Reports

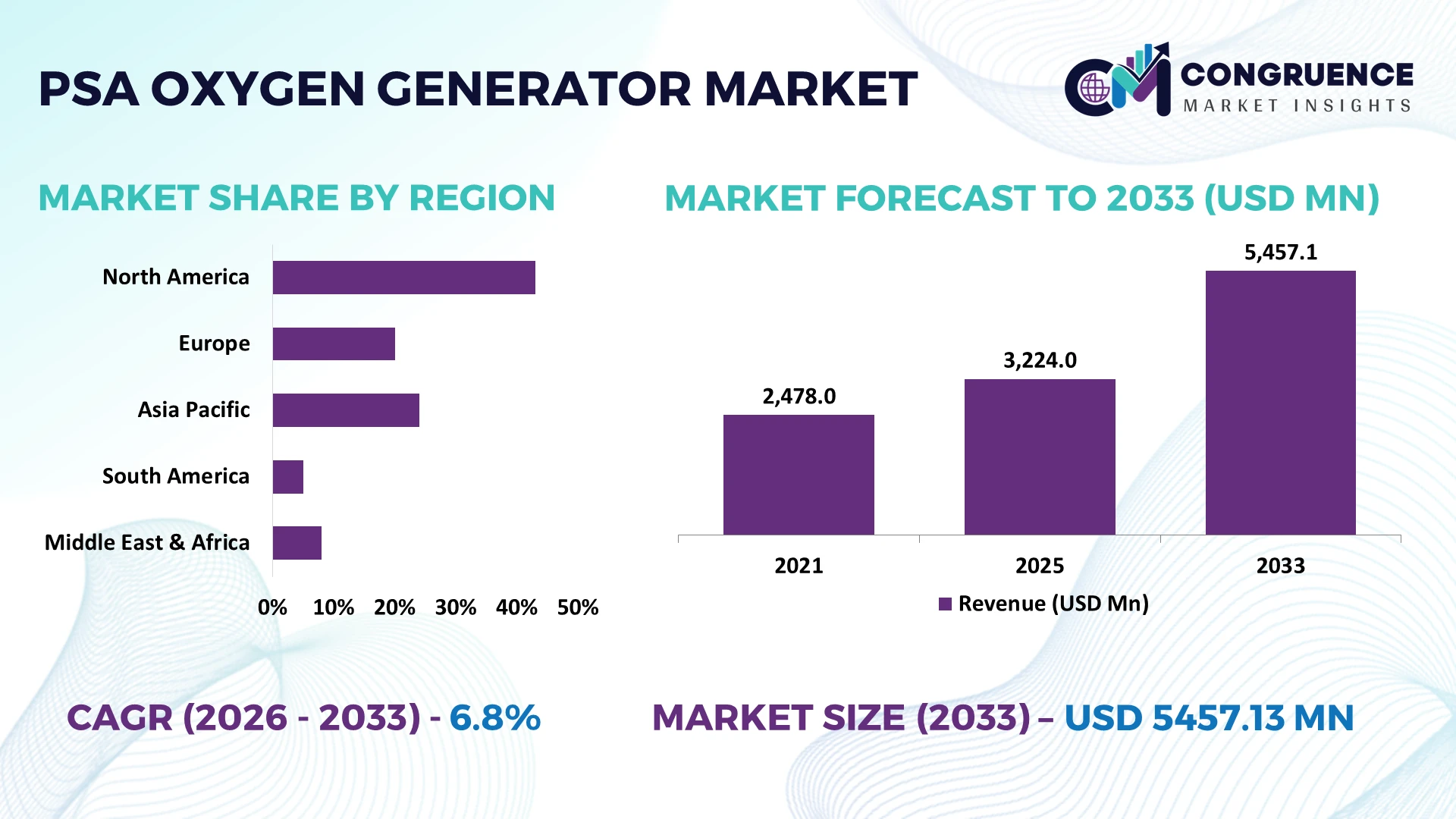

The Global PSA Oxygen Generator Market was valued at USD 3224 Million in 2025 and is anticipated to reach a value of USD 5457.13 Million by 2033 expanding at a CAGR of 6.8% between 2026 and 2033. Growth is primarily driven by rising deployment of on-site oxygen generation systems across healthcare, industrial manufacturing, wastewater treatment, and metal processing facilities seeking lower operating costs and uninterrupted oxygen availability.

China remains the dominant production and deployment hub, accounting for approximately 34% of global manufacturing capacity, supported by large-scale steel, healthcare, and industrial gas infrastructure investments exceeding USD 2 billion in recent expansion programs. Compared with Germany's advanced engineering-led installations, China records over 25% higher annual equipment deployment, while ongoing industrial supply-chain diversification following Red Sea shipping disruptions has accelerated localized manufacturing and digital monitoring adoption.

Manufacturers expanding regional production capacity and integrating intelligent monitoring capabilities are positioned to strengthen competitiveness across high-growth industrial and healthcare applications.

Market Size & Growth: USD 3224 Million in 2025, reaching USD 5457.13 Million by 2033 at 6.8% CAGR, driven by decentralized oxygen generation and industrial automation.

Top Growth Drivers: Healthcare installations +18%, industrial gas demand +15%, wastewater treatment adoption +12% across major economies.

Short-Term Forecast: By 2028, operating costs decline nearly 20% through energy-efficient compressors and optimized adsorption cycle control.

Emerging Technologies: AI-enabled monitoring, predictive maintenance, and advanced zeolite adsorption systems improve uptime by approximately 25%.

Regional Leaders: Asia-Pacific exceeds USD 2300 Million, Europe approaches USD 1250 Million, North America surpasses USD 1100 Million, supported by localized manufacturing expansion.

Consumer/End-User Trends: More than 60% of new hospital oxygen infrastructure projects prioritize on-site PSA systems over bulk liquid oxygen.

Pilot/Case Example: In 2026, an industrial oxygen installation reduced logistics dependence by 35% while improving continuous oxygen availability.

Competitive Landscape: Top manufacturers collectively control roughly 42% of global activity, with Atlas Copco, Parker Hannifin, AirSep, NOVAIR, and Oxymat leading innovation.

Regulatory & ESG Impact: Energy-efficient system adoption lowers electricity consumption by nearly 15%, supporting industrial sustainability targets.

Investment & Funding: Over USD 1.4 billion supports manufacturing expansion, strategic partnerships, and regional supply-chain localization.

Innovation & Future Outlook: Smart remote diagnostics, modular containerized systems, and digital asset management accelerate deployment across high-growth industrial facilities.

Demand for PSA oxygen generator systems continues expanding across hospitals, specialty manufacturing, wastewater treatment, and metal fabrication where uninterrupted oxygen supply improves operational resilience. Intelligent remote monitoring and energy-optimized adsorption technologies have increased system efficiency by nearly 20%, while regional manufacturing localization and stricter operational reliability requirements are reshaping procurement strategies, setting the foundation for the following strategic market assessment.

The PSA Oxygen Generator Market has become strategically important as industries prioritize operational resilience through decentralized oxygen production rather than dependence on delivered liquid oxygen. Infrastructure modernization in healthcare, metallurgy, wastewater treatment, and electronics manufacturing is accelerating investment in on-site generation systems that reduce logistics exposure and improve production continuity. Recent supply-chain restructuring has encouraged manufacturers to establish localized assembly and component sourcing, strengthening equipment availability while reducing delivery lead times by nearly 20%.

Modern PSA oxygen generators equipped with intelligent automation, remote diagnostics, and high-performance molecular sieve technology consume approximately 15% less energy than conventional compressed oxygen supply systems while reducing routine maintenance requirements. China continues to lead large-scale industrial deployment through integrated manufacturing ecosystems, whereas Germany emphasizes premium automation, energy optimization, and digital process control for high-value industrial applications. Over the next two to three years, predictive maintenance integration is expected to expand across more than 40% of newly commissioned industrial systems, improving uptime and operational planning.

A recent deployment in a steel manufacturing facility demonstrated a 30% reduction in oxygen transportation dependency after installing an on-site PSA generation system integrated with automated process controls. Equipment manufacturers are expanding service partnerships, investing in modular product platforms, and strengthening regional manufacturing networks to enhance delivery flexibility. Companies combining digital capabilities with localized production and lifecycle service offerings will secure stronger competitive positioning and long-term operational advantages.

Industrial facilities are accelerating adoption of on-site oxygen generation to improve operational continuity and reduce dependence on external gas deliveries. Nearly 65% of new medium-scale healthcare and manufacturing projects now evaluate decentralized oxygen infrastructure during facility planning, while energy-efficient PSA systems reduce operating power consumption by approximately 15%. India's expansion of industrial manufacturing clusters and hospital infrastructure has increased procurement of modular oxygen systems following stronger supply security requirements. This structural shift enables uninterrupted production while lowering transportation complexity. Manufacturers are responding through localized assembly facilities, expanded distributor partnerships, and intelligent monitoring platforms, allowing faster deployment, stronger after-sales support, and improved equipment utilization across multiple industrial sectors.

High-performance valves, compressors, and molecular sieve materials remain exposed to procurement volatility, increasing total installation costs by nearly 12% in several industrial projects. Approximately 30% of project delays are linked to specialized component availability and engineering integration schedules rather than equipment manufacturing itself. Japan and several European suppliers continue to dominate premium adsorption material production, creating sourcing concentration for advanced systems. These constraints affect project scalability and procurement planning, particularly for medium-sized enterprises. Companies are reducing exposure through multi-country sourcing strategies, localized inventory programs, long-term supplier agreements, and standardized modular equipment configurations that shorten engineering timelines and improve procurement predictability.

Digital transformation is creating new opportunities beyond traditional healthcare deployment. AI-enabled process optimization and predictive maintenance improve equipment availability by approximately 25%, while automated oxygen purity monitoring reduces manual inspection requirements by nearly 35%. Southeast Asian industrial parks and India's electronics manufacturing expansion are increasing demand for compact, modular PSA installations supporting continuous production. Equipment suppliers are investing in remote diagnostics, cloud-connected monitoring platforms, and advanced adsorption materials to differentiate product performance. An emerging opportunity lies in integrated energy management software that synchronizes oxygen generation with facility power consumption, delivering measurable operational savings while strengthening long-term customer retention through digital service ecosystems.

As PSA oxygen generators become increasingly connected, execution complexity extends beyond equipment manufacturing into software integration, cybersecurity, and lifecycle asset management. More than 45% of industrial buyers now require remote monitoring capabilities, while digital commissioning can reduce startup time by around 20%. However, shortages of automation engineers and service specialists remain a significant constraint in several manufacturing hubs, including India and Mexico. Companies must also maintain interoperability between legacy industrial control systems and modern digital platforms without disrupting production. Leading manufacturers are expanding technical training programs, investing in secure industrial communication architectures, and strengthening regional service networks to ensure reliable long-term deployment and sustained competitive differentiation.

Smart Monitoring Becomes Standard Intelligent controllers, IoT connectivity, and predictive diagnostics are becoming default features in new PSA oxygen generators. More than 45% of newly installed industrial systems now include remote monitoring, while predictive maintenance reduces unplanned downtime by nearly 25%. Rising labor shortages in Germany and Japan are accelerating automation adoption, prompting manufacturers to expand digital service platforms and subscription-based maintenance programs that improve asset utilization and shorten response times.

Localized Manufacturing Expansion Supply-chain restructuring is driving regional production of compressors, control panels, and skid-mounted systems. Delivery lead times have declined by approximately 18%, while locally sourced components now account for nearly 40% of new production in several Asian manufacturing hubs. Companies are establishing assembly facilities and supplier partnerships closer to customers, improving procurement flexibility, reducing logistics exposure, and increasing responsiveness to industrial project schedules.

Modular Deployment Accelerates Projects Prefabricated modular PSA oxygen generator packages are reducing installation timelines by nearly 30% and lowering on-site engineering requirements by around 20%. Industrial parks and healthcare infrastructure projects increasingly favor scalable systems that support phased capacity expansion. Equipment suppliers are standardizing modular platforms, enabling faster commissioning, simplified maintenance planning, and improved lifecycle management without extensive facility modifications.

Energy Optimization Gains Priority Industrial operators are prioritizing energy-efficient adsorption cycles, variable-speed compressors, and advanced molecular sieve technologies that lower electricity consumption by approximately 15% while maintaining oxygen purity above 93%. Tightening industrial efficiency targets and modernization programs in India are reinforcing this transition. Manufacturers are strengthening technology partnerships and redesigning product portfolios around lower lifecycle operating costs rather than solely increasing production capacity.

Stationary PSA oxygen generators remain the dominant segment, accounting for approximately 48% of installations due to their continuous output, operational reliability, and seamless integration into hospitals and large industrial facilities. Their ability to support uninterrupted oxygen supply with lower long-term operating costs makes them the preferred choice for high-volume applications. High-capacity systems continue to serve steel manufacturing and chemical processing where continuous oxygen demand remains critical, while modular configurations are gaining attention for scalable industrial expansion projects.

Portable systems represent the fastest-growing segment as healthcare outreach, emergency preparedness, and temporary industrial operations demand flexible deployment. Adoption has increased by nearly 22% across mobile healthcare and remote project locations, while modular systems have shortened installation time by almost 30% through standardized configurations. Manufacturers are expanding modular product portfolios, enhancing mobility features, and investing in intelligent control technologies to address diverse operational requirements. These shifts are redirecting investment toward flexible product architectures capable of serving both permanent and temporary oxygen generation needs.

Medical Oxygen Supply remains the leading application, representing approximately 42% of overall demand as hospitals prioritize uninterrupted oxygen availability and reduced dependence on delivered liquid oxygen. Healthcare infrastructure modernization and stricter emergency preparedness programs continue to strengthen deployment across public and private facilities. Industrial Oxygen Generation is expanding steadily through steel production, electronics manufacturing, and chemical processing, while Food Processing and Wastewater Treatment maintain consistent adoption where process efficiency and environmental compliance remain operational priorities.

Metal Processing is the fastest-growing application, supported by increasing investment in advanced fabrication and high-efficiency cutting technologies. Oxygen consumption in automated metal processing facilities has increased by nearly 18%, while integrated PSA systems have reduced production interruptions by approximately 20%. Equipment suppliers are responding through application-specific engineering, automated purity control, and customized system integration. Demand is increasingly shifting toward installations that combine production efficiency, digital monitoring, and long-term operational stability across multiple industrial environments.

Hospitals remain the largest end-user group, accounting for approximately 40% of deployments because continuous oxygen availability is essential for emergency care, surgery, and intensive care operations. Healthcare providers increasingly prefer on-site generation systems to improve operational resilience and reduce supply disruptions. Manufacturing industries follow closely, benefiting from reliable oxygen supply for fabrication, electronics, and chemical production. Water treatment facilities and Food & Beverage companies continue expanding adoption as oxygen-intensive treatment and processing requirements become more automated.

Manufacturing industries represent the fastest-growing end-user segment, with industrial installations increasing by nearly 21% as companies modernize production infrastructure and automate oxygen-dependent processes. Metal Processing Companies are expanding investments in integrated oxygen systems supporting precision cutting and furnace operations, while Water Treatment Facilities are adopting compact modular units to improve treatment efficiency. Equipment manufacturers are targeting these segments through customized engineering, long-term maintenance agreements, and digital performance monitoring, strengthening customer retention while expanding recurring service opportunities.

Asia-Pacific accounted for the largest market share at 41.8% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a 7.6% between 2026 and 2033.

Strategic Modernization Through Industrial Automation

North America represents a mature PSA oxygen generator market supported by advanced healthcare infrastructure, high-value manufacturing, and widespread industrial automation. The region contributes approximately 24% of global demand, with deployment concentrated across hospitals, metal fabrication, chemicals, and wastewater treatment facilities. More than 55% of newly commissioned industrial oxygen systems incorporate digital monitoring and predictive maintenance capabilities, improving operational continuity and maintenance planning. Expansion of semiconductor manufacturing and critical infrastructure projects is accelerating investment in decentralized oxygen generation, while manufacturers continue strengthening regional service networks and engineering partnerships to reduce commissioning time and improve lifecycle performance. Standardized modular equipment is also increasing adoption across medium-scale industrial facilities seeking operational flexibility and lower logistics dependency.

United States Market Outlook: The United States leads regional deployment through its extensive healthcare network, advanced manufacturing ecosystem, and strong automation capabilities. Approximately 60% of large industrial oxygen generation projects integrate remote monitoring and intelligent process controls during installation. Continued investment in semiconductor fabrication, pharmaceutical production, and industrial modernization supports sustained equipment demand, while domestic engineering expertise and established service infrastructure enable faster implementation and long-term operational reliability.

Efficiency-Driven Industrial Modernization

Europe maintains a strong market position through advanced engineering, energy-efficient manufacturing, and stringent industrial performance standards. The region accounts for nearly 22% of global deployment, with oxygen generation systems increasingly integrated into pharmaceuticals, food processing, specialty manufacturing, and wastewater treatment. More than 48% of new industrial installations emphasize energy optimization and digital asset management, reflecting enterprise-wide modernization strategies. Industrial operators are replacing conventional oxygen supply models with on-site PSA systems to improve supply resilience and reduce operational complexity. Equipment suppliers continue expanding automation capabilities, modular product offerings, and lifecycle service agreements to meet evolving industrial efficiency requirements.

Germany Market Outlook: Germany remains the region's technology leader through its highly automated industrial base and precision engineering expertise. Industrial manufacturers increasingly deploy digitally integrated PSA oxygen systems capable of reducing maintenance interventions by approximately 20%. Strong collaboration between equipment suppliers, industrial automation companies, and manufacturing enterprises continues strengthening innovation, while advanced engineering standards support reliable deployment across metal processing, chemicals, and healthcare applications.

Manufacturing Scale Drives Market Leadership

Asia-Pacific leads the global PSA oxygen generator market through extensive industrial production, expanding healthcare infrastructure, and large-scale manufacturing investment. The region contributes approximately 41.8% of global demand, supported by strong deployment across steel manufacturing, electronics, healthcare, and wastewater treatment. More than 50% of new industrial oxygen installations are commissioned within major manufacturing economies, benefiting from localized production capabilities and integrated supply networks. Industrial modernization programs, expanding production capacity, and growing adoption of intelligent process automation continue strengthening market competitiveness. Equipment manufacturers are increasing local assembly operations and regional distribution networks to improve delivery efficiency and technical support.

China Market Outlook: China dominates regional production through its extensive manufacturing ecosystem and integrated industrial infrastructure. Approximately 34% of global PSA oxygen generator manufacturing capacity is concentrated in the country, supported by large-scale steel, electronics, and healthcare investments. Domestic producers continue expanding automated manufacturing facilities, strengthening export competitiveness, and investing in intelligent equipment platforms that improve production efficiency while supporting both domestic and international demand.

Industrial Infrastructure Supports Steady Adoption

South America is witnessing stable expansion as industrial modernization, healthcare investment, and environmental infrastructure projects increase demand for decentralized oxygen generation. The region represents approximately 7% of global deployment, with mining, food processing, healthcare, and wastewater treatment remaining the primary application sectors. Installation activity has increased by nearly 16% across industrial facilities adopting automated oxygen generation to reduce logistics dependence. While infrastructure limitations and engineering capacity vary between countries, equipment suppliers are expanding regional partnerships and localized technical services to improve deployment consistency and operational reliability.

Brazil Market Outlook: Brazil represents the largest national market due to its diversified industrial base, extensive healthcare network, and expanding food processing sector. Mining operations and manufacturing facilities increasingly deploy on-site oxygen systems to improve operational continuity and reduce transportation costs. Growing investment in industrial modernization and localized engineering support continues strengthening equipment adoption across both public and private sector projects.

Infrastructure Investment Reshapes Deployment Strategy

The Middle East & Africa market is advancing through healthcare expansion, industrial diversification, and infrastructure modernization programs. Approximately 5.5% of global deployment is concentrated within the region, with increasing investment in hospitals, petrochemical facilities, desalination plants, and industrial manufacturing. More than 18% growth in newly commissioned healthcare infrastructure projects has strengthened demand for reliable on-site oxygen generation. Equipment suppliers are establishing regional partnerships, expanding technical service capabilities, and introducing modular systems suited for remote industrial operations where continuous oxygen availability is operationally essential.

Saudi Arabia Market Outlook: Saudi Arabia leads regional demand through large-scale industrial diversification initiatives, healthcare infrastructure development, and expanding manufacturing investment. Industrial projects increasingly integrate automated PSA oxygen generators into petrochemical, metal processing, and healthcare facilities to improve operational resilience. Strong government-backed infrastructure programs and localized industrial expansion continue supporting advanced oxygen generation technologies while encouraging international technology partnerships and regional manufacturing collaboration.

The competitive landscape is led by Atlas Copco, Parker Hannifin, NOVAIR, Oxymat, and AirSep, competing directly against fast-growing regional manufacturers in China and India that emphasize lower production costs and faster delivery. The top five companies collectively account for approximately 43% of the global market, while regional specialists compete aggressively through localized engineering and customized system integration. Global leaders differentiate through digital automation, premium adsorption technology, and lifecycle service contracts, whereas cost-focused manufacturers reduce procurement costs by nearly 18% and shorten delivery cycles by approximately 20%. Competition increasingly centers on intelligent monitoring, modular product architecture, and vertically integrated manufacturing that improves component availability by nearly 15%. Strategic partnerships with EPC contractors, hospital infrastructure developers, and industrial automation providers are accelerating market penetration. The competitive shift favors suppliers controlling critical components and digital service ecosystems rather than standalone equipment sales. High engineering certification requirements and specialized adsorption expertise remain significant entry barriers. Sustainable competitive advantage depends on integrated technology, localized manufacturing, rapid deployment, and long-term service capability.

Atlas Copco

Parker Hannifin Corporation

NOVAIR

Oxymat A/S

AirSep Corporation

OXYPLUS Technologies

On Site Gas Systems

Peak Scientific

PCI Gases

Oxair Gas Systems

Erre Due S.p.A.

Inmatec GaseTechnologie GmbH

BERG GaseTech GmbH

Advanced PSA oxygen generator technology is rapidly transitioning from conventional standalone systems to digitally connected, intelligent platforms. AI-enabled controllers, IoT-based monitoring, and predictive maintenance are now integrated into approximately 45% of newly deployed industrial systems, reducing unplanned downtime by nearly 25%. Compared with legacy fixed-control equipment, modern automated PSA systems improve energy efficiency by approximately 15% while delivering more stable oxygen purity through adaptive process optimization. These improvements enable operators to reduce maintenance interventions and improve production continuity across healthcare and industrial environments.

Emerging technologies include advanced lithium-based molecular sieve materials, variable-speed compressor systems, and cloud-connected asset management platforms. Intelligent adsorption cycle optimization lowers compressed air consumption by around 12%, while remote diagnostics reduce service response times by nearly 30%. Large multinational manufacturers benefit from these technologies through scalable digital service offerings, whereas regional equipment suppliers gain competitiveness by integrating modular automation into cost-efficient product portfolios. Interoperability with industrial control systems is becoming a key purchasing criterion for enterprise customers.

Between 2026 and 2028, autonomous process optimization, digital twins, and edge-based analytics will become mainstream differentiators for premium PSA oxygen generator platforms. Adoption across new industrial installations is expected to exceed 55% as manufacturers prioritize operational resilience, lifecycle efficiency, and predictive asset performance. Companies investing now in intelligent software integration, modular engineering, and advanced adsorption materials will strengthen competitive positioning, accelerate deployment, and secure higher-value long-term service relationships in increasingly technology-driven procurement environments.

June 2024 Atlas Copco launched its next-generation OGP 2–225 PSA oxygen generator range with 17 capacity variants delivering oxygen up to 225 Nm³/h at 93% purity, strengthening energy-efficient on-site oxygen generation for industrial users and expanding deployment flexibility.

October 2024 NOVAIR introduced the ION Ionic Oxygen Generator, producing oxygen with purity exceeding 99.99%, marking a technology shift beyond conventional PSA systems while expanding high-purity medical oxygen capabilities and reinforcing innovation leadership. Source: https://www.novairmedical.com

May 2025 NOVAIR published results of an independent life-cycle assessment demonstrating environmental advantages of its on-site oxygen generation solutions, supporting lower logistics-related emissions and strengthening sustainability positioning for healthcare infrastructure investment decisions.

June 2026 NOVAIR showcased its ION oxygen generation platform at EUROSATORY 2026, highlighting oxygen purity above 99.99% and integrated on-site cylinder filling capabilities, improving operational autonomy for defense and critical infrastructure applications while reducing external supply dependence. Source: https://www.eurosatory.com

This report provides comprehensive analysis of the PSA Oxygen Generator Market across Stationary, Portable, Modular, and High-Capacity systems, covering Medical Oxygen Supply, Industrial Oxygen Generation, Wastewater Treatment, Food Processing, and Metal Processing applications. It evaluates demand across hospitals, manufacturing industries, water treatment facilities, food and beverage companies, and metal processing enterprises while assessing deployment trends, technology adoption, and operational performance across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. More than 40% of installations are concentrated in large industrial and healthcare environments, reflecting sustained infrastructure modernization.

The report further examines competitive positioning, digital automation, adsorption technology advances, modular deployment strategies, and intelligent monitoring solutions shaping procurement decisions between 2026 and 2033. Strategic insights include regional manufacturing expansion, supply-chain localization, enterprise partnerships, and emerging niche opportunities supporting investment planning, product development, market entry, capacity expansion, and long-term competitive differentiation across evolving industrial and healthcare ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

Market Revenue in 2025 | USD 3224 Million |

Market Revenue in 2033 | USD 5457.13 Million |

CAGR (2026 - 2033) | 6.8% |

Base Year | 2025 |

Forecast Period | 2026 - 2033 |

Historic Period | 2021 - 2025 |

Segments Covered | By Type

By Application

By End-User

|

Key Report Deliverable | Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

Region Covered | North America, Europe, Asia-Pacific, South America, Middle East, Africa |

Key Players Analyzed | Atlas Copco, Parker Hannifin Corporation, NOVAIR, Oxymat A/S, AirSep Corporation, OXYPLUS Technologies, On Site Gas Systems, Peak Scientific, PCI Gases, Oxair Gas Systems, Erre Due S.p.A., Inmatec GaseTechnologie GmbH, BERG GaseTech GmbH |

Customization & Pricing | Available on Request (10% Customization is Free) |