Reports

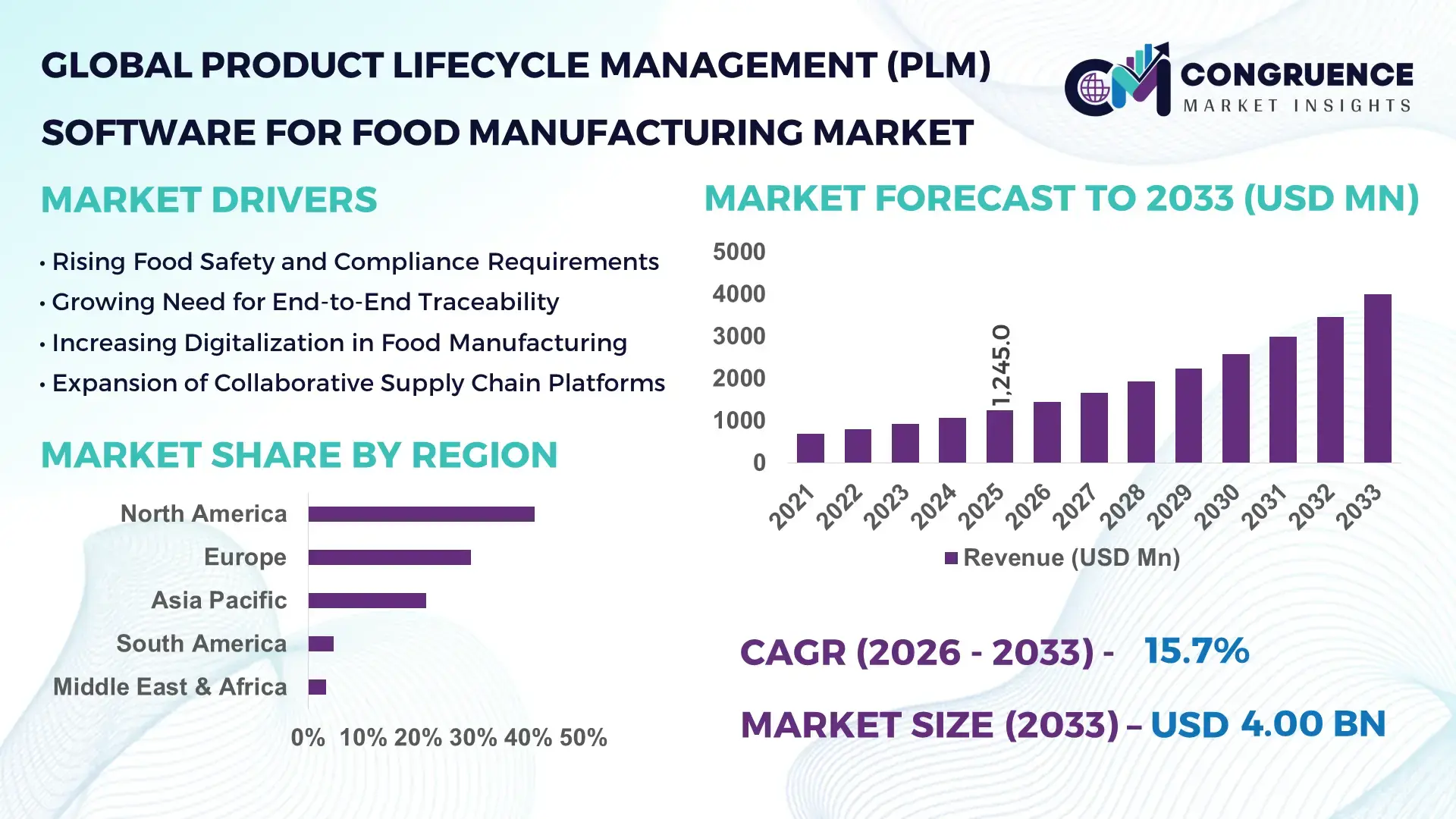

The Global Product Lifecycle Management (PLM) Software for Food Manufacturing Market was valued at USD 1,245.0 million in 2025 and is anticipated to reach USD 4,003.5 million by 2033, expanding at a CAGR of 15.72% between 2026 and 2033, according to an analysis by Congruence Market Insights. This rapid expansion is primarily driven by rising digitalization across food production, stricter regulatory compliance requirements, and growing demand for end-to-end traceability in supply chains.

The United States anchors the global PLM ecosystem for food manufacturing with one of the world’s most advanced digital food production infrastructures. Over 32,000 food and beverage processing facilities operate in the country, many integrating cloud-based PLM with MES and ERP platforms. U.S. food manufacturers invested more than USD 4.5 billion in smart factory and digital quality systems in 2024, with strong uptake in meat processing, dairy, and packaged foods. Large-scale producers increasingly deploy AI-enabled formulation management, digital twin simulations, and real-time allergen tracking across 60%+ of new production lines. Several leading multinationals run automated specification management platforms covering 15,000–40,000 SKUs per facility, while FDA compliance digitization programs have pushed adoption of electronic record-keeping across nearly 70% of mid-to-large plants. Pilot plants in California and Illinois are testing blockchain-linked PLM systems to trace ingredient provenance within minutes rather than days.

Market Size & Growth: Market valued at USD 1,245.0 million in 2025, projected to reach USD 4,003.5 million by 2033 at 15.72% CAGR, fueled by regulatory digitization and supply-chain transparency needs.

Top Growth Drivers: 68% rise in digital compliance adoption; 42% improvement in recipe cycle efficiency; 37% reduction in recall response time.

Short-Term Forecast: By 2028, automated specification workflows are expected to cut labeling errors by 30% and reduce product launch timelines by 25%.

Emerging Technologies: AI-driven formulation optimization, digital twins for production lines, and blockchain-enabled ingredient traceability.

Regional Leaders: North America (~USD 1.6 billion by 2033, advanced compliance automation); Europe (~USD 1.2 billion, sustainability-driven PLM use); Asia-Pacific (~USD 900 million, rapid plant digitalization).

Consumer/End-User Trends: Large processors lead adoption, while mid-sized firms increasingly shift to cloud PLM for cost efficiency and collaboration.

Pilot Example: In 2024, a U.S. dairy producer used AI-PLM to reduce rework by 28% and shorten recipe validation from 14 to 9 days.

Competitive Landscape: Dassault Systèmes (~22% share) leads, followed by Siemens, PTC, SAP, Oracle, and Ansys.

Regulatory & ESG Impact: Stricter FDA/EFSA digital record mandates and Scope 3 carbon tracking are accelerating PLM deployment.

Investment & Funding Patterns: Over USD 820 million invested in food tech PLM and quality software startups since 2023, with strong private equity interest.

Innovation & Future Outlook: Greater integration of PLM with IoT, predictive quality analytics, and automated supplier collaboration platforms.

Dairy, meat processing, and packaged foods account for the majority of PLM utilization due to complex formulations and compliance needs. Cloud-native platforms, AI-driven specification management, and real-time allergen monitoring are reshaping workflows. Stricter labeling laws, sustainability reporting requirements, and supply-chain disruptions are pushing faster digital adoption. North America leads consumption, while Asia-Pacific shows the fastest plant digitization growth. Future momentum will center on interoperable PLM–MES ecosystems, predictive quality analytics, and automated supplier data exchange.

Product Lifecycle Management (PLM) software has evolved from a back-office documentation tool into a core strategic platform for operational resilience, regulatory compliance, and innovation in food manufacturing. As global food supply chains become more complex, manufacturers increasingly rely on PLM to synchronize product design, formulation, sourcing, quality, and manufacturing execution across multi-plant networks. Modern AI-enabled PLM platforms deliver 35–45% faster recipe iterations compared to traditional spreadsheet-based systems, while reducing compliance rework by nearly 30% through automated version control and audit trails.

From a regional standpoint, Asia-Pacific dominates in production volume, driven by rapid capacity expansion in China, India, and Southeast Asia, while Europe leads in adoption, with approximately 58% of medium-to-large food enterprises now using integrated PLM–MES environments due to stringent EU traceability and sustainability regulations.

In the next 2–3 years, digital convergence will intensify. By 2028, AI-assisted formulation and predictive shelf-life modeling are expected to cut product development cycles by 25% and reduce spoilage-related losses by 18–22% across major processors. Cloud PLM combined with IoT sensors will enable continuous quality monitoring rather than periodic batch testing.

On the ESG front, leading food firms are committing to measurable sustainability targets. By 2030, more than 65% of top global processors plan to embed carbon tracking within PLM systems to achieve at least a 30% reduction in Scope 3 packaging emissions through optimized material choices and supplier collaboration.

A notable micro-scenario occurred in 2024, when a multinational packaged-food company deployed AI-integrated PLM across six plants in the U.S. and Europe, achieving a 27% reduction in reformulation waste and a 20% faster recall response time via real-time ingredient traceability.

Looking ahead, the Product Lifecycle Management (PLM) Software for Food Manufacturing Market is becoming a foundational pillar for resilient, compliant, and sustainable food systems—enabling faster innovation, stronger transparency, and smarter resource utilization across the global food value chain.

The Product Lifecycle Management (PLM) Software for Food Manufacturing Market is shaped by the convergence of digital transformation, regulatory complexity, and evolving consumer expectations. Rising demand for transparent labeling, real-time traceability, and faster product launches is pushing manufacturers toward integrated PLM ecosystems that connect R&D, quality, procurement, and production. Cloud-based deployments are replacing legacy on-premise systems, enabling cross-plant collaboration and data interoperability. Meanwhile, automation, AI-driven analytics, and IoT integration are increasing operational visibility and predictive quality control. Regulatory agencies such as the FDA and EFSA continue to tighten digital record-keeping requirements, further accelerating adoption. Supply-chain volatility, ingredient shortages, and sustainability mandates are also influencing investment in digital lifecycle management tools. Large enterprises lead adoption, but mid-sized firms are increasingly shifting to modular SaaS PLM solutions to reduce costs while improving compliance and agility.

Governments worldwide are mandating stricter digital documentation for food safety, traceability, and labeling accuracy. The U.S. Food Safety Modernization Act (FSMA) requires detailed electronic records for critical control points, pushing processors to adopt integrated PLM platforms that automatically log ingredient changes, supplier certifications, and batch histories. Similarly, the EU’s General Food Law emphasizes end-to-end traceability, compelling manufacturers to digitize product data across the lifecycle. Large processors handling tens of thousands of SKUs require centralized specification repositories to prevent mislabeling, allergen mismanagement, and costly recalls. Automated version control within PLM systems has reduced manual documentation errors by up to 40% in digitally mature plants. Additionally, increasing audits from retailers and regulators are forcing suppliers to demonstrate real-time compliance, making PLM a necessity rather than an option.

Despite clear benefits, the upfront cost of enterprise-grade PLM systems remains a major barrier for many mid-sized food manufacturers. Full-scale implementation—including software licensing, system integration, data migration, and employee training—can take 12–24 months and require significant capital investment. Many smaller firms still rely on fragmented legacy tools such as spreadsheets and standalone quality management systems, making PLM integration complex and expensive. Additionally, customizing PLM platforms to handle diverse recipes, allergens, and regional compliance rules often increases project costs. Limited IT expertise within smaller food companies further slows deployment, as they must rely on external consultants. As a result, adoption is uneven, with large multinationals moving quickly while smaller players lag behind.

AI-powered formulation tools integrated into PLM platforms are creating new opportunities for faster product innovation and waste reduction. By analyzing historical ingredient data, AI can suggest optimized recipes that maintain taste while lowering cost or improving nutritional profiles. Digital twins of production lines allow manufacturers to simulate process changes before physical trials, reducing pilot testing time by up to 30%. These technologies also support rapid scale-up from lab to factory by predicting equipment performance and quality outcomes. As plant automation expands, PLM systems that connect seamlessly with IoT sensors will enable real-time monitoring of temperature, humidity, and contamination risks. This convergence of AI, simulation, and real-time data is unlocking new efficiencies across product development and manufacturing operations.

Many food manufacturers operate with fragmented digital infrastructures, including separate ERP, MES, LIMS, and quality management systems that do not communicate seamlessly. Integrating these platforms with modern PLM software requires complex middleware solutions and extensive data standardization efforts. Inconsistent data formats, outdated databases, and siloed departmental workflows slow down implementation and reduce system effectiveness. Cybersecurity concerns also pose challenges, as cloud-based PLM platforms must comply with strict data protection regulations while ensuring secure supplier collaboration. Furthermore, frequent software updates and evolving regulatory requirements force companies to continuously modify their digital ecosystems, increasing maintenance costs and operational complexity.

Smart factories integrating PLM with IoT and automation: More than 70% of new large food plants are embedding PLM with IoT-enabled sensors that stream quality data in real time. Automated data capture has reduced manual inspections by 35% while improving defect detection by 28%. Digital dashboards now track temperature, humidity, and contamination risk across 100% of critical control points in leading facilities.

AI-driven specification and allergen management: AI-based PLM tools are now used in roughly 55% of major processors to auto-validate labels and ingredient lists. These systems have cut labeling errors by 30–40% and shortened regulatory review cycles from weeks to days. Several global brands report a 22% decline in allergen-related incidents after adopting AI-driven compliance workflows.

Cloud migration and supplier collaboration networks: Nearly 60% of food manufacturers shifted from on-premise to cloud PLM between 2022 and 2025. Cloud platforms enable real-time collaboration with over 1,000 suppliers per enterprise, reducing procurement delays by 25%. Multi-plant visibility has improved inventory accuracy by 18% through centralized data governance.

Sustainability tracking embedded in PLM workflows: Around 50% of large food companies now track packaging carbon footprints directly within PLM systems. Digital material passports have helped firms reduce plastic usage by 20% in redesigned products. Integrated lifecycle analytics are enabling annual packaging waste reductions of 15–25% across major processors.

The Product Lifecycle Management (PLM) Software for Food Manufacturing Market is structured around distinct layers of technology type, functional application, and end-user utilization, reflecting how digital lifecycle tools are embedded across the food value chain. By type, deployment models range from traditional cloud-native PLM platforms to advanced AI-enabled systems that integrate predictive analytics, digital twins, and real-time quality monitoring. Application-wise, usage spans formulation management, compliance documentation, supplier collaboration, production optimization, and recall management, with varying intensity depending on product complexity and regulatory exposure. End-users include large multinational processors, mid-sized regional manufacturers, ingredient suppliers, co-packers, and packaging producers, each adopting PLM at different levels of digital maturity. Large-scale producers prioritize enterprise-wide integration, while smaller firms focus on modular, use-case-driven implementations such as labeling accuracy or allergen tracking. Overall, segmentation reflects a market moving from basic documentation tools toward interconnected, data-driven lifecycle ecosystems that support innovation, transparency, and operational resilience.

Cloud-based PLM platforms represent the structural backbone of the market, enabling multi-plant collaboration, real-time data synchronization, and scalable integrations with ERP, MES, and quality systems. These solutions currently account for 48% of total adoption, driven by lower IT overhead, faster deployment, and superior interoperability compared to legacy systems.

AI-enabled PLM systems are the fastest-growing type at approximately 18% CAGR, propelled by rising demand for predictive quality analytics, automated formulation optimization, and intelligent labeling validation. Food companies increasingly use machine learning to reduce reformulation cycles, predict shelf life, and preempt compliance risks before products reach production.

Digital-twin-integrated PLM platforms are gaining traction in high-volume processing environments, allowing manufacturers to simulate production scenarios before physical trials. This segment holds about 17% of current adoption, with strong uptake in dairy, beverages, and packaged foods.

On-premise enterprise PLM remains relevant for large firms with strict data residency requirements, particularly in regulated markets, representing roughly 12% of usage. Meanwhile, modular SaaS PLM tools focused on niche functions—such as specification management or supplier portals—collectively contribute 23% combined share, serving mid-sized firms that prefer incremental digital upgrades rather than full enterprise overhauls.

Formulation and recipe management is the leading application area, representing 46% of market utilization, as companies prioritize consistent taste, nutrition, and cost optimization across multiple regions. Centralized digital formulation systems reduce variability and enable faster localization of products for different markets.

Compliance and traceability management is the fastest-growing application at about 17% CAGR, fueled by stricter labeling laws, allergen disclosure rules, and mandatory digital record-keeping requirements in the U.S. and EU. Automated audit trails and real-time ingredient tracking are becoming standard capabilities.

Production optimization and quality control together account for roughly 29% combined share, as manufacturers integrate PLM with IoT sensors to monitor temperature, contamination risks, and process deviations in real time.

Supplier collaboration platforms, representing about 15% of usage, are increasingly critical for managing ingredient sourcing, sustainability data, and procurement transparency. In 2025, more than 40% of global food manufacturers reported piloting integrated PLM–MES systems to improve product launch timelines and reduce compliance risk. Over 58% of large retailers now prefer suppliers that use digital PLM platforms for transparent ingredient documentation and recall readiness.

Large multinational food processors dominate end-user adoption, accounting for 52% of total PLM usage, as they require enterprise-wide data integration, global compliance alignment, and real-time multi-plant coordination. These firms typically manage tens of thousands of SKUs and rely on PLM as a core operational system.

Mid-sized regional manufacturers are the fastest-growing end-user segment at around 16% CAGR, driven by declining SaaS costs, easier cloud deployments, and rising retailer compliance demands. Many are transitioning from spreadsheets to modular PLM solutions focused on labeling accuracy and supplier management.

Ingredient suppliers and flavor houses represent about 18% combined share, using PLM to manage complex formulations, regulatory documentation, and cross-border ingredient approvals.

Packaging producers and co-packers contribute roughly 15% collectively, with growing use of PLM for material traceability, sustainability reporting, and customer collaboration. In 2025, nearly 37% of mid-sized food firms reported piloting cloud PLM tools to improve labeling compliance and reduce product rework. Around 55% of large processors are integrating PLM with IoT quality monitoring systems to minimize spoilage and recalls.

North America accounted for the largest market share at 41.2% in 2025, however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 18.4% between 2026 and 2033.

North America’s dominance is supported by high PLM penetration across large food processors, with over 65% of tier-1 manufacturers using integrated PLM–ERP–MES systems. Europe followed with a 29.6% share in 2025, driven by regulatory digitization and sustainability reporting mandates across the EU. Asia-Pacific held approximately 21.4% share in 2025, translating to a market value of about USD 266.4 million, supported by rapid industrialization and digital transformation of food plants in China and India. South America and Middle East & Africa together accounted for nearly 7.8% share, where adoption is rising gradually through export-oriented food processing and compliance modernization initiatives.

North America represented approximately 41.2% of the global Product Lifecycle Management (PLM) Software for Food Manufacturing Market in 2025, making it the largest regional contributor. Demand is driven by large-scale packaged food, dairy, meat processing, and beverage manufacturers managing tens of thousands of SKUs. Regulatory frameworks such as FSMA have accelerated digital recordkeeping, with nearly 70% of medium-to-large food plants now operating electronic specification and traceability systems. Technologically, the region leads in AI-enabled formulation optimization, digital twins, and cloud-native PLM adoption. Local players and system integrators are increasingly offering pre-configured compliance modules tailored for allergen tracking and recall readiness. Consumer behavior shows higher enterprise adoption of integrated digital platforms, with North American food manufacturers prioritizing speed-to-market, transparency, and audit readiness across multi-plant operations.

Europe accounted for nearly 29.6% of the global market share in 2025, with Germany, the UK, France, and Italy as key contributors. EU-wide regulations on traceability, food labeling, and sustainability reporting have driven PLM adoption, particularly for compliance documentation and supplier transparency. Over 60% of large European food enterprises have embedded PLM within sustainability and carbon-reporting workflows. Emerging technologies such as explainable AI, digital product passports, and lifecycle carbon tracking are increasingly integrated into PLM platforms. Local software providers focus on modular PLM tailored to regulatory audits. Regional consumer behavior reflects strong regulatory pressure, resulting in high demand for transparent, auditable, and explainable digital lifecycle systems.

Asia-Pacific ranked third by share but first by growth momentum, holding 21.4% of the global market in 2025, equivalent to a market value of approximately USD 266.4 million. China, India, and Japan are the largest consuming countries, supported by rapid expansion of food processing capacity and export-oriented manufacturing. Over 45% of new food plants commissioned since 2022 in China and India include cloud-based PLM or digital quality platforms at launch. Manufacturing trends emphasize automation, smart factories, and centralized formulation management. Regional innovation hubs in China, Japan, and South Korea are advancing AI-assisted quality analytics and supplier digitization. Consumer behavior is shaped by fast-growing e-commerce food channels, pushing manufacturers toward faster product iteration and real-time compliance visibility.

South America accounted for approximately 4.6% of the global market in 2025, led by Brazil and Argentina. Growth is supported by strong agricultural processing, meat exports, and packaged food industries targeting North American and European markets. Infrastructure upgrades in food plants and cold-chain facilities are increasing the need for digital documentation and traceability systems. Government-backed export compliance programs have encouraged adoption of digital quality and specification tools. Local technology providers focus on cost-efficient PLM modules for labeling and supplier data management. Consumer behavior shows demand tied to export standards and language localization for international labeling requirements.

The Middle East & Africa region held nearly 3.2% market share in 2025, with demand concentrated in the UAE, Saudi Arabia, and South Africa. Food security initiatives and import substitution strategies are encouraging investment in local food manufacturing. Governments are supporting digital modernization through smart industry and trade partnership programs. PLM adoption is increasing in dairy, bakery, and halal-certified food production to ensure compliance and export readiness. Regional players focus on cloud-based PLM deployments to overcome infrastructure constraints. Consumer behavior reflects rising preference for traceable and locally produced food, reinforcing demand for transparent digital lifecycle systems.

United States – 34.8% Market Share: High concentration of large-scale food processors, advanced digital infrastructure, and strong regulatory enforcement driving enterprise PLM adoption.

Germany – 11.2% Market Share: Strong manufacturing base, stringent EU food regulations, and high adoption of digital quality and lifecycle management systems across food production facilities.

The competitive environment in the Product Lifecycle Management (PLM) Software for Food Manufacturing Market is robust, with 30+ active global competitors ranging from enterprise software giants to specialized PLM innovators. The market retains a somewhat fragmented structure, yet the top 5 companies collectively account for approximately 58–62% of overall supplier influence, reflecting a balance between established leaders and emerging challengers. Major players position themselves through strategic initiatives such as AI integration, digital twin capabilities, cloud-native deployments, cross-platform interoperability, and deep industry-specific toolkits for formulation, traceability, and compliance. For instance, enterprise software firms are increasingly extending their PLM suites to support AI-enabled formulation matching, multi-country label automation, and real-time ingredient traceability, enhancing food-grade compliance systems.

Innovation trends include enhanced cloud collaboration modules, predictive analytics embedded within lifecycle workflows, and visual product boards to accelerate assortment planning and SKU rationalization. Companies are actively pursuing partnerships and alliances to expand PLM ecosystems—for example through ERP–PLM integration, regulatory database linkages, and expanded supplier connectivity networks that support over 220+ regulatory libraries. Furthermore, product launches and feature expansions focused on streamlined audit readiness, sustainability tracking, and digital quality convergence are reshaping competitive dynamics. Mid-tier and niche PLM vendors often differentiate with cloud-first modular suites tailored to mid-sized processors and co-packers, while enterprise incumbents prioritize global compliance, multi-language support, and seamless digital threads across R&D, quality, and manufacturing. Overall, the market remains competitive and innovation-driven, with companies striving for both depth in food manufacturing workflows and breadth across enterprise lifecycle management capabilities.

Dassault Systèmes

SAP SE

Autodesk Inc.

Aras Corporation

Aptean

Propel Software

Oracle PLM Solutions

IBM Corporation

Synergis Technologies

Arena Solutions

InfinityQS

DELMIA PLM

Technology is a defining competitive advantage in the Product Lifecycle Management (PLM) Software for Food Manufacturing Market, with decision-makers prioritizing capabilities that combine real-time data integration, advanced analytics, AI-driven automation, and cloud scalability. AI enhancements are being embedded to automate formulation management, optimize least-cost recipes, and streamline ingredient substitutions without manual recoding, supporting quality engineers and product developers in agile decision-making. Visual and collaborative technologies such as interactive product boards are enabling cross-functional planning from R&D through commercialization, improving SKU rationalization and reducing assortment development complexity in multi-category portfolios.

Cloud-native architectures continue to proliferate across PLM platforms, enabling distributed teams and supplier networks to collaborate on a single digital thread, eliminating data silos and manual reconciliation. These architectures also support multi-language and multi-regional compliance workflows, with automated regulatory libraries that track requirements across over 200+ jurisdictions, simplifying global label generation and audit readiness. Digital twin technologies, while more prevalent in discrete manufacturing, are increasingly applied within lifecycle contexts to simulate batch production variations, equipment adjustments, and quality outcomes before physical execution, reducing production trials and minimizing quality deviations.

Integration standards—encompassing ERP, MES, LIMS, and QMS systems—are advancing, enabling seamless interoperability that preserves product identity and traceability across supply chain nodes. Decision-makers are adopting API-led connectivity, open data models, and standardized schema libraries to support supplier enablement, smarter recall response playbooks, and unified master data governance. Predictive analytics, embedded within modern PLM engines, are enabling trend forecasting, anomaly detection in product quality indicators, and proactive scenario planning, giving food manufacturers an advanced view of risk and opportunity. Overall, technology trends are aligning PLM more closely with enterprise digital transformation strategies that emphasize speed-to-market, compliance assurance, and digital continuity across the full product lifecycle.

• In June 2025, Centric Software® was awarded the FoodTech Innovation Tastech Award at the Food 4 Future Expo in Bilbao, Spain, recognizing its Centric PLM™ solution as the most innovative digital technology tailored for food & beverage brands, retailers, and producers. The award highlights industry leadership in integrating formulation, compliance, and collaboration workflows. Source: www.centricsoftware.com

• In July 2025, Centric PLM™ was named a representative vendor in Gartner’s 2025 Market Guide for PLM in Food and Beverage Industries, acknowledging its unified platform for formulation, specifications, ingredient data, and regulatory compliance—accelerating development and reducing product complexity. Source: www.centricsoftware.com

• In August 2025, Centric Software announced powerful AI-driven feature updates and a breakthrough compliance engine in its Centric PLM™ platform, including intelligent supplier collaboration tools, a new mobile app, embedded AI workflows, and enhanced sustainability tracking—designed to boost performance and reduce time-to-market for food manufacturers and grocery retailers. Source: www.centricsoftware.com

• In October 2025, SAP’s Integrated Product Development received an update with new PLM capabilities including improved change management tools like the Configure Tags app and enhanced problem tracking to help teams categorize and control product revisions more efficiently within SAP’s PLM ecosystem. Source: www.linkedin.com

The scope of the Product Lifecycle Management (PLM) Software for Food Manufacturing Market Report encompasses an extensive analysis of the technologies, solutions, and industry drivers shaping digital lifecycle management across the food value chain. The report covers a broad array of PLM deployment models—including cloud-native, on-premise, and hybrid architectures—and examines functional modules such as formulation management, nutritional labeling, regulatory compliance, specification control, supplier collaboration, and SKU rationalization. It segments the market by technology type, exploring traditional PLM platforms as well as emerging AI-enabled systems that offer predictive analytics, visual planning boards, and automated quality checkpoints.

Geographically, the report analyzes regional ecosystems across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting adoption patterns, regulatory influences, technological readiness, and use-case variations across mature and developing food manufacturing markets. It also profiles key end-user segments including large-scale processors, mid-sized manufacturers, ingredient suppliers, co-packers, and packaging producers, detailing how PLM is deployed to support digital transformation efforts, compliance assurance, and product innovation priorities.

The report further evaluates integration trends, including the convergence of PLM with ERP, MES, LIMS, and QMS systems, as well as data interoperability frameworks that enable seamless digital threads across product lifecycle stages. It identifies niche and emerging segments such as blockchain-enabled traceability networks, digital twin simulations for batch production planning, and lifecycle carbon footprint tracking, all of which are gaining traction as food manufacturers pursue resilience, transparency, and sustainability goals. The scope also covers competitive landscapes, strategic initiatives like partnerships and acquisitions, and regional regulatory drivers that influence PLM adoption, offering decision-makers a comprehensive view of market evolution and operational priorities within the food manufacturing sector.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,245.0 Million |

| Market Revenue (2033) | USD 4,003.5 Million |

| CAGR (2026–2033) | 15.72% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | PTC Inc. PLM Solutions, Siemens Digital Industries Software, Centric Software® PLM, Dassault Systèmes, SAP SE, Autodesk Inc., Aras Corporation, Aptean, Propel Software, Oracle PLM Solutions, IBM Corporation, Synergis Technologies, Arena Solutions, InfinityQS, DELMIA PLM |

| Customization & Pricing | Available on Request (10% Customization Free) |