Reports

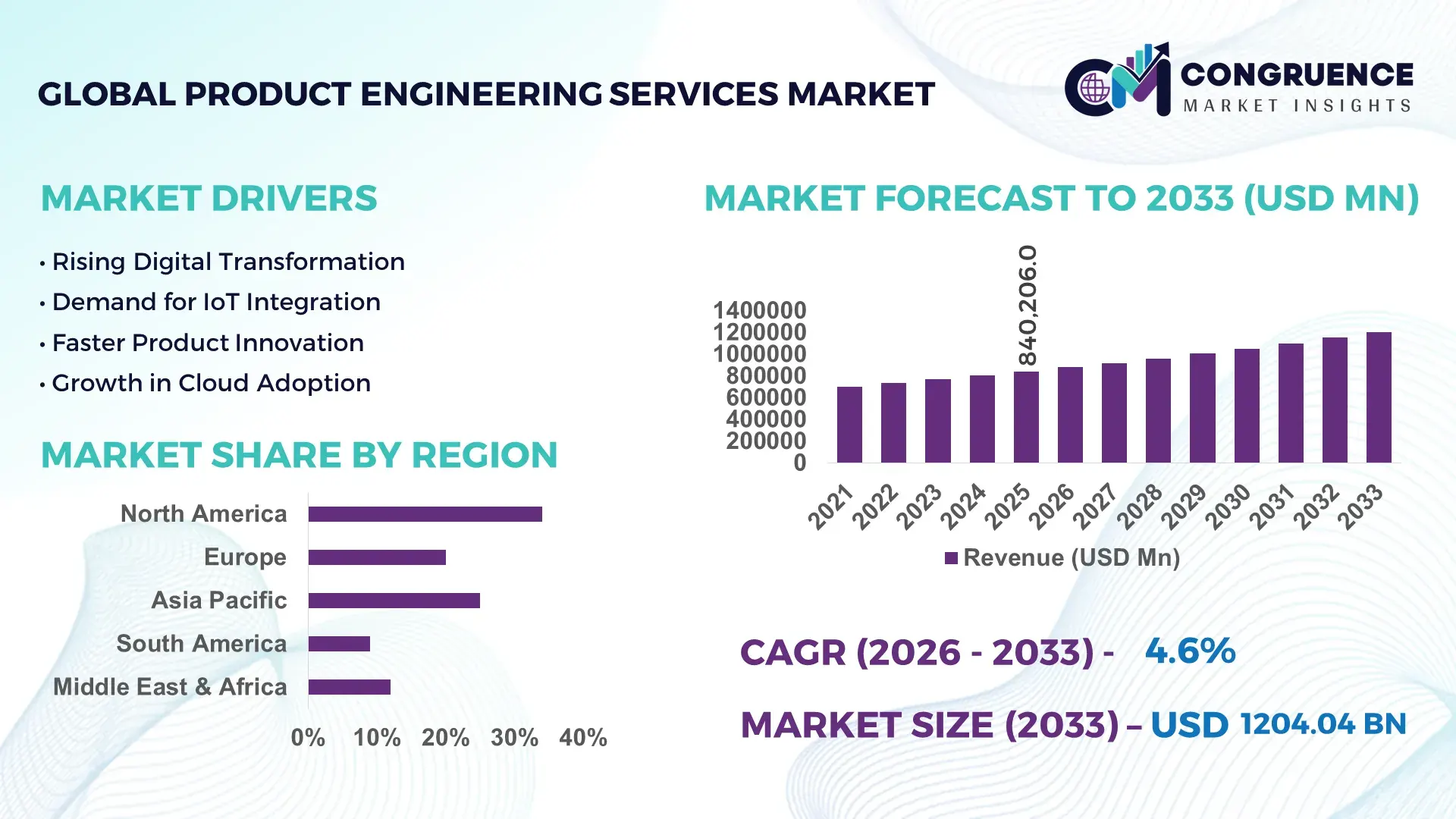

The Global Product Engineering Services Market was valued at USD 840205.98 Million in 2025 and is anticipated to reach a value of USD 1204035.37 Million by 2033 expanding at a CAGR of 4.6% between 2026 and 2033. Growth is being driven by accelerated digital product development, AI-enabled engineering workflows, software-defined products, semiconductor innovation programs, and increasing outsourcing of complex R&D functions across automotive, healthcare, industrial automation, and consumer electronics sectors.

The United States remains the dominant country, accounting for approximately 32% of global product engineering services activity in 2026, supported by strong investments in semiconductor manufacturing, aerospace systems, and software-defined mobility platforms. Compared with Germany, where engineering outsourcing penetration remains below 20% in several industrial segments, U.S. enterprises deploy advanced digital engineering tools at rates exceeding 65%. Ongoing technology realignment following global supply-chain diversification and strategic manufacturing localization initiatives continues to strengthen engineering service demand across high-value industries.

Organizations that align engineering partnerships with AI-driven design, embedded software capabilities, and rapid product commercialization strategies are positioned to capture higher innovation efficiency and faster market entry.

Market Size & Growth: USD 840205.98 Million in 2025 rising to USD 1204035.37 Million by 2033 at 4.6% CAGR, driven by AI-enabled product development and software-defined engineering programs.

Top Growth Drivers: AI engineering adoption (+28%), embedded software demand (+24%), and smart manufacturing integration (+21%) are accelerating project volumes.

Short-Term Forecast: By 2028, engineering cycle times are expected to decline by 18% while prototype validation efficiency improves by 22%.

Emerging Technologies: Generative AI, digital twins, and model-based systems engineering are improving development productivity by 15–30%.

Regional Leaders: North America exceeds USD 360 Billion, Europe approaches USD 290 Billion, and Asia-Pacific surpasses USD 420 Billion, supported by advanced R&D expansion.

Consumer/End-User Trends: More than 62% of enterprises prioritize connected, software-driven products requiring continuous engineering support.

Pilot/Case Example: In 2026, an AI-assisted industrial equipment development program reduced design iterations by 27% and testing costs by 19%.

Competitive Landscape: Leading providers collectively control nearly 35% of organized market activity, with major participation from global engineering specialists and technology consultancies.

Regulatory & ESG Impact: Digital engineering platforms support up to 20% reduction in product lifecycle emissions and improve compliance traceability.

Investment & Funding: Annual investments exceed USD 40 Billion, focused on engineering centers, automation platforms, and strategic technology partnerships.

Innovation & Future Outlook: Autonomous design systems, cloud-native engineering environments, and advanced simulation platforms are reshaping competitive differentiation.

Product Engineering Services Market demand is expanding across software-defined vehicles, medical devices, industrial automation systems, connected consumer electronics, and smart infrastructure applications. AI-assisted engineering platforms now improve design productivity by approximately 25%, while digital twin integration accelerates validation cycles. Supply-chain resilience programs and regional manufacturing expansion are increasing demand for localized engineering expertise, creating new opportunities for specialized service providers and setting the stage for deeper strategic market analysis.

Product engineering services have become a strategic lever for competitive differentiation as manufacturers and technology companies accelerate product innovation while reducing development timelines. Supply-chain restructuring, software-defined product architectures, and increasing digital adoption are shifting engineering from a support function to a core business capability. Organizations are using external engineering expertise to access specialized skills in AI, embedded systems, cloud integration, and advanced simulation without expanding fixed-cost structures.

Technology modernization is generating measurable operational advantages. AI-assisted design environments and digital engineering platforms reduce product development cycles by nearly 25% compared with traditional engineering workflows while lowering prototype iterations by approximately 20%. The United States leads in software-centric engineering deployment, whereas Germany maintains strength in industrial design and manufacturing integration. In India, engineering service hubs continue expanding due to strong talent availability and increasing adoption of model-based engineering frameworks across automotive and industrial sectors.

A practical example is the deployment of digital twin technology in industrial equipment development, enabling faster validation and predictive testing before physical production. Over the next two to three years, enterprise adoption of AI-enabled engineering tools is expected to exceed 60% among large manufacturers. Companies are increasing investments in engineering centers, strategic partnerships, and platform-based development ecosystems. Firms that integrate advanced engineering capabilities with scalable innovation processes will secure stronger competitive positioning and faster commercialization outcomes.

The transition toward software-defined products across automotive, healthcare, industrial automation, and consumer electronics sectors is a primary market accelerator. More than 60% of new product programs now incorporate embedded software as a core component, while AI-enabled engineering tools improve design productivity by approximately 25% and reduce validation cycles by nearly 20%. In the United States, semiconductor and advanced manufacturing investments are increasing demand for specialized engineering expertise. This shift creates a direct need for multidisciplinary development teams, accelerating outsourcing and co-engineering models. Companies are responding through engineering center expansion, AI platform investments, and strategic technology partnerships. A notable operational insight is that firms integrating software and hardware engineering workflows achieve faster product launch schedules and stronger lifecycle profitability than organizations maintaining fragmented development structures.

A persistent shortage of highly specialized engineering talent is constraining project scalability and delivery efficiency. In advanced domains such as AI, cybersecurity, and embedded systems, vacancy rates frequently exceed 15%, while engineering labor costs have increased by roughly 10–18% across major technology hubs. Supply-chain localization initiatives in the United States and Europe are intensifying competition for experienced technical professionals. These pressures raise project costs, extend development timelines, and reduce margin flexibility for service providers. Companies are mitigating exposure through offshore delivery networks, talent partnerships with universities, and workforce upskilling programs. A key strategic insight is that organizations with diversified engineering talent ecosystems maintain stronger utilization rates and more resilient delivery performance during periods of elevated demand.

The emergence of AI-enabled product development platforms is creating significant opportunities beyond traditional engineering outsourcing. Generative design applications can reduce engineering effort by nearly 30%, while digital twin deployment improves testing efficiency by approximately 25%. In India, increasing investments in engineering innovation centers are supporting large-scale adoption of cloud-native development frameworks. Growing demand for connected medical devices, industrial IoT systems, and autonomous technologies is expanding addressable service requirements. Companies are strengthening R&D programs, forming ecosystem partnerships, and investing in platform engineering capabilities. A non-obvious opportunity lies in lifecycle engineering services, where continuous software updates and performance optimization create recurring engagement models that extend beyond initial product development contracts.

As products incorporate AI, IoT connectivity, cloud architectures, and cybersecurity layers, engineering complexity is increasing substantially. More than 45% of enterprises report integration challenges across multi-vendor technology environments, while cybersecurity compliance requirements can add 10–15% to development workloads. In Japan and Germany, industrial manufacturers face growing pressure to modernize legacy systems without disrupting operational continuity. These challenges affect deployment consistency, product reliability, and long-term scalability. Companies must invest in systems engineering frameworks, interoperability standards, and specialized cybersecurity expertise to maintain competitiveness. A critical operational insight is that engineering providers capable of managing end-to-end integration and validation processes gain a sustainable advantage as product architectures become increasingly interconnected and software intensive.

Growing AI Engineering Adoption: Engineering teams are increasingly using AI-based design and development tools. Design productivity has improved by nearly 25%, while testing effort has declined by around 20%. Companies are integrating AI into product development workflows to accelerate launches and improve engineering efficiency amid skilled labor shortages.

Rise of Software-Defined Products: Software content in automotive systems, industrial equipment, and connected devices continues to increase. More than 60% of new product programs now require embedded software integration. Businesses are expanding software engineering capabilities and forming technology partnerships to support continuous product upgrades and faster deployment cycles.

Digital Twin Deployment Expansion: Digital twin platforms are becoming standard in product validation and performance testing. Organizations report up to 30% fewer physical prototypes and approximately 20% faster development cycles. Companies are investing in simulation-driven engineering to reduce costs, improve product reliability, and shorten time-to-market.

Shift Toward Global Engineering Hubs: Enterprises are expanding engineering operations in India and other major talent centers to improve scalability and optimize costs. Offshore engineering utilization has increased by nearly 18%, while project delivery efficiency has improved by about 15%. Companies are building dedicated engineering centers and strengthening global collaboration models to support complex product development programs.

Embedded Engineering represents the leading segment due to its critical role in connected products, automotive electronics, industrial automation systems, and smart devices. More than 45% of advanced product development programs now require embedded software and hardware integration. Its dominance is supported by strong scalability, real-time performance capabilities, and increasing demand for software-defined products. Product Design remains essential during early development stages, while Testing & Validation continues gaining importance as product complexity increases and regulatory requirements become stricter.

Sustenance Engineering is emerging as the fastest-growing segment as companies focus on extending product lifecycles, improving software updates, and reducing maintenance costs. Adoption has increased by approximately 22% across industrial and technology sectors. Prototyping remains strategically relevant for accelerating innovation cycles and reducing development risks. Companies are investing in digital engineering platforms, simulation tools, and embedded software expertise to strengthen competitive positioning and improve development efficiency.

Software Products account for the largest application segment as enterprises continue investing in cloud platforms, enterprise software, digital services, and intelligent applications. More than 55% of engineering service engagements now involve software-centric development activities. Strong demand for continuous updates, cybersecurity enhancements, and platform modernization supports sustained outsourcing activity. Connected Devices and Consumer Electronics continue expanding through IoT integration and increasing adoption of smart technologies.

Medical Devices represent the fastest-growing application area due to digital healthcare transformation and rising adoption of connected monitoring solutions. Engineering demand in this segment has increased by nearly 24% as manufacturers focus on compliance, interoperability, and product reliability. Automotive Systems and Industrial Equipment remain major contributors as software integration and automation requirements increase. Companies are expanding specialized engineering teams and investing in domain-specific expertise to support evolving application requirements.

Automotive remains the dominant end-user segment due to large-scale deployment of software-defined vehicles, advanced driver assistance systems, and vehicle connectivity technologies. More than 40% of complex engineering projects are linked to automotive development activities. High product complexity, regulatory compliance requirements, and rapid innovation cycles continue driving engineering service demand. Manufacturing and Consumer Electronics also maintain strong demand as automation and connected product adoption increase.

Healthcare is the fastest-growing end-user segment, supported by digital diagnostics, connected medical devices, and healthcare software integration. Engineering engagement levels in healthcare have increased by approximately 23% over recent years. Telecommunications continues expanding through network modernization initiatives, while Aerospace & Defense requires advanced engineering capabilities for mission-critical systems. Companies are responding through industry-specific engineering practices, strategic partnerships, and dedicated innovation centers to strengthen customer engagement and sector expertise.

North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.8% between 2026 and 2033.

Software-Driven Product Innovation Leadership

North America remains the largest market for product engineering services, supported by advanced digital engineering ecosystems, strong enterprise R&D spending, and high adoption of software-defined product architectures. The region contributes approximately 34% of global market activity, with significant deployment across aerospace, healthcare technology, industrial automation, and automotive engineering. More than 65% of large enterprises have adopted AI-assisted engineering tools to accelerate development cycles and improve product validation efficiency. Strategic investments in semiconductor manufacturing and digital infrastructure continue to strengthen engineering outsourcing demand. Companies are expanding engineering partnerships and cloud-based development frameworks to improve scalability and reduce product launch timelines.

United States Market Outlook: The United States leads regional demand through its concentration of technology companies, aerospace manufacturers, automotive innovators, and medical device developers. Over 70% of large-scale product development programs incorporate advanced simulation, AI-enabled design, or embedded software engineering. Federal investments supporting semiconductor production and industrial modernization continue to expand engineering requirements. Companies are strengthening engineering centers, increasing R&D collaboration, and adopting digital engineering platforms to support faster commercialization and product lifecycle optimization.

Industrial Digitalization and Sustainability Integration

Europe maintains a strong position through advanced manufacturing capabilities, engineering excellence, and increasing digital transformation across industrial sectors. The region accounts for nearly 28% of global demand, supported by automotive, industrial equipment, healthcare technology, and energy-transition projects. More than 55% of manufacturers are implementing model-based engineering and digital twin technologies to improve operational efficiency and regulatory compliance. Sustainability objectives are influencing product design priorities, driving demand for lifecycle engineering and validation services. Companies continue investing in smart manufacturing infrastructure and engineering automation platforms to improve development productivity.

Germany Market Outlook: Germany serves as the regional engineering hub due to its leadership in automotive production, industrial automation, and advanced manufacturing technologies. Nearly 60% of major industrial enterprises utilize digital engineering tools for product design and validation activities. Strong integration between manufacturing operations and engineering service providers supports rapid deployment of Industry 4.0 initiatives. Companies are prioritizing embedded software development, digital twins, and systems engineering capabilities to maintain technological competitiveness across export-oriented industries.

Engineering Scale and Talent Expansion

Asia-Pacific represents the fastest-expanding market, supported by large engineering talent pools, manufacturing strength, and growing digital product development activity. The region accounts for approximately 31% of global market demand and continues gaining share through investments in electronics, automotive systems, industrial automation, and telecommunications infrastructure. Engineering delivery capacity has increased by over 20% across major service hubs as enterprises expand global development operations. Strong adoption of cloud-native engineering and AI-assisted development tools is improving project efficiency. Companies are increasing investment in engineering centers and specialized technology capabilities to meet rising international demand.

India Market Outlook: India has emerged as a strategic global engineering destination due to its extensive technical workforce, digital infrastructure expansion, and strong software engineering ecosystem. More than 35% of global outsourced engineering projects involve delivery centers located in India. Enterprise investments in AI, embedded systems, and product lifecycle management platforms continue to accelerate. Companies are expanding innovation centers, strengthening university partnerships, and developing advanced engineering capabilities to support increasingly complex product development requirements.

Industrial Modernization Driving Demand

South America is experiencing steady growth as manufacturers modernize operations and increase investment in digital product development. The region accounts for approximately 4% of global market activity, supported by industrial equipment, automotive manufacturing, energy infrastructure, and telecommunications projects. Engineering service adoption has increased by nearly 15% in large enterprises seeking productivity improvements and operational modernization. Infrastructure limitations and uneven technology deployment remain challenges; however, growing enterprise digitization is creating new engineering opportunities. Companies are focusing on localized partnerships and specialized engineering expertise to support regional development requirements.

Brazil Market Outlook: Brazil dominates regional demand through its industrial base, automotive production capabilities, and expanding technology sector. Large manufacturers are increasingly deploying digital engineering tools to improve product quality and accelerate development processes. Engineering outsourcing activity has grown steadily as enterprises seek access to specialized technical expertise. Companies are investing in automation technologies, engineering partnerships, and workforce development initiatives to strengthen competitiveness and support industrial modernization programs.

Infrastructure and Technology Transformation Investments

The Middle East & Africa market is supported by infrastructure modernization, industrial diversification initiatives, and increasing technology investments. The region contributes approximately 3% of global market demand, with engineering services gaining importance across energy, telecommunications, smart city, and industrial development projects. Adoption of advanced engineering platforms has increased by nearly 18% among major enterprises pursuing digital transformation objectives. Government-backed modernization programs are supporting demand for systems engineering, product development, and industrial automation expertise. Companies are forming strategic alliances and expanding local engineering capabilities to support long-term infrastructure projects.

Saudi Arabia Market Outlook: Saudi Arabia leads regional activity through large-scale industrial diversification programs, smart infrastructure investments, and technology modernization initiatives. Industrial development projects are increasing demand for engineering design, automation integration, and digital engineering services. More than 40% of major industrial projects now incorporate advanced digital technologies during planning and deployment phases. Companies are establishing regional engineering partnerships and innovation centers to support infrastructure expansion, manufacturing growth, and technology-driven economic transformation.

The Product Engineering Services Market is characterized by competition between global engineering leaders such as Accenture, Capgemini, HCLTech, Tata Consultancy Services, Wipro, and EPAM Systems, alongside specialized engineering firms focused on embedded systems, industrial design, and product lifecycle services. The top five players collectively account for approximately 32–36% of organized market activity. Competition centers on engineering speed, domain expertise, AI-enabled development capabilities, and cost efficiency, with productivity improvements of 20–30% increasingly influencing vendor selection. Large providers compete through global delivery networks, platform-based engineering services, and strategic acquisitions, while specialized firms focus on high-value vertical expertise. Partnerships with cloud providers, semiconductor companies, and industrial technology vendors are becoming critical differentiators. Market consolidation is accelerating as enterprises prefer integrated engineering partners capable of managing complex product lifecycles. The primary entry barrier remains access to advanced engineering talent and domain-specific expertise. Winning requires scalable delivery, deep technical specialization, AI-enabled engineering capabilities, and strong customer integration.

Accenture

Capgemini

HCLTech

Tata Consultancy Services (TCS)

Wipro

Infosys

EPAM Systems

LTIMindtree

Persistent Systems

Tech Mahindra

Cognizant

Alten Group

Cyient

GlobalLogic

AI-assisted engineering platforms, digital twins, and cloud-native product development environments are reshaping product engineering workflows in 2026. More than 60% of large engineering organizations now use AI-enabled coding, testing, or design tools, improving engineering productivity by 20–30% and reducing validation effort by nearly 25%. Digital twin deployment has increased across automotive, industrial equipment, and healthcare sectors, cutting physical prototype requirements by approximately 30%. These technologies provide faster product launches, lower development costs, and stronger engineering scalability, creating measurable operational advantages for enterprises managing complex product portfolios.

Emerging technologies include generative engineering, model-based systems engineering, and AI-native software development environments. Adoption of model-based engineering has exceeded 45% among advanced manufacturers, improving system integration efficiency by nearly 18%. Compared with traditional development methods, AI-supported engineering workflows deliver approximately 25% faster design iterations and 20% higher engineering throughput. Companies are integrating engineering data platforms, simulation environments, and automated compliance frameworks to improve collaboration across global development teams while reducing deployment risks.

Disruptive technologies such as agentic AI, autonomous testing systems, and intelligent engineering copilots are expected to transform development practices between 2026 and 2028. Engineering providers with strong AI integration capabilities are gaining competitive advantage as enterprises prioritize automation and platform-based delivery. Organizations that accelerate adoption today can achieve 15–20% improvements in development speed, positioning themselves ahead of competitors relying on legacy engineering models.

October 2024 – Capgemini launched augmented engineering offerings powered by generative AI to accelerate engineering and R&D processes. The platform targets high-level automation across product development workflows, improving engineering efficiency and innovation speed. This strengthened Capgemini’s intelligent industry positioning and engineering automation capabilities. Source: capgemini.com

November 2024 – Capgemini was recognized as a global leader across engineering, digital engineering, AI engineering, and Industry 4.0 services among more than 75 evaluated ER&D providers. The recognition reinforced its competitive position across automotive, aerospace, semiconductor, and software engineering markets. Source: capgemini.com

January 2026 – EPAM Systems entered a strategic partnership with Cursor to scale AI-native engineering teams globally. The initiative supports deployment across thousands of developers, enabling measurable productivity improvements and faster adoption of AI-driven software engineering workflows for enterprise customers. Source: epam.com

March 2026 – HCLTech expanded its collaboration with Google Cloud to accelerate Agentic AI adoption. The program supports over 2,000 GenAI-led customer engagements and integrates AI agents into enterprise workflows, strengthening automation, engineering productivity, and digital transformation outcomes. Source: hcltech.com

The report provides comprehensive coverage of the Product Engineering Services Market across key service types including Product Design, Prototyping, Testing & Validation, Embedded Engineering, and Sustenance Engineering. It evaluates demand patterns across Software Products, Connected Devices, Industrial Equipment, Automotive Systems, Consumer Electronics, and Medical Devices while assessing adoption trends among Automotive, Healthcare, Manufacturing, Telecommunications, Aerospace & Defense, and Consumer Electronics organizations. The study analyzes engineering deployment models, digital transformation initiatives, AI integration rates, and evolving product development strategies influencing market dynamics.

The report delivers detailed regional assessment across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, covering operational trends, engineering capacity expansion, and technology adoption patterns. More than 60% of enterprise engineering programs now incorporate AI-enabled development tools, while embedded engineering and software-driven product development continue gaining strategic importance. The analysis supports investment prioritization, partnership evaluation, competitive benchmarking, expansion planning, and long-term positioning decisions between 2026 and 2033, with particular focus on AI-native engineering, digital twins, cloud-based development, and advanced automation ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 840205.98 Million |

|

Market Revenue in 2033 |

USD 1204035.37 Million |

|

CAGR (2026 - 2033) |

4.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Accenture, Capgemini, HCLTech, Tata Consultancy Services (TCS), Wipro, Infosys, EPAM Systems, LTIMindtree, Persistent Systems, Tech Mahindra, Cognizant, Alten Group, Cyient, GlobalLogic |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |