Reports

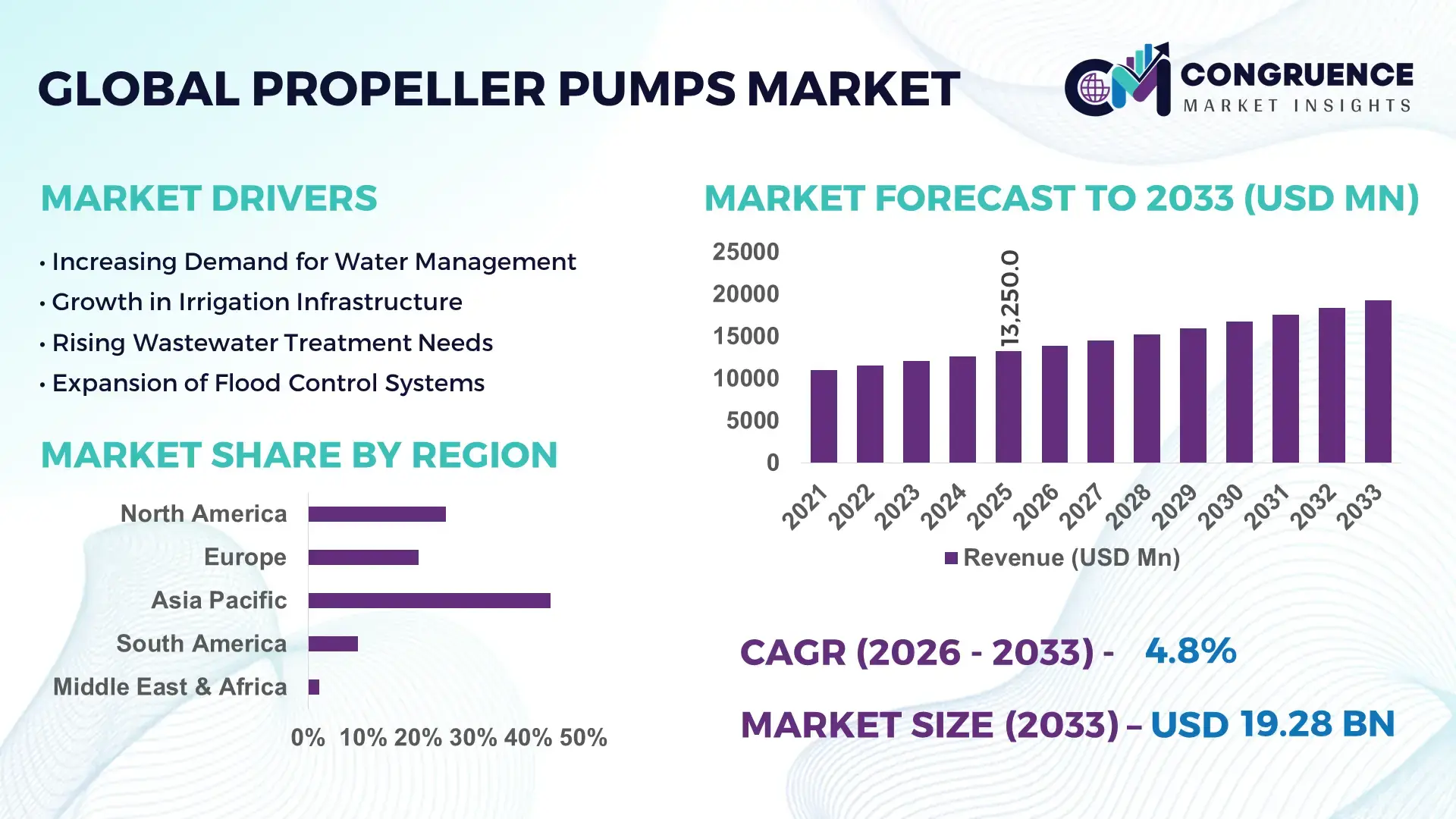

The Global Propeller Pumps Market was valued at USD 13250 Million in 2025 and is anticipated to reach a value of USD 19279.96 Million by 2033 expanding at a CAGR of 4.8% between 2026 and 2033.

Growth is being driven by the rapid modernization of irrigation infrastructure and wastewater management systems, where high-flow, low-head pumping solutions deliver up to 18% energy savings compared to conventional centrifugal alternatives. Between 2024 and 2026, tightening water-efficiency regulations and post-pandemic infrastructure stimulus programs across Asia and North America have accelerated procurement cycles and localized manufacturing strategies.

China dominates the global landscape with an estimated 32% production share, supported by large-scale agricultural irrigation projects and municipal flood control investments exceeding USD 8 billion annually. The country’s adoption of variable-speed propeller pump systems has increased by nearly 22% since 2023, driven by smart water grid integration. In comparison, the United States holds approximately 18% market share, focusing on advanced flood mitigation systems and industrial water recycling, while India contributes close to 11%, fueled by government-backed irrigation expansion and rural electrification programs. China’s manufacturing capacity surpasses India’s by nearly 2.5x, enabling faster deployment cycles and cost efficiencies of 12–15%.

Strategically, market participants must prioritize energy-efficient designs and regional manufacturing alignment to capture infrastructure-led demand and maintain cost competitiveness.

Market Size & Growth: USD 13250M (2025) to USD 19279.96M (2033) at 4.8%, driven by 18% efficiency gains from advanced axial-flow pump systems.

Top Growth Drivers: Irrigation demand (+21%), wastewater infrastructure (+17%), energy-efficient retrofits (+14%).

Short-Term Forecast: By 2027, operational costs decline by 12% due to smart motor integration and optimized flow control.

Emerging Technologies: AI-enabled monitoring, variable frequency drives, and corrosion-resistant composite materials improving lifespan by 20%.

Regional Leaders: Asia-Pacific (~USD 8.5B) with irrigation expansion, North America (~USD 4.2B) with flood control upgrades, Europe (~USD 3.6B) driven by wastewater reuse mandates.

Consumer/End-User Trends: Over 38% of municipal utilities shifting toward energy-efficient pumping systems for long-term cost savings.

Pilot/Case Example: 2025 Southeast Asia irrigation project improved water distribution efficiency by 26% using smart propeller pumps.

Competitive Landscape: Top players hold ~35% combined share; key companies include Xylem, KSB, Sulzer, Flowserve, and Ebara.

Regulatory & ESG Impact: Energy compliance standards reduced power consumption by 15% across new installations globally.

Investment & Funding: Over USD 2.4B invested in water infrastructure upgrades, with strong public-private partnerships post-2024.

Innovation & Future Outlook: Shift toward IoT-integrated pumping systems and modular designs enabling 25% faster deployment in high-growth regions.

Agriculture accounts for approximately 46% of total demand, followed by municipal wastewater at 34% and industrial applications at 20%, reflecting the dominance of water-intensive sectors. Recent innovations include composite propeller blades improving durability by 19% and smart monitoring systems enhancing uptime by 15%. Asia-Pacific leads demand with over 48% share, supported by infrastructure expansion, while Europe advances through strict water reuse mandates. A key emerging trend is the integration of digital twins for predictive maintenance, especially amid ongoing global supply chain restructuring. This evolution positions the market for more resilient, data-driven operational strategies.

Propeller pumps are rapidly becoming critical infrastructure assets as global water systems shift toward high-volume, energy-optimized flow management. Governments and utilities are accelerating investments in flood control, irrigation, and wastewater reuse, where axial-flow efficiency directly impacts operational economics. The market is transforming under pressure from stricter water-efficiency mandates and localized supply chain restructuring, forcing manufacturers to align production closer to demand centers and reduce lead times by over 15%.

Advanced variable-speed propeller systems outperform fixed-speed legacy units, where smart VFD-enabled pumps improve efficiency by 20% while reducing lifecycle cost by 14% compared to conventional centrifugal systems. Asia-Pacific leads in volume with over 48% deployment share, while Europe leads in innovation adoption with nearly 27% of installations integrating digital monitoring and predictive maintenance. Over the next 2–3 years, energy consumption per cubic meter pumped is expected to decline by 10–12%, driven by automation and real-time optimization. ESG alignment is emerging as a competitive advantage, with energy-efficient systems lowering carbon emissions by 16%, unlocking regulatory incentives and faster project approvals.

A 2025 flood control project in Southeast Asia demonstrated a 24% improvement in water discharge efficiency using smart propeller pumps, highlighting immediate ROI potential. Leading manufacturers are shifting capital toward modular designs and regional assembly hubs, increasing responsiveness by 18%. The strategic path forward is clear: companies that optimize efficiency, localize production, and integrate digital intelligence will secure long-term competitive dominance in a rapidly accelerating infrastructure-driven market.

Global infrastructure modernization is forcing a structural shift toward high-capacity, energy-efficient water movement systems. Irrigation expansion programs and urban flood control investments have increased demand for axial-flow pumps by over 19% since 2023. Simultaneously, energy cost pressures are pushing utilities to adopt systems that reduce consumption by 15–18%, directly improving operating margins. A key global trigger is the post-2024 public infrastructure push across Asia and North America, where water resilience has become a national priority. This demand surge is driving manufacturers to expand production capacity by nearly 22% and accelerate partnerships with engineering firms for turnkey solutions. The cause is clear: rising water demand and climate variability → need for efficient flow systems → aggressive procurement cycles. In response, companies are investing in localized assembly, scaling digital integration capabilities, and forming EPC collaborations to secure long-term contracts and strengthen competitive positioning.

The market faces significant constraints from raw material price volatility and supply concentration risks. Stainless steel and specialized alloys used in propeller systems have experienced price fluctuations of 18–25% over the past two years, directly impacting production costs. Additionally, over 60% of critical components are sourced from limited supplier clusters in East Asia, creating exposure to geopolitical disruptions and logistics delays. These constraints are increasing project lead times by up to 20% and reducing pricing flexibility for manufacturers. Infrastructure gaps in developing regions further limit large-scale deployment, particularly where grid reliability and maintenance capabilities remain inconsistent. To mitigate these risks, companies are diversifying supplier networks, locking in long-term procurement contracts, and exploring alternative composite materials that reduce dependency on metals by nearly 12%. This shift reflects a strategic balancing act between cost control and supply chain resilience.

Emerging opportunities are centered around smart water management systems and untapped rural irrigation markets. Digital integration, including IoT-enabled monitoring, is improving operational efficiency by up to 21% while reducing downtime by 17%, creating a strong value proposition for utilities. Africa and Southeast Asia are becoming high-growth regions, with irrigation infrastructure investments rising by over 23%, opening new demand channels. A key innovation shift is the development of composite propeller blades and modular pump architectures, enabling 20% faster deployment and lower lifecycle costs. Non-obvious upside lies in retrofitting aging infrastructure, where upgrading existing systems can deliver efficiency gains of 15% without full replacement. Companies are positioning for dominance by increasing R&D spending, expanding into emerging markets, and building ecosystem partnerships with digital solution providers. This strategic alignment is transforming the market from hardware-driven to solution-oriented competition.

Execution challenges are intensifying as projects scale in complexity and geographic diversity. Installation and maintenance inefficiencies can reduce system performance by up to 13%, particularly in regions lacking skilled technical labor. Grid instability and inconsistent power supply in developing markets further constrain performance reliability, impacting up to 28% of installations. Additionally, regulatory fragmentation across regions increases compliance costs by nearly 10%, complicating global expansion strategies. A real-world pressure point is the increasing demand for rapid deployment in climate-sensitive zones, where delays directly translate into economic and environmental losses. These challenges threaten long-term scalability and consistency of returns. To remain competitive, companies must invest in training programs, develop standardized modular systems, and strengthen after-sales service networks. Strategic partnerships with local contractors and digital monitoring integration are becoming essential to ensure performance optimization and sustain growth momentum.

The propeller pumps market is segmented by type, application, and end-user, with demand concentrated in high-flow, low-head water movement scenarios. Vertical and submersible configurations dominate installations due to scalability and operational efficiency, while mixed flow variants serve niche hybrid requirements. Irrigation and municipal water management collectively account for over 60% of demand, reflecting infrastructure-driven deployment patterns. Demand is shifting toward wastewater treatment and industrial circulation, where efficiency optimization and regulatory compliance are becoming critical. End-user concentration remains highest in agriculture and municipal sectors, but industrial and infrastructure segments are accelerating adoption due to modernization initiatives. This segmentation highlights a clear transition from volume-driven demand to efficiency-driven procurement, forcing companies to realign product strategies and target high-value applications.

Vertical Propeller Pumps dominate the market with approximately 38% share, driven by their superior performance in large-scale irrigation and flood control systems where high discharge capacity and vertical installation optimize space utilization. Submersible Propeller Pumps are the fastest-growing segment, expanding at nearly 21% in adoption, supported by increasing demand for compact, low-maintenance solutions in wastewater and urban drainage systems. Compared to vertical systems, submersible pumps reduce installation complexity by 25% and maintenance costs by 18%, accelerating their deployment in space-constrained environments.

Horizontal Propeller Pumps and Mixed Flow Pumps collectively account for around 41% of the market, serving specialized applications where horizontal alignment or combined radial-axial flow is required. While horizontal pumps remain relevant in industrial setups, mixed flow variants are gaining traction for hybrid use cases requiring moderate head and flow balance. Companies are responding by expanding submersible product lines and investing in modular vertical systems to capture both large-scale infrastructure and compact urban demand. The strategic implication is clear: investment is shifting toward flexible, low-maintenance designs that align with evolving infrastructure needs.

Irrigation remains the leading application, contributing approximately 36% of total demand due to large-scale agricultural dependency on high-volume water movement. Wastewater Treatment is the fastest-growing segment, with adoption increasing by nearly 23%, driven by stricter environmental regulations and the need for efficient water reuse systems. Compared to irrigation, which is volume-driven, wastewater applications are efficiency-driven, requiring advanced monitoring and energy optimization capabilities.

Flood Control and Water Supply together account for around 44% of the market, reflecting ongoing investments in urban infrastructure and climate resilience projects. Industrial Water Circulation, while smaller in share, is gaining importance due to rising demand for process optimization and cooling efficiency in manufacturing sectors. Companies are adapting by developing application-specific pump configurations and integrating digital monitoring to meet performance requirements. The business implication is a clear shift toward high-efficiency, regulation-driven applications, where value-added features are becoming critical for competitive differentiation.

Agriculture leads the market with approximately 40% share, driven by extensive irrigation requirements and government-backed rural infrastructure programs. Water Utilities are the fastest-growing end-user segment, with adoption increasing by 24%, fueled by modernization of urban water distribution and wastewater systems. Compared to agriculture’s volume-centric demand, utilities prioritize efficiency, reliability, and digital integration, creating a shift in product requirements.

Municipal and Infrastructure segments collectively account for around 37% of demand, supported by flood control and urban drainage investments. Industrial users, while representing a smaller share, are increasing adoption due to the need for efficient water circulation in manufacturing processes. Companies are targeting these segments through customized solutions, flexible pricing models, and strategic partnerships with EPC contractors. The business implication is a transition from bulk procurement to performance-driven purchasing, where long-term efficiency and reliability determine buying decisions.

Asia-Pacific accounted for the largest market share at 48% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 6.1% between 2026 and 2033.

Asia-Pacific dominates due to large-scale irrigation and flood control demand, while North America holds around 22% share driven by advanced infrastructure upgrades and digital pump integration. Europe contributes nearly 18%, leading in energy-efficient retrofitting with over 26% of systems upgraded to meet strict water reuse mandates. Meanwhile, Middle East & Africa, with ~7% share, is accelerating through infrastructure investments and water security programs, supported by over 30% growth in desalination-linked pumping systems. A key structural shift is the global push toward localized manufacturing, reducing supply chain risk and cutting delivery timelines by 15%. Strategically, companies are prioritizing Asia-Pacific for scale, Europe for innovation, and emerging regions for expansion-driven growth.

How are advanced infrastructure upgrades redefining high-efficiency water movement systems?

North America accounts for approximately 22% of global demand, driven by large-scale flood control, wastewater modernization, and industrial water recycling. Regulatory pressure to reduce energy consumption by 15% is accelerating the shift toward high-efficiency propeller pumps integrated with digital monitoring. A key structural force is federal infrastructure funding programs, which have increased project pipelines by nearly 18% since 2024. Utilities are adopting IoT-enabled systems, improving operational uptime by 16%. Companies are expanding regional manufacturing and service capabilities, with capacity investments rising by 12%. Buyers prioritize lifecycle efficiency over upfront cost, favoring advanced systems. The region remains a strategic investment hub due to its focus on performance optimization and long-term infrastructure resilience.

What is driving compliance-led transformation in energy-efficient pumping solutions?

Europe represents nearly 18% of the global market, with strong demand from countries such as Germany, France, and the Netherlands. Stringent ESG regulations and water reuse mandates are forcing adoption of energy-efficient systems, reducing energy consumption by up to 17%. Over 26% of installations now incorporate smart monitoring to meet compliance standards. This regulatory environment is driving a shift toward premium, high-performance pump systems. Companies are investing in advanced materials and digital integration to align with sustainability goals, with R&D spending increasing by 14%. Buyers exhibit compliance-first behavior, prioritizing certified, long-lifecycle solutions. The region compels continuous innovation, making it a benchmark for efficiency-driven product development and regulatory alignment.

Why is high-volume deployment accelerating large-scale water infrastructure transformation?

Asia-Pacific leads global demand with approximately 48% share, anchored by China and India, where irrigation and flood control projects dominate. The region benefits from strong manufacturing capacity, producing over 55% of global propeller pump units. Rapid infrastructure expansion is driving adoption, with deployment rates increasing by 27% since 2024. Localized production reduces costs by 14% and shortens delivery cycles significantly. Governments are scaling smart water management systems, pushing digital adoption to nearly 20% of new installations. Enterprises prioritize cost-efficiency and rapid deployment, favoring scalable solutions. This region is critical for volume growth and manufacturing scale, making it central to global expansion strategies.

How are infrastructure gaps and agricultural demand shaping adoption patterns?

South America holds approximately 9% of the global market, with Brazil and Argentina leading demand due to extensive agricultural irrigation needs. Irrigation accounts for over 45% of regional usage, driving steady demand for high-capacity pumps. However, infrastructure limitations and economic volatility increase project delays by up to 18%. Adoption is shifting toward cost-effective and durable systems, with low-maintenance pumps gaining traction by 16%. Companies are responding through localized partnerships and flexible pricing strategies to penetrate price-sensitive markets. Enterprises prioritize reliability and affordability over advanced features. This region presents a balanced opportunity—strong demand potential but constrained by infrastructure and financing challenges.

What is fueling rapid transformation in water infrastructure and resource management systems?

Middle East & Africa contributes around 7% of global demand, driven by water scarcity and large-scale infrastructure investments in countries such as Saudi Arabia and the UAE. Desalination and water transfer projects account for over 38% of pump usage, accelerating demand for high-efficiency systems. Strategic government investments have increased project activity by 30% since 2024. Adoption of advanced pumping technologies is rising, improving energy efficiency by 14%. Companies are entering partnerships with regional contractors to secure large infrastructure contracts. Buyers focus on reliability and long-term performance due to harsh operating conditions. The region is emerging as a high-growth, investment-driven market with strong long-term strategic importance.

China – 32% share in the Propeller Pumps Market, driven by large-scale manufacturing capacity and extensive irrigation and flood control infrastructure deployment.

United States – 18% share in the Propeller Pumps Market, supported by advanced wastewater management systems and strong investment in flood mitigation infrastructure.

The competitive landscape is defined by global engineering leaders such as Xylem, KSB, Sulzer, Flowserve, and Ebara competing against regional manufacturers and cost-focused suppliers. The top five players collectively hold approximately 35% market share, creating a semi-consolidated structure where global firms dominate high-value projects while regional players compete on price and delivery speed. Competition is primarily based on technology differentiation, cost efficiency, and supply chain responsiveness, with advanced systems delivering up to 18% higher efficiency and 12% lower lifecycle costs.

Companies are actively expanding regional manufacturing footprints, forming EPC partnerships, and investing in digital monitoring capabilities to strengthen market position. A key competitive shift is the move toward integrated solutions combining hardware with predictive maintenance services, increasing customer retention by 15%. Entry barriers remain high due to capital-intensive manufacturing and technical expertise requirements. To win, companies must balance cost competitiveness with advanced technology integration while ensuring rapid deployment and localized support.

Xylem Inc.

KSB SE & Co. KGaA

Sulzer Ltd.

Flowserve Corporation

Ebara Corporation

Grundfos Holding A/S

Wilo SE

Torishima Pump Mfg. Co., Ltd.

Kirloskar Brothers Limited

ITT Inc.

Pentair plc

SPX Flow, Inc.

Advanced variable frequency drive (VFD) integration is redefining performance benchmarks, with over 44% of new installations now incorporating speed-controlled systems. These technologies improve energy efficiency by 18% and reduce operational costs by 12% through real-time flow optimization. Utilities are deploying sensor-based control systems to dynamically adjust pumping loads, directly enhancing reliability and reducing energy waste across large-scale irrigation and wastewater networks. Emerging technologies such as IoT-enabled monitoring and digital twin modeling are gaining rapid traction, with adoption reaching nearly 24% across municipal and industrial deployments. These systems reduce unplanned downtime by 17% and improve maintenance scheduling accuracy by 21%. Integration with cloud-based analytics platforms is enabling operators to shift from reactive to predictive maintenance, creating measurable gains in asset lifespan and operational continuity.

Composite material innovation is disrupting traditional metal-based pump designs. High-strength polymer and coated alloy propellers improve corrosion resistance by 20% while reducing weight by 15%, lowering installation complexity. Compared to legacy cast-iron systems, next-generation composite propeller pumps improve efficiency by 16% while reducing maintenance cost by 14%, making them increasingly preferred in harsh and saline environments.

Between 2026 and 2028, technology convergence—combining automation, materials engineering, and data analytics—will accelerate system-level optimization. Market leaders and engineering-focused firms benefit most, as integrated solutions increase customer retention by 15%. Immediate action is critical: companies investing in smart, efficient, and durable pump technologies are securing operational advantage and long-term contract positioning.

March 2026 – Xylem Inc. launched a next-generation smart propeller pump platform integrating AI-based monitoring, improving energy efficiency by 19% across municipal systems. This strengthens digital service revenue streams and enhances lifecycle value for utilities. [Digital Integration]

Source: https://www.xylem.com

November 2025 – Sulzer Ltd. expanded its manufacturing facility in Asia, increasing axial-flow pump production capacity by 22%. This move reduces delivery lead times and strengthens regional supply chain resilience amid rising infrastructure demand. [Capacity Expansion]

Source: https://www.sulzer.com

July 2025 – KSB SE & Co. KGaA introduced corrosion-resistant composite propeller technology, extending pump lifespan by 18% in wastewater applications. This innovation reduces maintenance cycles and improves operational uptime for industrial clients. [Material Innovation]

Source: https://www.ksb.com

January 2024 – Flowserve Corporation partnered with a global EPC contractor to deploy high-capacity propeller pumps in flood control projects, achieving 25% faster installation timelines. This collaboration enhances project execution efficiency and strengthens infrastructure project pipelines. [Strategic Partnership]

Source: https://www.flowserve.com

This report delivers a comprehensive analysis of the propeller pumps market across core segments including types (vertical, horizontal, submersible, mixed flow), applications (irrigation, flood control, water supply, wastewater treatment, industrial circulation), and end-users (agriculture, municipal, industrial, utilities, infrastructure). It evaluates demand across five key regions, covering over 20 country-level markets, while integrating insights on emerging technologies such as IoT-enabled monitoring, composite materials, and modular pump systems, with adoption levels exceeding 20% in advanced deployments.

The analytical depth includes evaluation of more than 15 segment combinations, supported by operational metrics such as efficiency gains of 15–20% and maintenance cost reductions of up to 18% across modern systems. The report profiles leading companies and tracks competitive positioning through technology adoption, regional expansion, and supply chain strategies. It highlights demand distribution patterns, with irrigation and municipal applications contributing over 60% of usage, while wastewater and industrial segments show rising adoption trends above 20%.

Strategically, the report supports investment prioritization, market entry decisions, and product development planning by identifying high-impact growth pockets and technology shifts. It also outlines forward-looking dynamics for 2026–2033, focusing on digital integration, energy optimization, and infrastructure-led demand transformation, enabling stakeholders to align with evolving market realities and secure competitive advantage.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 13250 Million |

|

Market Revenue in 2033 |

USD 19279.96 Million |

|

CAGR (2026 - 2033) |

4.8% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Xylem Inc., KSB SE & Co. KGaA, Sulzer Ltd., Flowserve Corporation, Ebara Corporation, Grundfos Holding A/S, Wilo SE, Torishima Pump Mfg. Co., Ltd., Kirloskar Brothers Limited, ITT Inc., Pentair plc, SPX Flow, Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |