Reports

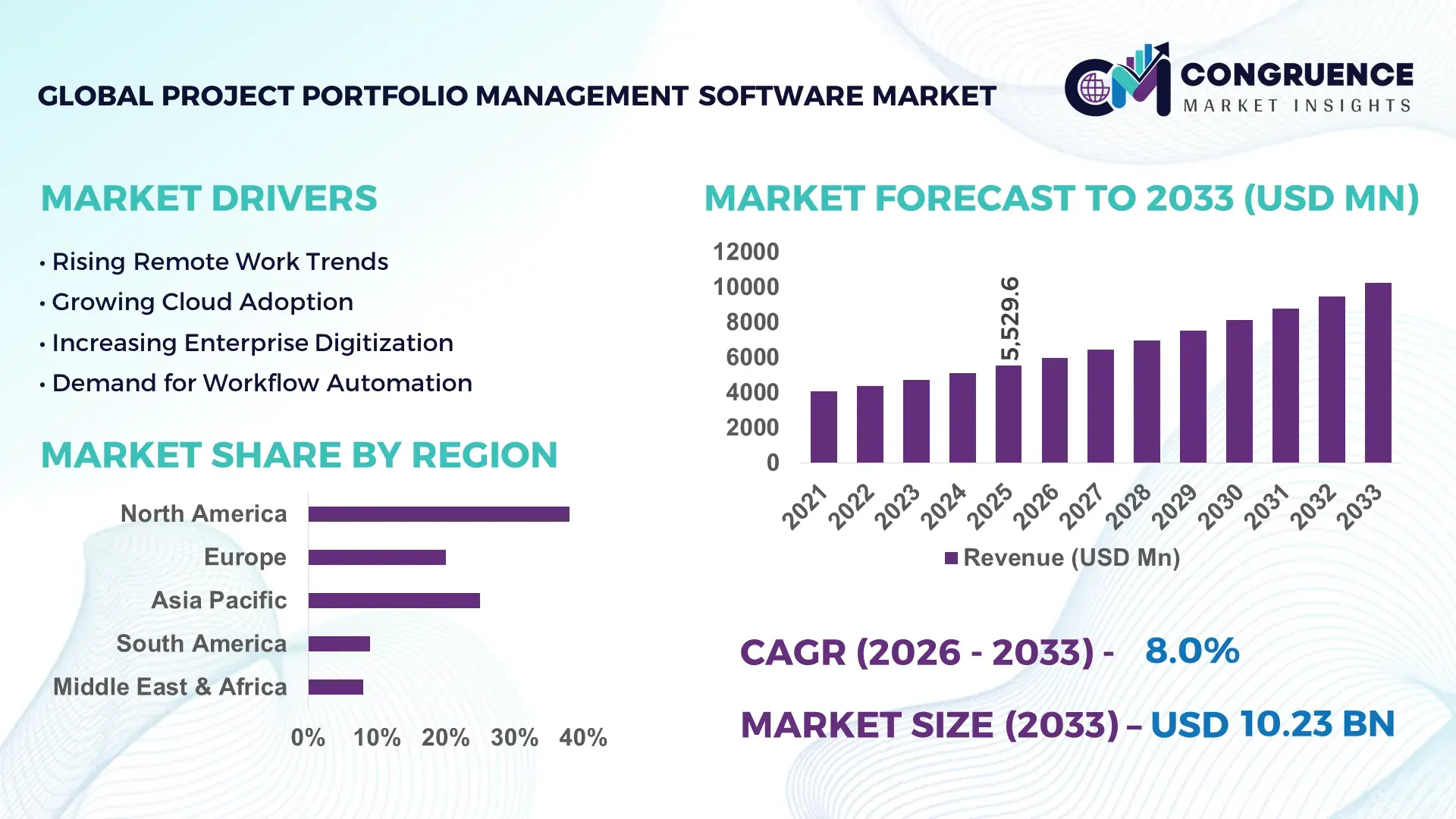

The Global Project Portfolio Management Software Market was valued at USD 5529.6 Million in 2025 and is anticipated to reach a value of USD 10234.9 Million by 2033 expanding at a CAGR of 8% between 2026 and 2033. Enterprise-wide migration toward AI-enabled portfolio governance, hybrid workforce coordination, and cloud-native resource optimization platforms accelerated software deployment across IT, construction, BFSI, and manufacturing sectors, with automated project prioritization reducing planning inefficiencies by nearly 28% in large organizations during 2025–2026.

The United States dominates the global Project Portfolio Management Software Market with nearly 34% market share, supported by strong enterprise SaaS spending, federal digital modernization programs, and large-scale adoption across technology, healthcare, aerospace, and financial services industries. More than 68% of Fortune 1000 enterprises integrated AI-assisted portfolio analytics into project governance frameworks by 2026, while enterprise cloud migration spending exceeded USD 210 billion across North America. Compared with traditional spreadsheet-based project tracking, advanced PPM platforms improved cross-functional resource utilization by over 31% and shortened project approval cycles by approximately 22%. Major investment concentration in enterprise automation hubs such as California, Texas, and New York further strengthened high-value software deployment and innovation scalability.

Market Size & Growth: USD 5529.6 Million in 2025 reaching USD 10234.9 Million by 2033 at 8% CAGR, driven by AI-enabled portfolio automation and enterprise cloud migration.

Top Growth Drivers: Cloud deployment adoption rose 42%, AI-based workflow optimization improved efficiency by 28%, and hybrid workforce management demand increased 33% globally.

Short-Term Forecast: By 2027, enterprises using advanced PPM platforms will reduce project overruns by 24% and improve resource allocation accuracy by 30%.

Emerging Technologies: AI forecasting, predictive analytics, and low-code automation platforms increased deployment efficiency by 26% across large enterprises in 2026.

Regional Leaders: North America exceeds USD 3.8 Billion with strong SaaS adoption, Europe advances through compliance-driven modernization, and Asia-Pacific records 11% enterprise deployment growth.

Consumer/End-User Trends: Over 64% of multinational enterprises shifted toward centralized portfolio dashboards to manage distributed operations and cross-border project execution.

Pilot/Case Example: In 2026, a global manufacturing enterprise reduced project delivery delays by 21% after integrating AI-driven portfolio prioritization tools across 14 business units.

Competitive Landscape: Leading vendors control nearly 38% market share, with competition centered around enterprise scalability, analytics depth, and workflow integration capabilities.

Regulatory & ESG Impact: ESG-linked project governance adoption increased 29% as enterprises aligned portfolio investments with sustainability disclosure and compliance mandates.

Investment & Funding: Enterprise software investment surpassed USD 18 Billion in 2025, fueled by strategic partnerships, automation expansion, and regional digital infrastructure programs.

Innovation & Future Outlook: Autonomous project orchestration, generative AI reporting, and real-time scenario simulation platforms are reshaping high-growth enterprise portfolio management strategies.

IT and enterprise services contribute nearly 36% of global Project Portfolio Management Software adoption, followed by construction and infrastructure projects at approximately 24%, driven by complex multi-site execution requirements. AI-powered workload balancing, predictive budgeting, and integrated risk analytics improved project visibility by over 27% during 2026 deployments. North America leads high-value enterprise integration, while Asia-Pacific records the fastest implementation growth due to rapid digital infrastructure expansion and manufacturing modernization. Rising compliance-focused investment governance and supply chain volatility are accelerating demand for centralized portfolio intelligence platforms, positioning advanced automation-led PPM ecosystems as a core strategic priority for global enterprises.

Project Portfolio Management Software is transforming from an operational support tool into a board-level strategic control system as enterprises intensify focus on capital efficiency, execution visibility, and AI-driven decision intelligence. Global organizations managing multi-region operations reduced project failure rates by nearly 26% after deploying integrated portfolio governance platforms during 2025–2026. Rising pressure from fragmented supply chains, stricter compliance oversight, and accelerated digital infrastructure investment is forcing enterprises to centralize portfolio execution and resource allocation. AI-powered predictive portfolio systems improve planning efficiency by 34% while reducing operational coordination costs by 21% compared to legacy spreadsheet-based systems, reshaping enterprise competitiveness across technology, manufacturing, healthcare, and infrastructure sectors.

North America leads in deployment volume due to high enterprise SaaS penetration, while Asia-Pacific leads in adoption acceleration with enterprise implementation rates increasing by 18% across manufacturing and construction ecosystems. Over the next three years, enterprises integrating real-time analytics and automated risk prioritization are expected to shorten project delivery cycles by 24% and improve budget adherence by 29%. ESG-linked portfolio governance has emerged as a measurable competitive advantage, reducing compliance management costs by 17% while improving procurement transparency and investor reporting efficiency across regulated industries.

In 2026, a multinational engineering firm deploying AI-enabled portfolio orchestration across 11 global divisions improved resource utilization by 31% and reduced inactive project backlog by 22% within twelve months. Enterprise software vendors are rapidly shifting capital allocation toward generative AI reporting engines, low-code integration frameworks, and predictive scenario modeling capabilities to secure long-term enterprise contracts. Companies optimizing cross-functional visibility, autonomous project governance, and sustainability-aligned investment planning are strengthening strategic resilience and positioning themselves ahead of competitors in the next phase of enterprise transformation.

Rapid enterprise digitization and rising project complexity are accelerating adoption of advanced Project Portfolio Management Software across global industries. More than 67% of large enterprises shifted toward centralized portfolio visibility platforms during 2025–2026 to improve execution control and capital allocation accuracy. AI-enabled forecasting tools reduced project scheduling conflicts by 28%, while automated resource optimization improved workforce utilization by 24% across multinational organizations. Ongoing supply chain restructuring and geopolitical trade disruptions forced enterprises to strengthen real-time operational coordination across distributed teams and vendors. In response, software providers are accelerating cloud infrastructure expansion, forming strategic ERP integration partnerships, and increasing AI analytics investments to secure long-term enterprise contracts and strengthen competitive differentiation across high-growth digital transformation markets.

Complex enterprise integration environments and fragmented legacy infrastructure are constraining scalable deployment of Project Portfolio Management Software across highly regulated industries. Nearly 41% of enterprises reported interoperability issues between existing ERP, HR, and financial systems during 2025 implementations, while migration-related deployment costs increased by 19% in multi-region operations. Rising cybersecurity compliance obligations and stricter cross-border data governance regulations are further delaying cloud-based portfolio integration strategies, particularly in finance and healthcare sectors. Limited internal digital expertise continues to extend implementation timelines and reduce platform optimization efficiency. To mitigate these risks, companies are diversifying cloud deployment models, expanding cybersecurity investments, and pursuing low-code integration partnerships to improve interoperability, accelerate onboarding, and reduce operational disruption across enterprise project ecosystems.

Predictive analytics, generative AI automation, and autonomous workflow orchestration are redefining competitive positioning in the Project Portfolio Management Software Market. Enterprises deploying AI-driven portfolio intelligence platforms improved decision-making speed by 32% and reduced budget forecasting errors by 23% during 2026 operational cycles. Emerging demand across Asia-Pacific, the Middle East, and industrial digitalization corridors is accelerating cloud-native PPM deployment in infrastructure, energy, and manufacturing sectors. A major innovation shift toward scenario-based planning engines and ESG-linked investment tracking is creating high-value enterprise demand beyond traditional project management functions. In response, leading vendors are expanding AI research programs, strengthening ecosystem partnerships, and building industry-specific analytics modules to secure long-term strategic differentiation and capture fast-growing enterprise transformation opportunities globally.

Scaling enterprise-wide Project Portfolio Management Software deployments remains challenging due to infrastructure fragmentation, inconsistent data quality, and workforce adaptation gaps. Approximately 38% of enterprises experienced delayed ROI realization during large-scale digital transformation programs because of poor cross-platform synchronization and limited user adoption efficiency. Increasing cloud infrastructure costs and rising AI processing demands elevated operational software management expenses by nearly 16% during 2026. Regulatory pressure surrounding data sovereignty and cybersecurity resilience is also forcing multinational organizations to redesign deployment architectures across multiple jurisdictions. Companies failing to modernize governance frameworks, workforce training systems, and interoperability capabilities risk reduced scalability and slower innovation execution. To remain competitive, vendors are prioritizing modular platform architecture, strategic hyperscaler alliances, and automation-focused product innovation investments.

AI-assisted workflow orchestration adoption increased 37% across enterprise deployments in 2026, reshaping operational execution models. Organizations are integrating predictive scheduling, automated budget alerts, and generative reporting into centralized PPM environments to reduce manual coordination workloads. AI-driven prioritization tools shortened project approval cycles by 23% while improving cross-team productivity by 19%. Software vendors are rapidly restructuring product architectures around embedded analytics and low-code automation to optimize enterprise scalability and reduce implementation friction.

Cloud-to-hybrid deployment transitions expanded 29% as enterprises tightened data governance and regional compliance control. Large financial and healthcare organizations are shifting sensitive project data toward hybrid infrastructure models following stricter cross-border regulatory oversight and rising cybersecurity pressure. Hybrid deployment environments reduced compliance-related operational disruptions by 18% while improving infrastructure flexibility across distributed operations. Vendors are responding through strategic hyperscaler partnerships, localized hosting expansion, and industry-specific compliance modules to capture regulated enterprise demand.

Asia-Pacific enterprise onboarding volumes climbed 33%, redefining regional implementation priorities across manufacturing and infrastructure sectors. Accelerated industrial digitalization and workforce decentralization are forcing organizations to standardize multi-site project coordination through integrated portfolio platforms. Unlike mature North American markets focused on optimization, Asia-Pacific enterprises are prioritizing rapid deployment scalability and mobile accessibility. Companies are increasing regional integration support teams and expanding cloud-native deployment frameworks to address faster implementation cycles and localized operational requirements.

Subscription-based consumption models accounted for 61% of new enterprise contracts, shifting software monetization and procurement behavior. Enterprises are replacing long-term perpetual licensing structures with modular, usage-based pricing to improve capital allocation flexibility during ongoing supply chain volatility. This transition reduced upfront deployment costs by 26% and accelerated implementation speed by 21%. Providers are optimizing recurring-service ecosystems, bundled analytics offerings, and managed integration services to strengthen retention rates and stabilize long-term enterprise relationships.

The Project Portfolio Management Software Market is segmented by type, application, and end-user, with cloud-based and AI-enabled platforms dominating enterprise deployment due to scalability and automation advantages. Resource management and workflow automation collectively account for over 44% of application demand as organizations prioritize operational visibility and execution speed. IT and telecom remain the largest end-user segment with nearly 31% share, while healthcare and construction are rapidly increasing adoption through compliance-driven digital coordination initiatives. Demand is shifting toward hybrid deployment and predictive analytics capabilities as enterprises optimize distributed workforce management, regulatory reporting, and multi-project governance across increasingly complex operational ecosystems.

Cloud-Based deployment dominates the Project Portfolio Management Software Market with nearly 46% share due to lower infrastructure dependency, faster scalability, and seamless integration with enterprise collaboration ecosystems. Large organizations are prioritizing cloud-native deployment to optimize distributed workforce coordination and reduce implementation timelines by approximately 24% compared to traditional infrastructure-heavy models. AI-Enabled Platforms represent the fastest-growing segment, with adoption increasing by nearly 31% during 2025–2026 as enterprises accelerate predictive analytics integration, automated portfolio prioritization, and real-time risk forecasting capabilities. Compared with On-Premises systems, AI-enabled cloud platforms improve resource allocation efficiency by 28% while reducing operational administration costs by 19%.

Hybrid Deployment models are gaining strategic traction across regulated sectors, particularly BFSI and healthcare, where compliance-driven data localization requirements remain critical. Mobile-Based Solutions and On-Premises systems collectively account for approximately 29% of market demand, serving field-intensive operations and high-security enterprise environments. Vendors are increasingly shifting product development toward AI-integrated cloud ecosystems, low-code interoperability frameworks, and mobile-responsive dashboards to capture enterprise modernization spending. Investment momentum is concentrating around scalable automation-centric platforms, while legacy standalone deployment structures continue losing competitive relevance across high-volume enterprise environments.

“According to a 2025 report by the Project Management Institute, cloud-based project portfolio management platforms were adopted by over 69% of enterprise organizations, resulting in nearly 27% improvement in cross-functional project efficiency and resource visibility, reinforcing their growing strategic importance.”

Resource Management leads the Project Portfolio Management Software Market with approximately 27% share as enterprises prioritize workforce optimization, utilization balancing, and multi-project coordination across distributed operational environments. Organizations deploying advanced resource allocation engines improved labor productivity by nearly 22% while reducing scheduling conflicts by 18% during 2026 implementation cycles. Workflow Automation is the fastest-growing application segment, expanding by approximately 34% due to increasing enterprise demand for AI-assisted approvals, automated reporting, and process standardization across large-scale transformation programs. Compared with traditional Project Scheduling tools, workflow automation platforms reduce manual intervention requirements by 31% and accelerate execution visibility across cross-functional teams.

Budget Management and Portfolio Analysis collectively represent around 33% of market demand as organizations intensify focus on capital governance, predictive forecasting, and investment prioritization amid tighter operational spending controls. Risk Management applications are also gaining traction across regulated industries responding to cybersecurity, compliance, and supply chain disruption pressures. Software providers are expanding embedded analytics capabilities, real-time monitoring frameworks, and automation-centric deployment models to strengthen enterprise retention and operational scalability. Demand is decisively shifting toward intelligent execution systems capable of integrating financial, operational, and strategic project oversight into centralized portfolio environments.

“According to a 2025 report by the International Institute of Business Analysis, workflow automation solutions were deployed across over 58,000 enterprise organizations, improving operational processing speed by 33%, highlighting rapid operational adoption across complex project environments.”

IT and Telecom dominates the Project Portfolio Management Software Market with nearly 31% share due to continuous digital transformation initiatives, large-scale software deployment cycles, and high dependency on agile project coordination frameworks. Enterprises within this sector improved cross-team delivery efficiency by approximately 26% after integrating centralized portfolio intelligence systems during 2026. Healthcare represents the fastest-growing end-user segment, with adoption rates increasing by nearly 29% as hospitals and healthcare networks strengthen compliance-driven operational coordination, infrastructure modernization, and digital patient management initiatives. Compared with Manufacturing organizations focused on production optimization, healthcare institutions prioritize regulatory reporting, resource visibility, and secure multi-department collaboration capabilities.

BFSI, Government, Construction, and Manufacturing collectively account for approximately 52% of total demand, driven by rising investment governance requirements, infrastructure modernization programs, and multi-vendor project complexity. Construction enterprises are rapidly adopting mobile-integrated portfolio systems to improve field coordination and reduce project delays linked to labor shortages and supply chain disruptions. Vendors are responding through sector-specific customization strategies, subscription-based pricing models, and strategic integration partnerships tailored to operational workflows. Future demand concentration is shifting toward regulated and infrastructure-intensive industries requiring scalable governance, predictive analytics, and compliance-focused execution platforms.

“According to a 2025 report by the Information Systems Audit and Control Association, adoption among healthcare organizations increased by 28%, with over 21,000 institutions implementing centralized portfolio management solutions, leading to 24% improvement in operational coordination efficiency, indicating a strong shift in demand dynamics.”

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.4% between 2026 and 2033.

North America leads in enterprise-scale deployment and AI-integrated portfolio governance adoption, supported by strong SaaS infrastructure and high digital transformation spending across IT, BFSI, and healthcare sectors. Europe holds nearly 27% share, driven by compliance-focused modernization and ESG-linked operational governance requirements. Asia-Pacific accounts for approximately 24% of global demand but is accelerating rapidly due to infrastructure expansion, manufacturing digitalization, and rising cloud deployment across India, China, and Southeast Asia. Meanwhile, Middle East investments in smart city and industrial diversification projects are increasing enterprise PPM integration demand. Ongoing supply chain regionalization and stricter cross-border data governance are reshaping deployment priorities globally. Companies are increasingly focusing expansion strategies on high-growth Asia-Pacific markets while maintaining innovation and enterprise retention leadership in North America and Europe.

North America commands nearly 38% of global Project Portfolio Management Software demand, driven by large enterprise digital transformation programs and high SaaS penetration across technology, healthcare, and financial services industries. More than 66% of Fortune 1000 companies integrated AI-assisted portfolio analytics into operational governance frameworks during 2026. Rising cybersecurity compliance requirements and increasing pressure to optimize distributed workforce productivity are accelerating migration toward centralized cloud-native PPM ecosystems. Enterprises reduced project execution delays by approximately 24% after deploying predictive resource allocation systems across multi-region operations. Software providers are expanding AI automation partnerships and industry-specific integration capabilities to strengthen enterprise retention. Organizations across the region prioritize scalability, analytics depth, and interoperability, making North America the leading investment destination for advanced enterprise portfolio intelligence platforms.

Europe represents approximately 27% of the global Project Portfolio Management Software Market, with Germany, the United Kingdom, and France leading enterprise deployment activity across manufacturing, BFSI, and public infrastructure sectors. Stringent ESG disclosure frameworks, cross-border data governance regulations, and sustainability-linked operational mandates are forcing organizations to strengthen centralized project oversight and compliance tracking capabilities. More than 48% of large enterprises adopted hybrid deployment architectures during 2026 to align with evolving regional data localization requirements. AI-enabled workflow automation reduced compliance reporting workloads by nearly 21% across regulated industries. Enterprises across Europe prioritize secure interoperability, operational transparency, and long-term efficiency optimization, prompting software vendors to accelerate localized cloud infrastructure investments and compliance-focused product innovation strategies throughout the region.

Asia-Pacific ranks as the fastest-expanding Project Portfolio Management Software Market, accounting for nearly 24% of global demand with strong acceleration across China, India, Japan, and Southeast Asia. Rapid infrastructure expansion, manufacturing digitalization, and large-scale enterprise cloud adoption are reshaping regional project execution models. Enterprise implementation volumes increased by approximately 33% during 2025–2026 as organizations prioritized centralized coordination across distributed operations and supplier ecosystems. Manufacturing and construction enterprises improved multi-site resource visibility by nearly 26% after integrating mobile-enabled portfolio platforms. Regional businesses favor scalable, cost-efficient deployment frameworks with faster onboarding cycles and localized integration support. Software providers are aggressively expanding regional delivery centers, cloud partnerships, and AI-enabled operational analytics capabilities to capture accelerating enterprise modernization demand across Asia-Pacific.

South America contributes nearly 6% of global Project Portfolio Management Software demand, with Brazil and Chile leading enterprise deployment across infrastructure, mining, financial services, and energy sectors. Increasing demand for centralized project coordination and operational transparency is accelerating adoption among mid-sized enterprises managing complex multi-vendor operations. However, limited cloud infrastructure maturity and elevated implementation costs continue constraining large-scale deployment scalability across several regional markets. During 2026, subscription-based PPM adoption increased by approximately 22% as enterprises shifted toward lower upfront investment models to manage economic volatility. Organizations increasingly prioritize modular deployment flexibility, localized service support, and mobile accessibility to optimize workforce coordination. The region presents strong expansion potential for vendors capable of balancing affordability, scalability, and localized integration capabilities effectively.

Middle East & Africa accounts for approximately 5% of the global Project Portfolio Management Software Market, driven by accelerating infrastructure modernization and large-scale industrial diversification programs across the UAE, Saudi Arabia, and South Africa. Construction, oil and gas, transportation, and smart city initiatives are increasing demand for centralized portfolio governance and real-time project monitoring systems. Enterprise deployment activity rose nearly 19% during 2026 as organizations strengthened digital oversight across multi-billion-dollar infrastructure ecosystems. Government-backed modernization programs and public-private technology partnerships are accelerating adoption of AI-enabled scheduling and workflow automation platforms. Enterprises prioritize operational visibility, mobile integration, and scalable cloud deployment to manage geographically distributed projects efficiently. Vendors investing in regional integration support and compliance-focused customization are gaining stronger competitive positioning across emerging transformation-driven markets.

United States – 34% market share in the Project Portfolio Management Software Market, supported by strong enterprise SaaS adoption, advanced AI integration, and large-scale digital transformation investments across IT, healthcare, and BFSI sectors.

China – 16% market share in the Project Portfolio Management Software Market, driven by rapid infrastructure expansion, manufacturing digitalization, and accelerating enterprise cloud deployment across industrial and public-sector operations.

The Project Portfolio Management Software Market is dominated by global enterprise software leaders competing against agile cloud-native platform providers and AI-focused workflow automation specialists. Microsoft, Oracle, SAP, Atlassian, and ServiceNow collectively control nearly 44% of global market influence through enterprise integration depth, AI analytics capability, and large-scale ecosystem compatibility. Competition is increasingly centered on automation intelligence, deployment speed, interoperability, and industry-specific customization rather than pricing alone. AI-enabled platforms improved enterprise resource optimization efficiency by approximately 28%, while low-code integration frameworks reduced deployment timelines by nearly 24%, intensifying technology-led competition. Leading vendors are accelerating strategic acquisitions, hyperscaler partnerships, and vertical-specific product expansion to secure long-term enterprise contracts. Regional players are targeting mid-market demand through subscription flexibility and localized deployment support. Rising cybersecurity compliance pressure and integration complexity remain major entry barriers. Companies succeeding in this market are those delivering scalable AI-driven orchestration, seamless interoperability, and measurable operational efficiency gains.

Microsoft Corporation

Oracle Corporation

SAP SE

Atlassian Corporation

ServiceNow Inc.

Planview Inc.

Broadcom Inc.

Smartsheet Inc.

Monday.com Ltd.

Asana Inc.

Adobe Inc.

Workfront Inc.

Celoxis Technologies Pvt. Ltd.

Wrike Inc.

AI-driven portfolio intelligence platforms are redefining enterprise project execution through predictive scheduling, automated budgeting, and real-time resource optimization capabilities. By 2026, more than 62% of large enterprises integrated AI-assisted workflow engines into centralized PPM environments to reduce operational bottlenecks and improve decision speed. Predictive analytics tools improved project forecasting accuracy by nearly 29%, while automated resource balancing reduced scheduling inefficiencies by 24%. Enterprises deploying AI-enabled orchestration platforms gained measurable advantages in cross-functional coordination, compliance monitoring, and capital allocation visibility across distributed operations.

Cloud-native and hybrid deployment technologies are accelerating enterprise modernization as organizations prioritize scalability, interoperability, and regulatory compliance. Hybrid PPM architectures improved infrastructure flexibility by approximately 21% compared to legacy on-premises systems while lowering maintenance overhead by 18%. Mobile-integrated portfolio dashboards and low-code workflow automation platforms are also expanding rapidly across construction, healthcare, and manufacturing sectors, where distributed workforce management remains critical. Vendors are aggressively integrating ERP, CRM, and cybersecurity frameworks to optimize enterprise-wide operational synchronization and strengthen long-term platform retention.

Between 2026 and 2028, generative AI agents, autonomous project orchestration, and scenario-based simulation engines will become major competitive differentiators across enterprise software ecosystems. Compared with traditional spreadsheet-driven project governance, AI-native portfolio systems improve execution efficiency by nearly 34% while reducing coordination costs by 22%. Technology leaders investing in agentic automation, real-time analytics infrastructure, and embedded ESG tracking capabilities are securing faster enterprise adoption, stronger retention rates, and higher operational scalability in increasingly complex multi-project business environments.

March 2026 – monday.com launched Agentalent.ai, an enterprise AI-agent marketplace developed with AWS and Anthropic to automate operational workflows and project coordination. The platform supports AI agent qualification, onboarding, and execution management, while monday.com reported adoption across more than 250,000 customer organizations, accelerating enterprise automation deployment efficiency. [Agent Workforce Shift]

May 2026 – monday.com transformed its platform into an AI Work Platform with native AI agents integrated directly into enterprise workflows. The company disclosed that only 34% of enterprises were deeply using AI operationally, prompting deployment of integrated AI orchestration capabilities designed to improve enterprise execution scalability and workflow automation performance. [Native AI Execution]

January 2025 – ServiceNow entered a strategic partnership with SoftwareOne to strengthen AI-driven cloud modernization and workflow automation capabilities for enterprise project environments. The collaboration focused on optimizing software investment governance and accelerating enterprise digital transformation through integrated automation frameworks that improve operational visibility and deployment efficiency. [Cloud Governance Alliance]

May 2024 – Atlassian unified Jira Work Management and Jira Software into a consolidated Jira experience to simplify enterprise project coordination workflows. The transition eliminated separate product purchasing structures while streamlining collaboration, workflow tracking, and cross-functional operational management for enterprise users adopting centralized project execution environments. [Unified Workflow Integration]

This report delivers comprehensive analysis of the global Project Portfolio Management Software Market across deployment types, operational applications, enterprise end-users, and regional demand ecosystems. Coverage includes Cloud-Based, On-Premises, Hybrid Deployment, AI-Enabled Platforms, and Mobile-Based Solutions, alongside operational applications such as Resource Management, Workflow Automation, Risk Management, Portfolio Analysis, Budget Management, and Project Scheduling. The study evaluates demand dynamics across IT and Telecom, BFSI, Healthcare, Manufacturing, Government, and Construction industries spanning North America, Europe, Asia-Pacific, South America, and Middle East & Africa. AI-enabled platforms accounted for nearly 31% adoption acceleration during 2026, while workflow automation deployments improved enterprise execution efficiency by approximately 28%.

The report profiles major enterprise software providers, evaluates technology integration trends, and analyzes competitive positioning across cloud-native ecosystems, AI orchestration frameworks, and hybrid deployment environments. More than 60% of large organizations are prioritizing centralized portfolio intelligence and predictive analytics integration to strengthen operational governance and distributed workforce coordination. Strategic assessment extends through 2026–2033, covering emerging technologies including generative AI agents, autonomous workflow orchestration, ESG-linked portfolio governance, and low-code interoperability frameworks. The report supports investment planning, regional expansion strategy, product positioning, and enterprise modernization decisions through execution-level market intelligence and measurable operational insights.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 5529.6 Million |

|

Market Revenue in 2033 |

USD 10234.9 Million |

|

CAGR (2026 - 2033) |

8% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Microsoft Corporation, Oracle Corporation, SAP SE, Atlassian Corporation, ServiceNow Inc., Planview Inc., Broadcom Inc., Smartsheet Inc., Monday.com Ltd., Asana Inc., Adobe Inc., Workfront Inc., Celoxis Technologies Pvt. Ltd., Wrike Inc. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |