Reports

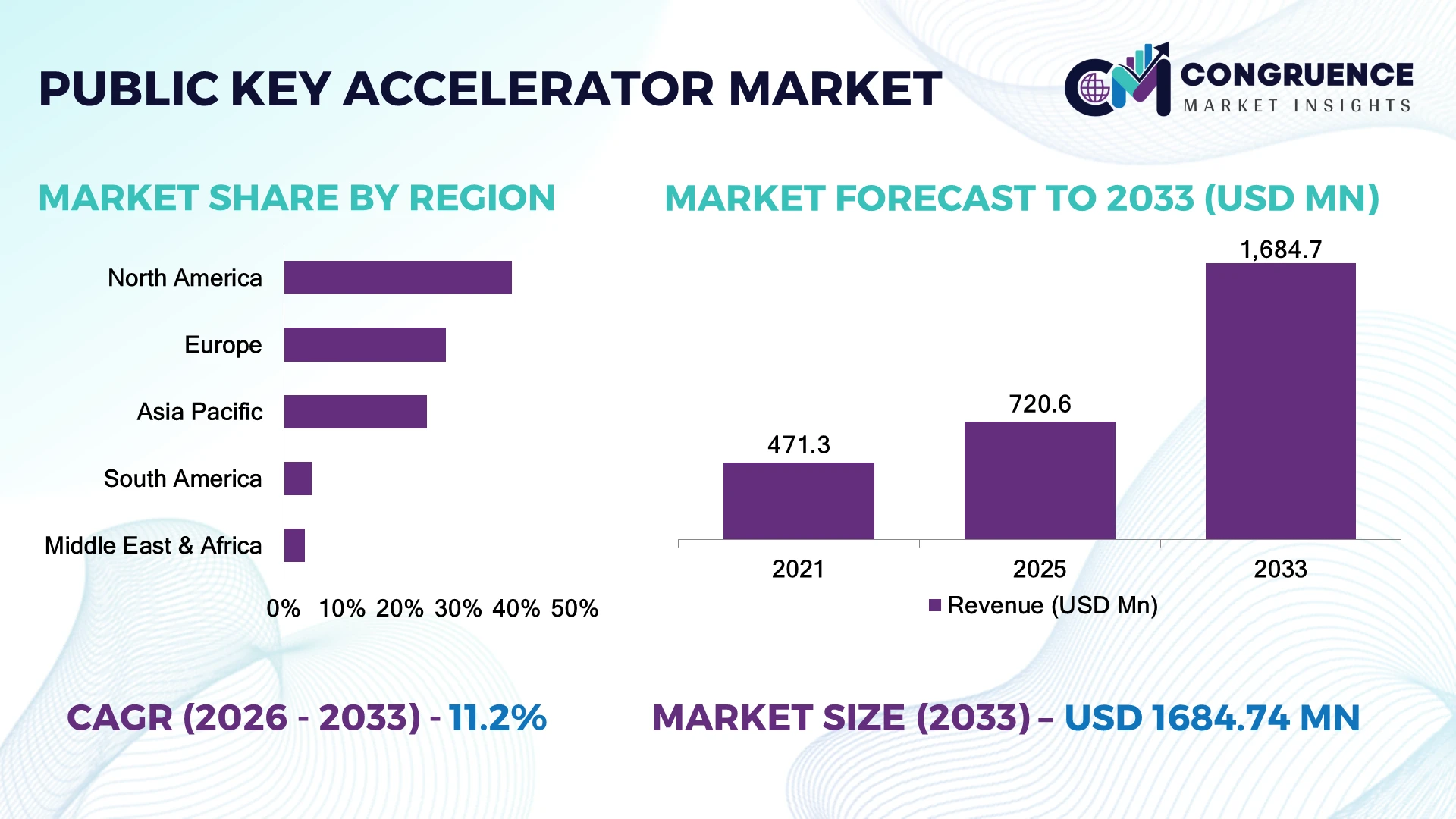

The Global Public Key Accelerator Market was valued at USD 720.6 Million in 2025 and is anticipated to reach a value of USD 1,684.7 Million by 2033 expanding at a CAGR of 11.2% between 2026 and 2033. Growing deployment of hardware-based cryptographic acceleration, post-quantum security preparation, and high-speed TLS encryption across cloud, financial, telecom, and government infrastructure is driving sustained market expansion.

The United States leads the market with approximately 38% of global deployment, supported by semiconductor innovation, hyperscale cloud infrastructure, and extensive cybersecurity investment. More than 73% of enterprise data centers deploy hardware cryptographic acceleration for secure transactions, compared with Japan's stronger emphasis on embedded security for industrial electronics. Rising geopolitical focus on cyber resilience and critical infrastructure protection continues accelerating secure hardware procurement and domestic semiconductor investment.

Organizations investing in high-performance cryptographic hardware and quantum-ready security architectures are strengthening long-term operational resilience and competitive advantage.

Market Size & Growth: USD 720.6 Million in 2025 reaches USD 1,684.7 Million by 2033 at a CAGR of 11.2%, driven by hardware cryptographic acceleration and secure cloud infrastructure.

Top Growth Drivers: Zero-trust adoption (+31%), cloud security (+29%), and post-quantum readiness (+24%) accelerate deployment.

Short-Term Forecast: By 2028, encryption latency declines nearly 34%, while cryptographic processing efficiency improves approximately 29%.

Emerging Technologies: Post-quantum cryptography, AI-assisted security, and hardware root-of-trust redefine secure computing.

Regional Leaders: North America exceeds USD 620 Million, Asia-Pacific approaches USD 470 Million, and Europe surpasses USD 360 Million through cybersecurity modernization.

Consumer/End-User Trends: More than 67% of enterprise security upgrades include hardware cryptographic acceleration.

Pilot/Case Example: In 2026, dedicated accelerator deployment improved TLS processing throughput by approximately 42% in enterprise data centers.

Competitive Landscape: Leading suppliers control nearly 47% of the market, led by Marvell, Microchip Technology, Rambus, Intel, and AMD.

Regulatory & ESG Impact: Hardware acceleration lowers encryption-related server power consumption by nearly 18%.

Investment & Funding: More than USD 1.6 Billion supports semiconductor expansion, cybersecurity hardware, and secure processor development.

Innovation & Future Outlook: Quantum-resistant accelerators and integrated security processors are reshaping enterprise infrastructure.

Public Key Accelerator solutions are experiencing expanding adoption across cloud computing, financial services, telecommunications, defense, and industrial automation as organizations strengthen cryptographic performance without sacrificing latency. Nearly 59% of enterprise security refresh projects now include hardware-based encryption acceleration, while evolving cybersecurity regulations and semiconductor supply-chain diversification continue influencing procurement strategies, creating the foundation for the broader strategic discussion.

The Public Key Accelerator Market has become strategically important because cryptographic performance is increasingly central to digital infrastructure, cloud services, financial transactions, and critical communications. Organizations are modernizing security architectures to support zero-trust frameworks, high-volume encrypted workloads, and quantum-resilient computing. At the same time, government cybersecurity mandates and semiconductor supply-chain restructuring are accelerating investment in dedicated cryptographic hardware rather than software-only encryption.

Modern hardware-based public key accelerators process asymmetric cryptographic operations approximately 45% faster than conventional software implementations while reducing CPU utilization by nearly 32%, allowing servers to dedicate more computing resources to application workloads. North America continues leading deployment through hyperscale cloud investment and advanced semiconductor capabilities, whereas Asia-Pacific is rapidly expanding manufacturing capacity and embedded security integration. Over the next two to three years, enterprise adoption of hardware cryptographic acceleration is expected to exceed 60% across security-sensitive digital infrastructure.

A cloud service provider deploying dedicated public key accelerators within secure data centers can significantly improve encrypted transaction throughput while lowering operational latency for large-scale customer environments. Technology vendors are expanding investments in post-quantum cryptography, secure silicon design, and semiconductor partnerships to strengthen product portfolios. Organizations combining hardware acceleration, quantum-ready algorithms, and integrated security architectures will achieve stronger competitive positioning, operational efficiency, and long-term cyber resilience.

Enterprise migration toward zero-trust cybersecurity architectures is accelerating deployment of dedicated public key accelerators across cloud infrastructure, financial networks, and mission-critical data centers. More than 69% of enterprise security modernization projects now incorporate hardware-based cryptographic acceleration, while dedicated accelerators improve asymmetric encryption throughput by approximately 43% and reduce processor utilization by nearly 31%. The United States continues expanding cybersecurity investment under critical infrastructure protection initiatives, increasing demand for high-performance cryptographic hardware. This structural shift enables secure, low-latency digital transactions at scale. Technology vendors are responding through quantum-ready accelerator development, semiconductor partnerships, advanced PCIe accelerator cards, and integrated security processor innovation, positioning cryptographic acceleration as a strategic computing capability rather than a standalone security component.

Public key accelerator manufacturing remains dependent on advanced semiconductor fabrication, exposing vendors to component shortages, long production cycles, and rising fabrication costs. Specialized cryptographic processors currently experience lead-time extensions of approximately 20%, while advanced packaging and testing increase hardware manufacturing costs by nearly 17%. Taiwan's concentration of leading-edge semiconductor production continues creating supply-chain sensitivity for enterprise security hardware manufacturers. These structural limitations delay large-scale deployment, increase procurement uncertainty, and compress hardware margins. Companies are reducing exposure through multi-foundry sourcing strategies, regional semiconductor partnerships, long-term wafer agreements, and modular hardware architectures that improve manufacturing flexibility while strengthening supply continuity.

The transition toward post-quantum cryptography is creating substantial opportunities for next-generation public key accelerator platforms. Nearly 56% of enterprise cybersecurity leaders are evaluating quantum-resistant encryption strategies, while hardware acceleration improves execution efficiency for post-quantum algorithms by approximately 27% compared with general-purpose processors. Japan continues expanding investment in quantum-safe cybersecurity research alongside secure semiconductor innovation. Technology providers are increasing R&D expenditure, collaborating with cryptography standards organizations, and developing programmable accelerator architectures capable of supporting evolving cryptographic algorithms. A significant strategic opportunity lies in offering field-upgradable hardware that enables seamless migration to future quantum-resistant security standards without replacing existing infrastructure.

Integrating dedicated public key accelerators into heterogeneous enterprise environments remains a significant execution challenge due to diverse security frameworks, legacy infrastructure, and evolving cryptographic standards. Approximately 48% of enterprise organizations continue operating mixed hardware and software encryption environments, while integration complexity increases deployment timelines by nearly 22%. Germany's industrial cybersecurity modernization initiatives require interoperability across operational technology and enterprise IT systems, increasing implementation complexity. These operational challenges directly affect deployment consistency, lifecycle management, and long-term infrastructure scalability. Vendors must strengthen standardized APIs, firmware lifecycle management, interoperability testing, and ecosystem partnerships while investing in developer tools and platform certification programs to support sustainable enterprise adoption.

Post-Quantum Hardware Readiness Hardware vendors are accelerating development of quantum-resistant cryptographic accelerators as more than 54% of enterprise security roadmaps include post-quantum planning. Optimized accelerator architectures improve cryptographic execution efficiency by approximately 26% while reducing migration complexity. Companies are expanding semiconductor collaborations and firmware-upgradable platforms to prepare customers for evolving encryption standards.

Integrated Security Processors Expand Dedicated cryptographic engines are increasingly integrated into server processors, networking equipment, and data center hardware, reducing encryption latency by nearly 33% while improving secure transaction throughput by approximately 29%. Demand for consolidated hardware security is encouraging semiconductor manufacturers to strengthen platform integration and strategic partnerships with enterprise infrastructure providers.

Cloud Encryption Offloading Grows Hyperscale cloud operators continue deploying hardware-based cryptographic acceleration to improve encrypted workload performance, with secure transaction capacity increasing by approximately 38% and processor overhead declining by nearly 30%. Growing cloud security requirements are prompting accelerator vendors to optimize PCIe cards, SmartNIC integration, and hardware security modules for large-scale cloud environments.

Programmable Accelerator Architectures Programmable cryptographic accelerators are gaining traction as enterprises seek flexible support for evolving encryption algorithms and compliance requirements. Configurable accelerator deployment has increased by approximately 23%, while firmware-based optimization reduces hardware refresh requirements by nearly 18%. Technology providers are investing in software-defined cryptography, ecosystem partnerships, and standardized development frameworks to improve long-term platform adaptability and enterprise infrastructure resilience.

Hardware Accelerators accounted for approximately 49% of the Public Key Accelerator Market in 2025, driven by their superior cryptographic throughput, low latency, and ability to offload computationally intensive asymmetric encryption from host processors. Their deployment across hyperscale data centers, financial networks, and telecom infrastructure makes them the preferred solution for high-volume secure transactions. Hardware Security Modules (HSMs) continue holding a strong position for regulated industries requiring certified key protection, while Crypto Co-processors remain essential for embedded systems and industrial security. Software-based acceleration solutions retain relevance for cost-sensitive deployments but are increasingly complemented by dedicated hardware. Vendors continue investing in PCIe accelerator cards, integrated security processors, and quantum-ready cryptographic engines to strengthen enterprise performance.

FPGA-Based Public Key Accelerators represent the fastest-growing segment as enterprises seek programmable cryptographic platforms capable of adapting to evolving encryption standards and post-quantum algorithms. Nearly 57% of advanced cybersecurity infrastructure projects now evaluate reconfigurable hardware architectures, while programmable acceleration improves cryptographic flexibility by approximately 24%. Companies are expanding FPGA partnerships, customizable accelerator portfolios, and firmware-driven feature upgrades, reflecting a strategic shift toward adaptable security hardware capable of extending infrastructure lifecycles.

According to 2025 enterprise security deployment findings published by the National Institute of Standards and Technology (NIST), organizations continue prioritizing hardware-assisted cryptographic acceleration to strengthen security performance and prepare for future cryptographic transitions.

Data Center Security accounted for approximately 36% of the Public Key Accelerator Market in 2025, supported by rising encrypted workloads, hyperscale computing, and increasing adoption of zero-trust architectures. Dedicated public key accelerators enable high-speed TLS processing, secure authentication, and efficient certificate management while reducing processor overhead. Financial Services continue representing a mature application because of intensive cryptographic transaction processing, whereas Government & Defense maintain sustained deployment through national cybersecurity initiatives. Telecommunications and Healthcare increasingly integrate hardware acceleration to strengthen network security, identity management, and protected data exchange across distributed digital environments.

Cloud Infrastructure represents the fastest-growing application as enterprise migration toward hybrid and multi-cloud platforms accelerates demand for hardware-based encryption offloading. Approximately 63% of newly deployed cloud security environments incorporate dedicated cryptographic acceleration, improving encrypted transaction throughput by nearly 35%. Vendors are responding through integrated cloud security platforms, SmartNIC-enabled acceleration, and partnerships with hyperscale infrastructure providers, positioning hardware cryptography as a core operational capability for scalable digital infrastructure.

A 2026 enterprise cybersecurity assessment released by the Cloud Security Alliance highlighted continued expansion of hardware-assisted encryption within cloud environments as organizations strengthen zero-trust implementation and secure workload protection.

Large Enterprises accounted for approximately 52% of total market demand in 2025 due to extensive deployment across financial institutions, telecommunications operators, hyperscale data centers, and multinational corporations managing high-volume encrypted communications. Their large-scale infrastructure, stringent compliance requirements, and advanced cybersecurity strategies sustain demand for dedicated cryptographic hardware. Government Agencies continue expanding secure communications infrastructure, while Banking & Financial Institutions maintain consistent investment in transaction security. Telecom Operators strengthen adoption through secure 5G infrastructure, and Healthcare Organizations increasingly deploy accelerator-based encryption to protect sensitive patient information and connected healthcare systems.

Cloud Service Providers represent the fastest-growing end-user segment as encrypted workloads, confidential computing, and secure digital services continue expanding globally. Nearly 61% of newly commissioned hyperscale cloud facilities integrate hardware cryptographic acceleration to improve processing efficiency and reduce server utilization. Companies are targeting this segment through customized accelerator platforms, semiconductor partnerships, cloud-native security integration, and scalable deployment models that strengthen competitive differentiation across enterprise cloud infrastructure.

According to the 2025 Cloud Security Alliance enterprise infrastructure study, hardware-assisted cryptographic acceleration continues gaining priority among cloud providers seeking higher encrypted workload performance and stronger operational security.

North America accounted for the largest market share at 39.2% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12.4% between 2026 and 2033.

Advanced cybersecurity infrastructure strengthens hardware cryptography leadership

North America accounted for approximately 39.2% of the global Public Key Accelerator Market in 2025, supported by hyperscale cloud infrastructure, advanced semiconductor capabilities, and large-scale cybersecurity modernization. Enterprise adoption continues expanding across financial institutions, defense organizations, telecommunications providers, and cloud service operators requiring high-speed cryptographic processing. More than 72% of hyperscale data centers deploy hardware-assisted encryption acceleration, while secure processor integration continues increasing across enterprise infrastructure. Semiconductor companies are strengthening strategic collaborations with cloud providers and security vendors to accelerate deployment of quantum-ready cryptographic hardware, reinforcing the region's leadership in secure computing infrastructure.

United States Market Outlook: The United States leads the regional market through advanced semiconductor design, extensive cloud infrastructure, and strong federal cybersecurity initiatives. Enterprise investments continue targeting secure silicon, hardware security modules, and dedicated cryptographic accelerators for zero-trust implementation. Approximately 75% of Fortune 500 organizations continue upgrading hardware-assisted encryption capabilities, strengthening domestic demand for high-performance cryptographic processing technologies and accelerating commercial deployment across critical digital infrastructure.

Digital sovereignty accelerates secure hardware deployment

Europe accounted for approximately 27.8% of the global market in 2025, driven by strict cybersecurity regulations, expanding sovereign cloud initiatives, and increasing investment in trusted semiconductor technologies. Financial institutions, industrial manufacturers, and government organizations continue deploying hardware cryptographic acceleration to strengthen secure communications and regulatory compliance. Nearly 61% of enterprise cybersecurity modernization projects incorporate hardware-based encryption technologies. Technology suppliers continue investing in secure processor development, cryptographic certification, and collaborative semiconductor research to improve deployment consistency across regulated industries.

Germany Market Outlook: Germany remains the regional leader through its advanced industrial cybersecurity ecosystem, automotive electronics expertise, and secure semiconductor innovation. Manufacturers continue integrating cryptographic accelerators into industrial automation, connected mobility, and enterprise infrastructure. More than 58% of large industrial organizations are expanding hardware-based security deployment, reinforcing Germany's position as a strategic center for trusted computing technologies.

Semiconductor manufacturing scale fuels rapid expansion

Asia-Pacific accounted for approximately 24.6% of the global market in 2025 and continues recording the fastest expansion through semiconductor manufacturing leadership, cloud infrastructure investment, and accelerating cybersecurity modernization. Regional technology companies increasingly integrate dedicated cryptographic accelerators into networking equipment, enterprise servers, and embedded platforms. Nearly 65% of new secure computing hardware development projects include dedicated cryptographic processing capabilities. Companies continue expanding advanced packaging capacity, secure chip manufacturing, and research partnerships to strengthen regional competitiveness in next-generation cybersecurity hardware.

China Market Outlook: China leads the regional market through its extensive semiconductor manufacturing ecosystem, rapidly expanding cloud infrastructure, and strategic investment in domestic cybersecurity technologies. Enterprise adoption continues increasing across telecommunications, financial services, and government digital infrastructure. More than 62% of newly deployed enterprise security appliances incorporate hardware cryptographic acceleration, strengthening domestic technology capability while reducing reliance on imported security hardware.

Financial sector modernization drives secure deployment

South America accounted for approximately 4.8% of the global market in 2025, supported by banking digitization, cloud adoption, and modernization of enterprise cybersecurity infrastructure. Financial institutions remain the largest users of dedicated cryptographic acceleration for secure transaction processing and identity verification. Approximately 44% of large enterprise cybersecurity investments now prioritize hardware-assisted encryption capabilities. While semiconductor manufacturing remains limited, regional organizations continue strengthening deployment through technology partnerships, cloud integration, and secure infrastructure modernization initiatives.

Brazil Market Outlook: Brazil dominates the regional market through its advanced banking sector, expanding cloud ecosystem, and increasing cybersecurity investment. Financial institutions continue deploying dedicated cryptographic hardware to strengthen payment security and digital identity management. Large enterprise organizations are expanding hardware-based encryption infrastructure to support secure financial transactions, regulatory compliance, and resilient digital service delivery across national networks.

Critical infrastructure investment expands cyber resilience

The Middle East & Africa accounted for approximately 3.6% of the global market in 2025, supported by national digital transformation initiatives, critical infrastructure modernization, and expanding cybersecurity investment. Government agencies, financial institutions, and telecommunications providers continue deploying hardware cryptographic solutions to strengthen secure communications and digital identity platforms. Approximately 41% of new cybersecurity infrastructure projects include dedicated hardware security technologies. Vendors continue expanding regional partnerships, technical support capabilities, and secure infrastructure deployment to strengthen long-term operational resilience.

Saudi Arabia Market Outlook: Saudi Arabia leads regional adoption through national digital transformation programs, expanding cloud infrastructure, and strategic cybersecurity investment. Government organizations and financial institutions continue integrating hardware-assisted encryption across digital public services and critical infrastructure. More than half of newly deployed national digital platforms incorporate dedicated cryptographic security technologies, encouraging technology providers to establish stronger regional partnerships and localized cybersecurity capabilities.

Public key accelerator vendors including Rambus, Marvell, Microchip Technology, Intel, and AMD compete directly with FPGA providers, security IP developers, and hardware security module specialists for enterprise cryptographic infrastructure. The top five players collectively command approximately 48% of the global market through semiconductor expertise, cryptographic IP portfolios, and long-term OEM partnerships. Competition is driven by encryption throughput, latency, silicon efficiency, and quantum-ready architecture rather than pricing. Advanced accelerator designs improve asymmetric cryptographic performance by nearly 42%, while optimized hardware integration reduces processor utilization by approximately 30% and lowers encryption latency by 28%. Companies are expanding through secure silicon partnerships, embedded security integration, programmable accelerator development, and post-quantum cryptography investment. The competitive shift increasingly favors programmable, quantum-ready accelerator architectures over fixed-function security hardware. High certification requirements, semiconductor design complexity, and ecosystem compatibility remain significant entry barriers. Market leadership depends on scalable cryptographic performance, interoperability, secure semiconductor innovation, and long-term platform compatibility.

Rambus Inc.

Marvell Technology, Inc.

Microchip Technology Inc.

Intel Corporation

Advanced Micro Devices, Inc. (AMD)

NVIDIA Corporation

Lattice Semiconductor Corporation

QuickLogic Corporation

NXP Semiconductors N.V.

Infineon Technologies AG

STMicroelectronics N.V.

Cadence Design Systems, Inc.

Dedicated cryptographic accelerator IP, hardware security modules, and integrated secure processors are redefining enterprise encryption infrastructure. Hardware-assisted public key processing improves asymmetric cryptographic throughput by approximately 43% while reducing CPU utilization by nearly 31%. More than 62% of hyperscale cloud deployments now integrate dedicated cryptographic acceleration to strengthen TLS performance, certificate management, and secure authentication. These technologies deliver lower latency, higher transaction capacity, and improved infrastructure scalability across cloud, financial, and telecommunications environments.

Emerging technologies including post-quantum cryptography, programmable FPGA-based accelerators, and SmartNIC-integrated security engines are replacing fixed-function cryptographic architectures. Compared with conventional software-based encryption, dedicated hardware acceleration delivers nearly 46% higher cryptographic efficiency while reducing response latency by approximately 28%. Semiconductor vendors with programmable architectures gain the strongest competitive advantage because field-upgradable platforms allow organizations to transition toward quantum-resistant algorithms without replacing deployed infrastructure.

Between 2026 and 2028, quantum-safe accelerator engines, chiplet-based security processors, and AI-assisted cryptographic workload optimization will reshape secure computing platforms. Hardware-assisted encryption adoption is expected to exceed 68% among large enterprise infrastructure deployments as zero-trust architectures mature. Organizations investing in programmable cryptographic hardware, standardized security APIs, and post-quantum acceleration capabilities will strengthen operational resilience, reduce infrastructure overhead, and establish long-term differentiation in enterprise cybersecurity.

May 2024 Marvell launched its Alaska® P PCIe Gen 6 retimer portfolio to strengthen connectivity between AI accelerators, CPUs, and infrastructure components, enabling higher-performance secure computing platforms with lower latency for next-generation data centers. Source: marvell.com (marvell.com)

March 2025 Marvell demonstrated its first 2nm silicon platform for accelerated infrastructure, enabling custom processors and accelerator designs with improved efficiency for cloud and security workloads, strengthening future secure hardware ecosystems. Source: marvell.com (marvell.com)

December 2025 Rambus and Microchip validated the Rambus ICE-IP-63 inline cryptographic accelerator on Microchip PolarFire® FPGA platforms, enabling deterministic hardware encryption for RISC-V systems with multi-channel line-rate performance. Source: microchip.com (Microchip)

2026 Rambus expanded its Quantum Safe Crypto Accelerator IP portfolio supporting ML-KEM and ML-DSA implementations with side-channel attack protection, enabling semiconductor developers to integrate quantum-resistant public key acceleration into next-generation ASIC and FPGA designs. Source: Rambus (Rambus)

The report provides comprehensive coverage of the Public Key Accelerator Market across hardware accelerators, hardware security modules, crypto co-processors, FPGA-based accelerators, and software-assisted cryptographic solutions. It evaluates deployment across data center security, cloud infrastructure, financial services, government and defense, telecommunications, healthcare, and industrial security while assessing procurement trends among large enterprises, cloud service providers, government agencies, banking institutions, and telecom operators. Regional assessment spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa.

The study examines hardware cryptographic acceleration, post-quantum cryptography, programmable security architectures, secure semiconductor technologies, SmartNIC integration, and cryptographic IP innovation alongside competitive benchmarking of major technology providers. It analyzes deployment patterns, enterprise adoption, interoperability strategies, and infrastructure modernization to support investment planning, cybersecurity roadmap development, product positioning, partnership evaluation, and long-term competitive strategy across the public key accelerator ecosystem between 2026 and 2033.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 720.6 Million |

|

Market Revenue in 2033 |

USD 1,684.7 Million |

|

CAGR (2026 - 2033) |

11.2% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Rambus Inc., Marvell Technology, Inc., Microchip Technology Inc., Intel Corporation, Advanced Micro Devices, Inc. (AMD), NVIDIA Corporation, Lattice Semiconductor Corporation, QuickLogic Corporation, NXP Semiconductors N.V., Infineon Technologies AG, STMicroelectronics N.V., Cadence Design Systems, Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |