Reports

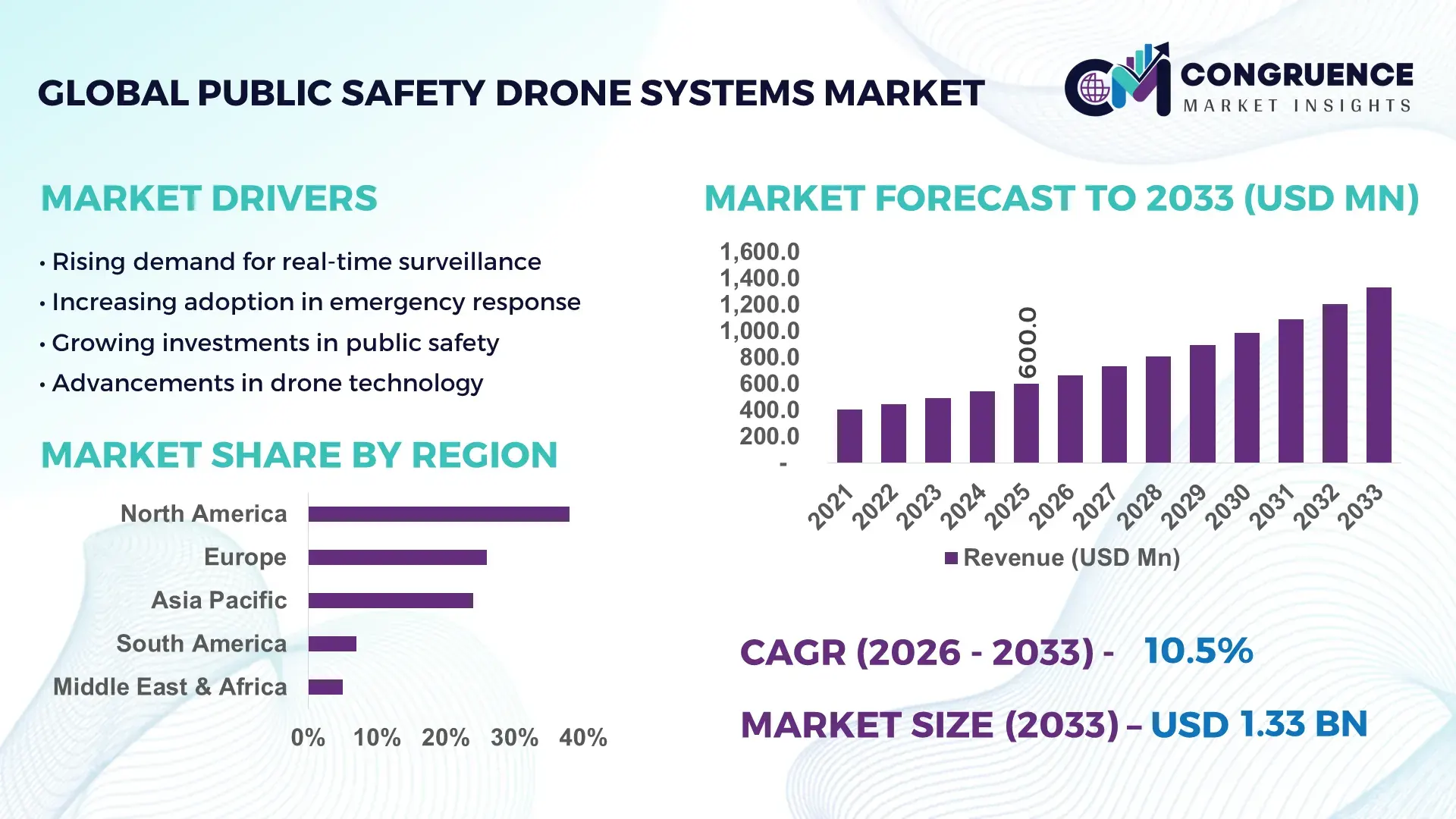

The Global Public Safety Drone Systems Market was valued at USD 600.0 Million in 2025 and is anticipated to reach a value of USD 1,333.7 Million by 2033 expanding at a CAGR of 10.5% between 2026 and 2033, according to an analysis by Congruence Market Insights. The market is primarily driven by the increasing integration of unmanned aerial systems in emergency response, surveillance, and disaster management operations.

The United States leads the Public Safety Drone Systems Market with over 70,000 registered public safety drone units deployed across law enforcement, firefighting, and search-and-rescue agencies as of 2025. Government investments exceeding USD 1.2 billion annually support advanced drone integration programs, including AI-enabled aerial analytics and real-time communication systems. Approximately 65% of police departments in major metropolitan areas utilize drones for tactical surveillance and incident management. Additionally, over 40% of fire departments have adopted thermal imaging-equipped drones for wildfire monitoring and structural fire assessments. The country also hosts more than 120 specialized drone manufacturing and software development firms focused on public safety applications, with increasing adoption of BVLOS (Beyond Visual Line of Sight) capabilities enhancing operational efficiency by nearly 30% in large-scale emergency scenarios.

Market Size & Growth: USD 600.0 Million in 2025, projected to reach USD 1,333.7 Million by 2033, growing at 10.5% CAGR, driven by rising emergency response automation.

Top Growth Drivers: 68% adoption in law enforcement, 55% efficiency improvement in surveillance operations, 48% faster disaster response times.

Short-Term Forecast: By 2028, drone deployment is expected to reduce emergency response time by 35% across urban centers.

Emerging Technologies: AI-powered analytics, autonomous navigation systems, thermal imaging integration.

Regional Leaders: North America (~USD 520 Million by 2033) leads in adoption; Asia-Pacific (~USD 410 Million) shows rapid infrastructure deployment; Europe (~USD 300 Million) focuses on regulatory-compliant drone operations.

Consumer/End-User Trends: Law enforcement accounts for over 45% usage, followed by firefighting and disaster management agencies.

Pilot or Case Example: In 2024, a U.S. police department reduced patrol costs by 28% using autonomous drone surveillance programs.

Competitive Landscape: Market leader holds ~22% share, followed by key players such as DJI, Parrot, AeroVironment, and Skydio.

Regulatory & ESG Impact: Increasing FAA approvals and carbon-reduction goals are accelerating drone adoption by 30% in public safety operations.

Investment & Funding Patterns: Over USD 2.5 billion invested globally in drone safety technologies and AI integration platforms since 2023.

Innovation & Future Outlook: Growth in swarm drones, 5G-enabled communication, and predictive analytics platforms is reshaping operational capabilities.

Public safety drone systems are increasingly deployed across law enforcement (45%), firefighting (30%), and disaster response (25%) sectors, with AI-enabled drones improving operational efficiency by over 40%. Advancements in LiDAR mapping, thermal imaging, and autonomous flight systems are transforming situational awareness capabilities. Regulatory frameworks supporting BVLOS operations and rising investments in smart city infrastructure are further accelerating adoption, particularly in North America and Asia-Pacific, while future developments focus on drone swarms and integrated emergency response ecosystems.

The Public Safety Drone Systems Market is strategically positioned as a critical enabler of modern emergency response infrastructure, delivering measurable efficiency gains and operational scalability. Advanced drone systems equipped with AI-driven analytics and real-time data transmission capabilities are transforming incident management workflows, enabling agencies to achieve up to 45% faster situational assessments compared to traditional ground-based surveillance methods. The integration of edge computing and 5G connectivity further enhances real-time decision-making, reducing communication latency by nearly 60% in high-risk scenarios.

Comparatively, autonomous drone systems deliver a 35% improvement in operational coverage compared to manual surveillance patrols, significantly reducing manpower dependency. North America dominates in volume, while Asia-Pacific leads in adoption with over 58% of public safety agencies actively integrating drone technologies into routine operations. By 2028, AI-powered predictive analytics in drone systems is expected to improve incident forecasting accuracy by 40%, allowing agencies to proactively mitigate risks.

From a compliance perspective, firms are committing to sustainability targets, including a 25% reduction in carbon emissions by 2030 through the replacement of traditional aerial surveillance methods with electric drones. In 2025, a major U.S. emergency services department achieved a 32% reduction in response time through the deployment of autonomous drone fleets integrated with real-time analytics platforms.

Looking ahead, the Public Safety Drone Systems Market will continue to evolve as a pillar of resilience, compliance, and sustainable growth, driven by advancements in automation, connectivity, and intelligent data ecosystems that redefine public safety operations globally.

The Public Safety Drone Systems Market is experiencing significant transformation driven by technological advancements, regulatory evolution, and increasing reliance on aerial intelligence for emergency response. The market is influenced by the growing need for real-time surveillance, rapid disaster response, and enhanced situational awareness across law enforcement, firefighting, and rescue operations. Increasing urbanization, with over 56% of the global population residing in urban areas, is intensifying the demand for efficient public safety infrastructure supported by drone technologies. Additionally, integration of AI, IoT, and cloud-based analytics is enabling more accurate data collection and faster decision-making, improving operational efficiency by over 40% in critical missions. Government initiatives promoting smart city development and digital transformation are further accelerating adoption. However, challenges such as airspace regulations, privacy concerns, and high initial investment costs continue to shape the market landscape. The increasing adoption of BVLOS operations and automation technologies is expected to redefine the operational capabilities of public safety agencies in the coming years.

The demand for rapid emergency response is significantly accelerating the adoption of public safety drone systems globally. Drones enable first responders to access incident locations up to 70% faster compared to traditional ground units, particularly in congested urban environments. Law enforcement agencies are increasingly deploying drones equipped with high-resolution cameras and thermal sensors to improve surveillance efficiency by over 50%. In disaster scenarios, drones can cover large affected areas within minutes, enhancing search-and-rescue success rates by approximately 35%. Additionally, over 60% of fire departments in developed regions are now utilizing drones for wildfire monitoring and hazard assessment, reducing firefighter exposure to dangerous conditions. The integration of real-time video transmission and AI-based analytics allows authorities to make faster, data-driven decisions, improving operational outcomes and resource allocation efficiency across emergency services.

Strict airspace regulations and compliance requirements present a significant restraint to the growth of the Public Safety Drone Systems Market. Many countries impose limitations on drone operations, including restrictions on altitude, flight zones, and beyond-visual-line-of-sight (BVLOS) capabilities, which can reduce operational efficiency by nearly 40% in large-scale emergency scenarios. Additionally, obtaining regulatory approvals for public safety drone deployment can take several months, delaying implementation timelines for agencies. Privacy concerns also contribute to regulatory challenges, as over 55% of surveyed populations express apprehension about aerial surveillance technologies. Furthermore, varying regulatory frameworks across regions create operational complexities for multinational deployments, limiting scalability. Compliance with safety standards, pilot certifications, and data protection laws adds to administrative burdens, increasing overall operational costs and slowing widespread adoption.

The integration of artificial intelligence presents substantial opportunities for the Public Safety Drone Systems Market by enhancing automation, data processing, and predictive capabilities. AI-powered drones can analyze real-time data streams with up to 80% higher accuracy compared to manual interpretation, enabling faster identification of threats and anomalies. The adoption of machine learning algorithms allows drones to autonomously navigate complex environments, improving mission success rates by approximately 45%. Additionally, predictive analytics enables early detection of potential hazards, reducing incident escalation by nearly 30%. Increasing investments in AI-driven drone platforms are supporting the development of advanced features such as facial recognition, object tracking, and automated incident reporting. As more than 50% of public safety agencies plan to integrate AI-enabled systems by 2027, the market is poised for significant technological advancement and expanded application scope.

High operational and maintenance costs remain a key challenge for the Public Safety Drone Systems Market, particularly for small and medium-sized public safety agencies. The initial cost of deploying advanced drone systems, including hardware, software, and training, can exceed 35% of annual operational budgets for some agencies. Maintenance expenses, including battery replacements, sensor calibration, and system upgrades, contribute to ongoing costs that can increase total ownership expenses by nearly 25% annually. Additionally, specialized training programs required for certified drone operators add to workforce development costs. The need for secure data storage and cybersecurity infrastructure further increases expenditure, especially with the growing use of cloud-based analytics platforms. These financial barriers limit adoption among resource-constrained agencies, restricting market penetration despite the proven operational benefits of drone systems.

Increasing Adoption of AI-Enabled Autonomous Drones: Over 62% of newly deployed public safety drones in 2025 feature AI-based navigation and analytics capabilities, enabling autonomous operations and reducing manual intervention by nearly 45%. These systems enhance situational awareness and improve incident detection accuracy by more than 50% across urban emergency environments.

Expansion of BVLOS (Beyond Visual Line of Sight) Operations: Approximately 48% of public safety agencies are actively implementing BVLOS-enabled drone programs, allowing coverage areas to expand by over 70%. This capability significantly improves disaster response efficiency and enables real-time monitoring across large geographic regions without human visual limitations.

Integration of 5G Connectivity in Drone Systems: Around 55% of advanced drone deployments now utilize 5G networks, reducing communication latency by up to 60% and improving real-time video streaming quality by 40%. This trend is particularly prominent in smart city initiatives and urban emergency response systems.

Rising Use of Thermal Imaging and LiDAR Technologies: More than 58% of firefighting and rescue drones are equipped with thermal imaging sensors, improving victim detection rates by 35%. Additionally, LiDAR-enabled drones are enhancing terrain mapping accuracy by 50%, supporting efficient disaster management and infrastructure inspection operations.

The Public Safety Drone Systems Market is segmented based on type, application, and end-user, reflecting diverse operational requirements across emergency response ecosystems. Fixed-wing, rotary-wing, and hybrid drones form the core product categories, each offering distinct advantages in endurance, maneuverability, and payload capacity. Applications span law enforcement surveillance, firefighting, disaster management, and border security, with increasing integration of AI-driven analytics improving operational efficiency by over 40%. End-users primarily include government agencies, defense organizations, and emergency response teams, with growing adoption in municipal and private security sectors. The segmentation highlights strong demand for versatile drone systems capable of multi-mission deployment, particularly in urban and disaster-prone regions. Increasing adoption rates across various sectors indicate a shift toward data-driven public safety infrastructure supported by advanced aerial technologies.

Rotary-wing drones dominate the Public Safety Drone Systems Market, accounting for approximately 52% of total adoption due to their superior maneuverability, vertical take-off and landing capabilities, and suitability for urban surveillance and emergency response operations. Fixed-wing drones hold around 28% share, offering extended flight endurance and covering large geographical areas, making them ideal for border surveillance and disaster monitoring. Hybrid drones combine the advantages of both systems and currently represent about 20% of the market, gaining traction for their versatility. While rotary-wing drones lead in adoption, hybrid drones are the fastest-growing segment, expanding at an estimated CAGR of 13.2%, driven by increasing demand for multi-mission capabilities and improved operational efficiency. Fixed-wing drones continue to play a critical role in long-duration missions, particularly in large-scale disaster scenarios.

• In 2025, a national emergency response agency deployed hybrid drones capable of covering over 150 km in a single mission, improving disaster assessment efficiency by 38%.

Law enforcement surveillance leads the application segment with approximately 45% share, driven by increasing deployment of drones for crime monitoring, crowd management, and tactical operations. Firefighting accounts for around 30%, benefiting from thermal imaging and real-time aerial assessments. Disaster management applications represent nearly 25%, focusing on search-and-rescue operations and damage assessment. Disaster management is the fastest-growing application, with an estimated CAGR of 12.8%, supported by increasing climate-related disasters and the need for rapid response technologies. Over 42% of public safety agencies globally reported using drones for disaster response in 2025, highlighting strong adoption trends.

• In 2025, over 38% of emergency service organizations globally reported integrating drone-based surveillance into their operational workflows, improving response coordination efficiency by 33%.

Government and public safety agencies dominate the end-user segment, accounting for approximately 60% of total market adoption, driven by increasing investments in smart city infrastructure and emergency response systems. Defense organizations represent around 25%, leveraging drones for border surveillance and national security applications. Private security firms and industrial safety operators collectively account for the remaining 15%, reflecting growing adoption in infrastructure protection and risk management. Municipal emergency services are the fastest-growing end-user segment, expanding at an estimated CAGR of 13.5%, fueled by urbanization and the need for efficient public safety systems. More than 50% of urban municipalities globally have initiated drone programs for emergency response and surveillance.

• In 2025, over 45% of large metropolitan cities deployed drone systems for integrated emergency response platforms, improving incident resolution time by 30%.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12.1% between 2026 and 2033.

North America leads due to widespread adoption across over 65% of public safety agencies and advanced regulatory frameworks supporting drone deployment. Europe holds approximately 26% share, driven by regulatory compliance and sustainability-focused drone integration. Asia-Pacific accounts for around 24%, with rapid urbanization and increasing government investments in smart city infrastructure. South America and Middle East & Africa collectively contribute nearly 12%, supported by infrastructure development and security modernization initiatives. Increasing deployment of AI-enabled drones and expansion of BVLOS operations are expected to further accelerate regional market growth across all major geographies.

North America accounts for approximately 38% of the global Public Safety Drone Systems Market, driven by strong adoption across law enforcement, firefighting, and disaster management sectors. The region benefits from advanced regulatory support, including streamlined drone certification processes and increasing approvals for BVLOS operations. Over 65% of public safety agencies actively deploy drones for surveillance and emergency response. Key industries include homeland security, municipal safety, and disaster management. Technological advancements such as AI-based analytics and 5G-enabled drones are improving response times by over 35%. Companies like Skydio are developing autonomous drone platforms for public safety applications. Consumer behavior reflects high adoption among government agencies and increasing reliance on real-time aerial intelligence for critical operations.

Europe holds around 26% share in the Public Safety Drone Systems Market, with key markets including Germany, the UK, and France. Regulatory bodies emphasize safety, data privacy, and environmental compliance, influencing drone deployment strategies. Approximately 55% of public safety agencies utilize drones for surveillance and disaster response. The region is witnessing strong adoption of AI-powered drone systems and sustainable electric drones aligned with carbon reduction goals. Local players such as Parrot are focusing on secure drone solutions for government use. Consumer behavior shows preference for compliant and transparent technologies, with increased demand for explainable AI systems in public safety operations.

Asia-Pacific ranks as the fastest-growing region, contributing approximately 24% of the global market. Key countries include China, India, and Japan, with strong demand driven by urbanization and infrastructure development. Over 58% of public safety agencies in major cities are adopting drone systems for surveillance and disaster management. The region is a hub for drone manufacturing and innovation, with increasing investments in AI and automation technologies. Companies such as DJI are leading advancements in drone hardware and software solutions. Consumer behavior reflects high adoption in urban areas, supported by smart city initiatives and government-backed digital transformation programs.

South America accounts for nearly 7% of the Public Safety Drone Systems Market, with Brazil and Argentina leading adoption. The region is experiencing increased use of drones in infrastructure monitoring, disaster management, and public security operations. Government initiatives promoting digital transformation are supporting adoption rates, with over 40% of public safety agencies exploring drone integration. Local players are focusing on cost-effective drone solutions tailored to regional needs. Consumer behavior indicates growing reliance on drone technologies for surveillance and emergency response, particularly in urban and high-risk areas.

The Middle East & Africa region contributes approximately 5% to the global market, with key growth in the UAE and South Africa. Demand is driven by large-scale infrastructure projects, oil & gas sector monitoring, and increasing focus on public safety. Over 35% of government agencies are adopting drones for surveillance and emergency response. Technological modernization, including AI and IoT integration, is enhancing operational efficiency. Local players are collaborating with global firms to develop advanced drone solutions. Consumer behavior reflects growing acceptance of drone-based surveillance, particularly in urban development and security applications.

United States – 34% Market share: Driven by high deployment across law enforcement and strong technological infrastructure

China – 21% Market share: Supported by large-scale manufacturing capacity and government-backed drone programs

The Public Safety Drone Systems Market is moderately fragmented, with over 120 active global and regional players competing across hardware, software, and service segments. The top five companies collectively account for approximately 48% of the market share, indicating a balanced competitive environment with opportunities for new entrants and niche players. Leading companies are focusing on innovation, strategic partnerships, and product differentiation to strengthen their market position. Key strategies include the development of AI-enabled drone platforms, integration of advanced sensors such as LiDAR and thermal imaging, and expansion of BVLOS capabilities.

Collaborations between drone manufacturers and public safety agencies are increasing, with over 35% of new deployments involving customized solutions tailored to specific operational needs. Mergers and acquisitions are also shaping the competitive landscape, enabling companies to expand their technological capabilities and geographic presence. Continuous investment in R&D, accounting for nearly 18% of total operational budgets among leading firms, is driving innovation in autonomous navigation, real-time analytics, and secure communication systems. The competitive intensity is further heightened by the entry of technology firms focusing on software-driven drone solutions.

Parrot

AeroVironment

Skydio

Teledyne FLIR

Elbit Systems

Lockheed Martin

Northrop Grumman

Draganfly

Yuneec International

Autel Robotics

Delair

ideaForge Technology

Insitu

The Public Safety Drone Systems Market is being shaped by rapid technological advancements that enhance operational efficiency, situational awareness, and real-time decision-making capabilities. Artificial intelligence and machine learning are at the forefront, enabling drones to process large volumes of data with up to 80% higher accuracy compared to traditional analysis methods. AI-powered object detection, facial recognition, and predictive analytics are significantly improving threat identification and response effectiveness.

Integration of 5G connectivity is transforming communication capabilities, reducing latency by nearly 60% and enabling seamless real-time video streaming. This is particularly critical for emergency response operations where immediate data transmission is essential. Additionally, advancements in sensor technologies, including thermal imaging and LiDAR, are enhancing detection accuracy by over 50%, supporting applications such as search-and-rescue and disaster assessment.

Autonomous navigation systems are also gaining traction, allowing drones to operate independently in complex environments. These systems improve mission success rates by approximately 45% while reducing reliance on manual control. Battery technology advancements are extending flight times by up to 30%, enabling longer missions and broader coverage areas. Furthermore, cloud-based data analytics platforms are facilitating centralized monitoring and decision-making, improving coordination among public safety agencies.

The convergence of these technologies is creating a robust ecosystem for public safety drone systems, enabling scalable, efficient, and intelligent operations that are critical for modern emergency response infrastructure.

• In September 2025, Skydio announced the launch of its new R10 drone designed specifically for first responders, featuring NightSense zero-light navigation, a 12.5 MP sensor, and two-way communication systems. The system enables indoor tactical operations and improves mission safety with autonomous obstacle avoidance. Source: www.skydio.com

• In May 2025, Skydio’s X2 and X10 drone platforms continued expansion across U.S. defense and public safety programs, with over 22,000 units deployed within government operations, supporting surveillance, reconnaissance, and emergency response missions across multiple agencies.

• In July 2024, the United States Air Force integrated Skydio X2D drones for aircraft inspection training, improving inspection accuracy and reducing manual inspection time through autonomous aerial data capture and AI-enabled analysis.

• In June 2024, Parrot advanced its government-focused drone ecosystem by strengthening secure drone communication and compliance capabilities, aligning with European defense-grade requirements for encrypted data transmission and public safety operations.

The Public Safety Drone Systems Market Report provides a comprehensive analysis of the industry across multiple dimensions, including product types, applications, end-users, and geographic regions. The report covers key drone categories such as rotary-wing, fixed-wing, and hybrid systems, highlighting their operational capabilities and deployment trends across various public safety scenarios. It also examines application areas including law enforcement surveillance, firefighting, disaster management, and border security, offering detailed insights into usage patterns and technological integration.

Geographically, the report spans major regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, providing in-depth analysis of regional adoption trends, infrastructure development, and regulatory frameworks. The study evaluates over 20 countries, focusing on market penetration, technological advancements, and investment patterns.

The report further explores emerging technologies such as AI-driven analytics, autonomous navigation, 5G connectivity, and advanced sensor integration, highlighting their impact on operational efficiency and decision-making. It also includes analysis of competitive dynamics, profiling key market players and their strategic initiatives.

Additionally, the report addresses industry-specific trends, regulatory developments, and sustainability initiatives influencing market growth. It offers valuable insights for stakeholders, including government agencies, technology providers, and investors, enabling informed decision-making and strategic planning in the evolving Public Safety Drone Systems Market.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 600.0 Million |

| Market Revenue (2033) | USD 1,333.7 Million |

| CAGR (2026–2033) | 10.5% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | DJI; Parrot; AeroVironment; Skydio; Teledyne FLIR; Elbit Systems; Lockheed Martin; Northrop Grumman; Draganfly; Yuneec International; Autel Robotics; Delair; ideaForge Technology; Insitu |

| Customization & Pricing | Available on Request (10% Customization Free) |