15% better processing stability and nearly 10% lower production variability. Global leaders compete through product innovation, technical service, and multinational supply networks, whereas regional producers focus on faster delivery and cost advantages. Current competition is shifting toward sustainable chemistry, tin-replacement technologies, and vertically integrated supply models. Regulatory approvals, formulation expertise, and customer qualification cycles create significant entry barriers. Winning requires compliant high-performance products, localized manufacturing, strong technical support, and long-term partnerships with PVC compounders and converters.

SONGWON Industrial Co., Ltd.

ADEKA Corporation

Valtris Specialty Chemicals

Galata Chemicals

Kisuma Chemicals

Reagens S.p.A.

PMC Group, Inc.

Pau Tai Industrial Corporation

Patcham FZC

Akdeniz Chemson

Nitto Kasei Co., Ltd.

Sun Ace Kakoh (Pte.) Ltd.

BASF SE

The current technology landscape is dominated by advanced calcium-zinc stabilizers, organotin systems, and integrated one-pack additive solutions. More than 65% of newly developed PVC formulations now utilize lead-free stabilization technologies to meet environmental and performance requirements. Modern one-pack stabilizers reduce formulation complexity by nearly 20% while improving production consistency by approximately 12%. Manufacturers increasingly deploy automated dosing systems and digital process monitoring platforms to enhance compound quality and reduce operational variability across high-volume processing lines.

Emerging technologies are focused on hybrid stabilizer chemistry, recycled PVC compatibility, and AI-assisted formulation optimization. Advanced calcium-organic stabilizers and multifunctional additive packages improve thermal stability by 10–15% compared with conventional systems while reducing additive loading rates by nearly 8%. Adoption of digitally optimized formulations has surpassed 25% among large-scale compounders seeking faster product qualification and lower development costs. Companies with strong specialty formulation capabilities benefit from higher-value applications in medical devices, potable water infrastructure, and electrical insulation systems.

The most disruptive shift between 2026 and 2028 will be the transition from conventional metal-based stabilization toward circular-economy-compatible systems designed for recycled PVC streams. Compared with legacy formulations, next-generation stabilizers can improve recycled material processing efficiency by up to 18%. Suppliers investing early in sustainable chemistry, automation, and application-specific technologies will gain stronger competitive positioning as compliance requirements and performance expectations continue evolving globally.

December 2024 – SONGWON Industrial entered a distribution partnership with Altek International across the Middle East, expanding PVC stabilizer market access through Altek's GCC network. The initiative strengthens regional supply coverage and customer responsiveness for high-growth construction applications. Source: www.songwon.com

July 2025 – SONGWON Industrial introduced its SONGSTAB™ Calcium Organic stabilizer family, expanding its advanced PVC stabilization portfolio. The development supports increasing demand for sustainable formulations and strengthens the company's position in lead-free PVC processing applications.

October 2025 – Baerlocher launched its Tin Replacement initiative featuring calcium-zinc technologies for regulated PVC applications. The program enables transition without additional equipment investment, supporting potable water, medical, and food-contact applications while improving regulatory compliance.

April 2026 – Baerlocher showcased PFAS-free and circular-economy additive solutions at PRSE 2026, reinforcing its sustainability strategy. The initiative supports recycled polymer processing and strengthens the company's competitive position as regulatory scrutiny of specialty additives intensifies globally.

The report provides comprehensive analysis of PVC stabilizers across major product categories including calcium-based stabilizers, lead-based stabilizers, tin-based stabilizers, barium-zinc stabilizers, and specialty formulations. It evaluates demand across pipes & fittings, wires & cables, profiles & tubing, coatings & flooring, and other industrial applications. End-user assessment covers construction, electrical & electronics, packaging, automotive, healthcare, and related sectors. Regional coverage spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, representing more than 95% of global PVC processing activity.

The study examines technology adoption trends, lead-free formulation transitions, hybrid stabilizer development, automated compounding technologies, and recycled PVC compatibility initiatives. It analyzes market positioning of leading manufacturers, emerging competitive strategies, supply-chain restructuring, and evolving regulatory frameworks. With over 60% of new formulation activity focused on sustainable stabilization systems, the report supports investment evaluation, product development planning, capacity expansion decisions, partnership strategies, and long-term competitive positioning between 2026 and 2033

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 480.0 Million |

| Market Revenue (2033) | USD 681.0 Million |

| CAGR (2026–2033) | 4.47% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Baerlocher GmbH; SONGWON Industrial Co., Ltd.; ADEKA Corporation; Valtris Specialty Chemicals; Galata Chemicals; Kisuma Chemicals; Reagens S.p.A.; PMC Group, Inc.; Pau Tai Industrial Corporation; Patcham FZC; Akdeniz Chemson; Nitto Kasei Co., Ltd.; Sun Ace Kakoh (Pte.) Ltd.; BASF SE |

| Customization & Pricing | Available on Request (10% Customization Free) |