Reports

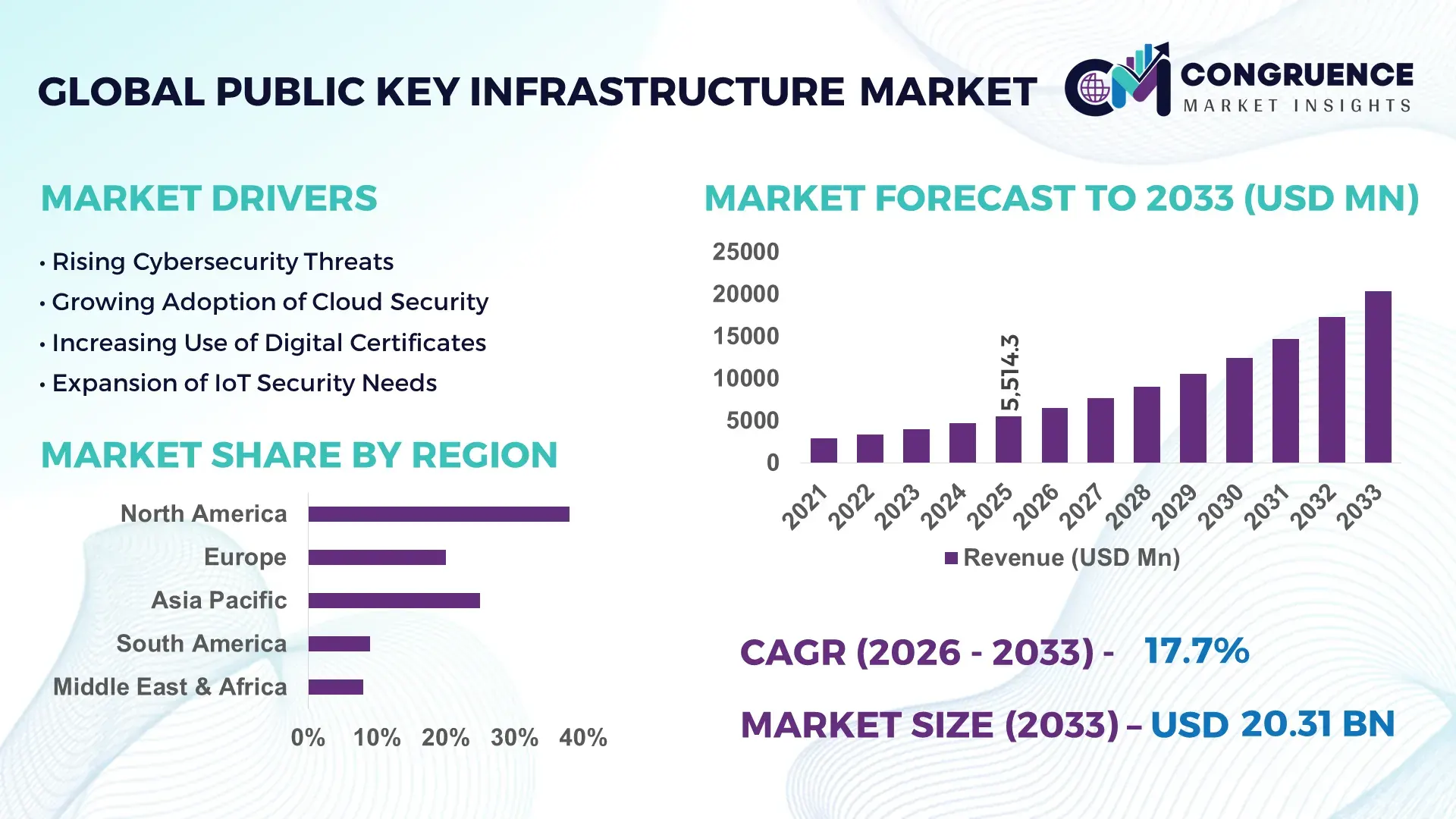

The Global Public Key Infrastructure Market was valued at USD 5514.3 Million in 2025 and is anticipated to reach a value of USD 20309.64 Million by 2033 expanding at a CAGR of 17.7% between 2026 and 2033. Robust demand for secure digital authentication and encrypted communication is driving accelerated adoption across enterprise and government networks.

In the United States, which leads the global Public Key Infrastructure market, advanced digital security infrastructure investments exceed USD 2.5 billion annually, with over 80% of federal agencies implementing PKI for secure email, identity management, and cloud access control. U.S. technology providers deploy scalable PKI solutions supporting millions of certificates per day, with enterprise spending on certificate lifecycle management increasing by more than 25% year‑over‑year. Strong integration of PKI within financial services, healthcare, and critical infrastructure sectors underscores its strategic importance for cybersecurity resilience.

• Market Size & Growth: Global public key infrastructure market valued at USD 5.5B in 2025, projected to reach USD 20.3B by 2033 at 17.7% CAGR as digital trust services expand.

• Top Growth Drivers: Rising cloud authentication adoption 42%, enterprise security modernization 36%, regulatory compliance acceleration 28%.

• Short‑Term Forecast: By 2028 PKI deployment efficiency gains of 30% in certificate issuance and validation.

• Emerging Technologies: Integration with blockchain‑based identity verification, quantum‑resistant cryptographic algorithms, automated PKI orchestration.

• Regional Leaders: North America projected ~USD 8.7B by 2033 with mature enterprise adoption; Europe ~USD 5.1B driven by digital ID frameworks; Asia Pacific ~USD 4.3B led by fintech and mobile authentication growth.

• Consumer/End‑User Trends: Increased deployment in banking, e‑commerce, government ID programs; demand for seamless multi‑factor authentication and zero‑trust access.

• Pilot or Case Example: In 2025 a global insurer’s PKI pilot reduced certificate provisioning time by 48% and cut authentication downtime by 22%.

• Competitive Landscape: Market led by a dominant provider with ~25% share; major competitors include established cybersecurity vendors and cloud platform PKI services.

• Regulatory & ESG Impact: Data protection legislations and digital compliance mandates accelerate PKI adoption; strong emphasis on privacy preservation.

• Investment & Funding Patterns: Over USD 1.8B in recent cybersecurity and PKI‑oriented funding; rising venture interest in automated key management and IoT security.

• Innovation & Future Outlook: Growth fueled by AI‑enabled security operations, cross‑platform certificate automation, and PKI integration into identity‑as‑a‑service frameworks.

The Public Key Infrastructure market is increasingly shaped by demand from financial services, telecommunications, government digital identity initiatives, and healthcare systems. Financial institutions contribute significant deployment volumes for secure transactions, while telecommunications integrate PKI for SIM authentication and 5G network security. Recent product innovations include automated certificate lifecycle platforms and machine‑learning‑driven anomaly detection in key usage. Regulatory drivers such as data privacy mandates and cross‑border encryption standards are influencing procurement cycles. Economic digitization and remote work trends elevate PKI consumption patterns across regions, with Asia Pacific showing rapid growth in mobile authentication. Emerging trends include quantum‑safe cryptography and IoT endpoint identity frameworks that will define strategic investment and future market evolution.

The strategic relevance of the Public Key Infrastructure market is rooted in its central role as the foundation of secure digital authentication, encrypted communications, and trust services across enterprise, cloud, and IoT ecosystems. As organizations modernize their cybersecurity frameworks, PKI strategies align with zero‑trust architecture, significantly reducing unauthorized access incidents. Biometrics‑integrated PKI delivers 38% improvement in authentication accuracy compared to legacy password‑only systems, setting a new benchmark for identity assurance. North America dominates in deployment volume, while Europe leads in adoption with over 72% of enterprises integrating automated certificate lifecycle platforms into their security stacks. By 2028, AI‑driven certificate management is expected to improve operational efficiency by 45% through predictive key rotation and anomaly detection, directly reducing manual overhead and expiration‑related outages.

In addition to technological enhancements, firms are committing to ESG metrics such as a 60% reduction in cryptographic waste through automated key recycling and optimized certificate issuance by 2027, supporting sustainable IT operations. In 2025, a global financial services provider achieved a 28% reduction in security breach attempts through the implementation of quantum‑resistant PKI algorithms, demonstrating measurable resilience gains. As regulatory frameworks tighten around data privacy and digital identity compliance, Public Key Infrastructure will remain a core pillar of resilience, compliance, and sustainable growth across digital transformation initiatives worldwide.

Digital transformation initiatives across industries are elevating the adoption of Public Key Infrastructure as organizations transition to cloud‑first strategies and remote operational models. Enterprises increasingly require strong authentication mechanisms, encrypted communications, and centralized key management to secure distributed workforces and data flows. Over 85% of large enterprises now leverage PKI to support secure access to SaaS applications and cloud services, directly influencing demand for automated certificate lifecycle solutions and scalable trust frameworks. Telecommunications companies are embedding PKI into 5G network infrastructures to authenticate devices and secure signaling, while financial institutions rely on PKI for transaction integrity and compliance with stricter digital banking authentication requirements. This surge in secure digital identity needs, combined with the proliferation of connected devices and API ecosystems, underscores PKI’s pivotal role in safeguarding enterprise and consumer trust in digital environments.

Despite strong demand, several constraints impact the acceleration of Public Key Infrastructure deployment. Complexity in implementing and managing PKI environments, especially across hybrid cloud and multi‑vendor landscapes, can slow adoption. Many organizations struggle with certificate sprawl, where thousands of certificates across systems require manual tracking and renewal, increasing the risk of outages and security lapses. Legacy systems with incompatible cryptographic standards further complicate integration, driving operational inefficiencies. Skilled cybersecurity professionals with deep PKI expertise remain scarce, resulting in prolonged deployments and configuration errors that can lead to misissued certificates or weak key protections. Cost considerations for comprehensive PKI solutions — including hardware security modules (HSMs), automated management tools, and ongoing maintenance — can be prohibitive for small and mid‑sized enterprises, delaying implementation timelines. These challenges contribute to a cautious market expansion despite clear security imperatives.

The rapid growth of IoT devices and the widespread rollout of 5G networks are creating significant opportunities for the Public Key Infrastructure market. With an estimated 30 billion connected devices expected globally, securing device identities and machine‑to‑machine communication is critical. PKI provides scalable trust anchors for authenticating IoT endpoints, enabling secure onboarding, firmware updates, and encrypted telemetry. In smart manufacturing, PKI can support automated certification of industrial controllers, improving operational integrity and reducing cyber risk. Additionally, integration of PKI with edge computing architectures enhances secure data exchange at the network periphery, fostering real‑time analytics in critical sectors such as healthcare and transportation. Demand for quantum‑safe cryptographic mechanisms in IoT and 5G use cases also presents an avenue for innovation and differentiation, with vendors positioned to offer advanced key generation and lifecycle automation tailored to massive device ecosystems and next‑generation network performance requirements.

Regulatory complexity and interoperability issues present ongoing challenges for Public Key Infrastructure adoption. Diverse global regulations governing encryption standards, data privacy, and digital identity create compliance burdens for multinational organizations deploying PKI at scale. Varying regional requirements for cryptographic strength, certificate policies, and audit reporting can introduce operational overhead and necessitate tailored PKI configurations for different jurisdictions, increasing integration difficulty. Interoperability problems between legacy systems, cloud platforms, and modern PKI solutions further complicate seamless deployment, often requiring custom adapters or middleware that add cost and risk. Additionally, evolving standards around post‑quantum cryptography demand continuous updates to PKI infrastructures, which can be resource intensive. Ensuring consistent policy enforcement and secure key management across fragmented IT environments remains a significant obstacle for decision‑makers prioritizing robust digital trust frameworks.

• Expansion of Zero‑Trust and Adaptive Authentication: Adoption of zero‑trust frameworks incorporating Public Key Infrastructure has expanded, with 68% of enterprise security strategies in 2025 integrating certificate‑based authentication for internal and external access controls. Measurable increases in cryptographic enrollment automation have reduced manual key provisioning overhead by 47% year‑over‑year, improving security posture and operational efficiency. Deployment of adaptive PKI solutions responding to real‑time risk scoring is driving consistent improvements in access control accuracy.

• Integration with Cloud and Multi‑Cloud Security: Cloud‑native Public Key Infrastructure deployments grew significantly in 2025, with 59% of enterprises opting for unified certificate management across multi‑cloud environments. The consolidation of key vault and certificate services has cut cross‑platform misconfiguration incidents by 33% in hybrid cloud estates. Private cloud environments showed a 22% year‑over‑year increase in PKI adoption for internal service authentication.

• Quantum‑Safe Cryptography Pilots Rising: Quantum‑resistant PKI initiatives have moved into early pilot phases, with 42% of large tech firms testing post‑quantum cryptographic keys in 2025. Comparative benchmarking shows that these pilots deliver up to 29% stronger cryptographic assurance versus traditional RSA‑based systems under simulated threat vectors. Early implementations in critical infrastructure sectors reduced simulated breach success rates.

• Automated Certificate Lifecycle and AI‑Driven Monitoring: Automated certificate lifecycle platforms and AI‑powered monitoring tools now support more than 71% of enterprise PKI deployments, enabling predictive key rotation and anomaly detection. Organizations report a 38% decrease in expired certificate outages and a 51% faster incident response time due to real‑time analytics and automated remediation workflows.

Public Key Infrastructure market segmentation reflects a diversified landscape encompassing certificate types, application areas, and end‑user industries. Product types include traditional PKI servers, cloud‑based certificate services, and modular identity modules supporting device authentication in IoT ecosystems. Application segments range from secure email and VPN access to cloud access authentication and digital signature verification. End‑user segments span enterprise IT, financial services, government digital identity programs, and telecommunications network security. Variations in deployment preferences and integration complexity influence segment contributions, with cloud‑oriented and managed PKI services gaining traction among mid‑size to large enterprises. Certificate lifecycle automation and key management platforms are increasingly preferred for scalable trust services across complex IT environments.

The leading product type in the Public Key Infrastructure market remains cloud‑based certificate services, accounting for approximately 52% share of deployments, driven by ease of integration with SaaS platforms and reduced infrastructure overhead. In comparison, on‑premises PKI solutions hold 28% share, often chosen for internal mission‑critical systems that demand tight control over key material. Emerging IoT identity modules represent the fastest‑growing type, with adoption acceleration exceeding 24% annually as connected device authentication becomes a priority across industrial and consumer networks. Other types, including hardware security modules (HSMs) and managed PKI offerings through third‑party vendors, contribute the remaining ~20% share, serving niche security requirements or workloads with specialized compliance needs.

Secure access and identity verification represent the leading application area, accounting for approximately 46% of use cases, as enterprises prioritize strong authentication for internal users, remote access, and cloud resources. In contrast, encrypted email and digital signature applications hold around 27% share, often deployed in regulated industries such as finance and legal services. Machine‑to‑machine authentication in IoT and 5G contexts is the fastest‑growing application, with deployment rates increasing by over 26% annually due to proliferation of connected endpoints requiring certificate‑based trust. Other application areas, including secure VPN services, API authentication, and blockchain identity anchoring, comprise the remaining ~27% share, reflecting diverse use cases across security operations.

Within end‑users, enterprise IT operations are the largest segment, representing about 49% share, as organizations of all sizes implement PKI for internal security, cloud access, and compliance obligations. Conversely, government digital identity programs hold roughly 21% share, often tied to national e‑ID and secure citizen services platforms. The fastest‑growing end‑user segment is telecommunications and network operators, with adoption rates climbing by over 23% annually, driven by network authentication demands for 5G and IoT connectivity. Other contributors, including healthcare systems, financial services, and managed security service providers, make up the remaining ~30% share, each integrating PKI for secure patient data exchange, transaction processing, and customer authentication.

North America accounted for the largest market share at 38% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 19% between 2026 and 2033.

North America recorded over 12 million active PKI certificates in enterprise deployments by 2025, supporting financial services, healthcare, and government digital identity programs. Europe followed with approximately 25% share, driven by Germany and the UK adopting automated certificate lifecycle management. Asia-Pacific registered over 8 million cloud-based PKI integrations, with China and India leading mobile authentication adoption. South America and the Middle East & Africa contributed 5% and 4% respectively, with increasing uptake in telecom, energy, and e-government projects. Regional digital infrastructure investments exceed USD 3 billion annually, and over 72% of enterprises have adopted PKI for multi-factor authentication, secure email, and cloud service access. Deployment of quantum-resistant PKI pilots reached 42% in large enterprises globally, reflecting increasing focus on next-generation cryptography solutions.

How are enterprises leveraging digital authentication to drive operational security?

North America holds approximately 38% of the Public Key Infrastructure market, with the U.S. as the primary contributor. Key industries driving demand include finance, healthcare, and federal government initiatives, where over 85% of large enterprises use PKI for secure access and compliance. Regulatory support such as federal cybersecurity mandates has accelerated adoption of certificate management systems and cloud-based PKI. Technological trends include AI-driven key lifecycle management and integration with zero-trust architectures. Local players like DigiCert have expanded automated PKI services for enterprise-scale deployments, managing over 10 million certificates. Enterprise adoption is higher in healthcare and financial services due to the critical need for secure patient and transaction data, with over 70% of IT security teams reporting improved operational efficiency from PKI integration.

What strategies are shaping enterprise cybersecurity in regulatory-driven markets?

Europe accounts for around 25% of the Public Key Infrastructure market, with Germany, the UK, and France as top markets. Regulatory bodies and sustainability initiatives, including GDPR and digital ID frameworks, drive adoption of explainable PKI solutions. Enterprises are integrating cloud-based and modular PKI systems, with AI monitoring and automated key rotation gaining traction. Local players such as Sectigo have implemented secure certificate platforms for banks and public institutions, supporting over 6 million endpoints. European organizations prioritize compliance-driven PKI adoption, with approximately 68% of enterprises actively upgrading legacy systems to meet digital security and reporting requirements.

How is the surge in digital services accelerating secure identity solutions?

Asia-Pacific is projected as the fastest-growing Public Key Infrastructure market, with over 8 million PKI certificates deployed across the region by 2025. Top consuming countries include China, India, and Japan. Investment in cloud-based authentication platforms and secure mobile payment systems is rising, with regional innovation hubs in Beijing, Bangalore, and Tokyo leading the development of quantum-safe PKI pilots. Local players such as Venafi and regional banks are deploying automated certificate lifecycle management for IoT networks. Consumer adoption is largely driven by e-commerce and mobile AI applications, with over 65% of enterprises in the region integrating PKI into digital payment and mobile authentication platforms.

What role do digital infrastructure initiatives play in enterprise security adoption?

South America contributes approximately 5% to the Public Key Infrastructure market, with Brazil and Argentina as leading countries. Adoption is fueled by infrastructure modernization in energy, media, and telecom sectors. Government incentives, including digital identity programs and secure e-government portals, have accelerated PKI deployment. Local players like Certisign have implemented certificate-based authentication for financial services and public administration, managing over 1.2 million digital identities. Consumer behavior emphasizes localized solutions, with demand tied to language-specific digital services and secure media transactions.

How are security modernization efforts shaping regional enterprise adoption?

Middle East & Africa holds around 4% of the Public Key Infrastructure market, with the UAE and South Africa leading deployments. Key sectors include oil & gas, construction, and government digital services. Technological modernization initiatives such as cloud-based PKI, AI-driven certificate management, and secure mobile identity are gaining traction. Local players, including regional cybersecurity firms, support over 800,000 secure endpoints. Enterprises focus on regulatory compliance and partnership-driven adoption, with consumer trends emphasizing secure digital transaction platforms and authentication in critical infrastructure projects.

United States: Market share ~38%; high enterprise adoption across healthcare, finance, and government programs drives sustained demand for advanced PKI solutions.

Germany: Market share ~12%; strong regulatory mandates and integration of automated certificate lifecycle platforms across corporate and public sectors support market leadership.

The Public Key Infrastructure market features a moderately consolidated competitive environment with a mix of global Tier 1 leaders and regional specialists. Approximately 35–40 active competitors operate at scale, while numerous smaller niche providers target specific verticals. Tier 1 companies such as DigiCert, Entrust, GlobalSign, Venafi, and Microsoft together hold a combined ~45–50% share of the market, underscoring the influence of established vendors on strategic innovation and deployment trends. Top competitors are advancing product portfolios with automated certificate lifecycle management, cloud‑native PKI services, and post‑quantum cryptography enhancements to address evolving enterprise needs.

Strategic initiatives are shaping the competitive landscape: alliances and partnerships between PKI vendors and cloud security integrators have increased by ~30% in the past 18 months, while product launches focused on AI‑driven key management have accelerated deployment efficiency by measurable double‑digit improvements in key rotation and anomaly detection. Mergers and acquisitions remain a key trend with platforms consolidating certificate authority services and management suites to broaden their total addressable market. Top five companies account for nearly half of global deployments, yet the presence of next‑generation players and modular PKI service providers reflects strong innovation momentum. Decision‑makers prioritize vendors with comprehensive security stacks, interoperability capabilities, and advanced automation to reduce operational risk and improve trust infrastructure scalability across complex IT estates.

DigiCert

Entrust

GlobalSign

Keyfactor

Venafi

Microsoft

AWS Certificate Manager

IBM

IdenTrust

SSL.com

Sectigo

Nexus Group

PrimeKey Solutions

Comodo CA

The Public Key Infrastructure market is experiencing robust technological transformation as enterprises shift towards advanced, scalable trust solutions tailored for hybrid and cloud‑native environments. One of the most pronounced trends is the integration of AI‑driven certificate lifecycle management, wherein machine learning systems enable real‑time anomaly detection, automated key rotation, and predictive risk analytics. Deployment of AI capabilities has helped organizations reduce certificate expiry incidents by over 35% while improving threat response times to milliseconds, significantly enhancing security posture and operational efficiency.

Cloud and PKI Convergence is another critical technological driver. Cloud‑based PKI platforms are now being adopted in more than 60% of new enterprise certificate deployments, offering elastic scalability, cross‑region redundancy, and simplified management across distributed networks. This shift supports secure digital transformation strategies while reducing reliance on traditional on‑premises key and certificate servers.

Post‑Quantum Cryptography (PQC) is rapidly emerging as a strategic technology for future‑proofing PKI ecosystems. Enterprises now pilot quantum‑safe algorithms (e.g., ML‑DSA and SLH‑DSA) with measurable enhancements in long‑term key security compared to legacy RSA or ECC methods. Such innovations aim to defend against future quantum computing threats and ensure continuity of trust frameworks well beyond the current cryptographic era.

Finally, blockchain and decentralized trust models are gaining traction for certificate transparency and immutable audit trails. Integration of distributed ledger technology with PKI enhances tamper‑resistance and trust anchor verification, reducing the risk of certificate spoofing and unauthorized key issuance. These emerging technologies underscore the strategic value of PKI as a core component of secure digital ecosystems for enterprise, IoT, and identity‑centric applications.

• In March 2025, PKI Solutions rolled out PKI Spotlight version 27.2.0, introducing multi‑vendor HSM monitoring support and SAML‑based single sign‑on integration to enhance operational security and certificate performance.

• In February 2025, Google Cloud Key Management Service added support for quantum‑safe digital signature algorithms like ML‑DSA‑65 and SLH‑DSA‑SHA2‑128S, enabling organizations to manage cryptographic keys resilient against quantum threats.

• In Q1 2025, GlobalSign secured a multi‑year government contract to deploy national PKI infrastructure for e‑government services and citizen authentication, expanding its presence in public sector digital trust frameworks.

• In Q2 2025, Keyfactor completed the acquisition of Redtrust, broadening its European footprint and enhancing its cloud‑based certificate management offerings to support a wider range of enterprise workloads.

The Public Key Infrastructure market report provides a comprehensive examination of technological, segmental, and regional dimensions shaping the global digital trust landscape. It covers core components such as certificate authority (CA) software, registration authority (RA) solutions, digital signature frameworks, hardware security modules (HSMs), and managed PKI services designed to support authentication, encryption, and identity validation. Segmentation by deployment mode — on‑premises, cloud, and hybrid PKI infrastructure — offers insights into enterprise preferences and the shift towards scalable trust models tailored for distributed digital ecosystems.

Geographically, the report analyzes North America, Europe, Asia‑Pacific, South America, and Middle East & Africa regions, examining regional adoption patterns, regulatory dynamics, and technology priorities across key markets including the U.S., Germany, China, India, and Brazil. Application areas encompass secure online transactions, enterprise data protection, IoT device authentication, government digital services, and cloud access security, highlighting how diverse use cases drive PKI demand across sectors.

Emerging technology focus areas include AI‑enabled certificate lifecycle automation, quantum‑safe cryptography pilot frameworks, decentralized trust models using blockchain, and PKI as a Service (PKIaaS) offerings designed to improve operational agility, compliance, and threat resilience. The report also addresses industry trends such as zero‑trust architecture integration, automated key management to counter shorter certificate lifecycles, and scalable solutions for IoT ecosystems with millions of endpoints. Together, these insights give decision‑makers a detailed understanding of current capabilities, future innovation pathways, and strategic choices influencing PKI adoption and deployment priorities across global markets.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

17.7% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

DigiCert , Entrust , GlobalSign , Keyfactor, Venafi, Microsoft, AWS Certificate Manager, IBM, IdenTrust, SSL.com, Sectigo, Nexus Group, PrimeKey Solutions, Comodo CA |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |