Reports

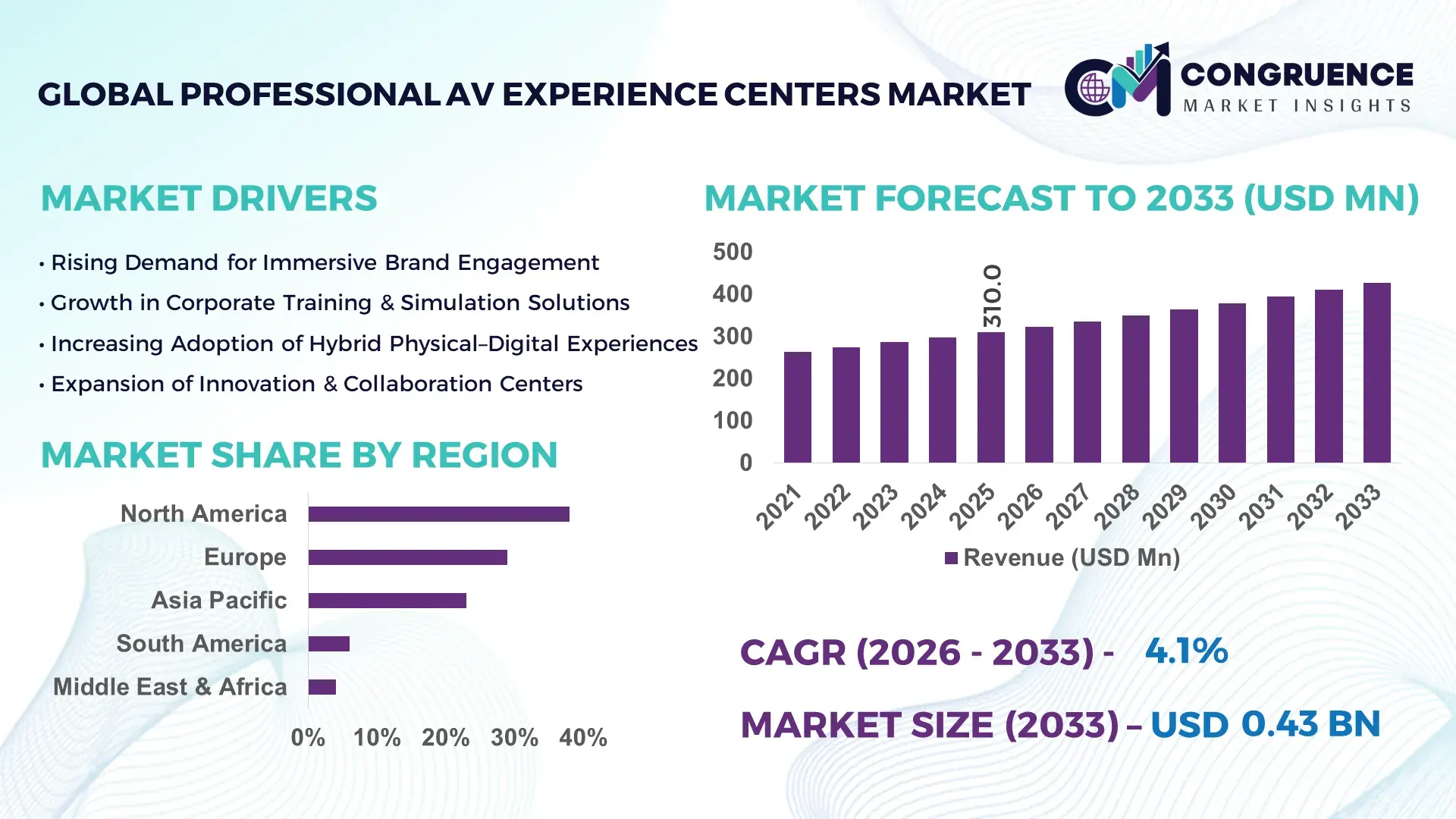

The Global Professional AV Experience Centers Market was valued at USD 310.0 Million in 2025 and is anticipated to reach a value of USD 427.5 Million by 2033 expanding at a CAGR of 4.1% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is primarily driven by rising enterprise investment in immersive customer engagement, digital transformation initiatives, and experience-led B2B sales environments.

The United States dominates the Professional AV Experience Centers Market through its scale of technology investment, advanced production ecosystems, and enterprise adoption depth. The U.S. hosts over 38% of global Pro AV manufacturing and system integration capacity, supported by more than 5,000 certified AV integrators and solution providers. Annual enterprise spending on immersive digital experience infrastructure exceeds USD 22 billion, with key applications across corporate headquarters, smart campuses, retail flagship stores, defense simulation labs, and healthcare training centers. Over 62% of Fortune 500 companies operate at least one dedicated AV experience or innovation center, leveraging AI-driven content orchestration, 8K visualization walls, and real-time collaboration systems. The country also leads in technology deployment, with over 70% adoption of IP-based AV systems and 45% penetration of AI-enabled analytics platforms within experience environments.

Market Size & Growth: Valued at USD 310.0 Million in 2025, projected to reach USD 427.5 Million by 2033, growing at a CAGR of 4.1% driven by immersive enterprise engagement demand.

Top Growth Drivers: Enterprise digital transformation (48%), customer experience optimization (41%), remote collaboration enablement (36%).

Short-Term Forecast: By 2028, immersive AV deployments are expected to improve client conversion rates by 22%.

Emerging Technologies: AI-driven content personalization, IP-based AV over Ethernet, real-time 3D visualization engines.

Regional Leaders: North America (USD 165.0 Million by 2033 – enterprise-led adoption), Europe (USD 120.0 Million – smart infrastructure focus), Asia Pacific (USD 95.0 Million – rapid commercial expansion).

Consumer/End-User Trends: Over 58% of deployments originate from corporate enterprises and technology vendors.

Pilot or Case Example: In 2024, a German automotive OEM reduced product demonstration cycle time by 31% using immersive AV centers.

Competitive Landscape: Market leader holds ~18% share, followed by diversified global AV solution providers.

Regulatory & ESG Impact: Energy-efficient AV systems reduced power consumption by up to 27% per installation.

Investment & Funding Patterns: Recent global investments exceeded USD 640 Million in experience-center infrastructure projects.

Innovation & Future Outlook: Convergence of AI, spatial computing, and cloud-managed AV platforms is reshaping experience delivery.

The Professional AV Experience Centers Market serves corporate (42%), retail and brand showrooms (28%), education and training (17%), and healthcare and defense applications (13%). Recent innovations include AI-assisted content analytics, modular AV architecture, and carbon-efficient display systems. Regulatory energy-efficiency mandates, regional digital infrastructure expansion, and rising experiential marketing budgets are shaping demand, with Asia Pacific emerging as a high-growth consumption hub.

The Professional AV Experience Centers Market holds growing strategic relevance as enterprises shift from product-centric selling to experience-driven engagement models. These centers function as decision-acceleration platforms, combining immersive visualization, real-time collaboration, and data-driven storytelling to shorten sales cycles and improve stakeholder alignment. AI-powered AV orchestration delivers up to 35% higher engagement effectiveness compared to traditional static demo environments, positioning experience centers as core assets in enterprise strategy.

From a technology benchmark perspective, IP-based AV systems deliver 28% higher scalability compared to legacy HDMI-centric architectures, enabling rapid content updates and centralized management across multiple sites. Regionally, North America dominates in deployment volume, while Europe leads in sustainable AV adoption with over 46% of enterprises integrating energy-optimized systems. Asia Pacific is emerging as the fastest adopter, with more than 52% of new enterprise campuses planning immersive experience facilities.

In the short term, by 2028, AI-driven content analytics and automation are expected to reduce operational downtime by 24%, improving center utilization efficiency. ESG considerations are increasingly integrated, with firms committing to 30% energy consumption reduction per experience center by 2030 through LED efficiency, smart power management, and recyclable materials.

A measurable micro-scenario highlights this shift: in 2024, a U.S. technology firm achieved a 29% increase in deal closure rates after deploying an AI-enabled AV experience center for enterprise clients. Looking ahead, the Professional AV Experience Centers Market is positioned as a pillar of organizational resilience, regulatory alignment, and sustainable, experience-led growth.

The Professional AV Experience Centers Market is shaped by accelerating enterprise digitalization, rising experiential marketing investment, and the convergence of IT and AV infrastructures. Organizations are prioritizing immersive environments to enhance customer engagement, internal collaboration, and complex solution demonstrations. Demand is influenced by advancements in visualization technologies, declining display hardware costs, and increased reliance on hybrid work models. At the same time, standardization of AV-over-IP protocols and cloud-based management platforms is reducing system complexity and improving scalability. The market is also affected by capital expenditure cycles, regional infrastructure readiness, and evolving compliance requirements related to energy efficiency and data security.

Enterprises are increasingly adopting immersive AV experience centers to improve customer engagement, internal decision-making, and brand differentiation. Studies indicate that immersive demonstrations improve information retention by up to 65% compared to traditional presentations. Over 60% of global enterprises report higher client confidence and reduced procurement timelines after implementing interactive AV environments. Growth is further supported by the expansion of complex solution selling in sectors such as IT, automotive, healthcare, and industrial automation, where visualization and simulation significantly enhance understanding and trust.

Despite long-term benefits, high upfront capital expenditure remains a restraint. A fully integrated professional AV experience center can require USD 0.8–2.5 million in initial investment, covering displays, control systems, content development, and facility upgrades. Smaller enterprises often face budget constraints, while ongoing maintenance, content refresh cycles, and skilled personnel requirements add operational complexity. Additionally, rapid technology evolution increases the risk of system obsolescence, causing cautious investment behavior among cost-sensitive organizations.

AI-enabled personalization presents significant growth opportunities by transforming static experience centers into adaptive engagement platforms. AI-driven content engines can tailor demonstrations in real time based on visitor profiles, improving engagement effectiveness by up to 33%. Integration of analytics enables enterprises to track visitor behavior, optimize layouts, and refine messaging. As over 45% of enterprises plan to deploy AI-enhanced customer experience platforms, experience centers are emerging as high-value data-driven engagement assets.

Integration of multi-vendor AV systems, IT networks, cybersecurity protocols, and building management systems presents operational challenges. Over 40% of deployments report delays due to interoperability issues between legacy AV hardware and modern IP-based systems. Ensuring low latency, system reliability, and secure data transmission requires specialized expertise, increasing dependence on skilled integrators. Shortages of certified AV professionals in emerging markets further constrain deployment timelines and scalability.

Expansion of AI-Driven Content Orchestration: AI-based content management platforms are increasingly deployed, enabling real-time adaptation of visuals and messaging. Over 47% of new experience centers now incorporate AI analytics, improving engagement metrics by 25–30% and reducing manual content updates by 40%.

Shift Toward AV-over-IP Architectures: AV-over-IP adoption has surpassed 68% in new installations, enabling flexible scaling and centralized management. Enterprises report 22% faster deployment times and 18% lower system reconfiguration costs compared to traditional architectures.

Sustainability-Focused AV Infrastructure: Energy-efficient LED walls, smart power management, and recyclable materials are gaining traction. Modern installations achieve up to 32% lower energy consumption, aligning experience centers with corporate ESG targets and regulatory efficiency standards.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Professional AV Experience Centers Market. Around 55% of new projects report cost benefits from prefabricated AV frameworks, reducing on-site labor by 35% and shortening project timelines by 20–25%, particularly in Europe and North America.

The Professional AV Experience Centers Market is segmented based on type, application, and end-user, reflecting how immersive audiovisual environments are designed, deployed, and consumed across industries. By type, the market spans fixed immersive installations, modular and reconfigurable systems, mobile/demo experience units, and hybrid digital-physical environments. Applications range from corporate brand experience and customer engagement to training, simulation, and retail visualization. End-user adoption is driven primarily by large enterprises and technology providers, followed by automotive, healthcare, education, and government institutions. Segmentation trends indicate a shift toward flexible, software-defined AV architectures, increased use of AI-driven content management, and higher demand for scalable experience platforms that can serve multiple stakeholder groups. Decision-makers increasingly evaluate segments based on adaptability, data integration capability, and long-term operational efficiency rather than purely hardware specifications.

The Professional AV Experience Centers Market includes fixed immersive experience centers, modular and reconfigurable AV systems, mobile or pop-up experience units, and hybrid virtual-physical experience platforms. Fixed immersive experience centers currently lead the market, accounting for approximately 44% of total adoption, due to their widespread use in corporate headquarters, flagship brand centers, and innovation labs where permanent, high-impact installations are required. These systems benefit from high-resolution visualization walls, integrated control rooms, and long lifecycle utilization.

Modular and reconfigurable AV systems represent the fastest-growing type, expanding at an estimated 5.6% CAGR, driven by enterprise demand for flexibility, faster deployment cycles, and lower reconfiguration costs. Organizations increasingly favor modular AV components that can be scaled or repurposed across multiple locations. Mobile and pop-up experience units, used extensively in events, exhibitions, and temporary demonstrations, contribute niche value with rapid setup advantages, while hybrid virtual-physical platforms are gaining relevance as digital twins and remote participation tools. Collectively, these remaining segments account for around 56% of installations, highlighting a diversified technology mix.

In 2025, a national innovation hub deployed a modular AV experience system across three cities, enabling reconfiguration within 48 hours and improving visitor throughput by over 30%.

By application, corporate brand experience and customer engagement leads the market with about 39% adoption, as enterprises increasingly rely on immersive storytelling to demonstrate complex solutions, products, and services. These environments are used to shorten sales cycles, improve stakeholder understanding, and enhance brand recall. Training and simulation applications are the fastest-growing, advancing at an estimated 6.1% CAGR, supported by rising demand for experiential learning in sectors such as manufacturing, healthcare, defense, and aviation.

Retail visualization, innovation showcases, and collaborative design review centers form other key application areas. Together, these secondary applications account for approximately 61% of overall usage, reflecting broadening adoption beyond traditional corporate showrooms.

Consumer and enterprise behavior supports this trend: in 2025, over 41% of global enterprises reported piloting immersive AV environments for customer experience and internal training, while nearly 58% of professionals indicated higher retention from interactive visual learning compared to conventional presentations.

In 2024, a multinational automotive company introduced immersive AV-based training simulators across its plants, reducing operator training time by 27%.

From an end-user perspective, large enterprises and multinational corporations dominate the Professional AV Experience Centers Market, representing approximately 46% of total adoption. These organizations deploy experience centers to support sales enablement, innovation collaboration, executive briefings, and partner engagement. Their scale and capital availability allow integration of advanced visualization, analytics, and automation technologies.

The automotive and advanced manufacturing sector is the fastest-growing end-user segment, expanding at an estimated 6.4% CAGR, fueled by demand for digital prototyping, virtual validation, and immersive training. Other significant end-users include healthcare providers, educational institutions, government agencies, and retail brands, which together contribute around 54% of market demand. Adoption rates are notable: over 42% of hospitals in developed economies are testing immersive AV environments for clinical training, while nearly 35% of universities have integrated experience centers into smart campus initiatives.

In 2025, a public-sector innovation agency implemented immersive AV experience centers across multiple regions, improving cross-department collaboration efficiency by 24%.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.6% between 2026 and 2033.

North America’s leadership is supported by high enterprise digitalization levels, with over 62% of large organizations operating dedicated immersive AV environments. Europe followed with 29% share, driven by regulatory-aligned digital infrastructure investments and sustainability-focused AV deployments. Asia-Pacific represented 23% of global adoption, supported by large-scale commercial infrastructure projects, smart city initiatives, and rapid enterprise technology upgrades. South America and the Middle East & Africa together accounted for the remaining 10%, reflecting growing but uneven adoption tied to infrastructure modernization and sector-specific investments.

North America holds approximately 38% of the global Professional AV Experience Centers Market, supported by strong demand from corporate headquarters, healthcare systems, financial institutions, and defense organizations. Over 58% of Fortune 1000 companies in the region use immersive AV environments for sales enablement and executive collaboration. Regulatory support for digital workplace modernization and energy-efficient infrastructure has accelerated upgrades to IP-based and AI-enabled AV systems. Technological advancements include widespread adoption of 8K visualization walls, cloud-managed AV platforms, and cybersecurity-integrated control systems. A leading U.S.-based AV integrator expanded modular experience center deployments across technology campuses in 2025, reducing system reconfiguration time by 30%. Regional consumer behavior shows higher enterprise adoption in healthcare and finance, where immersive visualization improves decision accuracy and training outcomes.

Europe accounts for around 29% of global market adoption, with Germany, the UK, and France contributing over 65% of regional demand. Strict sustainability directives and digital compliance frameworks have driven investment in energy-efficient displays and recyclable AV materials. More than 46% of newly deployed experience centers in Europe integrate low-power LED systems and smart energy monitoring. Adoption of emerging technologies such as AV-over-IP and real-time data visualization is rising across industrial design, automotive engineering, and public-sector innovation hubs. A European AV solutions provider introduced carbon-optimized immersive rooms in 2024, achieving 28% lower power consumption per installation. Regional consumer behavior reflects regulatory pressure, leading enterprises to prioritize transparent, auditable, and explainable digital experience platforms.

Asia-Pacific represents 23% of the global market and ranks as the fastest-growing region by volume expansion. China, India, and Japan together account for nearly 72% of regional deployments, supported by large-scale commercial real estate projects and smart campus developments. Manufacturing and IT services companies are major adopters, with over 49% of new enterprise facilities planning immersive AV zones. Regional trends include rapid deployment of modular AV systems, localized content engines, and AI-assisted multilingual interfaces. A Japanese electronics firm rolled out standardized experience centers across Asia in 2025, improving cross-border client engagement efficiency by 26%. Consumer behavior varies widely, with growth driven by e-commerce expansion, mobile-first engagement models, and digitally native enterprise workforces.

South America holds approximately 6% of global market share, led by Brazil and Argentina, which together contribute over 70% of regional installations. Demand is concentrated in media production, corporate communication hubs, and public-sector modernization projects. Infrastructure upgrades linked to urban development and energy-sector investments are supporting adoption of immersive visualization platforms. Government incentives promoting digital inclusion and smart infrastructure have encouraged pilot deployments in education and public administration. A Brazilian AV systems provider expanded localized content-driven experience centers for multilingual audiences, improving audience engagement by 22%. Regional consumer behavior highlights strong demand tied to media, language localization, and experiential brand communication.

The Middle East & Africa region accounts for roughly 4% of global adoption, with the UAE and South Africa emerging as key growth hubs. Demand is driven by large-scale construction projects, oil & gas sector visualization needs, tourism experiences, and smart city initiatives. Over 35% of new commercial developments in the Gulf region now integrate immersive AV environments during the design phase. Technological modernization includes adoption of high-brightness displays, digital twins, and centralized control systems. A UAE-based systems integrator deployed immersive command-and-experience centers for infrastructure projects in 2025, reducing project coordination delays by 19%. Consumer behavior varies by sector, with strong uptake in tourism, government showcases, and enterprise innovation centers.

United States – 31% Market Share: High enterprise concentration, advanced AV integration capacity, and widespread adoption across corporate, healthcare, and defense sectors.

Germany – 12% Market Share: Strong industrial base, advanced engineering applications, and regulatory-driven adoption of energy-efficient immersive AV environments.

The Professional AV Experience Centers Market exhibits a moderately fragmented competitive landscape, with numerous integrators, technology providers, and systems manufacturers participating across geographies. There are 30+ active competitors offering a range of immersive hardware platforms, control systems, software tools, and services designed to support enterprise AV environments. Leading companies maintain distinct market positioning: some focus on enterprise systems integration, others on display and projection technologies, and yet others on control and automation platforms. Collectively, the top 5 companies command an estimated combined share of around 42–48% of installed experience environments globally, indicating that while leaders have significant influence, there remains substantial room for niche and regional players to excel.

Competition is driven by strategic partnerships, innovative product launches, and acquisitions that broaden portfolios and deepen integration capabilities. For example, several major AV firms have introduced AI-assisted control platforms, cloud-managed AV services, and modular AV ecosystems that enhance scalability and user experience. Partnership initiatives between network technology firms and AV specialists are blurring traditional boundaries, with integrated collaboration systems becoming standard offerings. Innovation trends such as AI-enhanced user interfaces, AV-over-IP architectures, and immersive large-format LED solutions are reshaping competitive dynamics, compelling companies to invest in R&D and ecosystem development to maintain relevance. The competitive environment thus reflects both consolidation among major players and vibrant innovation from emerging technology providers, creating a dynamic market for decision-makers.

Barco

Extron Electronics

Yamaha

Sharp

Biamp Systems

AVIXA

LG Electronics

AVer Information

ViewSonic Corporation

Epson America

Shure Incorporated

IDK Corporation

Lightware Visual Engineering

Powersoft

Diversified

Technological developments are central to the evolution of the Professional AV Experience Centers Market, with integration, intelligence, and interactivity acting as core themes. AI-enhanced user interfaces are increasingly embedded in AV systems, enabling natural language voice control, gesture recognition, and adaptive automation that reduce operator burden and improve accessibility. By 2025, AI tools are becoming standard in control platforms, supporting personalized experiences and context-aware configurations that respond to user behavior and environmental conditions. Edge computing and centralized AV-over-IP (Audio-Visual over Internet Protocol) architectures are enabling scalable, networked deployments that reduce reliance on proprietary hardware while enhancing remote monitoring and configuration capabilities.

High-resolution LED displays and immersive visualization systems, including curvature screens and 8K environments, are now deployed across flagship experience centers and collaborative design suites, delivering richer visual fidelity and dynamic content presentation. Cloud-managed AV platforms are gaining traction, offering enterprises real-time system health insights, automated troubleshooting, and predictive maintenance analytics that improve uptime and reduce operational complexity. This trend is supported by integrated cybersecurity frameworks to safeguard AV network traffic and control protocols.

Modular AV components and standardized signal management systems are fostering flexibility in experience center design, allowing rapid reconfiguration of zones, displays, and audio segments without extensive rewiring. Collaboration with IT infrastructure providers is enabling unified communications integrations that blend video conferencing, content sharing, and immersive presentations into a seamless user experience. Spatial audio and advanced acoustics processing are also being embedded in professional environments to heighten engagement, especially in corporate and training settings. Collectively, these technological trends are reshaping how experience centers are designed, deployed, and maintained, emphasizing interoperability, intelligence, and operational efficiency for enterprise decision-makers.

• In June 2025, Panasonic Projector & Display Americas unveiled the MEVIX sub-brand at InfoComm 2025, expanding beyond hardware to integrated visual experience ecosystems that combine projection, display, software, and services for enhanced Pro AV environments. Source: www.avnetwork.com

• In October 2025, global IT solutions provider Zones officially entered the Pro AV industry at its Atlanta Tech Expo, introducing services focused on infrastructure modernization, security, and managed AV solutions to support enterprise integration and digital workplace AV deployments. Source: www.avnetwork.com

• In October 2025, Ross Video acquired immersive experiences platform provider ioversal, integrating its Vertex AV production suite into Ross Video’s ecosystem to expand capabilities in interactive exhibits and experiential AV solutions, enhancing creative storytelling tools. Source: www.avnetwork.com

• In mid-2025, several leading AV integrators introduced cloud-native AV control platforms that improved remote monitoring uptime by ~30% and reduced troubleshooting response times by nearly 40%, reflecting strong innovation in enterprise AV management.

The Professional AV Experience Centers Market Report provides a comprehensive analysis of the ecosystem encompassing immersive audiovisual environments used for corporate engagement, customer experience, training, simulation, and collaborative design. The scope includes detailed segmentation by type, such as fixed immersive installations, modular and reconfigurable systems, hybrid AV platforms, and mobile experience units, offering insights into deployment patterns and technological preferences across verticals. The report also examines application areas, including corporate brand centers, retail visualization hubs, educational and training environments, and specialized sectors like healthcare simulation labs and event spaces.

Geographically, the analysis covers North America, Europe, Asia-Pacific, South America, and Middle East & Africa, assessing market volumes, infrastructure readiness, regional technology adoption trends, and regulatory influences shaping investment decisions. Insights into technologies such as AI-enhanced AV interfaces, AV-over-IP architectures, high-resolution LED visualization systems, cloud-managed control platforms, and advanced audio processing are also included for professional evaluation. The report further explores end-user dynamics, highlighting enterprise, education, government, and specialized industry adoption patterns, along with consumer behavior variations influencing solution design.

Additionally, the study addresses competitive dynamics, profiling major players, strategic initiatives, partnerships, product innovations, and merger activity that influence market evolution. Emerging niche segments such as spatial audio environments, experiential retail AV deployments, and virtual-physical collaboration spaces are also examined. The report is structured to support strategic decision-making for industry professionals seeking a detailed view of market breadth, technological advancements, regional trends, and future opportunities.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 310.0 Million |

| Market Revenue (2033) | USD 427.5 Million |

| CAGR (2026–2033) | 4.1% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America, Europe, Asia-Pacific, South America, Middle East & Africa |

| Key Players Analyzed | Crestron Electronics, Cisco Systems, Panasonic Corporation, Barco, Extron Electronics, Yamaha, Sharp, Biamp Systems, AVIXA, LG Electronics, AVer Information, ViewSonic Corporation, Epson America, Shure Incorporated, IDK Corporation, Lightware Visual Engineering, Powersoft, Diversified |

| Customization & Pricing | Available on Request (10% Customization Free) |