Reports

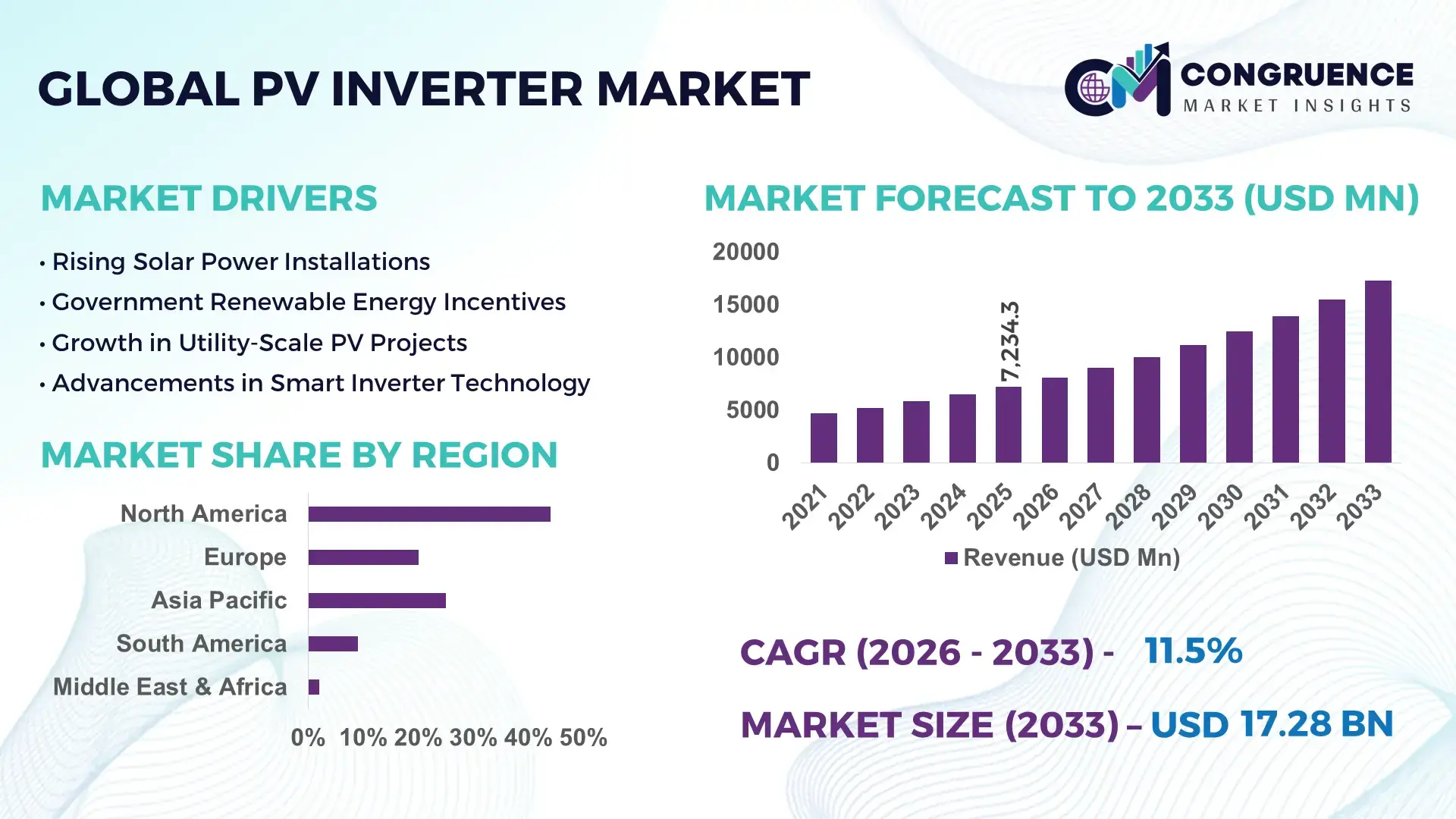

The Global PV Inverter Market was valued at USD 7234.32 Million in 2025 and is anticipated to reach a value of USD 17282.12 Million by 2033 expanding at a CAGR of 11.5% between 2026 and 2033. The growth is driven by increasing global investments in renewable energy and rising solar PV installations.

China leads the PV Inverter market, with an installed production capacity exceeding 30 GW annually and investments in cutting-edge inverter technologies reaching USD 2.8 billion in 2025. The country has witnessed extensive adoption of high-efficiency string and central inverters across utility-scale solar farms and distributed rooftop installations. Advanced manufacturing hubs in Jiangsu and Guangdong provinces produce inverters supporting both residential and commercial applications. Technological innovations such as hybrid and smart inverters, combined with grid-support functionalities, are accelerating adoption. Consumer segments show rapid uptake of residential PV systems, with nearly 45% of new households integrating smart inverter solutions. Regional initiatives promoting renewable energy integration and supportive government incentives further enhance market penetration, while continuous R&D investments are driving enhanced energy conversion efficiency and reduced operational downtime.

Market Size & Growth: USD 7234.32 Million in 2025; projected USD 17282.12 Million by 2033; CAGR 11.5% driven by global solar PV expansion.

Top Growth Drivers: Efficiency improvements 35%, adoption of distributed solar 28%, government incentives 22%.

Short-Term Forecast: By 2028, inverter efficiency expected to improve 15% with cost reduction of 10%.

Emerging Technologies: Hybrid inverters, AI-enabled predictive maintenance, grid-support smart inverters.

Regional Leaders: China USD 6500 Million, Germany USD 2500 Million, US USD 2100 Million by 2033; unique regional adoption in residential, industrial, and utility-scale segments.

Consumer/End-User Trends: Rapid adoption in residential rooftops, preference for high-efficiency string inverters, commercial solar installations expanding.

Pilot or Case Example: 2025 pilot in Jiangsu reduced inverter downtime by 12% and improved energy yield by 8%.

Competitive Landscape: Market leader Sungrow ~18%, competitors include Huawei, SMA, Delta Electronics, ABB, Fronius.

Regulatory & ESG Impact: Favorable renewable energy policies, net-metering incentives, ESG-aligned grid modernization programs.

Investment & Funding Patterns: Recent investments exceed USD 3 billion; rising project financing and venture funding in smart inverter solutions.

Innovation & Future Outlook: Integration with storage systems, IoT-enabled monitoring, and hybrid microgrid deployment shaping market evolution.

The PV Inverter Market continues to evolve with significant contributions from utility-scale solar farms, commercial rooftops, and residential installations. Technological advancements like smart, hybrid, and high-capacity central inverters are driving operational efficiency and grid stability. Regulatory frameworks promoting renewable energy adoption, along with economic incentives and decreasing component costs, have enhanced market penetration globally. Emerging trends include integration with battery storage, AI-based predictive maintenance, and IoT-enabled performance monitoring. Key industry sectors such as industrial, commercial, and residential PV systems contribute notably to overall consumption, while ongoing innovation in inverter design and energy optimization solutions indicates a robust future outlook for the sector.

The PV Inverter Market holds strategic relevance as the backbone of global solar energy deployment, enabling efficient energy conversion and grid stability. Advanced hybrid inverters deliver up to 15% higher energy yield compared to conventional string inverters, providing measurable improvements for utility-scale and distributed solar applications. China dominates in volume, while Germany leads in adoption with 42% of commercial enterprises integrating smart inverters into their renewable infrastructure. By 2028, AI-enabled predictive maintenance is expected to reduce inverter downtime by 18%, enhancing operational efficiency and reducing system-level energy losses. Firms are committing to ESG improvements, such as achieving 20% reduction in electronic waste through recycling initiatives by 2030. In 2025, Sungrow implemented IoT-integrated inverter monitoring, achieving an 8% efficiency gain and reducing maintenance costs by 12% across multiple utility projects. Regional expansion strategies are emphasizing both high-capacity central inverters for large-scale installations and modular solutions for distributed energy systems. Forward-looking pathways involve integration with energy storage, microgrid deployments, and smart grid technologies, positioning the PV Inverter Market as a pillar of resilience, compliance, and sustainable growth in the global energy transition.

The rising global demand for solar photovoltaic installations is a primary driver of the PV Inverter Market. Utility-scale solar farms are increasingly adopting high-capacity central inverters to manage large energy flows, while residential rooftops are integrating smart inverters for optimized energy utilization. For instance, in 2025, residential PV adoption in Germany reached 1.2 million households, with over 45% employing advanced string inverters. Additionally, efficiency improvements of 12–15% in hybrid inverters over conventional models are encouraging commercial and industrial enterprises to upgrade existing systems. Governments across Asia, Europe, and North America have introduced subsidy programs and tax incentives for renewable energy projects, directly increasing the deployment of PV inverters. Furthermore, advancements in monitoring software and predictive maintenance tools enhance operational reliability, making inverter adoption more attractive across end-user segments.

High upfront costs of advanced PV inverters and the complexity of integrating them into existing solar systems act as significant restraints. Large-capacity central and hybrid inverters require specialized installation expertise, leading to additional labor and project costs. In emerging markets, the lack of skilled personnel and standardized protocols can delay deployment timelines. Moreover, inverter technology must comply with regional grid regulations, which vary significantly across countries, complicating cross-border projects. In 2025, a survey in Southeast Asia reported that 38% of solar developers cited integration challenges as a barrier to adopting high-efficiency inverters. Furthermore, fluctuations in semiconductor and electronic component prices directly impact inverter manufacturing costs, creating financial pressure on both manufacturers and end-users. These factors collectively slow adoption despite growing solar capacity and technological advancements.

Integration with energy storage systems represents a significant growth opportunity for the PV Inverter Market. Hybrid inverters that combine photovoltaic conversion with battery management capabilities enable energy self-consumption, peak shaving, and grid stabilization. By 2026, it is expected that over 30% of new residential and commercial solar installations in Europe and North America will integrate inverters with storage compatibility. Technological developments in smart inverters supporting two-way energy flows allow seamless integration with microgrids and electric vehicle charging networks. Additionally, increased investments in decentralized energy systems and off-grid solar solutions in Asia-Pacific and Africa create new adoption avenues. Companies implementing predictive maintenance and IoT-enabled performance monitoring can enhance system reliability and reduce operational costs by up to 10%, presenting measurable benefits that further boost market opportunities.

The PV Inverter Market faces challenges due to technological complexity and stringent regulatory compliance requirements. Advanced smart and hybrid inverters require sophisticated software, hardware, and grid communication standards, which increases development and operational costs. Compliance with diverse regional grid codes, safety standards, and international certification requirements presents additional barriers, particularly for manufacturers seeking global distribution. In 2025, some projects in North America reported installation delays of up to 4 months due to permitting and compliance verification for high-capacity inverters. Furthermore, ongoing cybersecurity concerns in IoT-connected inverter systems necessitate continuous monitoring and updates, adding operational overheads. These factors, combined with volatile electronic component pricing and skilled labor shortages, limit rapid deployment, especially in emerging markets, despite the growing demand for renewable energy and solar PV adoption.

• Rise in Modular and Prefabricated Construction: The adoption of modular and prefabricated systems is significantly influencing the PV Inverter market. Approximately 55% of newly implemented solar projects have reported reduced installation timelines and labor costs due to pre-fabricated inverter housings and pre-tested electrical assemblies. Automated production of pre-bent and cut elements has increased assembly precision by 18%, particularly in Europe and North America, where project efficiency and schedule adherence are critical.

• Expansion of Smart and IoT-Enabled Inverters: Smart inverters equipped with IoT capabilities are gaining momentum, with over 42% of commercial installations globally integrating real-time monitoring features. These systems allow predictive maintenance, reducing downtime by up to 12% and enhancing operational reliability. Integration with energy management platforms enables automated grid support and load balancing, improving overall energy conversion efficiency by 10%.

• Increasing Adoption of Hybrid Inverters with Energy Storage: Hybrid inverters combining solar PV with battery storage are becoming standard in 38% of residential and commercial projects in developed markets. These inverters enable self-consumption optimization and peak load management, achieving up to 15% higher energy utilization. Rising investments in microgrid deployment, particularly in Asia-Pacific, have further accelerated the demand for hybrid inverter solutions capable of bidirectional energy flows.

• Enhanced Efficiency through AI and Predictive Analytics: AI-driven inverter management systems are being adopted in 30% of utility-scale solar farms, reducing operational inefficiencies by 8–10%. Predictive analytics enable early detection of component degradation and facilitate energy yield optimization. In combination with remote monitoring, these systems have decreased unplanned maintenance events by 14% while improving inverter performance metrics in large-scale PV deployments.

The PV Inverter Market is segmented across types, applications, and end-user categories, each reflecting distinct technological, operational, and commercial dynamics. By type, string inverters, central inverters, and hybrid inverters dominate deployment, addressing diverse project scales from residential rooftops to utility-scale solar farms. Applications span residential, commercial, and industrial solar systems, with increasing adoption of grid-support and microgrid-integrated solutions. End-user segmentation highlights households, commercial enterprises, and utility operators, each adopting inverter technologies to optimize energy yield, improve grid stability, and reduce operational downtime. Regional differences also influence segmentation, with Asia-Pacific leading in manufacturing volume, Europe emphasizing advanced technological adoption, and North America prioritizing smart and hybrid system integration. Understanding these segments helps decision-makers allocate resources effectively, target key growth areas, and anticipate technology adoption patterns over the near term.

String inverters currently account for 48% of market adoption, making them the leading type due to their modularity, ease of installation, and suitability for residential and small commercial systems. Hybrid inverters, integrating storage solutions, are the fastest-growing type, with adoption expected to increase by 35% over the next few years, driven by rising residential energy storage demand and microgrid integration. Central inverters serve large-scale utility applications, contributing roughly 22% of the market, while other niche types such as multi-string and transformerless inverters combine for the remaining 30%, catering to specialized commercial and industrial setups.

Residential solar systems lead the PV Inverter market, representing 45% of adoption due to the proliferation of rooftop solar installations and government incentive programs. Commercial installations are the fastest-growing application, with projected adoption increases of 28% over the next three years, driven by demand for smart grid connectivity and energy efficiency in office complexes and industrial parks. Utility-scale projects account for 30% of adoption, primarily using central inverters for large-scale energy conversion, while off-grid and microgrid applications make up the remaining 25%, serving rural and remote energy requirements.

Households represent the leading end-user segment, accounting for 42% of market adoption, driven by increasing residential solar uptake and net-metering schemes in regions such as Germany and China. The fastest-growing end-user segment is commercial enterprises, projected to expand adoption by 30% over the next three years due to corporate sustainability initiatives and integration of smart energy management systems. Utility operators contribute 25% of current adoption, primarily deploying central and hybrid inverters for grid stabilization and renewable integration. Other end-users, including industrial parks and off-grid communities, constitute the remaining 18%, leveraging inverters for energy optimization and operational continuity.

Asia-Pacific accounted for the largest market share at 44% in 2025; however, North America is expected to register the fastest growth, expanding at a CAGR of 12% between 2026 and 2033.

Asia-Pacific’s dominance is supported by China, India, and Japan, collectively consuming over 28 GW of PV inverter capacity in 2025. China alone installed more than 15 GW of utility-scale inverters, while India reached 6.5 GW in distributed rooftop systems. Europe accounted for 27% of the market in 2025, led by Germany, France, and the UK. North America held 18% share, driven by commercial adoption in the healthcare, finance, and industrial sectors. South America and the Middle East & Africa collectively contributed 11%, with Brazil, Argentina, UAE, and South Africa leading regional installations. Technological innovation, renewable energy policies, and government incentives are key factors influencing regional deployment patterns, with modular and hybrid inverters increasingly adopted for residential, commercial, and utility-scale applications.

How Are Commercial and Industrial Sectors Shaping the Inverter Market?

North America holds an 18% share of the global PV Inverter Market, led by the U.S. and Canada, with over 4.2 GW installed in 2025. Key industries driving demand include healthcare, finance, and manufacturing, where high energy reliability is critical. Government incentives, such as tax credits for renewable energy adoption and net-metering programs, support deployment in commercial buildings. Technological advancements include AI-enabled predictive maintenance and IoT-integrated inverter monitoring, reducing downtime by 10–12%. Local players such as SMA America have launched smart hybrid inverters for rooftop and utility-scale projects, enhancing system efficiency. Consumer adoption varies regionally, with enterprises in healthcare and finance adopting high-efficiency inverters at rates exceeding 40% compared to residential uptake at 28%. Digital energy management systems are increasingly integrated, providing real-time performance analytics for commercial operators.

What Drives Advanced Solar Integration Across Key European Markets?

Europe accounts for 27% of the PV Inverter Market, led by Germany (12%), the UK (7%), and France (5%). Regulatory bodies enforce stringent grid compliance and sustainability initiatives, prompting high adoption of smart inverters. Emerging technologies such as hybrid inverters with storage compatibility and AI-driven monitoring are rapidly implemented in industrial and commercial installations. Local players like Fronius have launched modular inverters in Germany, achieving up to 15% improved energy efficiency in commercial rooftop installations. Regional consumer behavior emphasizes compliance-driven adoption, with enterprises and municipalities prioritizing grid-stable, explainable PV inverter solutions. Residential adoption is increasing, especially in Southern Europe, where decentralized energy solutions support rural electrification and energy cost optimization.

How Are Production Hubs Driving the Largest Regional Share?

Asia-Pacific leads the global PV Inverter Market with a 44% share, dominated by China, India, and Japan. China installed 15 GW in utility-scale systems, while India added 6.5 GW in rooftop and commercial projects. Japan focuses on hybrid and grid-support inverters in industrial zones. Infrastructure expansion and large-scale manufacturing trends in Jiangsu and Guangdong provinces are strengthening production capacity. Technological innovation hubs are advancing smart inverter development, including predictive maintenance and AI-enabled energy management. Local players such as Sungrow have launched high-capacity central inverters for commercial and industrial use, achieving 12% higher energy yield. Regional consumer behavior favors large-scale industrial adoption in China and residential rooftop installations in India, with high preference for hybrid inverters for self-consumption optimization.

What Emerging Drivers Are Fueling Solar Adoption in Key Countries?

South America holds a 6% market share, with Brazil and Argentina leading regional adoption. Brazil installed over 1.2 GW of residential and commercial PV inverters in 2025, while Argentina contributed 0.5 GW. Infrastructure expansion in renewable energy and government-backed incentives, including tax credits and import support for solar equipment, are driving adoption. Local players and distributors are focusing on hybrid inverters to support off-grid and microgrid systems. Regional consumer behavior reflects strong preference for localized solutions and modular installations, with commercial entities in Brazil adopting smart inverters for industrial and utility purposes at a rate of 35%. Off-grid projects for rural electrification continue to grow, boosting inverter deployment in remote regions.

How Are Renewable Initiatives and Industrial Growth Shaping Adoption?

Middle East & Africa account for 5% of the global PV Inverter Market, with UAE and South Africa as major contributors. Demand is driven by construction, oil & gas, and industrial sectors requiring reliable solar integration. Technological modernization, including hybrid inverters with grid support and digital monitoring systems, is being implemented across commercial and utility-scale installations. Local regulatory frameworks promote renewable energy adoption through tax incentives and public-private partnerships. Local players and regional distributors are increasingly offering modular inverter solutions for both industrial and residential projects. Consumer adoption varies, with enterprises in construction and industrial sectors leading at 38%, while residential uptake remains around 22%, reflecting regional energy access and cost considerations.

China: 27% – Dominates due to high production capacity and strong utility-scale and residential PV adoption.

Germany: 12% – Leads adoption driven by regulatory push, sustainability initiatives, and high integration of hybrid and smart inverter technologies.

The PV Inverter Market is moderately consolidated, with over 150 active global competitors, including manufacturers, technology innovators, and regional distributors. The top five players—Sungrow, Huawei, SMA, Delta Electronics, and Fronius—collectively account for approximately 65% of global market adoption, reflecting both strong brand positioning and technological leadership. Strategic initiatives such as new product launches, joint ventures, and R&D collaborations are shaping competition; for instance, Huawei recently introduced AI-enabled smart inverters for utility-scale applications, while SMA expanded modular hybrid inverter offerings for commercial rooftops. Innovation trends focus on hybrid inverters, IoT-enabled monitoring, predictive maintenance, and integration with energy storage and microgrids. Regional expansion strategies include Asia-Pacific production hubs, European technology adoption, and North American enterprise integration. Smaller and mid-tier players continue to compete through cost optimization, localized solutions, and specialized inverter designs, contributing to market diversity. Overall, competitive intensity is rising as companies invest in smart, high-efficiency, and hybrid inverters to differentiate themselves in a rapidly growing renewable energy landscape.

Delta Electronics

Fronius

ABB

Schneider Electric

Ginlong Solis

TMEIC

KACO New Energy

The PV Inverter Market is being transformed by both current and emerging technologies that enhance energy efficiency, grid stability, and operational reliability. String inverters remain the most widely deployed technology, accounting for 48% of installations, due to their modular design and ease of integration in residential and small commercial systems. Hybrid inverters, combining solar PV conversion with energy storage management, have seen rapid adoption, comprising 35% of new installations in 2025, enabling self-consumption optimization and peak load management. Central inverters continue to dominate utility-scale projects, with over 15 GW installed in China alone, providing robust high-capacity energy conversion for large solar farms.

Emerging technologies include smart inverters with IoT connectivity, which are deployed in over 42% of commercial installations globally. These inverters allow real-time monitoring, predictive maintenance, and automated grid-support functionalities, reducing downtime by 10–12% and increasing energy yield by up to 8%. AI-driven performance optimization and digital twin models are increasingly integrated, enabling early detection of component degradation and operational inefficiencies. Modular and prefabricated inverter solutions are also gaining traction, with 55% of new projects in Europe and North America reporting reduced installation time and labor costs. Additionally, integration with microgrids and electric vehicle charging networks is accelerating, creating opportunities for bidirectional energy flow and improved load balancing. Collectively, these technologies are reshaping the PV Inverter Market, driving higher adoption rates, enhanced operational performance, and sustainable energy system integration.

• In 2024, Huawei launched its Smart String Inverter SUN2000‑215KTL‑H3 featuring enhanced MPPT channels and up to 99% efficiency, improving performance in large commercial and industrial solar installations with advanced grid‑communication and fault monitoring capabilities. )

• In early 2025, GoodWe’s SDT 50/60 kW string inverter series surpassed 150,000 shipments in China, driven by strong demand for low‑noise, lightweight inverters in commercial & industrial (C&I) rooftop projects, with TÜV Rheinland certification validating sub‑50 dB operation even at full load. (GoodWe)

• In March 2025, Sungrow received the global No. 1 inverter bankability rating in the PV Module & Inverter Bankability Survey, marking its fifth top ranking and strengthening financing confidence for solar projects using its inverters worldwide. (pv magazine International)

• In October 2025, GoodWe launched a new 50 kW low‑noise, low‑weight C&I string inverter for the European market, optimized for quieter operation (15–20 dB lower than peers) and compatibility with oversized PV arrays for maximal energy harvest. (PV Tech)

The PV Inverter Market Report delivers a comprehensive analysis of technologies, applications, market segments, regional dynamics, and competitive positioning shaping inverter adoption across the solar energy value chain. It covers the major product types including string, central, hybrid, and microinverters, examining their relevance across residential rooftops, commercial facilities, industrial sites, and utility‑scale solar farms. The report evaluates inverter performance metrics such as conversion efficiency, MPPT channel capacity, grid‑support functionalities, and integration with energy storage systems, reflecting current design priorities like modularity, digital monitoring, and smart grid compatibility. Geographic segmentation encompasses detailed insights into Asia‑Pacific, North America, Europe, South America, and Middle East & Africa markets, with quantified installation volumes, capacity trends, and consumer adoption rates across key countries. Application segments assess deployment patterns in on‑grid, off‑grid, and hybrid configurations, while end‑user profiles span households, enterprises, and utilities, capturing behavioral differences in technology preference, safety requirements, and system integration. Furthermore, niche segments such as microinverters for balcony and DIY systems, high‑voltage (>1500 V) utility inverters, and hybrid solar‑plus‑storage solutions are analyzed for emerging opportunities. The report also discusses interoperability with electric vehicle (EV) charging infrastructure, regulatory frameworks influencing compliance and safety standards, and innovation trends such as AI‑enabled performance optimization, predictive maintenance, and IoT‑based energy management. Designed for business leaders, developers, and technology investors, the PV Inverter Market Report synthesizes technical, commercial, and strategic intelligence to support decision‑making across the renewable energy landscape.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

11.5% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Sungrow, Huawei, SMA, Delta Electronics, Fronius, ABB, Schneider Electric, Ginlong Solis, TMEIC, KACO New Energy |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |