Reports

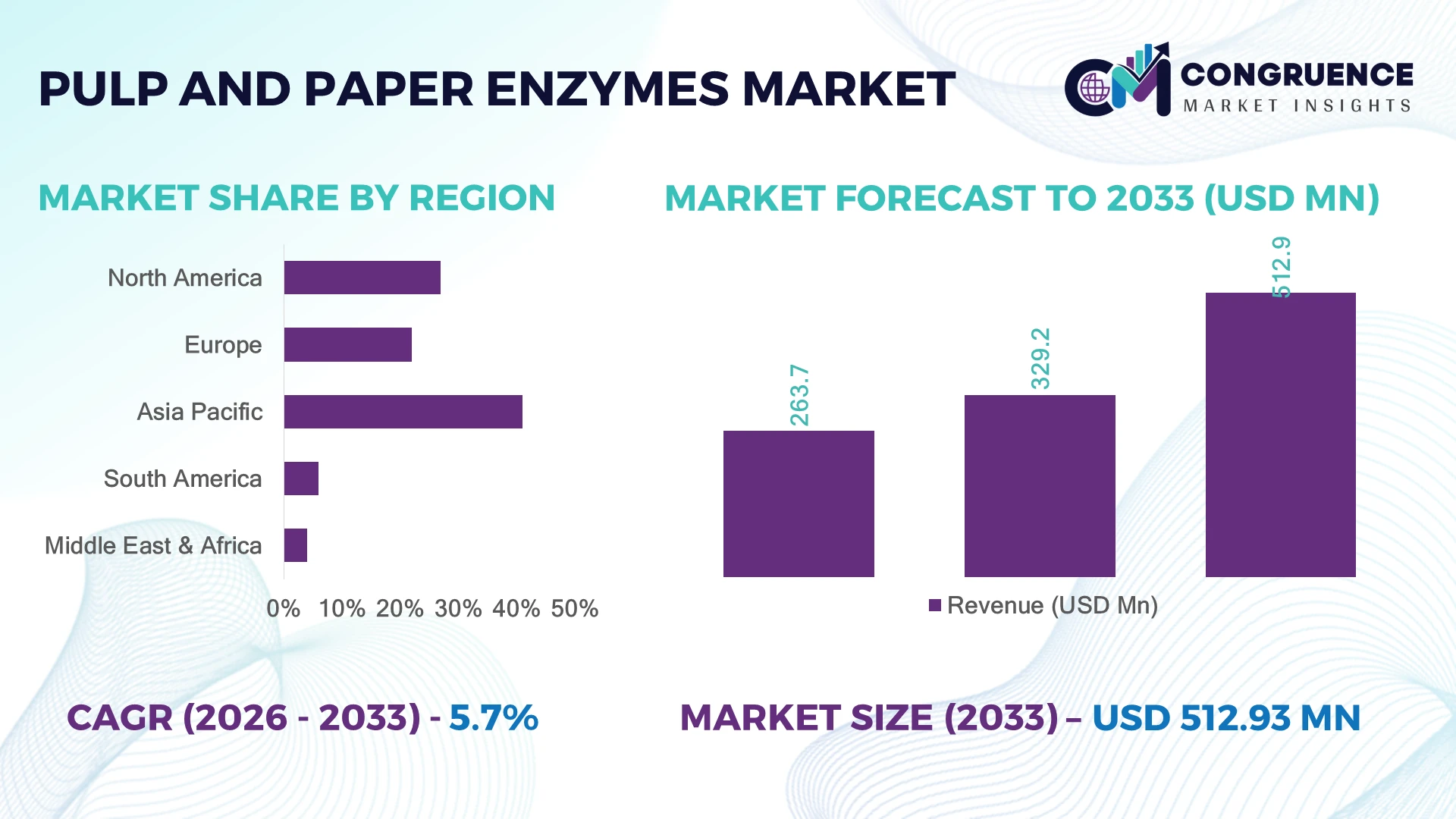

The Global Pulp and Paper Enzymes Market was valued at USD 329.2 Million in 2025 and is anticipated to reach a value of USD 512.9 Million by 2033 expanding at a CAGR of 5.7% between 2026 and 2033. Growth is driven by rising enzyme adoption to reduce bleaching chemicals, improve fiber yield, lower energy consumption, and meet stricter environmental compliance across modern pulp and paper mills.

China dominates the global pulp and paper enzymes market with approximately 34% of global pulp production capacity, supported by large-scale paper manufacturing investments, bio-based processing upgrades, and expanding packaging demand. The country operates more than 2,500 paper and board mills, while Finland leads in advanced enzyme-enabled sustainable pulp processing with significantly higher mill automation and biorefinery integration. Ongoing sustainability targets under global climate commitments continue to accelerate enzyme deployment across industrial operations.

Strategically, suppliers prioritizing high-performance enzyme formulations and regional manufacturing partnerships will secure stronger long-term competitiveness across sustainable pulp processing value chains.

Market Size & Growth: USD 329.2 Million (2025) to USD 512.9 Million (2033) at 5.7% CAGR, supported by advanced enzyme-based chemical reduction and sustainable pulp processing.

Top Growth Drivers: Bleaching chemical use ↓25%, energy consumption ↓18%, wastewater load ↓20% through advanced enzymatic processing.

Short-Term Forecast: By 2028, leading mills are expected to improve fiber processing efficiency by over 15% through integrated enzyme optimization.

Emerging Technologies: AI-driven process control, precision enzyme engineering, and automated dosing systems improve production consistency and resource efficiency.

Regional Leaders: Asia Pacific (~USD 195 Million), Europe (~USD 140 Million), North America (~USD 110 Million), supported by sustainable manufacturing expansion and packaging modernization.

Consumer/End-User Trends: More than 60% of premium paper producers prioritize bio-based processing technologies to reduce chemical dependency and operating costs.

Pilot/Case Example: In 2024, enzyme-assisted kraft pulping projects reported nearly 18% lower bleaching chemical consumption and improved pulp brightness.

Competitive Landscape: Novonesis holds approximately 22% market share alongside AB Enzymes, BASF, DuPont, Buckman, and Kerry Group.

Regulatory & ESG Impact: Sustainable manufacturing initiatives lowered wastewater pollutant loads by nearly 20% while supporting stricter environmental compliance across major regions.

Investment & Funding: Over USD 600 Million has supported bioprocessing expansion, enzyme production capacity, and strategic partnerships amid global supply-chain localization.

Innovation & Future Outlook: Next-generation multifunctional enzymes and digital process optimization are strengthening operational resilience and accelerating sustainable mill transformation.

Increasing adoption of specialty packaging papers, tissue products, and recycled fiber processing continues to strengthen demand for advanced pulp and paper enzymes. Precision enzyme formulations now improve fiber quality while reducing chemical intensity by nearly 20%. Supply-chain localization and tightening industrial discharge regulations are encouraging manufacturers to expand regional production capabilities, creating a stronger foundation for strategic investments and technology partnerships.

The Pulp and Paper Enzymes Market has become strategically important as manufacturers pursue cleaner production, higher fiber utilization, and improved operating efficiency under increasingly stringent environmental regulations. Supply-chain restructuring is encouraging regional enzyme production and closer partnerships between biotechnology companies and paper producers to ensure reliable industrial supply while reducing dependence on imported specialty chemicals. These developments are reshaping competitive positioning across both mature and emerging paper-producing economies.

Modern enzyme-assisted pulping typically reduces bleaching chemical consumption by 20–25% while lowering energy requirements by around 15% compared with conventional chemical-intensive processing. Europe leads in advanced sustainable mill integration and process innovation, whereas Asia Pacific commands larger production volumes through rapid capacity expansion and modernization of packaging paper facilities. Over the next two to three years, digital process monitoring and automated enzyme dosing are expected to be implemented across more large-scale mills, improving production consistency and reducing operational waste.

Large integrated paper manufacturers are expanding pilot-scale enzyme programs into commercial operations through technology partnerships and long-term supply agreements. Investment priorities increasingly focus on customized enzyme solutions for recycled fiber and high-performance packaging grades. Companies that combine biotechnology expertise with digital process optimization and sustainable manufacturing capabilities will establish stronger competitive advantages, improve operational resilience, and reinforce long-term relevance within the evolving global pulp and paper industry.

The transition toward low-chemical and energy-efficient pulp manufacturing is becoming the primary structural driver for enzyme adoption. Enzyme-assisted processing reduces bleaching chemical consumption by 20–25%, lowers refining energy demand by nearly 15%, and improves fiber recovery by approximately 8–10%, delivering measurable operational savings. China continues expanding high-capacity packaging paper facilities while tightening industrial wastewater regulations, prompting mills to replace conventional chemical-intensive stages with advanced enzymatic treatment. This operational shift improves compliance and production efficiency simultaneously. In response, leading biotechnology companies are expanding customized enzyme portfolios, investing in application laboratories, and forming technical partnerships with integrated paper producers to optimize mill-specific formulations. A key strategic advantage lies in combining process optimization services with specialty enzymes, strengthening customer retention beyond conventional product supply.

Production economics remain constrained by fluctuating fermentation feedstock prices, specialized manufacturing requirements, and dependence on temperature-controlled logistics. Enzyme production costs have increased by approximately 12–18% during recent supply-chain disruptions, while transportation expenses for biotechnology products remain nearly 10% above pre-disruption averages in several industrial markets. India and parts of Southeast Asia continue facing uneven enzyme distribution infrastructure, extending delivery lead times and limiting rapid commercial deployment. These structural limitations directly affect procurement planning, operating margins, and adoption among mid-sized paper mills. To reduce exposure, manufacturers are localizing production, establishing long-term raw material agreements, expanding regional warehousing networks, and diversifying microbial production platforms to improve supply continuity while protecting profitability from future logistics volatility.

Advanced enzyme engineering combined with digital process optimization is creating new commercial opportunities beyond conventional bleaching applications. AI-assisted dosing systems improve enzyme utilization by nearly 15%, while next-generation multifunctional enzymes increase recycled fiber processing efficiency by approximately 18% and reduce freshwater consumption by almost 20%. Finland is accelerating industrial biorefinery integration, creating demand for customized enzyme solutions that support circular manufacturing objectives. Companies are increasing R&D investment, collaborating with automation providers, and developing data-driven enzyme management platforms tailored to individual mills. An emerging strategic opportunity lies in subscription-based technical optimization services, allowing suppliers to generate recurring value through continuous process improvement rather than relying solely on enzyme product sales.

Achieving uniform enzyme performance across different pulp grades, wood species, and mill configurations remains a significant execution challenge. Process efficiency can vary by 10–15% depending on feedstock quality, while implementation timelines often extend by 20% when legacy production systems require integration with automated dosing technologies. Canada and other major forestry producers operate mills with diverse equipment generations, making standardized deployment more complex. These variations influence production consistency, sustainability targets, and long-term competitiveness. Companies must strengthen pilot-scale validation, invest in digital process monitoring, expand technical support capabilities, and collaborate with automation specialists to ensure reliable large-scale implementation. Organizations that successfully standardize enzyme integration across diverse operating environments will establish stronger operational resilience and differentiated competitive positioning.

Bold Shift Toward Precision Enzymes: Paper manufacturers are increasingly deploying application-specific enzyme formulations, with customized enzyme adoption rising by nearly 28% across integrated mills. Advanced dosing systems improve enzyme utilization by approximately 15%, reducing process variability and chemical dependency. China’s tightening industrial discharge standards have accelerated this transition, prompting suppliers to expand technical service teams and mill-specific optimization programs that strengthen long-term customer relationships.

Digital Process Control Integration: Automated process monitoring and intelligent dosing platforms are transforming enzyme deployment, improving bleaching consistency by nearly 18% while lowering process interruptions by around 12%. Mills are integrating production analytics into existing control systems to optimize fiber quality in real time. Leading biotechnology firms are partnering with industrial automation providers to deliver integrated digital process packages rather than standalone enzyme products.

Expansion of Recycled Fiber Solutions: Growing recycled fiber utilization has increased demand for specialized deinking and fiber-conditioning enzymes, with recycled pulp processing volumes expanding by more than 20% in several packaging-focused facilities. Rising recovered paper availability and circular economy initiatives are encouraging enzyme suppliers to develop formulations that improve contaminant removal while maintaining fiber strength. Companies are expanding pilot collaborations with packaging manufacturers to validate large-scale deployment.

Localized Production and Technical Support: Supply-chain diversification is encouraging enzyme manufacturers to regionalize production and application support. Local manufacturing initiatives have reduced average delivery lead times by approximately 18%, while regional technical laboratories have increased customer response efficiency by nearly 25%. India and Southeast Asia continue attracting investment in localized enzyme blending facilities, enabling suppliers to improve supply reliability and accelerate commercial implementation across expanding paper manufacturing hubs.

Xylanases remain the dominant enzyme type, accounting for approximately 38% of commercial enzyme utilization across pulp and paper processing due to their proven effectiveness in reducing bleaching chemicals, improving pulp brightness, and integrating seamlessly into existing kraft pulp operations. Their scalability, consistent process performance, and compatibility with continuous production systems make them the preferred solution for large integrated pulp mills. Cellulases continue supporting fiber modification and recycled paper processing, while Lipases and Esterases address pitch control and contaminant management in specialty applications. Collectively, these mature enzyme categories remain essential for optimizing production efficiency and reducing chemical intensity. Mannanases represent the fastest-growing segment as manufacturers increasingly process softwood pulp and mixed recycled fibers requiring targeted hemicellulose degradation. Adoption has expanded by nearly 19%, while pilot deployments have demonstrated fiber yield improvements approaching 8%. Companies are strengthening product portfolios through enzyme engineering, collaborative mill trials, and region-specific formulations to improve substrate compatibility. Investment priorities are steadily shifting toward multifunctional enzyme blends capable of delivering operational flexibility across diverse feedstocks.

Bleaching remains the leading application, representing nearly 35% of enzyme deployment because it delivers measurable reductions in chlorine-based chemical consumption while improving pulp brightness and environmental performance. Enzyme-assisted bleaching typically lowers bleaching chemical requirements by 20–25%, making it a preferred solution for mills pursuing cleaner production and regulatory compliance. Pulp Processing continues supporting production efficiency across high-capacity facilities, while Drainage Improvement enhances machine productivity through improved water removal. Fiber Modification and Other niche applications strengthen product quality for premium paper grades. Deinking is emerging as the fastest-growing application, supported by rising recycled paper utilization and expanding circular manufacturing initiatives. Advanced deinking enzymes improve ink removal efficiency by approximately 18% while preserving fiber integrity and reducing reject volumes. Manufacturers are scaling specialized product lines, integrating automated dosing technologies, and collaborating with recycled paper processors to optimize performance under varying feedstock conditions. Investment increasingly targets recycled fiber optimization as sustainability objectives reshape production priorities across packaging and tissue manufacturing.

Paper Mills remain the largest end-user segment, accounting for approximately 42% of enzyme consumption due to continuous production volumes, extensive bleaching operations, and increasing requirements for cost-efficient manufacturing. Large facilities benefit from automated enzyme dosing, standardized production workflows, and greater economies of scale. Packaging Manufacturers are expanding enzyme adoption alongside growing corrugated board production, while Tissue Manufacturers increasingly utilize enzyme technologies to improve fiber softness and production efficiency. Specialty Paper Producers continue adopting tailored formulations to achieve consistent product quality for high-value grades. Packaging Manufacturers represent the fastest-growing buyer group as recycled fiber utilization expands across global e-commerce supply chains. Adoption has increased by nearly 21%, while enzyme-assisted recycled fiber processing has improved production efficiency by approximately 14%. Suppliers are responding through customized technical support, long-term supply partnerships, and performance-based commercial agreements designed for large converting facilities. Competitive differentiation increasingly depends on delivering application expertise alongside enzyme performance rather than competing primarily on product pricing.

Asia-Pacific accounted for the largest market share at 41% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 6.3% between 2026 and 2033.

North America represented approximately 27% of the global market in 2025, supported by widespread modernization of pulp and paper mills and strong adoption of enzyme-assisted manufacturing technologies. Large integrated producers continue replacing conventional chemical-intensive operations with enzyme-enabled processing to improve fiber recovery and reduce operating costs. Automated dosing systems are now deployed across more than 55% of large-scale pulp facilities, improving production consistency and minimizing process variability. Strategic collaborations between biotechnology developers and paper manufacturers continue accelerating commercial deployment, while investments in mill digitalization strengthen operational efficiency and environmental compliance across the United States and Canada.

United States Market Outlook: The United States leads the regional market through its extensive pulp and paper manufacturing base, advanced biotechnology ecosystem, and continuous investment in sustainable industrial production. More than 65% of regional enzyme deployment is concentrated in U.S. manufacturing facilities, supported by large integrated paper companies implementing intelligent process control and customized enzyme applications. Growing investments in recycled fiber processing and specialty packaging production continue strengthening long-term operational competitiveness.

Europe accounted for approximately 22% of the global market, driven by stringent environmental regulations and continuous modernization of mature pulp manufacturing facilities. Enzyme-assisted bleaching and fiber optimization have become standard operational practices among leading producers seeking lower chemical consumption and improved production efficiency. More than 60% of newly upgraded pulp processing lines incorporate advanced enzymatic treatment technologies as part of broader sustainability initiatives. Companies continue investing in industrial biotechnology partnerships and precision enzyme development to improve mill productivity while supporting circular manufacturing objectives.

Finland Market Outlook: Finland remains the strategic leader within Europe owing to its highly automated forest products industry, advanced biorefinery infrastructure, and strong innovation ecosystem. Integrated pulp producers continue expanding enzyme deployment across high-capacity production lines, with automated process optimization implemented in over 70% of major manufacturing facilities. Close collaboration between biotechnology companies and forest industry operators supports continuous development of next-generation enzyme formulations for sustainable pulp processing.

Asia-Pacific dominated the global market with a 41% share in 2025, supported by extensive paper production capacity, expanding packaging demand, and continuous investment in high-efficiency manufacturing infrastructure. China, India, and Indonesia continue expanding industrial pulp capacity while integrating enzyme technologies to reduce processing chemicals and improve production efficiency. More than 50% of new large-scale paper production projects within the region include advanced enzyme application systems during commissioning. Manufacturers are strengthening regional production capabilities and technical support networks to meet growing commercial demand across packaging, tissue, and recycled paper segments.

China Market Outlook: China remains the largest national market due to its extensive paper manufacturing infrastructure and ongoing industrial modernization. The country operates more than 2,500 paper and board mills while accounting for approximately 34% of global pulp production capacity. Government-led environmental compliance programs continue encouraging enzyme-assisted processing, prompting suppliers to establish localized manufacturing, application laboratories, and strategic partnerships with integrated paper producers.

South America represented approximately 6% of the global market, benefiting from expanding eucalyptus pulp production and increasing adoption of environmentally efficient manufacturing technologies. Brazil and neighboring countries continue investing in export-oriented pulp facilities where enzyme applications improve fiber quality and reduce bleaching chemical requirements. Several integrated pulp producers have expanded process optimization programs, contributing to operational efficiency improvements approaching 15%. While transportation infrastructure and logistics remain execution constraints, biotechnology suppliers are strengthening regional partnerships and technical support capabilities to improve commercial penetration.

Brazil Market Outlook: Brazil dominates the regional market through its globally competitive eucalyptus pulp industry and large export-oriented production base. Continuous investment in modern pulp mills and sustainable forestry operations supports broader enzyme adoption across bleaching and fiber optimization processes. Advanced mill upgrades have enabled greater automation, while long-term technology partnerships continue improving production consistency and environmental performance throughout the country's expanding pulp manufacturing sector.

The Middle East & Africa accounted for approximately 4% of the global market, supported by gradual expansion of tissue manufacturing, packaging production, and industrial diversification initiatives. Regional manufacturers are adopting enzyme-assisted processing to improve operational efficiency while reducing chemical consumption and wastewater treatment requirements. Industrial modernization projects have increased enzyme utilization across selected manufacturing facilities by nearly 12%, particularly in newly commissioned production lines. International biotechnology suppliers continue expanding distributor partnerships and localized technical support to strengthen market access despite relatively limited regional pulp production capacity.

Saudi Arabia Market Outlook: Saudi Arabia leads regional development through ongoing investment in industrial diversification and advanced manufacturing infrastructure. Packaging and tissue producers are increasingly integrating enzyme-based processing technologies within modern production facilities to improve resource efficiency and product quality. Expansion of industrial zones and strategic manufacturing initiatives continues attracting technology partnerships, positioning the country as the primary commercial hub for advanced pulp and paper enzyme solutions in the Middle East.

The competitive landscape is led by Novonesis, AB Enzymes, BASF SE, Buckman Laboratories, and IFF, competing against regional biotechnology suppliers and application-focused enzyme developers. Global leaders differentiate through proprietary enzyme engineering, integrated technical services, and worldwide supply networks, while regional companies compete on pricing, localized support, and customized formulations. The top five players collectively account for approximately 48% of global market share, reflecting a moderately consolidated structure. Competition increasingly centers on enzyme performance, process optimization, and mill-specific customization, with advanced formulations reducing bleaching chemicals by 20–25% and lowering refining energy by nearly 15%. Companies continue strengthening market positions through manufacturing expansion, strategic distribution partnerships, application laboratories, and vertically integrated biotechnology capabilities. Consolidation and digital process optimization are shifting competitive advantage toward innovation-driven suppliers. High R&D investment, stringent industrial qualification requirements, and long customer validation cycles remain key entry barriers. Winning requires superior enzyme performance, technical collaboration, reliable supply resilience, and continuous process innovation.

AB Enzymes GmbH

BASF SE

Buckman Laboratories International, Inc.

IFF (DuPont Industrial Biosciences)

Advanced Enzyme Technologies Ltd.

Amano Enzyme Inc.

Kerry Group plc

DSM-Firmenich

Rossari Biotech Limited

Specialty Enzymes & Probiotics

Enzymatic Deinking Technologies

Enzyme engineering is transforming pulp and paper processing through high-performance xylanases, cellulases, and multifunctional enzyme blends capable of operating under wider pH and temperature conditions. Modern enzyme formulations reduce bleaching chemical consumption by 20–25% while lowering refining energy demand by approximately 15%. Nearly 60% of newly upgraded integrated mills now incorporate advanced enzyme dosing technologies, enabling greater process stability and reduced operating costs. These innovations strengthen fiber quality while supporting stricter environmental compliance across commercial paper manufacturing.

Artificial intelligence, digital twins, and automated dosing platforms are becoming core operational technologies. Compared with conventional manual dosing, AI-assisted optimization improves enzyme utilization by approximately 15% and reduces process variability by nearly 18%. Large biotechnology suppliers benefit most by integrating digital services with enzyme portfolios, allowing customers to optimize production continuously rather than relying solely on periodic process adjustments. This integrated technology model is creating stronger customer retention and expanding long-term technical partnerships.

Between 2026 and 2028, machine learning-assisted enzyme optimization, engineered chimeric enzymes, and precision biocatalyst platforms are expected to reshape commercial deployment. Companies investing in intelligent process automation, customized enzyme formulations, and integrated biotechnology services will secure faster mill adoption, stronger operational differentiation, improved sustainability performance, and greater competitive resilience across global pulp and paper manufacturing.

August 2025 – AB Enzymes received the EcoVadis Platinum Medal, placing the company among the highest-rated sustainability performers globally. The recognition strengthens customer confidence in environmentally responsible enzyme manufacturing and supports long-term partnerships with pulp and paper producers. Source: www.abenzymes.com

September 2024 – Novonesis announced a USD 150 million expansion of global enzyme manufacturing capacity across three continents, including Singapore, improving supply-chain resilience and production support for industrial biosolutions, including pulp and paper applications.

August 2024 – AB Enzymes entered a strategic partnership to strengthen pulp and paper enzyme solutions across Asia, expanding regional technical support and accelerating commercial deployment through localized customer collaboration.

September 2025 – Novonesis introduced advanced enzymatic paper-processing solutions that reduce energy, water, and chemical consumption while enabling stronger recycled-fiber performance, improving mill productivity and supporting lower operating costs across commercial paper manufacturing.

This report provides a comprehensive assessment of the global Pulp and Paper Enzymes Market across enzyme types, applications, end-users, and regional markets between 2026 and 2033. It evaluates Xylanases, Cellulases, Lipases, Esterases, Mannanases, and other specialty enzymes across pulp processing, bleaching, deinking, fiber modification, drainage improvement, and emerging applications. The study covers Paper Mills, Pulp Mills, Tissue Manufacturers, Packaging Manufacturers, Specialty Paper Producers, and other industrial users while examining market dynamics across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

The analysis includes competitive benchmarking of 12+ leading companies, regional market-share distribution, technology adoption trends, deployment patterns, and operational developments shaping industry competitiveness. It further evaluates digital enzyme optimization, AI-assisted process control, enzyme engineering, sustainability initiatives, and circular manufacturing practices. Strategic insights support investment planning, product development, expansion priorities, partnership evaluation, competitive positioning, and long-term decision-making across the evolving global pulp and paper enzyme value chain.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 329.2 Million |

| Market Revenue (2033) | USD 512.9 Million |

| CAGR (2026–2033) | 5.7% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Novonesis; AB Enzymes GmbH; BASF SE; Buckman Laboratories International, Inc.; IFF (DuPont Industrial Biosciences); Advanced Enzyme Technologies Ltd.; Amano Enzyme Inc.; Kerry Group plc; DSM-Firmenich; Rossari Biotech Limited; Specialty Enzymes & Probiotics; Enzymatic Deinking Technologies |

| Customization & Pricing | Available on Request (10% Customization Free) |