Reports

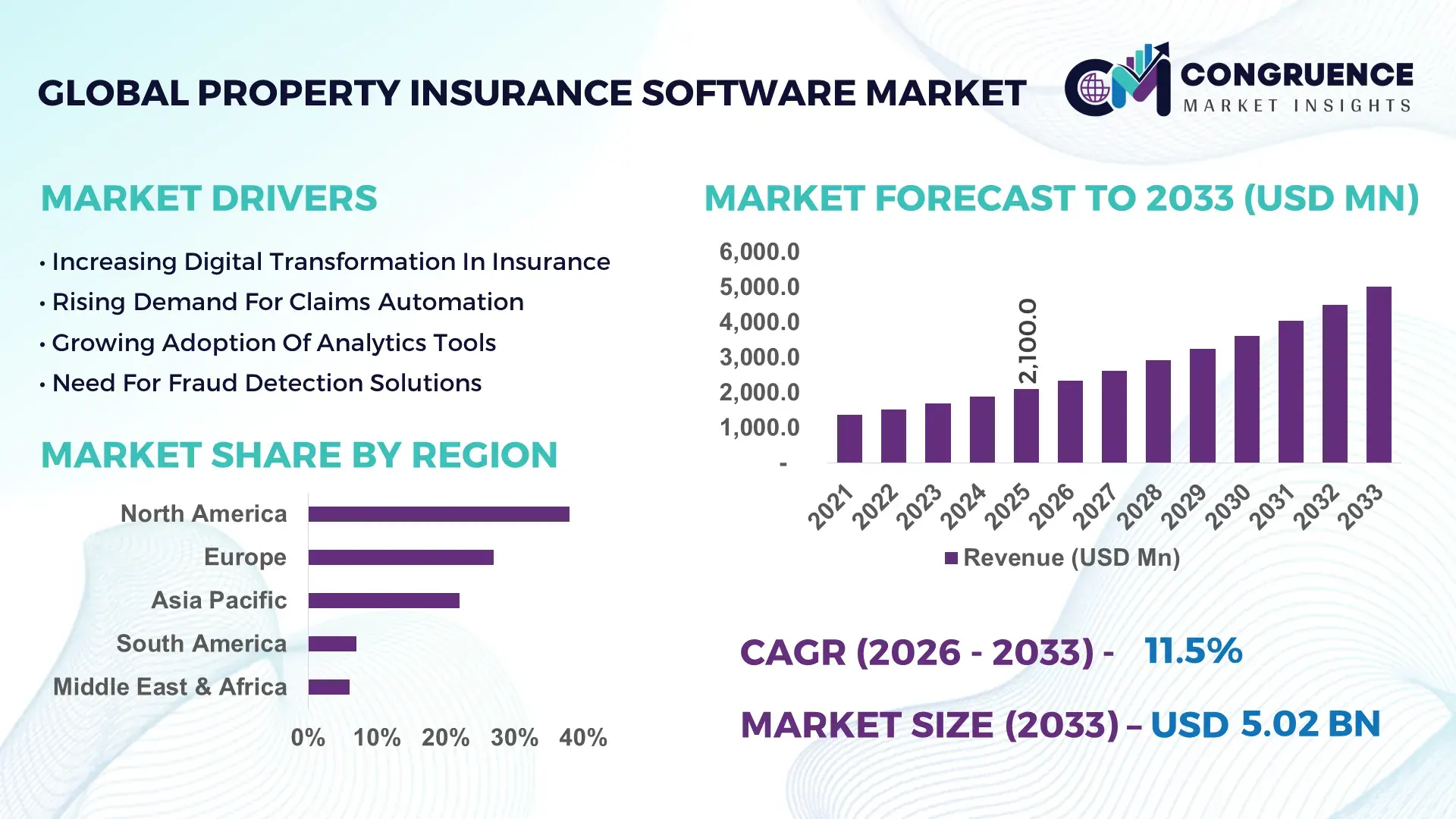

The Global Property Insurance Software Market was valued at USD 2,100.0 Million in 2025 and is anticipated to reach a value of USD 5,016.7 Million by 2033 expanding at a CAGR of 11.5% between 2026 and 2033, according to an analysis by Congruence Market Insights. Growth is primarily driven by increasing adoption of digital underwriting platforms and AI-powered claims automation across insurers.

The United States leads the Property Insurance Software Market with advanced digital infrastructure and high enterprise-level adoption. Over 68% of large insurers in the country have integrated cloud-based policy administration systems, while nearly 52% utilize AI-driven risk modeling tools. Investment in InsurTech exceeded USD 8.5 billion in 2025, with more than 120 active technology providers supporting underwriting, fraud detection, and claims automation. Additionally, over 45% of insurers deploy predictive analytics to improve loss ratio performance, while API-based integrations are implemented by 60% of mid-to-large carriers to streamline operations across property portfolios.

Market Size & Growth: USD 2,100.0 Million in 2025, projected to reach USD 5,016.7 Million by 2033 at 11.5% CAGR, driven by digitization of insurance operations.

Top Growth Drivers: Cloud adoption (72%), AI-driven claims processing efficiency (48%), automation in underwriting (55%).

Short-Term Forecast: By 2028, operational cost reduction expected by 30% through automation and analytics integration.

Emerging Technologies: AI-based risk scoring, blockchain-enabled policy management, and API-driven ecosystems.

Regional Leaders: North America (USD 1,950 Million by 2033, strong cloud adoption), Europe (USD 1,420 Million, regulatory-driven digitalization), Asia-Pacific (USD 1,180 Million, rapid InsurTech expansion).

Consumer/End-User Trends: Over 62% insurers prioritize digital claims platforms; SME insurers show 40% rise in SaaS adoption.

Pilot or Case Example: In 2025, a U.S. insurer reduced claims processing time by 35% using AI-based automation tools.

Competitive Landscape: Market leader holds ~18% share; key players include Guidewire Software, Duck Creek Technologies, Sapiens, Majesco, and TIA Technology.

Regulatory & ESG Impact: Over 50% insurers aligning with ESG compliance frameworks; digital reporting tools rising by 38%.

Investment & Funding Patterns: Global InsurTech funding crossed USD 10 billion in 2025 with increased venture investments.

Innovation & Future Outlook: Integration of IoT-based property monitoring and predictive analytics expected to reshape underwriting models.

Property insurance software adoption is concentrated across commercial property (48%), residential insurance (32%), and industrial risk management (20%). AI-based underwriting tools improved risk assessment accuracy by 27%, while regulatory digitization mandates increased compliance software usage by 35%. North America leads consumption, while Asia-Pacific shows strong expansion due to 45% rise in digital insurance platforms and increasing cloud-based deployments among insurers.

The Property Insurance Software Market holds strong strategic relevance as insurers transition toward digital-first operating models. Increasing climate-related risks have pushed insurers to adopt predictive analytics and AI-driven underwriting systems, improving risk accuracy by over 30% compared to traditional actuarial models. Advanced analytics platforms deliver 25% faster claims settlement compared to legacy manual systems, highlighting measurable efficiency gains.

North America dominates in volume due to high insurer density and mature digital ecosystems, while Asia-Pacific leads in adoption with over 58% of insurers implementing cloud-based platforms. By 2028, AI-enabled automation is expected to reduce claims processing time by 40%, improving operational efficiency and customer satisfaction metrics significantly.

Firms are committing to ESG metrics, including reducing paper-based workflows by 60% by 2030 through digital documentation and automation. In 2025, a leading U.S.-based insurer achieved a 33% reduction in fraud-related losses by deploying machine learning algorithms for real-time claims validation.

Strategically, insurers are investing in modular software architectures and API integrations, enabling faster deployment cycles and interoperability with third-party systems. The integration of IoT-based property monitoring is also gaining traction, with over 35% of insurers piloting connected-device ecosystems.

Looking ahead, the Property Insurance Software Market is positioned as a critical pillar of resilience, regulatory compliance, and sustainable growth, enabling insurers to manage risks effectively while enhancing operational transparency and customer experience.

The Property Insurance Software Market is experiencing significant transformation driven by digital innovation, regulatory mandates, and evolving customer expectations. Insurers are increasingly investing in cloud-based policy administration systems, with adoption rates exceeding 65% among large enterprises. The integration of artificial intelligence and machine learning has improved underwriting accuracy by nearly 30%, while claims automation platforms have reduced processing time by over 35%. Additionally, increasing exposure to climate-related risks has accelerated the demand for predictive analytics tools. Regulatory requirements for data transparency and compliance have further driven software adoption, particularly in developed markets. The rise of InsurTech startups, which grew by over 40% globally in the last five years, has intensified competition and innovation. Furthermore, the shift toward API-driven ecosystems has enabled seamless integration across platforms, enhancing operational efficiency and scalability for insurers worldwide.

The rapid digital transformation of the insurance industry is a major driver for the Property Insurance Software Market. Over 70% of insurers have adopted digital platforms to streamline underwriting, policy administration, and claims processing. Automation technologies have improved operational efficiency by nearly 45%, reducing manual intervention and human error. Additionally, AI-based risk assessment tools have enhanced underwriting precision by approximately 28%, enabling insurers to price policies more accurately. Cloud adoption has also increased significantly, with more than 65% of insurers deploying SaaS-based solutions to enhance scalability and reduce IT infrastructure costs. Furthermore, digital claims platforms have improved customer satisfaction rates by over 30%, as claims processing times have been reduced substantially. The integration of advanced analytics allows insurers to analyze large datasets, improving fraud detection rates by 25% and optimizing loss ratios. These factors collectively contribute to the strong demand for property insurance software solutions globally.

Data security concerns and integration complexities present significant challenges for the Property Insurance Software Market. Approximately 48% of insurers report difficulties in integrating new software solutions with legacy systems, leading to increased implementation timelines and operational disruptions. Additionally, the insurance sector is highly sensitive to data breaches, with cyberattacks increasing by over 35% in recent years. Compliance with stringent data protection regulations such as GDPR and regional privacy laws requires substantial investment in cybersecurity infrastructure. Around 40% of insurers face challenges in maintaining secure data environments while implementing cloud-based solutions. Furthermore, interoperability issues between different software platforms hinder seamless data exchange, affecting efficiency and scalability. The lack of standardized data formats across insurers also complicates integration efforts. These factors increase operational costs and limit the adoption of advanced property insurance software solutions, particularly among small and mid-sized insurers.

The adoption of AI and predictive analytics presents significant opportunities for the Property Insurance Software Market. AI-driven underwriting systems have improved risk assessment accuracy by over 30%, enabling insurers to minimize losses and optimize pricing strategies. Predictive analytics tools are increasingly used to assess property risks related to climate change, with over 50% of insurers incorporating weather and geospatial data into their models. Additionally, fraud detection systems powered by machine learning have increased detection rates by approximately 27%, reducing financial losses. The growing use of IoT devices, such as smart home sensors, has enabled insurers to monitor property conditions in real time, reducing claims frequency by nearly 20%. Furthermore, digital platforms have improved customer engagement, with over 60% of policyholders preferring online policy management systems. These advancements create new growth avenues for software providers, particularly in emerging markets where digital adoption is accelerating rapidly.

High implementation costs and a shortage of skilled professionals are key challenges for the Property Insurance Software Market. Deploying advanced software solutions requires significant investment in IT infrastructure, with implementation costs increasing by approximately 25% for large-scale deployments. Additionally, nearly 42% of insurers report a shortage of skilled professionals capable of managing AI and analytics platforms. Training and upskilling employees further add to operational costs. Small and medium-sized insurers face particular difficulties, as limited budgets restrict their ability to adopt advanced technologies. Moreover, the rapid pace of technological change creates challenges in maintaining updated systems and ensuring compatibility with evolving standards. Integration of new technologies such as blockchain and IoT requires specialized expertise, which is currently limited in the market. These factors collectively hinder the widespread adoption of property insurance software solutions across different regions.

AI-Driven Claims Automation Adoption Increasing by 48% Across Insurers: Insurers are rapidly integrating AI-based claims processing systems, with nearly 48% of global insurers adopting automated claims platforms in 2025. These systems have reduced claims settlement time by 35% and improved fraud detection rates by 27%. The trend is particularly strong in North America and Europe, where digital maturity is higher.

Cloud-Based Policy Administration Systems Surpassing 65% Adoption Rate: Cloud deployment models now account for over 65% of software implementations, enabling insurers to reduce IT costs by 30% and improve scalability. SaaS-based platforms are particularly popular among mid-sized insurers, which have increased adoption by 42% in the past three years.

Integration of IoT in Property Risk Monitoring Growing by 38%: IoT-enabled devices such as smart sensors and connected home systems are being used by approximately 38% of insurers to monitor property risks in real time. This has reduced claim frequency by 20% and improved preventive risk management capabilities.

API-Based Ecosystems Enhancing Interoperability by 55% Efficiency Gains: API-driven software architectures are enabling seamless integration between systems, improving data exchange efficiency by 55%. Over 60% of insurers are now using API-based platforms to connect underwriting, claims, and customer management systems, enhancing operational agility.

The Property Insurance Software Market is segmented based on type, application, and end-user, reflecting diverse operational requirements across the insurance value chain. Software types include policy administration, claims management, underwriting, and analytics platforms, each addressing specific business needs. Applications span personal property insurance, commercial property insurance, and specialty insurance segments, with varying adoption levels depending on risk complexity. End-users primarily include insurance companies, brokers, and third-party administrators. The increasing need for digital transformation has driven higher adoption across all segments, particularly in commercial insurance where risk assessment complexity is higher. Additionally, cloud-based deployment and AI integration are influencing segmentation trends, with insurers prioritizing scalable and data-driven solutions to improve efficiency and customer experience.

Policy administration software leads the segment, accounting for approximately 34% share due to its critical role in managing policy lifecycles, billing, and compliance processes. Claims management systems hold around 28%, driven by increasing demand for automation and faster claims processing. Underwriting software contributes nearly 22%, benefiting from AI-based risk assessment capabilities. Analytics and reporting tools, along with other niche solutions, collectively account for 16% of the market. Among these, underwriting software is the fastest-growing segment, with an expected CAGR of 13.2%, driven by the adoption of predictive analytics and machine learning models that enhance risk evaluation accuracy. Claims management systems are also gaining traction due to their ability to reduce processing time and improve customer satisfaction. Policy administration remains dominant due to its foundational role in insurance operations.

• In 2025, a major global insurer implemented AI-driven underwriting software, improving risk assessment accuracy by 29% and reducing underwriting time by 22% across its property insurance portfolio.

Commercial property insurance dominates the application segment with approximately 46% share, driven by the complexity of risk assessment and higher policy values. Personal property insurance accounts for around 34%, supported by increasing consumer adoption of digital insurance platforms. Specialty insurance applications contribute nearly 20%, addressing niche market requirements. Commercial insurance remains dominant due to the need for advanced analytics and risk modeling tools. However, personal property insurance is the fastest-growing segment, with a CAGR of 12.8%, driven by rising digital adoption among individual consumers and SMEs. Specialty applications are gaining importance in high-risk sectors such as industrial and infrastructure insurance. In 2025, over 58% of insurers reported adopting digital platforms for commercial property insurance, while nearly 45% of individual policyholders preferred online policy management systems.

• In 2025, a national insurance body reported that digital claims platforms were deployed across more than 150 commercial insurance providers, improving claims processing efficiency by 31%.

Insurance companies dominate the end-user segment, accounting for approximately 62% share due to their direct involvement in underwriting, claims management, and policy administration. Brokers and agents contribute around 23%, leveraging software platforms for customer relationship management and policy distribution. Third-party administrators and other service providers account for the remaining 15%. Insurance companies remain the largest segment due to their extensive operational requirements and high investment capacity in digital technologies. However, brokers and agents represent the fastest-growing segment, with a CAGR of 12.5%, driven by increasing demand for digital sales platforms and customer engagement tools. Third-party administrators are also adopting advanced software solutions to improve efficiency and service quality. In 2025, over 60% of insurers reported implementing AI-driven platforms, while 38% of brokers adopted cloud-based CRM tools to enhance customer interactions.

• In 2025, a leading industry association reported that over 500 insurance firms globally upgraded their digital platforms, improving operational efficiency by 28% and customer satisfaction scores significantly.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 12.9% between 2026 and 2033.

North America leads due to high digital adoption among insurers, with over 68% using cloud-based platforms. Europe follows with a 27% share, driven by regulatory compliance requirements and digital transformation initiatives. Asia-Pacific holds around 22%, supported by rapid InsurTech expansion and increasing adoption of digital insurance solutions in countries such as China, India, and Japan. South America and the Middle East & Africa collectively account for 13%, with growing investments in digital infrastructure. The increasing focus on automation, AI integration, and regulatory compliance continues to shape regional market dynamics.

North America holds approximately 38% share of the Property Insurance Software Market, driven by high adoption of cloud and AI technologies. The region’s insurance sector is highly digitized, with over 68% of insurers using SaaS-based platforms. Regulatory frameworks promoting data transparency and cybersecurity compliance further support adoption. Key industries include commercial property insurance and real estate. Companies such as Guidewire Software are actively enhancing their platforms with AI capabilities. Consumer behavior shows strong preference for digital claims processing, with over 65% of policyholders opting for online services.

Europe accounts for around 27% of the market, with key countries including Germany, the UK, and France. Regulatory initiatives such as GDPR have increased demand for secure and compliant software solutions. Over 55% of insurers in the region have adopted digital platforms. Sustainability initiatives are also driving ESG-focused software adoption. Local players are focusing on AI integration and cloud migration. Consumer behavior reflects strong demand for transparent and compliant insurance services.

Asia-Pacific holds approximately 22% share and is the fastest-growing region. Countries such as China, India, and Japan are leading adoption. Over 50% of insurers are investing in digital platforms. The rise of InsurTech startups and mobile-based insurance solutions is driving growth. Regional innovation hubs are focusing on AI and big data analytics. Consumer behavior shows strong preference for mobile-based insurance services.

South America accounts for around 7% of the market, with Brazil and Argentina as key contributors. Increasing investments in digital infrastructure and insurance penetration are driving adoption. Government initiatives supporting financial inclusion are also contributing. Local insurers are adopting cloud-based platforms to improve efficiency. Consumer behavior indicates growing acceptance of digital insurance platforms.

The Middle East & Africa region holds approximately 6% share, with key markets including the UAE and South Africa. Growth is driven by infrastructure development and increasing insurance penetration. Digital transformation initiatives and government support are enhancing adoption. Local players are investing in AI-based platforms. Consumer behavior reflects increasing demand for digital insurance services.

United States – 38% Market share: strong digital infrastructure and high enterprise adoption of advanced insurance platforms.

United Kingdom – 12% Market share: regulatory-driven demand and widespread adoption of compliance-focused software solutions.

The Property Insurance Software Market is moderately fragmented, with over 120 active global and regional players competing across various segments. The top five companies collectively hold approximately 42% of the market, indicating a competitive yet evolving landscape. Key players are focusing on product innovation, strategic partnerships, and acquisitions to strengthen their market position. Over 35% of companies have launched AI-enabled solutions in the past two years, reflecting a strong shift toward advanced analytics and automation. Cloud-based platforms account for more than 60% of new product deployments, highlighting the growing preference for scalable solutions.

Additionally, mergers and acquisitions have increased by 28% in recent years, enabling companies to expand their technological capabilities and geographic presence. Strategic collaborations between insurers and InsurTech firms are also rising, with over 45% of insurers partnering with technology providers to enhance digital capabilities. The competitive environment is characterized by continuous innovation and increasing investment in next-generation technologies.

Duck Creek Technologies

Sapiens International Corporation

Majesco

TIA Technology

SAP SE

Oracle Corporation

Microsoft Corporation

IBM Corporation

Infosys Limited

Cognizant Technology Solutions

Accenture PLC

Pegasystems Inc.

Fadata Group

The Property Insurance Software Market is heavily influenced by advancements in artificial intelligence, cloud computing, and data analytics. AI-driven underwriting systems have improved risk assessment accuracy by over 30%, while machine learning algorithms have enhanced fraud detection rates by approximately 27%. Cloud-based platforms dominate deployment models, with over 65% of insurers adopting SaaS solutions to improve scalability and reduce infrastructure costs.

Blockchain technology is gaining traction, with nearly 25% of insurers piloting blockchain-based policy management systems to enhance transparency and reduce fraud. Additionally, IoT integration is transforming property risk management, with smart sensors reducing claims frequency by 20% through real-time monitoring. API-based architectures are also becoming standard, enabling seamless integration across platforms and improving operational efficiency by 55%.

Advanced analytics tools are being used by over 50% of insurers to process large datasets, enabling better decision-making and predictive modeling. Robotic process automation (RPA) has reduced manual workload by 40%, improving operational efficiency. Furthermore, cybersecurity technologies are increasingly important, as insurers invest in advanced security solutions to protect sensitive data. These technological advancements are shaping the future of the market, enabling insurers to enhance efficiency, reduce risks, and improve customer experience.

• In October 2025, Guidewire Software expanded its global partner ecosystem and removed e-learning fees for partners to accelerate implementation capabilities and digital transformation. The initiative also added new technology partners and expanded its Marketplace platform to enhance insurer efficiency and integration capabilities. Source: www.guidewire.com

• In October 2025, Guidewire Software recognized multiple insurers and partners at its Connections Conference for deploying cloud-based platforms that significantly improved underwriting speed and reduced manual processing hours, with over 3,000 participants showcasing innovation in intelligent insurance solutions.

• In March 2025, Majesco launched its Spring ’25 Release featuring AI-powered automation tools that enabled insurers to achieve up to 75% faster quote generation, 98% accuracy in cash application processes, and 50% reduction in implementation timelines through pre-configured insurance workflows

• In September 2025, Majesco introduced its Fall ’25 platform enhancements with over 13 new AI agents and advanced analytics capabilities, enabling real-time underwriting, claims automation, and processing of over 100,000 transactions with improved scalability and operational efficiency.

The Property Insurance Software Market Report provides a comprehensive analysis of key segments, technologies, and regional dynamics shaping the industry. The report covers multiple software types, including policy administration, claims management, underwriting, and analytics platforms, each addressing distinct operational requirements within the insurance value chain. It also examines applications across commercial, personal, and specialty property insurance segments, highlighting variations in adoption and usage patterns.

Geographically, the report analyzes five major regions, including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, with detailed insights into country-level trends. The report further explores technological advancements such as AI, machine learning, blockchain, IoT, and cloud computing, which are transforming the industry.

Additionally, the report evaluates end-user segments, including insurance companies, brokers, and third-party administrators, providing insights into their adoption patterns and operational needs. It also highlights emerging trends such as API-driven ecosystems, digital claims platforms, and predictive analytics. The scope includes competitive analysis, covering over 100 market participants, along with their strategic initiatives and innovation trends. Overall, the report serves as a valuable resource for decision-makers, offering actionable insights into market opportunities, challenges, and future growth prospects.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 2,100.0 Million |

| Market Revenue (2033) | USD 5,016.7 Million |

| CAGR (2026–2033) | 11.5% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Guidewire Software; Duck Creek Technologies; Sapiens International Corporation; Majesco; TIA Technology; SAP SE; Oracle Corporation; Microsoft Corporation; IBM Corporation; Infosys Limited; Cognizant Technology Solutions; Accenture PLC; Pegasystems Inc.; Fadata Group |

| Customization & Pricing | Available on Request (10% Customization Free) |