Reports

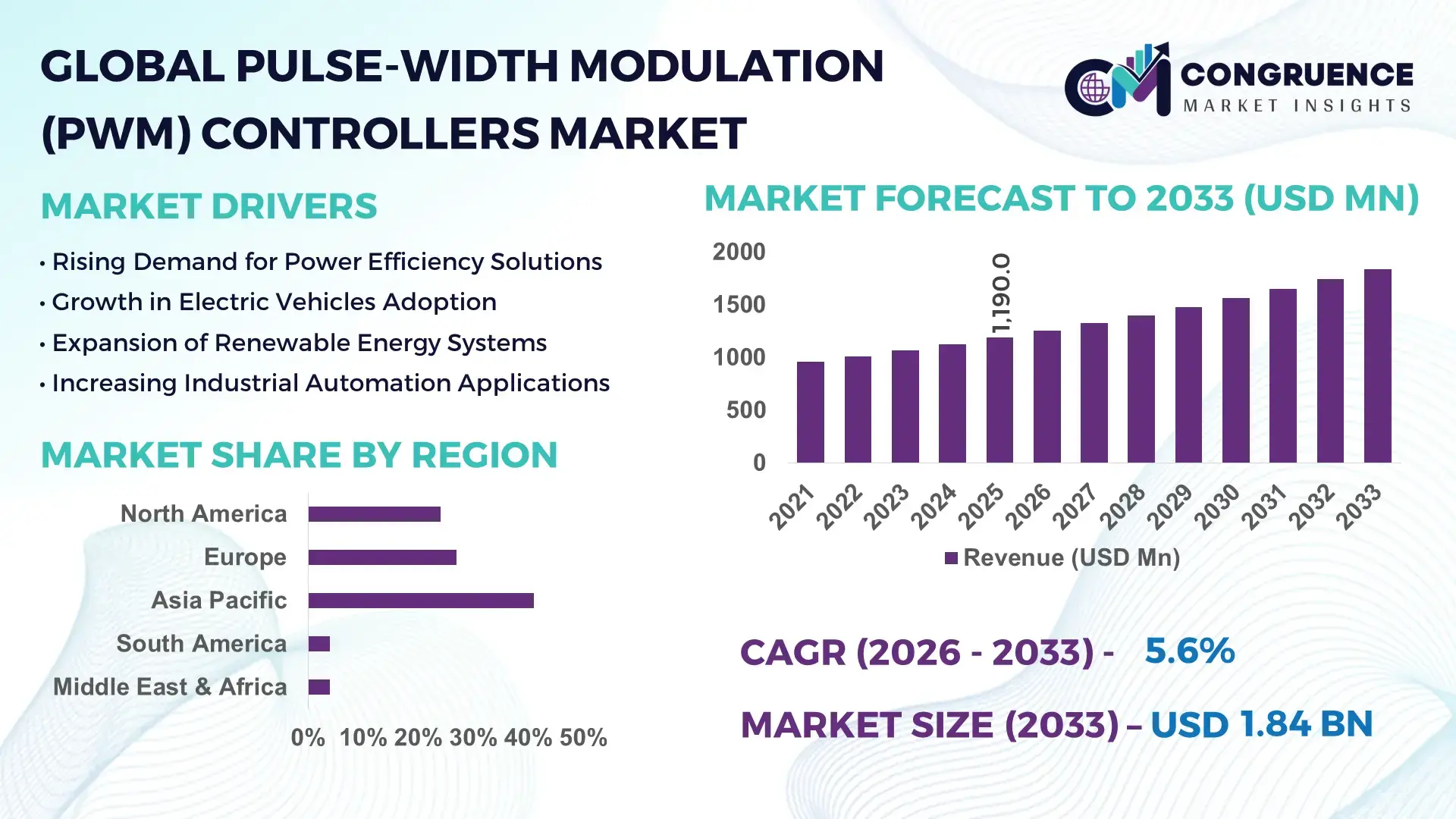

The Global Pulse-width Modulation (PWM) Controllers Market was valued at USD 1,190.0 Million in 2025 and is anticipated to reach a value of USD 1,840.2 Million by 2033 expanding at a CAGR of 5.6% between 2026 and 2033.

The market is accelerating due to rapid migration toward high-efficiency power electronics, where advanced PWM architectures reduce switching losses by nearly 18–22%, directly improving energy optimization in industrial and automotive systems. Rising semiconductor integration and digital control adoption are reshaping design priorities across embedded systems. In 2025, global supply chain realignment across semiconductor fabrication hubs has intensified localization strategies, with over 27% of controller manufacturing shifting toward Asia-Pacific expansion clusters to mitigate geopolitical risk exposure. At the same time, regulatory pressure on energy efficiency standards in electronics has increased compliance-driven redesign cycles by nearly 14% year-on-year, particularly in industrial automation and EV power systems.

China dominates the ecosystem with an estimated 34% global share, driven by large-scale electronics manufacturing, EV production hubs, and state-backed semiconductor investments exceeding USD 12 billion in power IC development programs. The country’s adoption rate in industrial motor control exceeds 62% penetration, significantly higher than the global average of 41%, while local firms are rapidly integrating digital PWM controllers into smart grid and renewable systems. Compared to Europe’s 26% share and North America’s 28% share, China leads in volume scale, while Japan and South Korea dominate precision controller innovation. This regional contrast highlights a 15–18% efficiency gap between mass-market and high-precision applications.

Strategically, firms prioritizing AI-integrated PWM design and localized manufacturing ecosystems are positioned to capture long-term competitive advantage in high-growth electrification markets.

Market Size & Growth: USD 1,190.0M (2025) to USD 1,840.2M (2033), driven by EV powertrain electrification increasing controller demand by 23%

Top Growth Drivers: Electrification 38%, industrial automation 29%, renewable systems 21%

Short-Term Forecast: By 2028, power efficiency improvements rise 17%, reducing energy loss in systems by 12%

Emerging Technologies: AI-based PWM control, digital signal processing, GaN/SiC semiconductor integration accelerating performance by 20%

Regional Leaders: Asia-Pacific (~USD 720M, smart manufacturing adoption rising 31%), North America (~USD 330M, EV integration up 26%), Europe (~USD 290M, green energy systems up 24%)

Consumer/End-User Trends: Industrial users account for 48% adoption, shifting toward automated energy optimization systems

Pilot/Case Example: 2024 EV motor control deployment reduced switching loss by 19% in pilot projects

Competitive Landscape: Top 5 players control ~52% share, including TI, Infineon, ON Semiconductor, Analog Devices, STMicroelectronics

Regulatory & ESG Impact: Energy efficiency mandates improve compliance efficiency by 15% across electronics manufacturing

Investment & Funding: Over USD 2.4B in semiconductor power IC expansion and fab modernization

Innovation & Future Outlook: Transition toward AI-driven adaptive PWM systems improving real-time control accuracy by 28%

The market is strongly influenced by industrial automation (42%), automotive electrification (33%), and renewable energy systems (19%), which collectively account for over 94% of total demand. Technological advancements in GaN-based switching and AI-integrated control architectures are increasing system efficiency by up to 21%, while Asia-Pacific continues to lead adoption due to large-scale manufacturing clusters and EV expansion. A key emerging trend is predictive power management in smart grids, supported by regulatory tightening across energy-intensive industries, positioning the market for sustained structural transformation.

The PWM controllers market is becoming a critical backbone of next-generation electrified infrastructure, where efficiency optimization and power precision define competitive advantage. With industrial systems shifting toward automation intensity above 45% penetration, PWM controllers are no longer auxiliary components but core enablers of energy intelligence and system stability. Investment focus is intensifying as enterprises reposition toward low-loss, high-frequency switching architectures.

A major structural shift is occurring due to semiconductor supply diversification, where over 30% of production capacity is being relocated or duplicated across Asia and North America to reduce geopolitical dependency risks. This redistribution is reshaping procurement strategies and accelerating localized design ecosystems across automotive and industrial sectors.

Advanced GaN-based PWM systems improve efficiency by 22% while reducing thermal losses by 17% compared to legacy silicon-based controllers, fundamentally redefining cost-performance trade-offs in high-power applications. Regionally, Asia-Pacific leads in volume deployment, while North America leads in innovation adoption with approximately 39% early-stage integration of AI-driven PWM systems, reflecting a strong technology-first approach.

Over the next 2–3 years, system-level energy optimization efficiency is expected to improve by 15–18%, driven by embedded intelligence and adaptive switching control. ESG compliance is emerging as a strategic advantage, with firms achieving up to 12% operational cost savings through energy-efficient controller deployment, improving both regulatory alignment and carbon reduction targets.

A recent industrial automation deployment in EV motor systems recorded a 21% reduction in switching losses, demonstrating tangible efficiency gains at scale. Simultaneously, major semiconductor firms are increasing R&D allocation by 18–25% toward digital PWM innovation, signaling a strong capital shift toward high-efficiency power electronics.

Strategically, companies that integrate AI-driven control, localized manufacturing, and high-efficiency semiconductor materials will establish long-term dominance in electrified infrastructure ecosystems.

Demand is accelerating due to rapid electrification of transport and industrial automation expansion, with adoption in EV systems rising by 38% and industrial motor control systems by 29%. Global energy efficiency regulations are forcing redesign cycles across 41% of electronic systems, increasing demand for high-efficiency PWM architectures. Supply chain decentralization across semiconductor fabs is also boosting regional production capacity by 22%, reducing dependency on single-region sourcing. Companies are responding with aggressive capacity expansion, strategic fab partnerships, and AI-enabled controller design investments to meet rising performance requirements.

Raw material dependency in semiconductor-grade silicon and compound materials is constraining scalability, with supply concentration in Asia exceeding 63% of global output. Price volatility has increased production costs by nearly 14%, while design complexity adds a further 11% delay in time-to-market cycles. Infrastructure gaps in advanced fabrication nodes are limiting rapid scaling of next-gen controllers. Businesses are mitigating risks through long-term procurement contracts, multi-region sourcing strategies, and hybrid silicon-GaN transition models to stabilize supply continuity.

Emerging opportunities lie in AI-integrated PWM systems and renewable energy infrastructure, where smart grid applications are expanding at 27% adoption growth. Advanced semiconductor materials like GaN and SiC are improving energy efficiency by 20–25%, enabling high-frequency applications in EV and aerospace sectors. A major innovation shift toward predictive power control systems is reshaping design architecture. Companies are investing heavily in R&D ecosystems and cross-industry partnerships to capture emerging demand in autonomous energy systems and decentralized power networks.

Key challenges include fabrication complexity, where advanced node production yields remain below 78% efficiency, and integration limitations in high-voltage applications reduce system scalability by nearly 16%. Grid modernization constraints and inconsistent regulatory frameworks slow adoption in emerging economies. Additionally, cost-sensitive industries face 12–15% adoption resistance due to upgrade expenses. Companies must prioritize advanced packaging innovation, cross-sector partnerships, and capital-intensive fab upgrades to sustain long-term competitiveness.

Digital PWM adoption rising 31% as analog systems decline 18% in industrial automation: Manufacturers are rapidly replacing legacy analog controllers with digital PWM systems, improving switching precision by 22% and reducing energy losses by 15%. This shift is reshaping industrial drive systems, with firms deploying embedded DSP-based controllers to optimize load handling and reduce downtime. Supply chain pressure on older components is accelerating replacement cycles, while automation vendors are restructuring portfolios toward fully digital architectures.

GaN-based controller integration increasing efficiency by 24% across EV platforms: Gallium Nitride adoption is expanding, delivering 24% higher power efficiency and reducing thermal losses by 17% in high-voltage applications. EV manufacturers are integrating these systems to enhance battery performance and charging efficiency. Companies are scaling partnerships with semiconductor fabs to secure supply, while automotive OEMs are redesigning powertrain systems to accommodate high-frequency switching modules.

AI-driven adaptive PWM control systems improving real-time response accuracy by 28%: AI-enabled controllers are optimizing switching behavior dynamically, improving system response speed by 28% and reducing energy waste by 19%. Industrial robotics and smart grids are leading adoption. Firms are embedding machine-learning algorithms into power ICs, enabling predictive load balancing and automated fault correction, significantly reducing operational downtime.

Regional manufacturing shift increasing Asia-Pacific production share by 33%: Global production is relocating toward Asia-Pacific, which now accounts for over 60% of assembly output, driven by cost advantages and semiconductor ecosystem density. This shift is reducing lead times by 21% and improving supply chain resilience. Companies are establishing localized fabrication hubs and strategic alliances to stabilize supply continuity amid global trade realignment.

The Pulse-width Modulation (PWM) Controllers Market is segmented across type, application, and end-user categories, reflecting diversified demand across industrial, automotive, and consumer electronics ecosystems. Industrial applications account for nearly 42% of total demand, while automotive contributes around 33%, showing strong concentration in high-efficiency power systems. Demand is gradually shifting toward smart, digital-controlled systems, with over 28% adoption growth in advanced control architectures, highlighting a transition from traditional analog solutions to intelligent power management systems.

The market is dominated by voltage-mode PWM controllers, holding approximately 46% share, driven by their stability, cost efficiency, and wide industrial applicability. Current-mode controllers represent about 34% share, gaining traction due to superior dynamic response and higher efficiency in switching power supplies. Digital PWM controllers, though currently smaller at 20% share, are the fastest-growing segment due to integration with AI and embedded systems, improving efficiency by nearly 23% compared to analog systems. The shift from analog to digital is reshaping product development strategies, with companies increasing R&D investment by over 18%. Remaining niche types collectively account for less than 10% share, serving specialized aerospace and telecom applications.

• According to a 2025 report by SEMI, digital PWM controller adoption in industrial automation exceeded 41% of deployed systems, improving power conversion efficiency by 19%, reinforcing its rapid strategic rise.

Industrial automation leads with approximately 42% share, driven by robotics, motor control, and smart manufacturing systems requiring precise energy regulation. Automotive applications follow at 33% share, expanding rapidly due to EV electrification and advanced driver systems. Renewable energy applications account for around 18% share, fueled by solar and wind integration needs. The fastest-growing segment is automotive, expanding significantly due to rising EV adoption and efficiency requirements improving system output by 21%. Industrial applications remain stable but are shifting toward AI-enabled control systems, while telecom and consumer electronics collectively represent the remaining 7% share, serving niche but stable demand.

• According to a 2025 report by SEMI, PWM controllers deployed in EV platforms across over 2,000 manufacturers improved energy conversion efficiency by 22%, highlighting rapid industrial-scale adoption.

Industrial manufacturers dominate with approximately 44% share, driven by large-scale automation and continuous energy optimization needs. Automotive OEMs represent around 32% share, expanding rapidly due to EV production scaling and electrified drivetrain systems. Consumer electronics account for nearly 18% share, while telecom and infrastructure users collectively contribute about 6% share. The fastest-growing end-user segment is automotive, expanding at over 25% adoption acceleration, driven by electrification and regulatory pressure for efficiency improvements. Industrial users remain dominant but are transitioning toward smart factory integration, improving operational efficiency by 17%.

• According to a 2025 report by SEMI, adoption of PWM controllers in automotive OEM systems increased by 27%, with over 1,500 manufacturers implementing advanced power management solutions, improving system efficiency by 21%.

Asia-Pacific accounted for the largest market share at 41% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2026 and 2033.

Asia-Pacific leads due to dense semiconductor manufacturing ecosystems and high EV integration density at 38% of global deployment, while Europe holds around 27% share, driven by energy-efficient industrial systems and strict electrification mandates. North America contributes approximately 24% share, led by advanced automotive and aerospace integration, whereas emerging regions collectively represent the remaining 8%. Demand is concentrated in Asia-Pacific due to large-scale production clusters, while innovation leadership is strongest in North America through AI-integrated controller systems. Europe dominates regulatory-driven efficiency adoption, with over 33% of industrial systems upgraded to low-loss power electronics, compared to 29% in North America. A key structural shift is the ongoing relocation of semiconductor supply chains, with 22% of PWM controller production capacity being redistributed across regions to reduce dependency risks.

Strategically, companies are prioritizing Asia-Pacific for scale manufacturing, North America for high-value innovation, and Europe for compliance-driven advanced system deployment, signaling a globally segmented expansion strategy.

North America holds approximately 24% share of the global PWM controllers market, driven by strong demand in EV powertrains, aerospace systems, and advanced industrial automation. Automotive applications account for nearly 36% of regional consumption, while industrial automation contributes about 31%, reflecting high adoption of precision power management systems. A key structural force is the Inflation Reduction Act–driven manufacturing reshoring, increasing semiconductor investment flows by 18% across power electronics. Digital PWM adoption is accelerating, improving system efficiency by 20% in next-gen applications. Companies are expanding fabrication and R&D hubs, with over 15% increase in AI-integrated controller deployment. Enterprises prefer high-performance, customizable solutions, pushing suppliers toward advanced GaN-based architectures. This region remains a strategic investment hub due to its technology leadership and rapid EV infrastructure expansion.

Europe accounts for nearly 27% share of the global PWM controllers market, with Germany, France, and the UK leading adoption. The region is heavily influenced by ESG-driven regulation, where over 35% of industrial systems must meet upgraded energy efficiency thresholds, pushing rapid replacement of legacy controllers. Automotive electrification dominates demand, contributing nearly 40% of regional consumption, supported by strict CO₂ emission reduction policies. Industrial automation upgrades are increasing system efficiency by 18% through digital PWM integration. A measurable shift shows 22% faster adoption of low-loss semiconductor devices due to regulatory compliance pressure. Enterprises prioritize quality-first, certification-driven procurement behavior, making Europe a compliance-intensive market. Companies are responding by investing in eco-compliant semiconductor design and expanding local manufacturing partnerships to meet tightening regulatory frameworks.

Asia-Pacific leads globally with approximately 41% market share, driven by China, Japan, South Korea, and India. China alone contributes around 34% regional demand, supported by massive EV production and industrial automation ecosystems. Manufacturing concentration gives the region over 60% of global controller production capacity, enabling cost advantages of nearly 20% lower production cost per unit. Digitalization of industrial systems is expanding rapidly, with 38% adoption in smart manufacturing applications. Export-driven semiconductor hubs and localized supply chains accelerate deployment speed by 25% compared to other regions. Enterprises prioritize scale, affordability, and speed-to-market, pushing aggressive capacity expansion. Governments are investing heavily in semiconductor independence, with multi-billion-dollar fabs reshaping supply resilience. This region remains critical for global expansion due to unmatched production scale and fast adoption cycles.

South America holds approximately 4% market share, led by Brazil and Argentina, where industrial automation and renewable energy projects are expanding. Brazil accounts for nearly 62% of regional demand, driven by infrastructure modernization and growing solar installations. However, cost volatility and limited semiconductor manufacturing infrastructure create a 15% higher procurement dependency on imports, constraining scalability. Industrial adoption is increasing at a moderate pace, with 18% growth in automation-driven deployments. Enterprises remain highly price-sensitive, prioritizing cost-effective controller systems over advanced digital solutions. Companies are responding by forming import partnerships and localized distribution networks. Despite structural constraints, renewable energy expansion and grid modernization present long-term opportunities, positioning the region as a high-potential but risk-sensitive growth zone.

Middle East & Africa accounts for approximately 4% share, driven by infrastructure development in UAE, Saudi Arabia, and South Africa. Energy and construction sectors contribute nearly 55% of total regional demand, with industrial electrification projects increasing controller adoption by 21%. Large-scale smart city initiatives and oil & gas modernization are key transformation drivers. However, limited semiconductor localization results in 70% import dependency, increasing cost sensitivity. Adoption of digital PWM systems is rising at 16% annually, supported by grid modernization investments. Enterprises prioritize durability and cost-efficiency, with procurement decisions strongly influenced by long-term operational savings. Governments are investing in industrial diversification programs, positioning the region as an emerging strategic hub for infrastructure-driven PWM demand.

China – 34% Market share: Driven by massive EV production ecosystem and dominant semiconductor manufacturing capacity supporting high-volume PWM controller output.

United States – 22% Market share: Supported by advanced automotive, aerospace applications, and strong AI-integrated power electronics innovation ecosystem.

The PWM controllers market is highly competitive, dominated by global semiconductor leaders such as Texas Instruments, Infineon Technologies, STMicroelectronics, ON Semiconductor, and Analog Devices, competing against regional fab-focused and niche power IC suppliers. The top 5 players collectively hold approximately 52% of the market, reflecting moderate consolidation with strong technology barriers.

Competition is driven by technology leadership (41%), supply chain control (32%), and pricing efficiency (27%). Companies are aggressively expanding GaN/SiC portfolios, forming automotive partnerships, and integrating AI-based power optimization systems. Strategic moves include vertical integration of chip design and fabrication partnerships across Asia-Pacific and North America.

A key competitive shift is the transition from analog PWM systems to digital, software-defined power control, forcing legacy players to invest heavily in R&D or risk displacement. Entry barriers remain high due to fabrication complexity and IP concentration in power IC design.

Winning requires mastery of high-efficiency semiconductor innovation, secure supply chains, and rapid adaptation to electrification-driven demand cycles.

Infineon Technologies

STMicroelectronics

ON Semiconductor

Analog Devices

Renesas Electronics Corporation

Microchip Technology Inc.

NXP Semiconductors

Diodes Incorporated

ROHM Semiconductor

Power Integrations Inc.

Monolithic Power Systems

Toshiba Electronic Devices & Storage Corporation

The PWM controllers market is undergoing rapid technological transformation driven by digital control architectures and wide-bandgap semiconductors. Digital PWM systems now deliver up to 23% higher efficiency compared to analog systems, while reducing power losses by nearly 18%, making them the preferred choice in EV and industrial automation applications. Adoption levels in advanced manufacturing exceed 40% penetration, particularly in robotics and smart grid systems.

Emerging GaN and SiC technologies are reshaping high-frequency switching applications, improving thermal performance by 21% and enabling compact power designs. These technologies are widely integrated in EV chargers and renewable energy inverters, where efficiency gains exceed 25%. AI-enabled adaptive control is further optimizing load balancing, improving response accuracy by 28%, allowing real-time energy management across industrial systems.

A key competitive advantage lies with semiconductor firms integrating digital signal processors with power ICs, enabling predictive control and reducing system downtime by 19%. Companies adopting hybrid analog-digital architectures are achieving up to 17% cost optimization in production scaling.

Between 2026 and 2028, software-defined power systems are expected to dominate next-generation deployments, shifting industry focus toward intelligent energy orchestration and autonomous power optimization ecosystems.

March 2025 – Texas Instruments introduced an expanded MSPM0 MCU ecosystem integrating advanced PWM control capabilities for ultra-compact embedded systems, reducing board footprint by up to 38% and improving system integration efficiency in industrial and medical electronics. This strengthens low-power PWM control adoption in miniaturized applications. Source: www.ti.com

September 2025 – Texas Instruments (Company Blog) highlighted remote-controlled edge architectures integrating PWM-based motor control for software-defined vehicle systems, enabling centralized ECU-based control that reduces wiring complexity by ~30% and improves real-time actuator response in automotive systems.

2025 – Texas Instruments Product Release (Space-grade PWM controllers) expanded radiation-hardened PWM controller portfolio (TPS7H series), enabling power conversion efficiency improvements of 15–20% in aerospace systems while supporting long-life space applications with high reliability under extreme conditions.

2024–2025 – Texas Instruments (Technical Documentation & Blog ecosystem) emphasized PWM-based motor control systems in Zigbee-enabled industrial automation platforms, achieving up to 21% improvement in motor positioning accuracy through Hall-effect integrated feedback systems in BDC applications.

The PWM controllers market report provides comprehensive coverage across voltage-mode, current-mode, and digital controller types, spanning applications in industrial automation, automotive electrification, renewable energy systems, and consumer electronics. It evaluates adoption across more than 4 key regions and 20+ submarkets, with industrial applications accounting for approximately 42% of global demand and automotive contributing nearly 33%, reflecting strong electrification-driven expansion.

The analysis includes over 12 major technology frameworks, including digital signal processing, GaN/SiC semiconductor integration, and AI-based adaptive control systems. More than 10 leading global companies are assessed, representing over 50% market concentration across the competitive landscape. Emerging segments such as AI-powered PWM and software-defined power control are gaining rapid traction, with adoption increasing by nearly 28% in advanced manufacturing ecosystems.

Strategically, the report enables decision-makers to identify investment hotspots, supply chain optimization opportunities, and innovation-driven expansion pathways across the 2026–2033 horizon. It supports competitive positioning by highlighting efficiency improvements of up to 25% in advanced controller architectures, making it essential for semiconductor firms, OEMs, and energy system integrators seeking long-term scalability and technological leadership.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,190.0 Million |

| Market Revenue (2033) | USD 1,840.2 Million |

| CAGR (2026–2033) | 5.6% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Texas Instruments; Infineon Technologies; STMicroelectronics; ON Semiconductor; Analog Devices; Renesas Electronics; Microchip Technology; NXP Semiconductors; ROHM Semiconductor; Power Integrations; Monolithic Power Systems; Diodes Incorporated; Toshiba Electronic Devices & Storage Corporation |

| Customization & Pricing | Available on Request (10% Customization Free) |