Reports

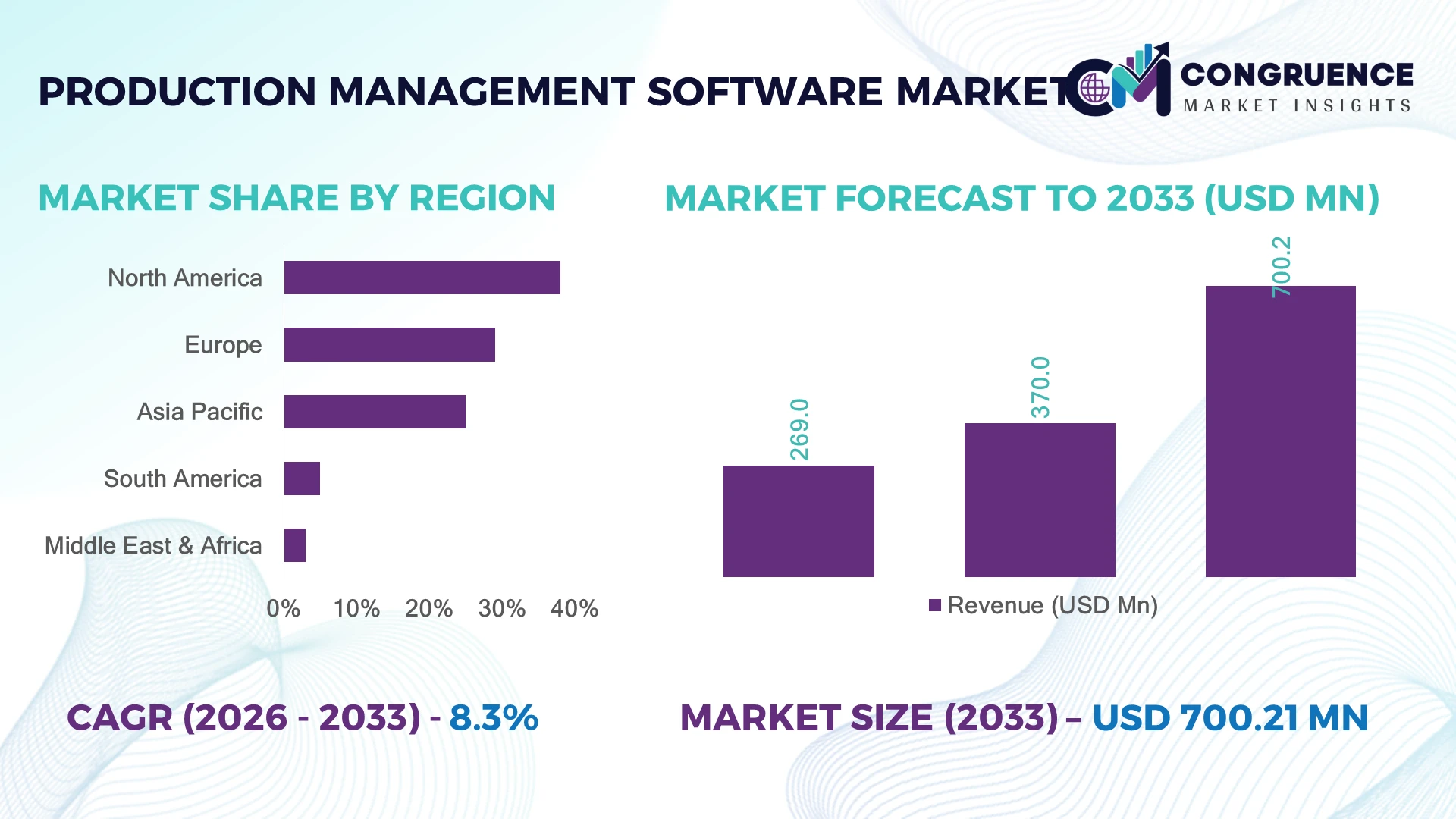

The Global Production Management Software Market was valued at USD 370.0 Million in 2025 and is anticipated to reach a value of USD 700.2 Million by 2033 expanding at a CAGR of 8.3% between 2026 and 2033. Rapid integration of AI-enabled production scheduling, cloud-based manufacturing execution systems, and real-time factory analytics is accelerating operational visibility, reducing production downtime, and improving multi-site manufacturing efficiency across industrial sectors.

The United States dominates the global market with an estimated 31% share, supported by widespread adoption across aerospace, automotive, electronics, and industrial manufacturing. More than 72% of large manufacturers have implemented advanced digital production platforms, while federal initiatives under the CHIPS and Science Act continue strengthening domestic manufacturing capabilities. In comparison, Germany demonstrates stronger Industry 4.0 integration in precision manufacturing, with higher factory automation intensity despite a comparatively smaller software deployment base.

This leadership reinforces investment priorities toward intelligent production ecosystems, scalable cloud deployments, and integrated manufacturing intelligence platforms.

Market Size & Growth: Valued at USD 370.0 Million (2025) and projected to reach USD 700.2 Million by 2033 at 8.3% CAGR, driven by AI-powered production optimization and factory digitalization.

Top Growth Drivers: AI scheduling adoption +42%, cloud manufacturing deployments +38%, industrial automation investments +29%.

Short-Term Forecast: By 2028, manufacturers are expected to improve production efficiency by 18% while reducing unplanned downtime by 22%.

Emerging Technologies: AI-based planning, Industrial IoT integration, and digital twin platforms are transforming advanced production environments globally.

Regional Leaders: North America (~USD 240 Million), Europe (~USD 190 Million), Asia-Pacific (~USD 175 Million); regional expansion is fueled by smart factory deployment and supply-chain modernization.

Consumer/End-User Trends: Nearly 68% of large manufacturers prioritize cloud-based production management for real-time operational visibility.

Pilot/Case Example: In 2024, a smart automotive production deployment improved scheduling accuracy by 25% and reduced cycle time by 17%.

Competitive Landscape: The leading vendor holds approximately 16% market share; major participants include Siemens, SAP, Dassault Systèmes, Oracle, and Rockwell Automation.

Regulatory & ESG Impact: Digital production platforms help manufacturers lower operational waste by nearly 15% while supporting industrial sustainability and compliance initiatives.

Investment & Funding: More than USD 2.4 Billion has been directed toward industrial software, cloud manufacturing, and strategic digital transformation partnerships.

Innovation & Future Outlook: Generative AI, predictive production intelligence, and connected manufacturing ecosystems are strengthening global operational resilience amid ongoing supply-chain restructuring.

Production Management Software Market solutions are gaining momentum across automotive, electronics, pharmaceuticals, and industrial equipment manufacturing as organizations seek greater production visibility and operational synchronization. AI-assisted scheduling, predictive analytics, and cloud-native deployment continue enhancing factory performance, while nearly 40% of manufacturers are expanding smart production initiatives. Growing emphasis on resilient supply chains and digitally connected operations is further accelerating enterprise-wide production management adoption, setting the foundation for broader strategic transformation.

Production management software has become a strategic business platform as manufacturers prioritize operational resilience, digital transformation, and faster decision-making across increasingly complex production networks. Supply-chain restructuring, regional manufacturing expansion, and workforce shortages are encouraging organizations to replace fragmented legacy systems with integrated production management environments that improve planning accuracy, resource utilization, and operational transparency. This shift is strengthening competitiveness while enabling faster responses to fluctuating customer demand.

Modern AI-enabled production management platforms deliver measurable advantages over conventional spreadsheet-driven or standalone scheduling systems by improving production planning efficiency by approximately 25% while reducing manual scheduling effort by nearly 30%. North America leads enterprise-scale deployments supported by advanced manufacturing investments, whereas Asia-Pacific is witnessing faster implementation across electronics, automotive, and industrial equipment sectors as manufacturers modernize production infrastructure. Over the next two to three years, cloud-based deployments and predictive production intelligence are expected to become standard capabilities across large manufacturing enterprises.

Manufacturers are increasingly partnering with automation providers, ERP vendors, and industrial AI specialists to deploy unified production ecosystems. For example, automotive manufacturers are integrating production management software with Industrial IoT platforms to optimize machine utilization, improve quality monitoring, and shorten production cycles. Organizations investing in intelligent production orchestration, scalable cloud architecture, and connected manufacturing ecosystems are establishing stronger competitive positioning while improving long-term operational agility and enterprise-wide manufacturing performance.

Manufacturers are rapidly replacing isolated production planning systems with AI-enabled production management platforms that improve scheduling accuracy, resource allocation, and factory-wide visibility. Nearly 72% of large manufacturers have adopted digital production initiatives, while AI-assisted scheduling has reduced production planning time by approximately 30% and improved equipment utilization by over 20%. The United States continues expanding advanced manufacturing under the CHIPS and Science Act, encouraging greater software integration across semiconductor and electronics production. This structural shift enables real-time coordination between ERP, MES, and Industrial IoT environments. In response, leading software vendors are expanding cloud-native portfolios, investing in predictive analytics, and forming automation partnerships to deliver scalable manufacturing intelligence. A notable strategic advantage lies in unified data orchestration, allowing manufacturers to optimize multiple production facilities through a single digital platform.

Many industrial facilities continue operating with aging production equipment that lacks compatibility with modern cloud-based production management software. Approximately 58% of mid-sized manufacturers still depend on legacy operational technology, while integration projects can consume nearly 35% of overall implementation effort. German and Japanese manufacturers operating mature industrial plants frequently encounter interoperability constraints between proprietary automation systems and modern software architectures. These compatibility issues increase deployment complexity, delay digital transformation initiatives, and extend operational transition periods. To minimize disruption, companies are adopting phased implementation strategies, investing in middleware platforms, and localizing system integration expertise. A key operational insight is that interoperability has become a competitive differentiator rather than simply a technical requirement, directly influencing implementation speed and production continuity.

Cloud-first production management platforms are unlocking new opportunities through connected manufacturing ecosystems, AI-driven optimization, and digital twin technologies. More than 65% of manufacturers plan to expand cloud-based production operations within the next three years, while predictive analytics can improve production efficiency by nearly 18% and reduce maintenance interventions by approximately 25%. India's manufacturing expansion through digital factory initiatives is creating strong demand for scalable production software across automotive, electronics, and industrial machinery sectors. Vendors are accelerating investments in low-code platforms, industrial AI, and ecosystem partnerships to deliver interoperable manufacturing solutions. An emerging strategic opportunity lies in combining production management with sustainability monitoring, enabling manufacturers to simultaneously improve operational efficiency and environmental performance through unified digital platforms.

As production management platforms become increasingly interconnected with Industrial IoT devices and enterprise systems, cybersecurity and workforce capability have emerged as critical execution barriers. Manufacturing accounts for nearly 25% of reported industrial cyber incidents, while approximately 41% of organizations identify shortages of digital manufacturing professionals as a major implementation constraint. The rapid expansion of connected factories in the United States has intensified pressure to secure operational technology networks against sophisticated cyber threats. Inconsistent cybersecurity maturity and limited technical expertise reduce deployment consistency, increase operational risk, and slow enterprise-wide software adoption. Companies are responding through zero-trust security frameworks, workforce upskilling initiatives, strategic cybersecurity partnerships, and continuous infrastructure modernization. Organizations that successfully integrate cyber resilience with production intelligence will establish stronger long-term operational competitiveness.

AI-Powered Production Intelligence AI-driven production scheduling and predictive analytics are becoming standard across manufacturing operations, with nearly 46% of large enterprises integrating AI into production workflows and planning accuracy improving by approximately 28%. Labor shortages and increasing production complexity are accelerating deployment, particularly in the United States. Software providers are expanding AI capabilities through strategic partnerships and embedded machine learning to improve throughput while minimizing manual intervention.

Cloud-Native Factory Operations Cloud-based production management platforms now represent over 60% of new enterprise deployments, while implementation timelines have shortened by nearly 35% compared with conventional on-premise environments. Multi-site manufacturers are centralizing production data to improve visibility and collaboration. In response to supply-chain volatility, companies are migrating toward scalable SaaS architectures, enabling faster software updates, standardized workflows, and lower infrastructure management costs across distributed manufacturing facilities.

Industrial Platform Convergence Manufacturers are increasingly integrating MES, ERP, PLM, and Industrial IoT platforms into unified production ecosystems. Approximately 58% of digital transformation projects now prioritize interoperability, reducing duplicate data handling by nearly 30%. German manufacturers continue leading standardized smart factory integration, while enterprise software vendors are strengthening open APIs, strategic acquisitions, and ecosystem partnerships to simplify cross-platform production orchestration and improve operational responsiveness.

Sustainability-Driven Production Optimization Environmental reporting requirements and operational efficiency initiatives are reshaping production management priorities. Digital production monitoring has reduced material waste by nearly 16% and improved energy utilization by approximately 12% across advanced manufacturing facilities. Companies are embedding sustainability dashboards, real-time resource tracking, and carbon performance metrics into production platforms, transforming compliance activities into measurable operational improvements while strengthening long-term manufacturing resilience.

Cloud-Based solutions represent the leading segment, accounting for an estimated 52% of enterprise deployments due to their scalability, centralized production visibility, and rapid implementation capabilities. Manufacturers operating multiple facilities increasingly prefer cloud platforms because they simplify software updates, enable remote production monitoring, and integrate seamlessly with AI, Industrial IoT, and analytics platforms. Vendors continue strengthening cloud portfolios through subscription-based licensing, cybersecurity enhancements, and continuous feature releases, supporting enterprise-wide digital manufacturing strategies. Hybrid deployment is emerging as the fastest-growing segment as manufacturers balance legacy infrastructure with modern cloud functionality. Nearly 41% of industrial enterprises are adopting hybrid architectures to maintain operational continuity while gradually modernizing production systems. On-Premise deployments remain strategically important for highly regulated industries requiring maximum control over operational data, particularly within defense and pharmaceutical manufacturing. Software providers are expanding interoperability capabilities and migration services, allowing organizations to modernize without disrupting critical production environments. Investment priorities increasingly favor flexible deployment models that accommodate diverse operational requirements while protecting existing infrastructure investments.

Manufacturing Execution Systems (MES) remain the dominant application segment, supported by extensive deployment across high-volume manufacturing environments where real-time production visibility, quality monitoring, and shop-floor coordination are essential. Approximately 48% of manufacturers identify MES as the foundation of digital factory initiatives, while integrated execution platforms improve production traceability by nearly 30%. Vendors continue enhancing MES functionality through AI-assisted scheduling, predictive maintenance integration, and advanced production analytics. Product Lifecycle Management (PLM) is the fastest-growing application as manufacturers seek tighter integration between product engineering and production execution. ERP platforms continue serving enterprise planning requirements by synchronizing procurement, finance, and manufacturing activities, while Inventory & Supply Chain applications are expanding rapidly in response to ongoing supply-chain restructuring and inventory optimization initiatives. Nearly 44% of industrial organizations are investing in integrated production applications that connect planning, execution, logistics, and quality management through unified digital ecosystems, improving responsiveness and reducing operational silos.

The Automotive industry represents the largest end-user segment, contributing approximately 34% of enterprise software deployments due to its highly automated production environments, complex supplier ecosystems, and continuous manufacturing operations. Connected production platforms improve scheduling efficiency, quality management, and production synchronization across multiple assembly facilities. Major software providers continue expanding automotive-focused solutions through digital twin capabilities, AI-powered production optimization, and strategic automation partnerships. The Pharmaceuticals sector is the fastest-growing end-user as manufacturers strengthen digital batch management, regulatory documentation, and production traceability. Electronics manufacturers continue increasing software investments to support high-mix production environments, while Food & Beverage companies prioritize production visibility and quality compliance across distributed facilities. Aerospace & Defense organizations maintain steady demand for secure production management platforms supporting precision manufacturing and lifecycle traceability. Nearly 57% of industrial software providers are expanding vertical-specific capabilities to address unique operational requirements, reinforcing competitive differentiation through customized deployment strategies and industry-focused innovation.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.1% between 2026 and 2033.

North America maintains the largest share of the Production Management Software Market due to extensive deployment across automotive, aerospace, semiconductor, and industrial manufacturing facilities. High enterprise digital maturity and widespread adoption of AI-enabled production platforms continue strengthening operational efficiency. Nearly 72% of large manufacturers have implemented connected production management solutions, while Industrial IoT integration continues expanding across multi-site operations. Strong investment in smart manufacturing infrastructure, supported by semiconductor production expansion and factory modernization initiatives, has accelerated software deployment. Technology vendors are strengthening cloud-native platforms, cybersecurity capabilities, and automation partnerships to improve production visibility, planning precision, and cross-facility operational synchronization.

United States Market Outlook: The United States remains the regional growth engine through its advanced manufacturing ecosystem, strong enterprise software adoption, and ongoing factory modernization initiatives. Automotive, aerospace, electronics, and semiconductor manufacturers continue investing in integrated production intelligence platforms that combine AI, MES, ERP, and Industrial IoT capabilities. More than 75% of large manufacturing enterprises have adopted digital production initiatives, while domestic semiconductor investments continue creating additional demand for advanced production management solutions supporting operational resilience, workforce productivity, and supply-chain optimization.

Europe represents a highly mature production management software landscape driven by advanced industrial automation, digital manufacturing strategies, and sustainability-focused factory modernization. Approximately 29% of global deployments are concentrated across the region, supported by strong adoption within automotive, industrial equipment, pharmaceuticals, and precision engineering industries. Manufacturers increasingly integrate production management software with digital twins, predictive maintenance, and quality analytics to improve operational consistency. Continuous investment in Industry 4.0 initiatives and standardized industrial connectivity is accelerating enterprise-wide deployment while strengthening cross-border manufacturing collaboration and production traceability.

Germany Market Outlook: Germany remains Europe's most influential market due to its leadership in industrial automation, machine manufacturing, and smart factory deployment. Automotive manufacturers and industrial equipment producers continue integrating production management software with robotics, Industrial IoT, and AI-driven production optimization. More than 60% of large industrial enterprises operate connected manufacturing environments, encouraging software vendors to expand localized cloud services, industrial partnerships, and advanced analytics capabilities tailored to high-precision manufacturing requirements.

Asia-Pacific is rapidly expanding through large-scale manufacturing investments, digital industrial transformation, and increasing enterprise software adoption across electronics, automotive, pharmaceuticals, and consumer goods production. The region contributes approximately 25% of current global market demand while demonstrating the fastest deployment momentum. Manufacturers are replacing fragmented production systems with integrated cloud-based platforms supporting centralized scheduling, quality management, and supply-chain coordination. Rising investment in factory automation, semiconductor manufacturing, and export-oriented production capacity continues encouraging software providers to expand regional partnerships and localized implementation services.

China Market Outlook: China leads regional adoption through its extensive manufacturing infrastructure, advanced electronics production, and government-supported industrial digitalization initiatives. Large manufacturers continue deploying intelligent production platforms integrating AI, Industrial IoT, and predictive analytics across multiple production facilities. More than 55% of medium and large industrial enterprises are actively investing in smart manufacturing technologies, encouraging software vendors to strengthen domestic partnerships, localized cloud infrastructure, and industry-specific digital production capabilities.

South America is witnessing gradual adoption of production management software as manufacturers improve operational visibility, production efficiency, and supply-chain coordination across automotive, food processing, mining equipment, and industrial manufacturing sectors. The region represents approximately 5% of global market activity, with enterprise deployments increasing through cloud-first implementation strategies that reduce infrastructure costs. Manufacturers are prioritizing integrated production planning and inventory visibility to improve competitiveness while responding to evolving export requirements. Software vendors continue expanding regional channel partnerships and implementation support to overcome technical capability gaps.

Brazil Market Outlook: Brazil dominates the regional market through its diversified industrial base and expanding manufacturing modernization initiatives. Automotive assembly, food processing, pharmaceuticals, and industrial equipment manufacturers increasingly deploy integrated production management platforms to improve scheduling accuracy and factory utilization. Approximately 45% of large manufacturers have initiated digital production transformation projects, creating sustained opportunities for enterprise software providers focused on scalable cloud deployment and localized technical services.

The Middle East & Africa market is advancing through industrial diversification programs, manufacturing infrastructure expansion, and increasing investment in digitally enabled production facilities. The region contributes nearly 3% of global demand while demonstrating improving enterprise software adoption across industrial manufacturing, energy equipment, pharmaceuticals, and food production. Governments continue promoting industrial modernization strategies that encourage automation, connected manufacturing, and cloud-enabled production management. Technology providers are expanding implementation partnerships, regional support centers, and localized software capabilities to address evolving manufacturing requirements and operational efficiency goals.

Saudi Arabia Market Outlook: Saudi Arabia represents the strongest market opportunity in the region through ongoing industrial diversification under Vision 2030 and substantial investment in advanced manufacturing infrastructure. Industrial companies are integrating production management software with automation systems, enterprise resource planning, and predictive maintenance platforms to strengthen operational performance. Nearly 40% of newly established manufacturing facilities are adopting digital production technologies during initial deployment, positioning the country as a leading destination for industrial software investment and long-term manufacturing transformation.

The Production Management Software Market is characterized by competition between global enterprise software leaders including Siemens, SAP, Oracle, Rockwell Automation (Plex), Dassault Systèmes, and AVEVA, alongside specialized MES providers and regional manufacturing software vendors. The top five players collectively account for approximately 48% of the global market, reflecting moderate consolidation with strong enterprise influence. Competition centers on cloud deployment, AI-enabled production intelligence, interoperability, and implementation speed rather than pricing alone. Nearly 62% of enterprise buyers prioritize seamless ERP-MES integration, while 58% evaluate vendors based on cybersecurity and scalability capabilities. Companies are strengthening market positions through cloud expansion, industrial partnerships, vertical-specific solutions, and acquisitions that enhance end-to-end manufacturing portfolios. The competitive landscape is shifting toward unified digital manufacturing ecosystems where integrated AI, Industrial IoT, and analytics platforms outperform standalone production applications. High implementation complexity and deep enterprise integration create significant entry barriers for new participants. Sustained leadership depends on delivering scalable, interoperable, industry-specific platforms with measurable operational outcomes and continuous innovation.

SAP SE

Oracle Corporation

Dassault Systèmes

Rockwell Automation

AVEVA Group plc

Hexagon AB

Infor

Epicor Software Corporation

Plex Systems

Tulip Interfaces

Critical Manufacturing

IFS AB

GE Vernova (Proficy Software)

Production management software is rapidly evolving through the convergence of artificial intelligence, Industrial IoT, cloud-native architectures, edge computing, and digital twin technology. More than 60% of newly deployed enterprise platforms now integrate AI-assisted production scheduling and predictive analytics, while connected Industrial IoT environments improve equipment utilization by approximately 18%. Cloud-native deployment has become the preferred implementation model for multi-site manufacturers seeking centralized operational visibility and continuous software enhancement.

Modern intelligent production platforms outperform conventional standalone scheduling systems through real-time data orchestration, automated workflow optimization, and machine learning. Compared with legacy production planning software, AI-enabled platforms reduce manual scheduling effort by nearly 30% while improving production planning accuracy by approximately 25%. Automotive, semiconductor, and electronics manufacturers gain the greatest competitive advantage because integrated MES, ERP, and PLM environments enable synchronized decision-making across engineering, production, and supply-chain functions. Enterprise adoption has exceeded 65% among large manufacturers pursuing smart factory transformation.

Between 2026 and 2028, generative AI, autonomous production optimization, industrial copilots, and low-code manufacturing applications will redefine production management capabilities. Vendors are embedding sustainability analytics, cybersecurity-by-design, and digital thread technologies into unified manufacturing platforms. Organizations investing now will achieve stronger operational resilience, faster deployment cycles, lower maintenance costs, and superior manufacturing agility as intelligent, connected production ecosystems become the competitive benchmark.

January 2025 – Siemens Digital Industries Software was recognized as a Leader in the IDC MarketScape Worldwide Manufacturing Execution Systems 2024–2025 assessment, reinforcing the competitiveness of its Opcenter platform for scalable, integrated manufacturing operations. The recognition highlights broad enterprise deployment across multi-plant environments. Source: www.news.siemens.com

March 2025 – Siemens announced that OPmobility adopted Teamcenter X cloud PLM as its enterprise product backbone to optimize product development and shorten engineering lead times. The deployment supports multiple global business units and strengthens digital continuity across complex mobility programs.

February 2025 – Rockwell Automation (Plex) was named a Leader in the IDC MarketScape Worldwide Manufacturing Execution Systems assessment and a Major Player in SaaS manufacturing ERP evaluations, strengthening its cloud manufacturing portfolio and enterprise positioning.

May 2025 – Siemens released Opcenter Execution Semiconductor 2504, introducing containerized deployment support, enhanced scheduling with Critical Ratio calculation, and improved semiconductor production workflows, enabling greater scalability and execution efficiency for wafer fabrication and assembly operations. Source: Siemens Opcenter Blog.

The report provides comprehensive analysis across Cloud-Based, On-Premise, and Hybrid deployment models while evaluating key application segments including MES, ERP, PLM, and Inventory & Supply Chain solutions. It further examines demand across major end-user industries comprising Automotive, Electronics, Pharmaceuticals, Food & Beverage, and Aerospace & Defense. Regional assessment spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting enterprise deployment patterns, digital manufacturing maturity, technology adoption, and competitive positioning across industrial ecosystems.

The study evaluates adoption trends, deployment strategies, cloud migration, AI-enabled manufacturing, Industrial IoT integration, cybersecurity, digital twins, and predictive production intelligence. It profiles leading technology providers, compares competitive strategies, and assesses operational benchmarks supporting investment planning, expansion priorities, product development, and partnership opportunities. Strategic insights covering enterprise modernization, deployment models, vertical demand, and emerging manufacturing technologies provide decision-makers with actionable intelligence to strengthen competitive positioning and guide market expansion between 2026 and 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 370.0 Million |

| Market Revenue (2033) | USD 700.2 Million |

| CAGR (2026–2033) | 8.3% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Siemens Digital Industries Software; SAP SE; Oracle Corporation; Dassault Systèmes; Rockwell Automation; AVEVA Group plc; Hexagon AB; Infor; Epicor Software Corporation; Plex Systems; Tulip Interfaces; Critical Manufacturing; IFS AB; GE Vernova (Proficy Software) |

| Customization & Pricing | Available on Request (10% Customization Free) |