Reports

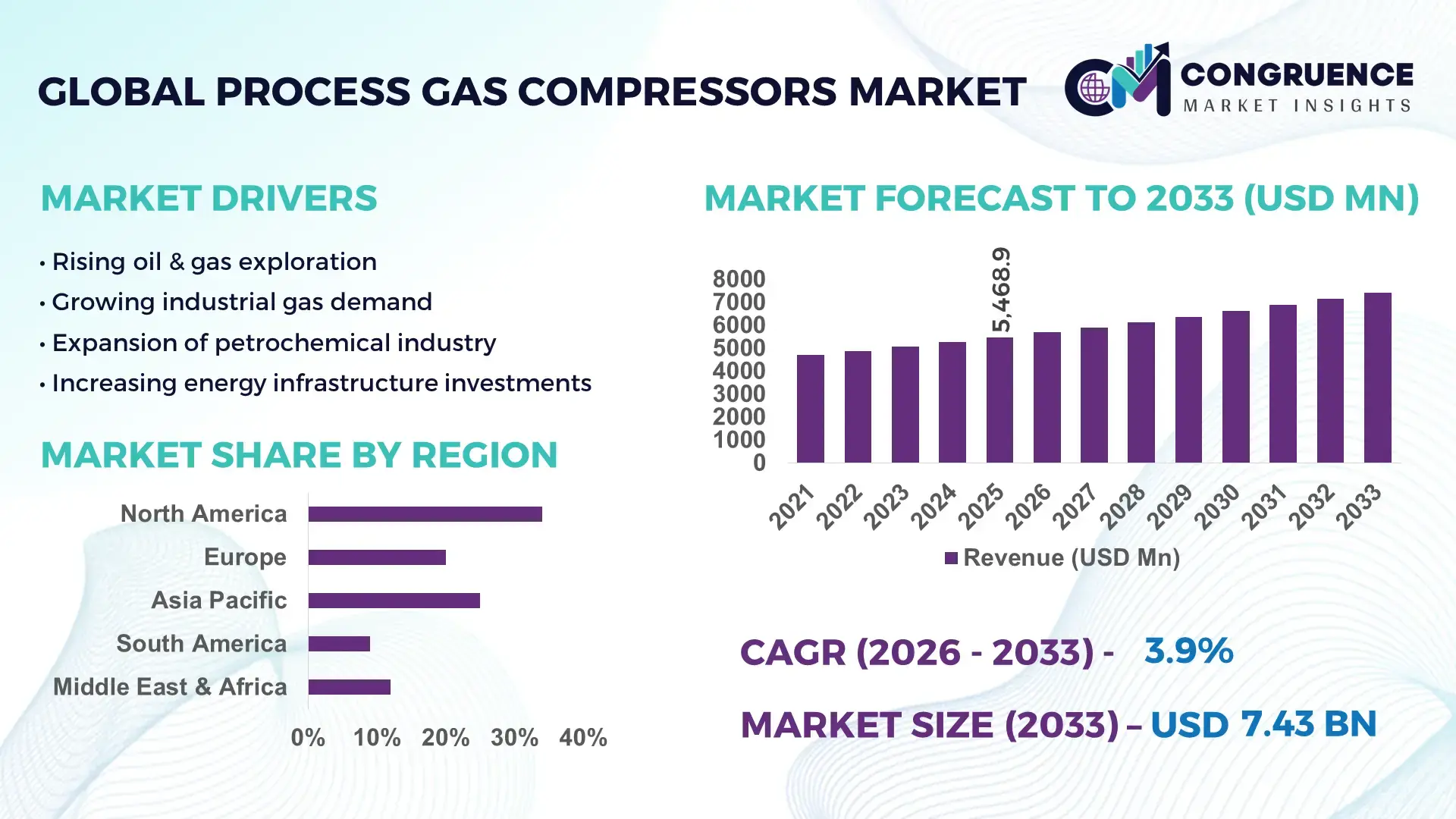

The Global Process Gas Compressors Market was valued at USD 5468.85 Million in 2025 and is anticipated to reach a value of USD 7427.12 Million by 2033 expanding at a CAGR of 3.9% between 2026 and 2033. The growth is primarily driven by the increasing deployment of high-efficiency gas compression systems across expanding petrochemical, LNG, and hydrogen processing infrastructure.

In the United States, the process gas compressors market reflects a highly developed industrial ecosystem supported by robust investments in energy and chemical processing facilities. The country operates more than 135 refineries and over 1,000 natural gas processing plants, generating continuous demand for advanced compressor systems. Capital investments exceeding USD 25 billion in LNG export infrastructure and shale gas processing have accelerated the installation of large-scale centrifugal compressors. Approximately 68% of operational gas facilities in the U.S. utilize digitally integrated compressor monitoring systems, improving reliability and uptime. Furthermore, nearly 40% of newly installed compressors incorporate oil-free and energy-efficient drive technologies, supporting stricter emission standards and operational efficiency targets across industries.

Market Size & Growth: Valued at USD 5468.85 Million in 2025 and projected to reach USD 7427.12 Million by 2033, growing at a CAGR of 3.9% driven by expanding LNG and petrochemical processing capacity.

Top Growth Drivers: Industrial gas consumption increased by 18%, LNG infrastructure expansion by 22%, and energy efficiency upgrades by 15% across major industries.

Short-Term Forecast: By 2028, predictive maintenance and smart monitoring systems are expected to reduce downtime by 25% and enhance operational efficiency by 18%.

Emerging Technologies: Rapid adoption of oil-free compressors, AI-based predictive analytics, and variable speed drive systems improving performance and sustainability.

Regional Leaders: North America projected to reach USD 2.6 billion by 2033 driven by shale gas expansion; Asia-Pacific at USD 2.3 billion due to industrial growth; Europe at USD 1.5 billion with strong decarbonization focus.

Consumer/End-User Trends: Petrochemical, oil & gas, and LNG sectors account for over 70% of compressor usage, with increasing preference for energy-efficient and low-emission systems.

Pilot or Case Example: In 2024, a large-scale LNG facility upgrade achieved 30% reduction in unplanned downtime through AI-driven compressor monitoring solutions.

Competitive Landscape: Atlas Copco leads with approximately 20% share, followed by Siemens Energy, Baker Hughes, Ingersoll Rand, and Mitsubishi Heavy Industries.

Regulatory & ESG Impact: Emission reduction policies are driving adoption of low-carbon compressors, with firms targeting up to 35% reduction in emissions by 2030.

Investment & Funding Patterns: Over USD 18 billion invested globally in gas infrastructure modernization, with increasing adoption of public-private partnerships and green financing models.

Innovation & Future Outlook: Integration of hydrogen-compatible compressors, digital twin technologies, and automation systems is shaping next-generation industrial gas compression solutions.

The process gas compressors market is strongly influenced by the oil & gas sector, which contributes nearly 45% of total demand, followed by petrochemicals at approximately 30% and power generation and industrial gases collectively accounting for over 20%. Recent innovations such as high-speed magnetic bearing compressors and oil-free centrifugal systems are improving operational efficiency by up to 20% while reducing maintenance requirements. Regulatory frameworks focused on carbon emissions and energy efficiency are pushing manufacturers toward cleaner and more sustainable compressor technologies. Asia-Pacific continues to experience rapid consumption growth due to industrial expansion, while Europe focuses on energy transition projects including hydrogen processing. Emerging trends such as digitalization, remote monitoring, and integration of AI-driven analytics are expected to redefine operational performance and lifecycle management in the coming years.

The process gas compressors market holds critical strategic relevance as industries increasingly prioritize energy efficiency, operational reliability, and low-emission production systems. Advanced compressor technologies such as magnetic bearing systems deliver nearly 30% improvement in energy efficiency compared to conventional oil-lubricated compressors, making them a preferred choice in high-demand industrial environments. North America dominates in volume due to its extensive oil & gas and LNG infrastructure, while Asia-Pacific leads in adoption with over 55% of industrial facilities integrating modern compressor technologies to support rapid industrialization.

In the short term, by 2028, AI-enabled predictive maintenance systems are expected to improve equipment reliability by 25% while reducing maintenance costs by up to 20%. Companies are increasingly aligning with environmental, social, and governance goals by targeting emission reductions of up to 35% and improving energy efficiency through electrified compression systems. For example, in 2024, a major LNG processing facility in the United States achieved a 28% reduction in operational downtime through the implementation of AI-based compressor monitoring and digital twin technology.

Strategically, the market is also witnessing increased adoption of hydrogen-compatible compressors as global energy systems transition toward cleaner fuels. Electrification of compressors and integration with renewable energy sources are becoming key investment priorities. The process gas compressors market is positioned as a critical enabler of industrial resilience, regulatory compliance, and sustainable growth, supporting both conventional and emerging energy ecosystems.

The increasing global demand for liquefied natural gas and petrochemical products is a major driver of the process gas compressors market. LNG trade volumes have grown by over 20% in recent years, necessitating advanced compression systems for gas liquefaction, transportation, and regasification. Petrochemical production capacity has expanded by more than 15% globally, with compressors playing a critical role in handling process gases such as ethylene, propylene, and hydrogen. High-capacity centrifugal compressors are widely used in LNG terminals and refineries due to their efficiency and reliability. Additionally, the shift toward cleaner fuels is encouraging the use of natural gas, further increasing the need for compression systems. Industrial facilities are also upgrading existing compressor units to improve efficiency and reduce emissions, contributing to sustained market demand.

One of the primary restraints in the process gas compressors market is the high initial investment and ongoing maintenance costs associated with advanced compressor systems. Large-scale industrial compressors can require significant capital expenditure, often exceeding millions of dollars depending on capacity and technology. Maintenance costs can account for up to 25% of total lifecycle expenses, particularly for systems operating in harsh environments such as offshore platforms and chemical plants. Additionally, the need for skilled technicians and specialized components increases operational complexity. Small and medium-sized enterprises often face financial constraints that limit their ability to invest in high-performance compressor systems. These cost-related challenges can delay equipment upgrades and impact overall market growth.

The rapid expansion of hydrogen production and clean energy initiatives presents significant opportunities for the process gas compressors market. Hydrogen demand is expected to increase by over 40% in industrial applications, requiring specialized compressors capable of handling high-pressure and low-density gases. Governments and private organizations are investing heavily in hydrogen infrastructure, including production plants and distribution networks. Advanced compressors designed for hydrogen applications are gaining traction due to their ability to operate efficiently under challenging conditions. Additionally, the integration of renewable energy sources with gas compression systems is creating new avenues for innovation. These developments are expected to drive demand for next-generation compressors that support sustainable energy systems.

Stringent environmental regulations and emission standards pose significant challenges for the process gas compressors market. Governments worldwide are implementing strict policies to reduce greenhouse gas emissions, requiring industries to adopt cleaner and more efficient technologies. Compliance with these regulations often involves upgrading existing equipment or investing in new low-emission compressor systems, which can be costly and time-consuming. Additionally, monitoring and reporting requirements add to operational complexity. For instance, industrial facilities are required to reduce methane emissions by up to 30% in certain regions, necessitating advanced sealing and monitoring technologies. These regulatory pressures can impact profitability and require continuous investment in research and development to meet evolving standards.

Digitalization and Smart Monitoring Adoption Exceeding 60% Across Industrial Facilities: The integration of IoT-enabled sensors and AI-driven predictive maintenance systems has expanded rapidly, with over 60% of large-scale gas processing plants deploying real-time monitoring solutions. These systems have demonstrated up to 25% reduction in unplanned downtime and nearly 18% improvement in operational efficiency. Advanced analytics platforms are also enabling predictive fault detection with accuracy levels exceeding 85%, significantly lowering maintenance intervals and enhancing equipment lifespan in high-pressure applications.

Accelerated Shift Toward Oil-Free and Energy-Efficient Compressors Achieving 30% Energy Savings: Oil-free compressor technologies are gaining traction, with approximately 45% of new installations incorporating oil-free designs to meet stringent emission norms. These systems reduce contamination risks and improve gas purity levels by over 90%, making them ideal for hydrogen and specialty gas applications. Energy-efficient compressors equipped with variable speed drives have achieved up to 30% reduction in energy consumption, contributing to lower operational costs and improved sustainability performance across industries.

Expansion of Hydrogen Compression Infrastructure Growing by Over 40% in Industrial Applications: The emergence of hydrogen as a clean energy source has driven demand for specialized compressors, with hydrogen-related projects increasing by more than 40% globally. High-pressure compressors capable of handling pressures above 700 bar are being widely deployed in hydrogen refueling stations and production facilities. Nearly 35% of new compressor developments are now focused on hydrogen compatibility, reflecting the growing importance of energy transition initiatives and decarbonization strategies.

Rise in Modular and Prefabricated Compressor Systems Delivering 55% Cost Efficiency Gains: Modular and prefabricated compressor units are transforming project execution strategies, with over 55% of new industrial projects reporting cost and time efficiency improvements. Prefabricated systems reduce on-site installation time by nearly 40% and minimize labor requirements through pre-engineered components. Adoption is particularly strong in North America and Europe, where approximately 50% of new gas processing facilities utilize modular compressor designs to enhance scalability, reduce downtime, and streamline commissioning processes.

The process gas compressors market is segmented based on type, application, and end-user industries, each contributing distinctively to overall demand patterns. Centrifugal and reciprocating compressors dominate the type segment due to their widespread use in large-scale gas processing and high-pressure applications. In terms of applications, oil & gas remains the primary segment, driven by extensive use in upstream, midstream, and downstream operations. Petrochemical and chemical processing sectors also contribute significantly due to their reliance on continuous gas compression systems. From an end-user perspective, energy and industrial manufacturing sectors account for the majority of installations, supported by growing infrastructure investments and increasing demand for efficient gas handling systems. The segmentation reflects a strong alignment with industrial growth, technological adoption, and evolving energy requirements across global markets.

Centrifugal compressors currently lead the process gas compressors market, accounting for approximately 48% of total adoption due to their high efficiency, continuous operation capability, and suitability for large-scale applications such as LNG and petrochemical plants. Reciprocating compressors hold around 32% share, widely used in high-pressure and low-flow applications, particularly in gas transmission and storage. However, screw compressors are emerging as the fastest-growing segment, expanding at an estimated CAGR of 5.6%, driven by their compact design, lower maintenance requirements, and increasing adoption in medium-capacity industrial processes.

Other compressor types, including diaphragm and rotary vane compressors, collectively contribute nearly 20% of the market, serving niche applications such as specialty gas handling and laboratory-scale operations. Technological advancements in magnetic bearing systems and oil-free compression are further enhancing the performance of these specialized compressors.

The oil & gas sector dominates the application segment, accounting for approximately 45% of total compressor usage due to extensive requirements in gas extraction, processing, and transportation. Petrochemical applications follow with nearly 30% share, where compressors are essential for handling process gases such as ethylene and propylene. However, hydrogen and clean energy applications are emerging as the fastest-growing segment, expanding at an estimated CAGR of 6.2%, driven by global decarbonization initiatives and increasing investment in hydrogen production and distribution infrastructure.

Other applications, including power generation and industrial manufacturing, collectively represent around 25% of the market, with steady demand for gas compression in energy generation and process industries. The diversification of applications is also supported by advancements in compressor efficiency and adaptability to different gases and operating conditions.

The energy sector, including oil & gas and power generation, leads the end-user segment with approximately 50% share, driven by extensive infrastructure and continuous demand for gas compression systems. The chemical and petrochemical industries account for around 30% of adoption, relying heavily on compressors for process efficiency and safety in handling volatile gases. Meanwhile, the industrial manufacturing sector is the fastest-growing end-user segment, expanding at an estimated CAGR of 5.1%, supported by increasing automation and demand for efficient gas handling systems in production processes.

Other end-users, including food processing, pharmaceuticals, and specialty gas industries, collectively contribute about 20% of the market, with growing adoption of oil-free compressors to meet stringent purity and safety standards. Industry adoption rates indicate that over 65% of large-scale industrial facilities have already integrated advanced compressor technologies to enhance productivity and reduce operational costs.

Region North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2026 and 2033.

North America’s dominance is supported by over 1,000 operational gas processing facilities and more than 135 refineries, driving consistent demand for high-capacity compressors. Europe follows with approximately 27% share, driven by strict emission standards and over 60% adoption of energy-efficient compressor systems across industrial plants. Asia-Pacific holds nearly 29% share, with China and India contributing over 65% of regional demand due to rapid industrialization and infrastructure expansion. The Middle East & Africa accounts for around 6%, supported by oil production exceeding 30 million barrels per day, while South America contributes close to 4%, with Brazil alone representing over 55% of regional compressor installations. Increasing investments in LNG terminals, hydrogen projects, and digital monitoring technologies are further shaping regional dynamics, with over 50% of new installations globally incorporating smart monitoring systems.

How are advanced industrial systems reshaping demand for high-efficiency gas compression technologies?

North America holds approximately 34% of the global process gas compressors market, driven by strong demand from oil & gas, petrochemical, and LNG sectors. The region operates more than 70 LNG facilities and over 1,000 gas processing plants, contributing to high equipment utilization rates. Regulatory frameworks targeting methane emission reductions of up to 30% are pushing industries toward energy-efficient and low-emission compressor technologies. Digital transformation is highly advanced, with nearly 65% of facilities adopting IoT-enabled monitoring and predictive maintenance systems, improving operational efficiency by over 20%. A leading player in the region has implemented AI-based compressor diagnostics, reducing maintenance costs by 18% across multiple facilities. Consumer behavior in this region reflects high enterprise adoption, with over 75% of large industrial operators prioritizing automation and performance optimization in compressor systems.

Why are sustainability mandates accelerating adoption of energy-efficient compression systems?

Europe accounts for approximately 27% of the process gas compressors market, with Germany, the UK, and France serving as key industrial hubs. Over 60% of industrial facilities in the region have transitioned to energy-efficient compressor technologies to comply with strict environmental regulations targeting carbon emission reductions of up to 40% by 2030. The European market is characterized by rapid adoption of oil-free compressors, with nearly 50% of new installations meeting stringent air quality and emission standards. Advanced technologies such as variable speed drives and digital twins are increasingly integrated, improving system efficiency by up to 22%. A prominent regional manufacturer has introduced hydrogen-compatible compressors, supporting over 100 clean energy projects across the continent. Consumer behavior reflects strong regulatory influence, with more than 70% of enterprises prioritizing sustainability and compliance-driven investments in compressor systems.

What factors are accelerating industrial-scale adoption of gas compression systems across manufacturing hubs?

Asia-Pacific represents nearly 29% of the global process gas compressors market and ranks as the fastest-growing region in terms of volume expansion. China, India, and Japan collectively account for over 65% of regional demand, driven by rapid industrialization and expanding energy infrastructure. The region has witnessed more than 40% increase in petrochemical production capacity, directly boosting compressor demand. Manufacturing trends indicate that over 55% of new industrial plants are incorporating advanced compression systems with digital monitoring capabilities. Innovation hubs in China and Japan are leading in the development of high-speed, energy-efficient compressors, improving operational efficiency by up to 25%. A leading regional manufacturer has deployed modular compressor units across 200+ facilities, reducing installation time by 35%. Consumer behavior is characterized by strong demand for cost-efficient and scalable solutions, with over 60% of enterprises opting for modular systems.

How is energy sector expansion influencing demand for industrial gas compression solutions?

South America holds approximately 4% of the global process gas compressors market, with Brazil and Argentina emerging as key contributors. Brazil alone accounts for over 55% of regional installations, supported by its extensive oil & gas and biofuel production activities. The region’s energy sector has seen a 20% increase in upstream exploration activities, driving demand for high-pressure compressors. Government incentives promoting domestic energy production and infrastructure upgrades are further supporting market growth. Technological adoption is moderate, with around 40% of facilities integrating digital monitoring systems to improve efficiency. A regional energy company recently upgraded its gas compression systems, achieving a 15% improvement in operational efficiency. Consumer behavior indicates demand closely tied to energy sector performance, with industrial operators focusing on cost-effective and durable compressor solutions.

Why is large-scale hydrocarbon production driving demand for advanced compression technologies?

The Middle East & Africa accounts for nearly 6% of the global process gas compressors market, driven by extensive oil & gas production activities exceeding 30 million barrels per day. Countries such as the UAE and Saudi Arabia are leading investments in gas processing and petrochemical infrastructure, with over 25 major projects currently under development. Technological modernization is accelerating, with approximately 45% of new installations incorporating advanced compression systems designed for high-temperature and high-pressure environments. Regional regulations are increasingly focusing on emission reduction, with targets of up to 25% reduction in flaring activities. A major regional operator has deployed high-efficiency compressors across multiple facilities, improving gas recovery rates by 20%. Consumer behavior reflects a strong preference for high-capacity and durable systems capable of operating in extreme conditions.

United States – 28% share: Process Gas Compressors market leadership driven by extensive oil & gas infrastructure and over 1,000 gas processing facilities.

China – 22% share: Process Gas Compressors market growth supported by rapid industrialization and over 40% expansion in petrochemical production capacity.

The process gas compressors market is moderately consolidated, with over 35 active global and regional competitors operating across various product segments. The top five companies collectively account for approximately 52% of the total market share, reflecting a competitive yet structured industry landscape. Key players are focusing on strategic initiatives such as mergers, acquisitions, and partnerships to strengthen their market position and expand global reach. Over the past three years, more than 20 strategic collaborations have been recorded, particularly in the areas of digital monitoring and energy-efficient compressor technologies.

Product innovation remains a critical competitive factor, with companies investing heavily in research and development to introduce advanced solutions such as oil-free compressors, magnetic bearing systems, and AI-enabled predictive maintenance platforms. Nearly 60% of leading manufacturers have integrated digital technologies into their product portfolios, enhancing performance and reducing lifecycle costs. Additionally, customization and modular solutions are gaining prominence, with over 45% of new product launches focusing on scalable and prefabricated compressor systems. Competitive differentiation is increasingly based on energy efficiency, reliability, and compliance with environmental regulations, shaping the overall market dynamics.

Atlas Copco

Siemens Energy

Baker Hughes

Ingersoll Rand

Mitsubishi Heavy Industries

Howden Group

Gardner Denver

Ariel Corporation

MAN Energy Solutions

Burckhardt Compression

Kobe Steel Ltd.

Hitachi Industrial Equipment Systems

Technological advancements in the process gas compressors market are increasingly focused on improving energy efficiency, operational reliability, and environmental compliance. One of the most significant developments is the adoption of oil-free compression technology, which now accounts for nearly 45% of new installations across industries such as petrochemicals and hydrogen processing. These systems eliminate contamination risks and enhance gas purity levels by over 90%, making them critical for high-specification applications.

The integration of digital technologies, including IoT-enabled sensors and AI-based predictive maintenance platforms, has transformed compressor operations. More than 60% of large-scale industrial facilities have implemented smart monitoring systems capable of detecting faults with over 85% accuracy, reducing unplanned downtime by up to 25%. Digital twin technology is also gaining traction, enabling real-time simulation and performance optimization, with efficiency improvements reaching approximately 20% in complex gas processing environments.

Variable speed drive (VSD) systems are another key innovation, allowing compressors to operate at optimized load conditions. These systems have demonstrated energy savings of up to 30%, particularly in fluctuating demand scenarios. Additionally, magnetic bearing technology is being increasingly adopted in high-speed compressors, reducing mechanical friction and maintenance requirements by nearly 35% while extending equipment lifespan.

Emerging technologies are also supporting the transition toward clean energy. Hydrogen-compatible compressors capable of operating at pressures exceeding 700 bar are being widely deployed, with over 35% of new product developments focused on hydrogen applications. Furthermore, modular and prefabricated compressor systems are improving deployment efficiency, reducing installation time by approximately 40%. These technological advancements are collectively reshaping the market by enabling higher performance, lower emissions, and greater operational flexibility.

In March 2025, Atlas Copco launched an advanced oil-free centrifugal compressor platform designed for hydrogen and specialty gas applications, achieving up to 20% higher energy efficiency and reducing maintenance intervals by 15%, supporting cleaner industrial operations. Source: www.atlascopco.com

In November 2024, Siemens Energy introduced a digitally integrated compressor solution featuring real-time monitoring and predictive analytics, enabling up to 25% reduction in unplanned downtime across gas processing facilities and improving lifecycle performance. Source: www.siemens-energy.com

In July 2025, Baker Hughes expanded its portfolio with high-pressure hydrogen compressors capable of operating above 700 bar, enhancing gas handling efficiency by 30% and supporting large-scale hydrogen infrastructure projects globally. Source: www.bakerhughes.com

In September 2024, Mitsubishi Heavy Industries deployed next-generation centrifugal compressors with magnetic bearing technology in LNG facilities, reducing energy consumption by 18% and lowering maintenance requirements through frictionless operation. Source: www.mhi.com

The Process Gas Compressors Market Report provides a comprehensive analysis of key industry segments, technological advancements, and regional dynamics shaping global demand. The scope encompasses detailed segmentation by compressor type, including centrifugal, reciprocating, screw, and specialized compressors, which collectively address over 90% of industrial gas compression requirements. The report also examines a wide range of applications, with oil & gas accounting for approximately 45% of demand, followed by petrochemicals at 30%, and emerging sectors such as hydrogen and clean energy contributing over 15%.

Geographically, the report covers major regions including North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, representing 100% of global industrial activity related to gas compression systems. Asia-Pacific alone contributes nearly 29% of demand, while North America leads with approximately 34% share due to its extensive energy infrastructure. The report further explores regional consumption patterns, infrastructure investments, and regulatory influences that impact market development.

Technological coverage includes digital monitoring systems, oil-free compression, variable speed drives, and hydrogen-compatible technologies, with over 60% of modern installations incorporating at least one advanced feature. The report also highlights emerging trends such as modular compressor systems, which are utilized in more than 50% of new industrial projects to improve scalability and reduce deployment time.

In addition, the scope includes analysis of end-user industries such as energy, chemicals, manufacturing, and specialty gases, along with insights into operational efficiency improvements, which have reached up to 30% through technology integration. The report is designed to support strategic decision-making by offering a structured and data-driven overview of market dynamics, innovation pathways, and industry-specific demand trends.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

3.9% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Atlas Copco, Siemens Energy, Baker Hughes, Ingersoll Rand, Mitsubishi Heavy Industries, Howden Group, Gardner Denver, Ariel Corporation, MAN Energy Solutions, Burckhardt Compression, Kobe Steel Ltd., Hitachi Industrial Equipment Systems |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |