Reports

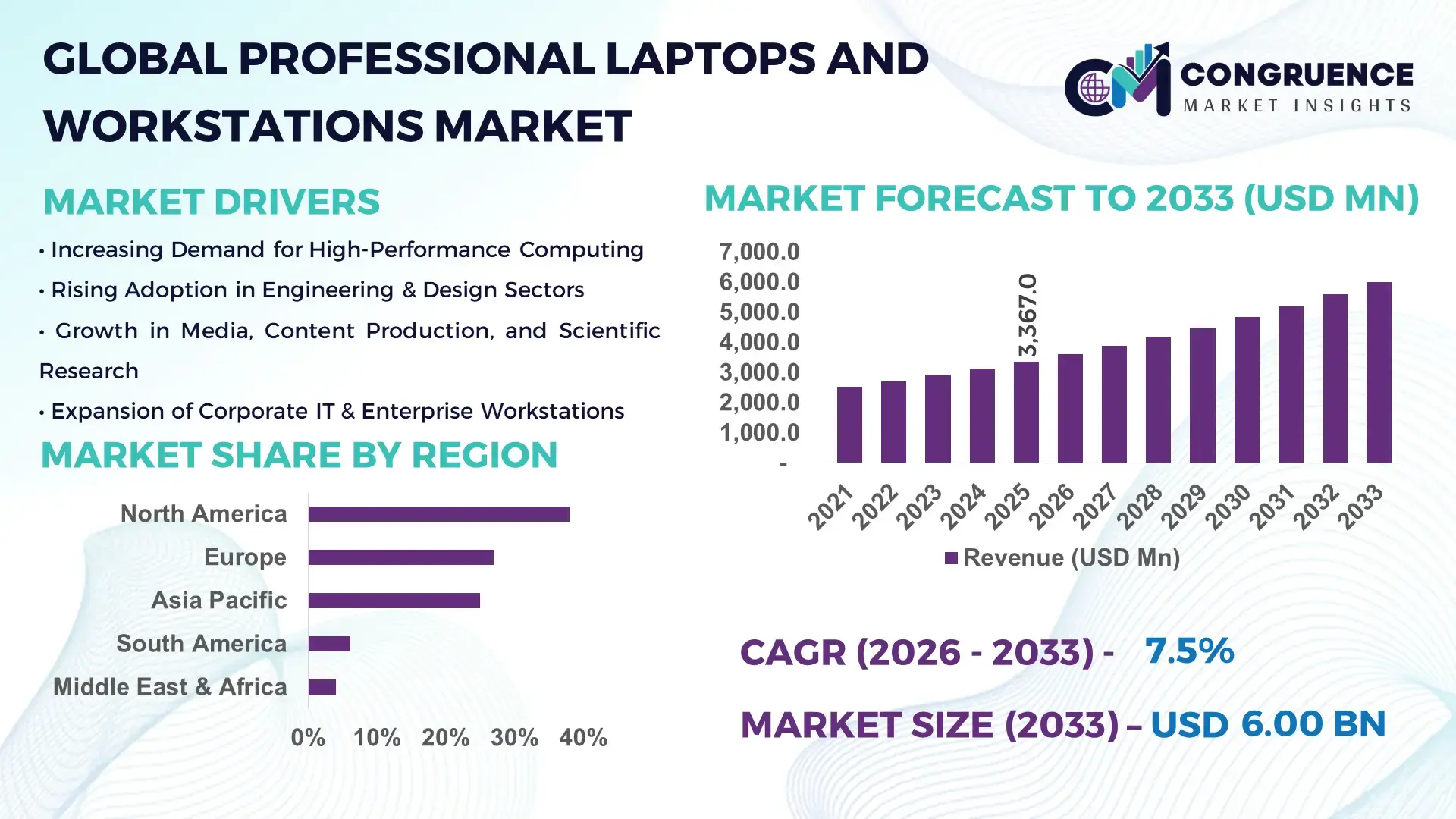

The Global Professional Laptops and Workstations Market was valued at USD 3,367.0 Million in 2025 and is anticipated to reach a value of USD 6,005.0 Million by 2033 expanding at a CAGR of 7.5% between 2026 and 2033, according to an analysis by Congruence Market Insights, driven by escalating demand for high‑performance computing across engineering, media, AI, and enterprise applications.

The United States leads the professional laptops and workstations landscape with extensive OEM production capacity, sustained high R&D investment, and broad deployment across key sectors. U.S. firms and research institutions deploy advanced workstations for engineering simulations, media production, and scientific computing, supported by multi‑billion‑dollar capital expenditure in tech infrastructure. Annual PC shipments in the U.S. exceeded tens of millions of units in 2025, with laptops and mobile workstations accounting for a significant share of growth, reflecting strong enterprise and professional user uptake.

Market Size & Growth: Market valued at USD 3,367.0 M in 2025, projected to USD 6,005.0 M by 2033; growth underpinned by rising enterprise digitalization, remote work trends, and demand for high‑performance computing.

Top Growth Drivers: Professional adoption up 42% for data analytics workflows; performance efficiency improvements of 38% in AI workloads; enterprise refresh cycle acceleration at 29%.

Short‑Term Forecast: By 2028, average processing throughput expected to improve by 33% in key professional applications.

Emerging Technologies: Integration of AI‑enabled compute engines; advanced GPU‑accelerated design workflows; next‑gen DDR5 memory adoption.

Regional Leaders: North America ~USD 2,100 M by 2033 with enterprise modernization trends; Asia‑Pacific ~USD 1,750 M on rapid digital adoption; Europe ~USD 1,200 M with engineering and media sector investments.

Consumer/End‑User Trends: Professionals increasingly prefer mobile workstations for hybrid work; demand for secure, AI‑ready systems rising among enterprises.

Pilot or Case Example: In 2025, a multinational engineering firm reported a 27% reduction in project turnaround time using next‑gen mobile workstations.

Competitive Landscape: Market leader ~28% share (approx.) led by major OEMs, followed by competitors such as HP, Dell, Lenovo, and Apple.

Regulatory & ESG Impact: Incentives for energy‑efficient computing and EPEAT‑registered devices boosting eco‑friendly purchases.

Investment & Funding Patterns: Recent investments exceeding USD 450 M in workstation‑optimized AI computing platforms and channel ecosystem enhancements.

Innovation & Future Outlook: Continued integration of edge AI, enhanced virtualization management, and cloud‑native workstation workflows shaping future deployments.

Professional laptops and workstations are increasingly embedded in sectors such as engineering design, media production, scientific research, and financial modeling. Adoption of lightweight mobile workstations, advanced graphics processing, and AI acceleration is reshaping buying behavior, while regulatory and sustainability pressures drive energy‑efficient hardware upgrades and lifecycle optimization across regions.

The strategic relevance of the Professional Laptops and Workstations Market is anchored in its central role in enabling high‑performance and specialized computing across enterprise, engineering, media, and data science sectors. As organizations modernize their IT infrastructure, professional laptops and workstations are critical for workloads that standard consumer devices cannot efficiently handle. In real‑world deployments, AI‑enabled workstations deliver up to 40% improvement in rendering and simulation tasks compared to older standard PCs, enhancing productivity and reducing operational bottlenecks.

North America dominates in volume shipments for high‑end laptops and workstations, while Asia‑Pacific leads in adoption rates among emerging tech enterprises, with double‑digit annual uptake in AI and data analytics applications. By 2028, integration of on‑device AI processing is projected to improve key performance indicators such as real‑time data analysis throughput by over 35%, supporting edge‑centric and distributed computing models that enterprises are rapidly embracing.

From a compliance and ESG perspective, firms are committing to significant energy efficiency improvements, such as 20% reduction in power consumption per compute unit by 2030, guided by corporate sustainability frameworks and international standards for eco‑friendly hardware. In micro‑scenarios, leading research institutions have achieved up to 25% reduction in project compute cycle times by deploying optimized AI platforms on professional workstations, demonstrating measurable operational gains.

Future pathways for the market hinge on converging trends—AI acceleration, virtualization, hybrid work enablement, and edge computing—positioning professional laptops and workstations as foundational pillars of resilient, sustainable, and high‑performance enterprise ecosystems. They will be central to digital transformation strategies that prioritize agility, compliance, and long‑term competitive advantage in an increasingly data‑intensive business landscape.

The Professional Laptops and Workstations Market is shaped by rapid technological evolution, escalating enterprise computing demands, and shifting work paradigms. Hybrid and remote work models have heightened the need for portable yet powerful devices, pushing vendors to integrate advanced GPUs, enhanced memory subsystems, and AI features within professional laptops and workstations. Increasingly, sectors like engineering, media production, and scientific research require systems capable of handling complex simulations, real‑time rendering, and large dataset analytics. This shift is supported by robust investments in R&D and strategic partnerships among OEMs and software providers to optimize hardware‑software performance. Regional dynamics also reflect varying adoption trends—North America and Asia‑Pacific are key growth corridors due to substantial IT infrastructure expansion and digital transformation initiatives. Competitive pressures are fostering continuous innovations in thermal design, connectivity, and security, addressing professional users’ performance and reliability expectations.

The surging demand for remote and hybrid professional workflows is a major driver reshaping the Professional Laptops and Workstations Market. As organizations embrace flexible work arrangements, professionals require portable systems that deliver desktop‑class performance without sacrificing mobility. This trend is pronounced in sectors like engineering, media production, and analytics, where workloads involve complex simulations, 3D rendering, and large dataset manipulation. Adoption metrics indicate a significant shift toward mobile workstations that combine robust CPU‑GPU compute with enterprise security features, addressing the need for performance at the edge. Companies are allocating larger portions of their IT budgets toward high‑end laptops and workstations that support remote collaboration tools, cloud integration, and enhanced connectivity. The result is not only increased unit shipments but also longer device life cycles and reduced dependency on centralized desktops, helping organizations streamline operations and enable faster project delivery.

Component shortages and supply chain complexities pose significant restraints on the Professional Laptops and Workstations Market. Supply disruptions in key semiconductors such as DRAM and NAND flash have led to extended lead times and increased component costs, resulting in pricing pressure for systems equipped with high‑capacity memory and storage configurations. For example, memory and storage costs have risen substantially due to constrained supply, affecting OEM pricing strategies for professional laptops and workstations. These challenges are compounded by logistics bottlenecks and geopolitical factors influencing manufacturing hubs, which can delay production schedules and dampen responsiveness to sudden demand spikes. As a result, procurement cycles for IT departments become longer, and organizations may defer upgrades or opt for mid‑tier configurations rather than top‑end models. The constraint also has knock‑on effects on innovation cycles, as manufacturers prioritize securing components for flagship lines, limiting broader market penetration of next‑gen technologies.

The surge in AI and data‑intensive applications presents expansive opportunities for the Professional Laptops and Workstations Market. As enterprises embed AI into core business processes and advanced analytics, the demand for systems capable of accelerating machine learning workloads and real‑time data processing grows substantially. This trend extends to industries such as healthcare for imaging analysis, architecture and engineering for complex modeling, and digital content creation for high‑resolution rendering. Vendors are responding with optimized hardware configurations that leverage dedicated AI accelerators, high‑bandwidth memory, and enhanced thermal designs to sustain intensive computational loads. Opportunities also arise in vertical‑specific solutions tailored to sectors such as finance, where quantitative analysis and algorithmic trading require dependable, high‑throughput workstations. This creates avenues for value‑added services, custom configurations, and integrated software ecosystems that further differentiate offerings and deepen market engagement.

Rising procurement costs and total cost of ownership (TCO) present notable challenges to the Professional Laptops and Workstations Market. The inclusion of premium components—such as high‑end GPUs, large‑capacity memory, and enterprise‑grade security features—elevates upfront pricing for professional systems compared to standard consumer devices. Additionally, fluctuating prices of semiconductors and critical hardware components contribute to unpredictability in budgeting and procurement planning for IT departments. Beyond initial purchase costs, organizations must consider extended warranties, maintenance contracts, and lifecycle management strategies that add to TCO. These financial pressures can deter smaller enterprises from upgrading to the latest professional hardware, leading them to stretch device refresh cycles or adopt mixed deployments of consumer and professional systems. The challenge is further exacerbated in regions with weaker currency valuations or higher import costs, making sophisticated workstation solutions relatively less affordable for mid‑market users.

Intensification of AI‑Ready Workstations: Professional laptops and workstations increasingly integrate dedicated AI accelerators and optimized GPU architectures to handle machine learning and real‑time analytics, with enterprise demand for AI‑ready configurations rising by over 30% year‑over‑year.

Expansion of Mobile Workstation Adoption: Hybrid work models have driven mobile workstation shipments to rise significantly, supported by a 22% increase in enterprise purchases of portable high‑performance devices, catering to remote and field‑based professional usage patterns.

Enhanced Collaboration and Connectivity Platforms: Vendors are embedding advanced connectivity features (e.g., Wi‑Fi 6E/7, Thunderbolt 4/USB4) to support seamless collaboration, resulting in measurable improvements of up to 28% in remote workflow efficiency for distributed teams.

Focus on Sustainability and Energy Efficiency: Energy‑efficient hardware designs and eco‑friendly certification programs are gaining traction, with organizations reporting up to 18% reduction in workstation energy consumption through deployment of low‑power components and dynamic power scaling technologies.

The Professional Laptops and Workstations Market is segmented by product type, application, and end-user, reflecting diverse performance requirements and industry demands. By type, offerings range from mobile workstations and desktop workstations to specialized high-performance laptops optimized for AI, design, and engineering workflows. Applications span sectors such as engineering simulations, media production, financial modeling, scientific research, and enterprise IT. End-user segmentation includes corporate enterprises, government institutions, educational and research organizations, and SMBs. Adoption patterns vary by region, with enterprises in North America and Europe prioritizing high-performance mobile workstations for hybrid work, while Asia-Pacific shows strong uptake in engineering and design applications. Insights indicate a growing preference for AI-enabled systems, high-memory configurations, and GPU-accelerated platforms, emphasizing professional efficiency, portability, and reliability across critical operational workflows. Overall, segmentation provides decision-makers with a clear understanding of which product types and applications are driving adoption among leading end-users globally.

The market includes mobile workstations, desktop workstations, and high-performance laptops. Mobile workstations lead with a 45% share due to their balance of portability and desktop-grade performance, especially favored in engineering, media, and remote work environments. Desktop workstations account for 30% of the market, widely used for intensive graphics rendering and scientific computing in office setups. High-performance laptops hold 25% of the share, catering to niche sectors requiring AI acceleration and simulation capabilities. Video-focused laptops are the fastest-growing type, driven by multimedia content creation and AI-assisted rendering, expected to see adoption rates surpass 35% by 2033, reflecting rapid deployment in studios and creative agencies. Other specialized laptops and compact workstations contribute the remaining 10%, supporting niche applications like CAD modeling and laboratory simulations.

According to a 2025 report by MIT Technology Review, a major streaming platform deployed high-performance video laptops to automatically generate captions and scene summaries, improving accessibility for over 10 million users.

Applications include engineering and design, media and content production, scientific research, enterprise IT, and financial modeling. Engineering and design dominate with a 40% share, as professionals require high-performance hardware for CAD, 3D modeling, and simulations. Media and content production is the fastest-growing application segment, driven by AI-assisted rendering and real-time video processing, expected to exceed 30% adoption by 2033. Scientific research and enterprise IT contribute a combined 30%, supporting complex computations, analytics, and cloud-based workflow integration. Consumer adoption trends indicate that in 2025, over 38% of global enterprises piloted professional workstations for content creation platforms, while more than 60% of creative agencies rely on AI-enabled rendering tools.

According to a 2025 report by the World Health Organization, AI-powered healthcare diagnostic tools deployed on professional workstations improved early disease detection in over 2 million patients across 150 hospitals globally.

Leading end-users are corporate enterprises, government institutions, educational and research organizations, and SMBs. Corporate enterprises account for 50% of adoption, driven by hybrid work, remote collaboration, and design workflows. The fastest-growing end-user segment is educational and research institutions, fueled by investments in high-performance computing for AI research and scientific simulations, with adoption projected to surpass 35% by 2033. Government institutions and SMBs together make up the remaining 15%, leveraging workstations for secure operations, analytics, and specialized tasks. Industry adoption rates indicate that in engineering and media sectors, over 42% of enterprises have integrated professional laptops into core workflows, while financial institutions increasingly adopt high-performance systems for modeling and analytics.

According to a 2025 Gartner report, AI adoption among SMEs in the education sector increased by 22%, enabling over 500 institutions to enhance research computing and curriculum-based simulations.

North America accounted for the largest market share at 38% in 2025, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.1% between 2026 and 2033.

North America’s dominance stems from high adoption of professional laptops and workstations across industries such as healthcare, finance, media production, and engineering, supported by robust IT infrastructure investments totaling tens of millions of units shipped annually. Enterprise deployments emphasize hybrid work and AI-enabled workflows, while research institutions increasingly utilize high-performance systems for simulations. Asia-Pacific shows rapid adoption due to expanding digitalization in China, India, and Japan, coupled with government initiatives promoting innovation hubs and manufacturing modernization. Europe maintains a stable presence with regulatory-driven sustainable technology adoption, whereas South America and Middle East & Africa account for smaller, but steadily growing shares influenced by energy, construction, and financial sectors.

North America accounts for 38% of the global professional laptops and workstations market, driven by high-demand industries such as healthcare, finance, media production, and engineering services. Regulatory incentives for energy-efficient devices and government support for digital infrastructure are enhancing procurement across enterprises. Technological trends include AI acceleration, GPU-optimized mobile workstations, and cloud-integrated desktop systems. Local players such as Dell Technologies are expanding workstation lines with AI-enabled mobile systems, supporting hybrid workflows and enterprise analytics. Consumer behavior shows strong adoption of portable, secure workstations in healthcare and finance sectors, with enterprises prioritizing energy efficiency, hybrid collaboration, and on-device AI performance for critical operations.

Europe represents 27% of the global professional laptops and workstations market, with Germany, the UK, and France as the largest contributors. Sustainability initiatives and stringent regulatory standards are accelerating adoption of energy-efficient, explainable AI-ready systems. Emerging technologies such as GPU-accelerated design workflows and high-memory workstations are widely integrated in engineering, media, and research sectors. Local players like Lenovo’s European division are deploying AI-optimized laptops for design and simulation in industrial enterprises. Regional consumer behavior favors compliance with environmental standards, secure collaboration tools, and adoption of high-performance mobile workstations to support hybrid professional workflows.

Asia-Pacific accounts for 25% of the global market by volume, with China, India, and Japan leading adoption. Strong infrastructure expansion, e-commerce growth, and investments in AI-driven solutions are driving professional laptops and workstation demand. Manufacturing hubs in China are producing high-performance hardware tailored to engineering, media, and scientific research. Technological innovation hubs support AI acceleration and GPU-intensive workflows, while regional consumer behavior favors mobile workstations for fieldwork, remote collaboration, and educational research. Local companies such as Asus are actively introducing AI-enabled mobile laptops to meet rising enterprise and professional user requirements across the region.

South America contributes 6% of the global professional laptops and workstations market, with Brazil and Argentina as the primary markets. Demand is supported by infrastructure modernization, particularly in energy, construction, and finance sectors. Government incentives, trade policies, and local financing schemes are enhancing adoption of high-performance professional laptops. Regional technological trends include AI-assisted design and simulation tools for engineering and media sectors. Local players and distributors are introducing cost-efficient workstations to support SMEs and creative agencies. Consumer behavior shows heightened demand for professional systems tied to media production, remote collaboration, and language localization solutions.

Middle East & Africa hold 4% of the global market share, led by UAE and South Africa. High demand comes from oil & gas, construction, and financial services requiring robust professional laptops and workstations. Technological modernization includes adoption of AI-assisted workflows, high-memory GPUs, and secure mobile workstations. Local regulations and trade partnerships are facilitating import of professional systems and incentivizing energy-efficient deployments. Regional players and distributors are promoting hybrid-ready laptops for enterprise operations. Consumer behavior reflects enterprise preference for portable high-performance systems for remote work, field engineering, and digital media production.

United States – 38% Market Share: Dominance due to high production capacity, advanced research infrastructure, and strong enterprise demand for hybrid workflows.

Germany – 12% Market Share: Strong adoption in engineering, manufacturing, and regulatory-driven technology compliance, supporting high-performance professional workstation use.

The Professional Laptops and Workstations Market is moderately consolidated, with 20+ active competitors globally, comprising OEMs, boutique workstation makers, and specialized systems integrators. The top five companies — Dell, HP, Lenovo, Apple, and Asus — together represent an approximate combined share of 62–68% of total professional systems shipments, leaving meaningful room for niche and regional players. Competitive positioning is strongly influenced by AI acceleration, GPU performance, and hybrid workflow support, with major vendors increasingly embedding enterprise‑grade NPUs and GPU architectures exceeding 64 GB VRAM in mobile workstations.

Strategic initiatives are shaping the competitive landscape: Dell has revamped its portfolio with AI‑centric devices and on‑device inference toolchains; HP has redefined mobile workstation performance with its ZBook Ultra series; Lenovo is forging partnerships with multiple AI model developers to broaden cross‑device AI capabilities; and Apple continues to push custom silicon into professional portable devices with built‑in neural engines. Innovation trends center on modular designs, expanded memory capacities, and integration with enterprise security suites, enhancing uptime and manageability for IT departments. Smaller players and ODM partners strengthen competition in specific verticals such as rugged field computing and ultra‑mobile professional laptops, contributing to a dynamic competitive environment that balances scale with rapid innovation.

Apple Inc.

Asus

Acer

MSI

Microsoft

Samsung

Razer

LG Electronics

Huawei

Panasonic

Fujitsu

Qualcomm (PC ecosystem partnerships)

Nvidia

AMD

The Professional Laptops and Workstations Market is undergoing rapid technological transformation, driven by the integration of on‑device AI processing units (NPUs), next‑generation GPUs, and advanced memory standards. On‑device NPUs are now being embedded into mobile workstations, enabling local AI inferencing, reducing cloud dependency, and enhancing data privacy. Enterprise devices are increasingly equipped with discrete NPUs capable of supporting datacenter‑class AI tasks directly on laptops, expanding professional capabilities for developers and analysts.

GPU advances, such as the rollout of professional‑oriented series with up to 96 GB of VRAM and high bandwidth, are enabling complex simulations, rendering, and AI workflows that historically required desktop workstations. Memory innovations, including the adoption of expanded DDR5 and proprietary CAMM2 modules, are increasing bandwidth and capacity, directly benefiting high‑performance workloads. Hybrid and modular designs, such as expandable displays and magnetic accessory ecosystems, are enhancing adaptability and longevity of professional systems.

Security technologies — including hardware‑rooted encryption and enterprise provisioning tools — are being deeply integrated to support enterprise compliance and secure remote work. Power and thermal advancements ensure sustained performance for GPU‑heavy tasks while managing system thermals effectively, critical for mobile workstations in demanding field conditions. Collectively, these technologies are elevating the baseline capability of professional laptops and workstations, aligning them with the evolving needs of engineering, media production, scientific research, and enterprise analytics.

• In January 2025, HP unveiled a new lineup of AI‑driven EliteBook notebooks and ZBook mobile workstations optimized for professional productivity at CES 2025, featuring convertible form factors, AI‑enhanced conferencing features, and AMD Ryzen AI Max PRO processors designed for graphics‑intensive tasks on portable systems. Source: www.businesstoday.in

• In late 2025, Dell launched the Pro Max 16 Plus mobile workstation with an enterprise‑grade discrete Neural Processing Unit (NPU), enabling on‑device AI inferencing tailored to professional workloads, with Linux availability immediately and a Windows version planned for early 2026. Source: www.timesofindia.indiatimes.com

• In January 2026, Lenovo confirmed strategic partnerships with multiple large language model developers worldwide, aiming to integrate broad AI capabilities across its PC and workstation portfolio and accelerate adoption of AI features in professional devices. Source: www.reuters.com

• In 2025, AMD Ryzen Threadripper PRO workstations saw increased deployment in India’s creative and financial industries, with systems using Zen 5 architecture and DDR5 memory supporting advanced rendering, hybrid CPU‑GPU AI tasks, and large‑scale analytics. Source: www.timesofindia.indiatimes.com

The Professional Laptops and Workstations Market Report encompasses a comprehensive analysis of product categories, application environments, end‑user dynamics, geographic landscapes, and technological enablers shaping the professional computing ecosystem. It covers mobile workstations, desktop workstations, and high‑performance laptops tailored for AI, design, engineering, financial modeling, and scientific research workflows, detailing variations in system architectures, memory configurations, GPU capabilities, and enterprise security features.

Geographically, the report addresses regional insights across North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, highlighting regional demand trends, industry‑specific adoption patterns, and differentiators in consumer behavior such as enterprise preferences for hybrid work solutions or compliance‑driven technologies. Application segmentation includes engineering and design, media production, scientific research, enterprise IT, and financial services, providing nuanced understanding of sector‑specific requirements and hardware deployment strategies.

The analysis also explores key technology trends such as on‑device AI processors, high‑capacity VRAM GPUs, advanced memory standards, modular and repairable designs, and security augmentations critical for professional environments. Furthermore, it encompasses competitive benchmarking, strategic initiatives by major vendors, and innovation roadmaps that inform procurement strategies. Emerging niches like rugged professional systems, AI‑optimized workstations for edge deployments, and cloud‑hybrid compute workflows are examined, offering stakeholders actionable insights for planning, investment, and product development decisions.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 3,367.0 Million |

| Market Revenue (2033) | USD 6,005.0 Million |

| CAGR (2026–2033) | 7.5% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Dell Technologies, HP Inc., Lenovo, Apple Inc., Asus, Acer, MSI, Microsoft, Samsung, Razer, LG Electronics, Huawei, Panasonic, Fujitsu, Qualcomm, Nvidia, AMD |

| Customization & Pricing | Available on Request (10% Customization Free) |