Reports

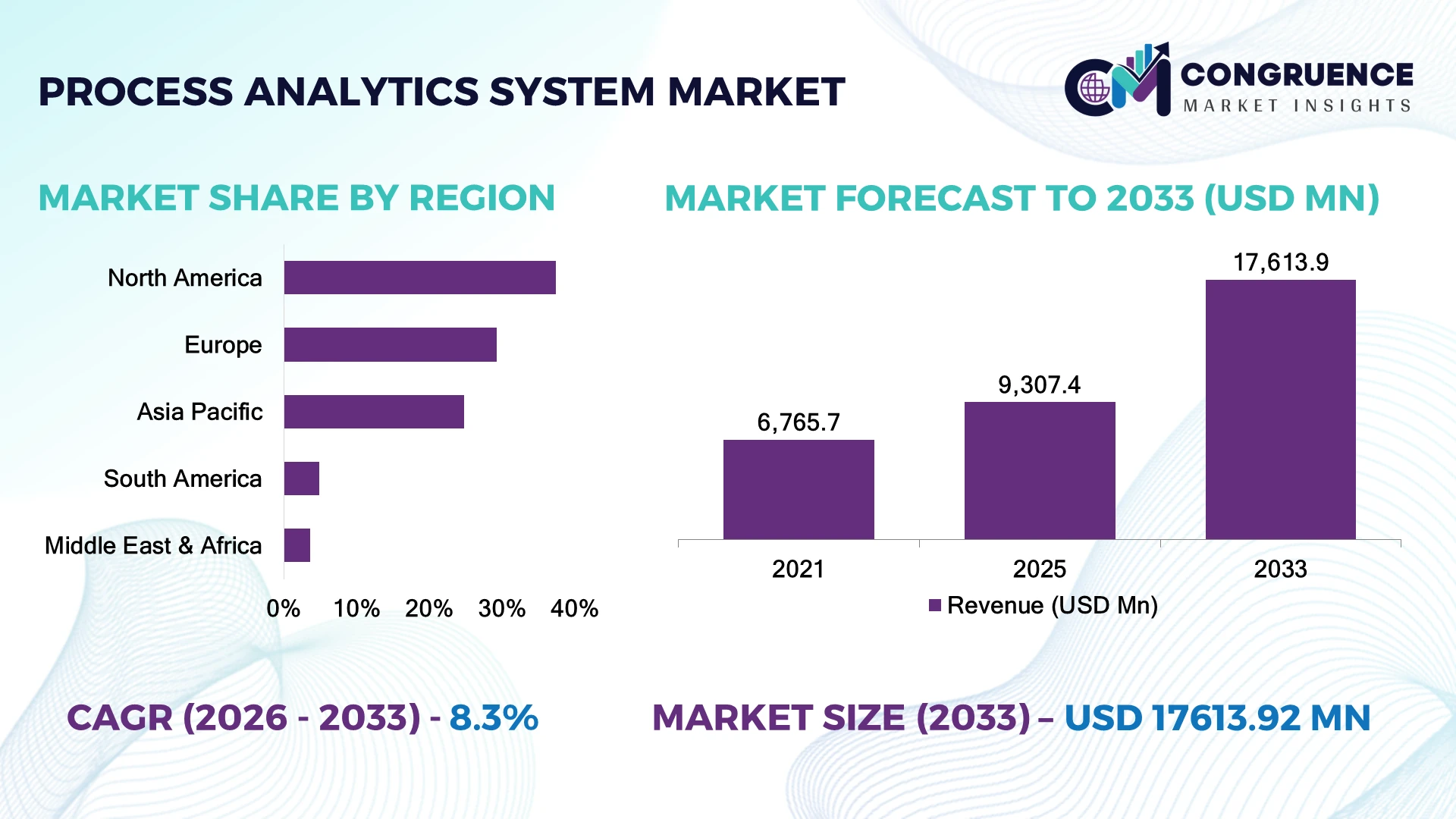

The Global Process Analytics System Market was valued at USD 9,307.4 Million in 2025 and is anticipated to reach a value of USD 17,613.9 Million by 2033 expanding at a CAGR of 8.3% between 2026 and 2033. Rising implementation of Industry 4.0, continuous manufacturing, predictive quality control, and stringent process compliance across pharmaceutical, chemical, food, and energy industries is accelerating deployment of advanced process analytics systems.

The United States accounted for approximately 34% of global process analytics system deployments, supported by large-scale investments in pharmaceutical manufacturing, oil & gas, chemicals, and smart industrial automation. Nearly 71% of large production facilities utilize real-time process monitoring compared with Germany's stronger emphasis on precision manufacturing and PAT-driven pharmaceutical operations. Ongoing industrial supply-chain diversification and critical manufacturing modernization initiatives continue strengthening investment in intelligent process monitoring infrastructure.

Organizations prioritizing AI-enabled process analytics and real-time operational intelligence will establish stronger production efficiency, compliance, and long-term manufacturing competitiveness.

Market Size & Growth: USD 9,307.4 Million in 2025 reaches USD 17,613.9 Million by 2033 at a CAGR of 8.3%, driven by smart manufacturing and process automation.

Top Growth Drivers: Industrial automation (+34%), pharmaceutical PAT adoption (+28%), predictive maintenance (+25%).

Short-Term Forecast: By 2028, production downtime declines nearly 23% while process efficiency improves approximately 27%.

Emerging Technologies: AI analytics, digital twins, machine learning, and advanced spectroscopy transform process optimization.

Regional Leaders: North America exceeds USD 6.0 Billion, Europe surpasses USD 4.7 Billion, Asia-Pacific approaches USD 4.5 Billion through industrial digitalization.

Consumer/End-User Trends: More than 66% of large manufacturers deploy real-time process monitoring systems.

Pilot/Case Example: In 2026, AI-enabled process analytics reduced quality deviations by approximately 31% within continuous pharmaceutical production.

Competitive Landscape: Leading companies hold nearly 44% share, led by ABB, Siemens, Emerson, Yokogawa, and Endress+Hauser.

Regulatory & ESG Impact: Intelligent analytics reduce process waste by approximately 18% while improving energy efficiency.

Investment & Funding: More than USD 2.3 Billion supports industrial digitalization, automation, and smart process modernization.

Innovation & Future Outlook: Edge analytics, cloud connectivity, and autonomous process optimization redefine industrial operations.

Process Analytics Systems are becoming essential across pharmaceuticals, chemicals, food processing, energy, and water treatment as manufacturers prioritize continuous quality monitoring, predictive operations, and regulatory compliance. Approximately 61% of new digital manufacturing projects integrate advanced process analytics, while evolving industrial modernization initiatives and resilient supply-chain strategies continue accelerating intelligent production infrastructure, setting the stage for broader strategic transformation.

The Process Analytics System Market has become strategically important because manufacturers increasingly compete on production efficiency, quality consistency, and operational intelligence rather than production scale alone. Industrial facilities are integrating advanced analytics with automation platforms to strengthen real-time decision-making while meeting increasingly stringent quality and environmental regulations. Supply-chain diversification and factory modernization initiatives are accelerating investment in intelligent monitoring infrastructure across pharmaceuticals, chemicals, food processing, and energy industries.

Modern AI-enabled process analytics systems improve anomaly detection accuracy by approximately 37% while reducing manual quality inspection requirements by nearly 29% compared with conventional laboratory-based monitoring. North America leads deployment through advanced industrial automation and pharmaceutical manufacturing, whereas Asia-Pacific is rapidly expanding smart manufacturing infrastructure and continuous production capabilities. Over the next two to three years, more than 65% of newly commissioned production facilities are expected to integrate real-time process analytics into core manufacturing operations.

A pharmaceutical manufacturer implementing spectroscopy-based process analytics within continuous manufacturing can significantly reduce batch deviations while accelerating product release. Technology providers continue expanding cloud analytics platforms, industrial AI capabilities, and strategic automation partnerships to strengthen end-to-end process visibility. Organizations combining real-time analytics, predictive intelligence, and automated process control will secure stronger operational resilience, regulatory performance, and long-term manufacturing competitiveness.

Rapid deployment of Industry 4.0 technologies and continuous manufacturing is driving widespread adoption of process analytics systems across pharmaceutical, chemical, food, and energy facilities. More than 68% of large industrial plants now integrate real-time process monitoring, while AI-enabled analytics improve production efficiency by approximately 29% and reduce quality deviations by nearly 24%. Germany continues expanding smart factory initiatives, encouraging manufacturers to modernize process control infrastructure with advanced analytical instrumentation. This shift enables faster operational decisions and higher product consistency. Technology providers are responding through AI-integrated software platforms, cloud-enabled analytics, strategic automation partnerships, and expanded digital service portfolios, positioning process analytics as a core operational intelligence platform rather than a standalone quality monitoring tool.

Industrial facilities operating legacy automation environments continue facing integration challenges when deploying advanced process analytics platforms. Approximately 46% of manufacturers still rely on fragmented control systems, while interoperability limitations increase implementation costs by nearly 19% and extend commissioning timelines by approximately 21%. Japan's mature industrial facilities require extensive modernization before advanced analytics can operate seamlessly across production assets. These structural constraints reduce deployment scalability and delay digital transformation initiatives. Companies are addressing these limitations through modular analytics platforms, standardized industrial communication protocols, long-term automation partnerships, and phased modernization strategies that minimize production disruptions while improving infrastructure compatibility.

The convergence of digital twins, edge computing, and industrial AI is creating significant opportunities for next-generation process analytics systems. Nearly 57% of advanced manufacturers are evaluating digital twin integration, while predictive analytics reduce process variability by approximately 26% and improve asset utilization by nearly 22%. Singapore continues investing in smart manufacturing ecosystems that encourage adoption of intelligent industrial analytics and connected production technologies. Solution providers are expanding cloud-native platforms, industrial AI research, and strategic ecosystem partnerships to deliver predictive process optimization. A particularly valuable opportunity lies in combining real-time analytical data with autonomous process control to improve production flexibility without major infrastructure expansion.

Extracting maximum value from advanced process analytics requires specialized expertise in industrial automation, data science, and analytical instrumentation, creating a significant execution challenge. Around 49% of manufacturers report shortages of skilled personnel capable of managing AI-enabled industrial analytics, while advanced system configuration increases deployment complexity by approximately 23%. South Korea's rapidly digitalizing manufacturing sector continues investing in industrial workforce development to address this capability gap. Without adequate expertise, organizations struggle to optimize predictive insights and maintain analytical accuracy. Vendors are expanding technical training programs, remote diagnostic services, intuitive software interfaces, and collaborative implementation partnerships to improve long-term operational performance.

AI-Powered Process Intelligence Manufacturers increasingly integrate artificial intelligence into process analytics platforms, improving anomaly detection accuracy by approximately 35% while reducing false process alarms by nearly 27%. Industrial labor shortages and higher quality expectations are accelerating deployment. Technology providers are expanding AI software capabilities and automation partnerships to strengthen predictive operational decision-making.

Edge Analytics Deployment Expands Edge-based process analytics adoption continues accelerating across pharmaceutical and chemical facilities, reducing analytical response time by approximately 31% while lowering cloud data transmission by nearly 24%. Companies are restructuring production workflows through localized data processing and distributed industrial computing, enabling faster corrective actions and improved production continuity.

Continuous Manufacturing Integration Process analytics systems are becoming integral to continuous manufacturing environments, where inline analytical monitoring improves batch consistency by approximately 28% and decreases production waste by nearly 19%. Regulatory emphasis on process validation is encouraging manufacturers to integrate advanced spectroscopy, automated sensors, and intelligent control platforms throughout production operations.

Cloud-Connected Industrial Platforms Secure cloud-enabled process analytics platforms are transforming multi-site manufacturing by improving enterprise-wide process visibility by approximately 33% while reducing maintenance planning time by nearly 21%. Industrial software providers are strengthening cybersecurity capabilities, cloud partnerships, and unified analytics dashboards, enabling manufacturers to standardize production intelligence across globally distributed manufacturing facilities.

Online Process Analytics Systems accounted for approximately 56% of the Process Analytics System Market in 2025, driven by continuous monitoring capabilities, immediate process feedback, and seamless integration with distributed control systems and industrial automation platforms. Their ability to provide real-time quality assurance, minimize production variability, and reduce manual sampling makes them the preferred solution across pharmaceutical, chemical, and food manufacturing. At-line Systems continue serving production environments requiring rapid verification near manufacturing lines, while Offline Systems remain relevant for laboratory validation and specialized analytical testing. Companies are strengthening online analytics portfolios through AI integration, cloud connectivity, and modular sensor technologies to improve operational visibility and manufacturing efficiency.

Hybrid Process Analytics Systems represent the fastest-growing segment as manufacturers combine online and laboratory-based analytics for greater flexibility and regulatory compliance. Nearly 59% of newly modernized production facilities now deploy hybrid analytical architectures, improving process visibility by approximately 27% while reducing quality investigation time by nearly 22%. Vendors continue investing in interoperable platforms, spectroscopy innovation, and strategic automation partnerships, shifting industry investment toward integrated process intelligence capable of supporting increasingly complex production environments.

According to 2025 implementation findings published by the International Society for Pharmaceutical Engineering (ISPE), manufacturers continue prioritizing real-time analytical technologies to strengthen process control, product quality, and continuous manufacturing performance.

Pharmaceutical Manufacturing accounted for approximately 33% of the Process Analytics System Market in 2025 due to stringent quality requirements, Process Analytical Technology (PAT) implementation, and increasing adoption of continuous manufacturing. Real-time analytical systems enable consistent product quality, regulatory compliance, and faster production decisions. Chemical Processing continues representing a mature application because of its extensive use of spectroscopy and process optimization technologies, while Oil & Gas utilizes advanced analytics to optimize refining operations. Water & Wastewater Treatment and Power Generation remain strategically important as operators strengthen process efficiency, regulatory compliance, and asset performance through intelligent monitoring.

Food & Beverage Processing represents the fastest-growing application as manufacturers accelerate automation, contamination prevention, and product consistency initiatives. Approximately 62% of newly upgraded food manufacturing facilities integrate real-time process monitoring, improving production efficiency by nearly 25% while reducing product waste by approximately 18%. Companies are expanding automated sensor deployment, AI-driven process optimization, and cloud-enabled analytics platforms to strengthen operational transparency and manufacturing agility across high-volume production environments.

A 2026 industrial manufacturing assessment released by the International Society of Automation (ISA) highlighted increasing deployment of real-time process analytics across regulated manufacturing sectors to improve production consistency and operational control.

Large Manufacturing Enterprises accounted for approximately 58% of total market demand in 2025 owing to their extensive production infrastructure, high automation levels, and continuous investment in digital manufacturing technologies. These organizations deploy process analytics systems across multiple production lines to strengthen quality assurance, predictive maintenance, and regulatory compliance. Pharmaceutical Companies remain significant buyers because of stringent manufacturing standards, while Chemical Producers, Energy Companies, and Food Manufacturers continue expanding analytical capabilities to optimize production efficiency and operational reliability. Vendors are strengthening enterprise adoption through scalable software platforms, customized analytical solutions, and long-term digital transformation partnerships.

Contract Manufacturing Organizations (CMOs) represent the fastest-growing end-user segment as outsourced production continues expanding across pharmaceutical, biotechnology, and specialty chemical industries. Nearly 55% of newly commissioned CMO facilities integrate advanced process analytics to improve batch consistency and client compliance requirements. Companies are targeting this segment through modular deployment models, cloud-based analytics, flexible pricing structures, and collaborative technology partnerships that improve production transparency while supporting scalable manufacturing operations.

According to the 2025 International Society for Pharmaceutical Engineering (ISPE) industry assessment, contract manufacturing facilities continue increasing investments in advanced process analytical technologies to strengthen continuous manufacturing performance and regulatory compliance.

North America accounted for the largest market share at 37.4% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.6% between 2026 and 2033.

Advanced industrial automation reinforces real-time process intelligence

North America accounted for approximately 37.4% of the global Process Analytics System Market in 2025, supported by mature automation infrastructure, advanced pharmaceutical manufacturing, and widespread deployment of Industrial Internet of Things (IIoT) technologies. Manufacturers increasingly integrate AI-enabled analytics with distributed control systems to optimize production quality and reduce operational downtime. Nearly 69% of large manufacturing facilities operate continuous real-time process monitoring, while smart factory investments continue expanding across pharmaceutical, chemical, and energy industries. Industrial automation providers are strengthening software ecosystems, cloud-based analytics platforms, and strategic technology partnerships to improve enterprise-wide process visibility and operational efficiency.

United States Market Outlook: The United States dominates the regional market through its advanced pharmaceutical production, specialty chemicals, oil and gas processing, and digital manufacturing ecosystem. Industrial enterprises continue investing in spectroscopy-based analytics, AI-driven quality monitoring, and predictive manufacturing platforms. More than 72% of large pharmaceutical production sites have implemented Process Analytical Technology (PAT), positioning the country as the primary innovation hub for intelligent manufacturing solutions.

Process compliance accelerates digital manufacturing transformation

Europe accounted for approximately 29.3% of the global market in 2025, driven by advanced manufacturing standards, industrial digitalization, and stringent product quality regulations across pharmaceutical and specialty chemical industries. Manufacturers continue integrating inline process analytics to improve production consistency and regulatory compliance. Approximately 63% of newly modernized manufacturing facilities incorporate advanced process monitoring technologies. Automation suppliers continue expanding AI-enabled software, spectroscopy solutions, and industrial digital platforms that strengthen manufacturing precision while reducing production variability.

Germany Market Outlook: Germany leads the regional market through its highly automated manufacturing base, advanced industrial engineering, and strong pharmaceutical production capabilities. Companies continue investing in smart factory infrastructure, intelligent sensor networks, and digital process optimization technologies. Nearly 66% of large chemical manufacturing facilities utilize integrated process analytics systems to enhance production efficiency, product consistency, and regulatory compliance.

Industrial modernization drives intelligent manufacturing adoption

Asia-Pacific accounted for approximately 24.8% of the global market in 2025 and continues recording the fastest expansion through large-scale manufacturing modernization, expanding pharmaceutical production, and accelerating industrial automation. China, Japan, South Korea, and India continue investing heavily in digital manufacturing infrastructure and AI-enabled production technologies. Approximately 61% of newly established industrial production lines incorporate real-time process monitoring capabilities. Technology providers are expanding regional manufacturing, application engineering centers, and automation partnerships to strengthen intelligent production ecosystems and improve industrial productivity.

China Market Outlook: China leads the regional market through extensive manufacturing capacity, rapidly expanding pharmaceutical production, and nationwide industrial digitalization initiatives. Domestic manufacturers continue integrating advanced spectroscopy, industrial AI, and predictive process monitoring into high-volume production environments. More than 64% of newly commissioned smart manufacturing projects include intelligent process analytics platforms, strengthening production quality and operational efficiency across multiple industrial sectors.

Industrial efficiency strengthens analytical deployment

South America accounted for approximately 4.9% of the global market in 2025, supported by increasing modernization across food processing, mining, chemicals, and energy industries. Industrial operators are deploying process analytics systems to improve operational efficiency, product quality, and environmental compliance. Nearly 42% of industrial modernization projects now integrate automated analytical monitoring technologies. While infrastructure modernization progresses unevenly across industries, suppliers continue expanding localized engineering services, digital maintenance capabilities, and strategic automation partnerships to improve adoption.

Brazil Market Outlook: Brazil remains the region's leading market through its diversified industrial production, expanding food processing sector, and growing chemical manufacturing base. Manufacturers increasingly deploy real-time analytical systems to optimize production consistency and reduce operational losses. Continuous investment in industrial automation and intelligent manufacturing platforms is strengthening demand for advanced process monitoring technologies across large production facilities.

Industrial diversification expands intelligent process control

The Middle East & Africa accounted for approximately 3.6% of the global market in 2025, driven by industrial diversification, refinery modernization, and expanding investments in water treatment, petrochemicals, and food processing. Industrial operators increasingly implement advanced process analytics to improve production reliability and regulatory compliance. Approximately 39% of newly commissioned industrial projects integrate digital monitoring and intelligent process optimization technologies. Technology providers continue strengthening regional engineering capabilities, industrial partnerships, and localized automation services to support expanding manufacturing modernization initiatives.

Saudi Arabia Market Outlook: Saudi Arabia leads regional adoption through large-scale investments in petrochemical processing, industrial diversification, and advanced manufacturing infrastructure. Industrial enterprises continue integrating process analytics with automation platforms to improve operational efficiency and product quality across energy and specialty chemical production. More than 53% of newly developed industrial facilities incorporate intelligent process monitoring systems, reinforcing the country's leadership in digital industrial transformation.

The Process Analytics System Market is led by automation specialists including Siemens, ABB, Emerson Electric, Yokogawa Electric, and Endress+Hauser, which compete against analytical instrumentation providers such as Thermo Fisher Scientific, Agilent Technologies, and Mettler-Toledo, while niche spectroscopy innovators target specialized applications. The top five players collectively account for approximately 54% of global market share. Competition centers on measurement accuracy, software integration, lifecycle services, and deployment speed, with AI-enabled analytics improving process optimization by nearly 28% and cloud-enabled monitoring reducing maintenance costs by approximately 22%. Leading vendors are expanding through digital platform acquisitions, strategic partnerships, Ethernet-APL interoperability, and vertically integrated instrumentation portfolios. The competitive shift favors unified automation ecosystems over standalone analyzers. High certification requirements, long customer validation cycles, and deep process expertise remain major entry barriers. Success increasingly depends on delivering interoperable, intelligent, and scalable analytical platforms supported by strong global service networks.

Siemens AG

ABB Ltd.

Emerson Electric Co.

Yokogawa Electric Corporation

Endress+Hauser Group

Thermo Fisher Scientific Inc.

Agilent Technologies Inc.

Mettler-Toledo International Inc.

HORIBA Ltd.

AMETEK Inc.

Danaher Corporation

SUEZ Group

Bruker Corporation

Metrohm AG

Artificial intelligence, machine learning, Raman spectroscopy, tunable diode laser absorption spectroscopy (TDLAS), and edge analytics are redefining process analytics platforms. Nearly 67% of newly commissioned pharmaceutical and chemical production facilities now integrate AI-assisted process monitoring, while advanced spectroscopy improves measurement precision by approximately 24% and reduces laboratory dependency by nearly 30%. Vendors increasingly combine analyzers with industrial IoT architectures to provide continuous quality assurance and predictive process optimization.

Modern inline analytics outperform conventional offline laboratory sampling by reducing response time by approximately 70% while improving production consistency by nearly 26%. More than 58% of industrial digital transformation projects now incorporate cloud-connected analytical platforms supporting remote diagnostics and lifecycle management. Automation leaders benefit most because integrated control systems, intelligent sensors, and analytics software create higher switching costs and stronger long-term customer retention through unified operational ecosystems.

Between 2026 and 2028, software-defined analytics, digital twins, autonomous calibration, and Ethernet-APL connectivity will accelerate intelligent manufacturing deployment. Configurable analytics platforms are expected to reduce commissioning effort by approximately 19%, while predictive maintenance algorithms improve equipment availability by nearly 21%. Companies investing in interoperable architectures, AI-ready instrumentation, cybersecurity, and scalable cloud platforms will strengthen operational resilience and gain sustainable competitive differentiation as industrial manufacturers prioritize continuous optimization over periodic quality inspection.

April 2025 Endress+Hauser reported launching 81 new products during 2024 while investing heavily in process automation, gas analysis, and digital measurement technologies, strengthening its analytical instrumentation portfolio and long-term innovation capacity. Source: Endress+Hauser

June 2025 Endress+Hauser completed large-scale Ethernet-APL interoperability testing involving nearly 240 field devices integrated with Emerson DeltaV, validating multi-vendor process automation performance and accelerating deployment of digital process analytics across industrial plants. Source: us.endress.com

July 2025 Emerson introduced the Ovation AI-enabled Virtual Advisor within the Ovation 4.0 Platform, enhancing predictive operational support for power and water industries while improving maintenance efficiency through generative AI-assisted diagnostics.

April 2025 European Pharmacopoeia updated guidance supporting handheld Raman technology validation for pharmaceutical manufacturing, simplifying regulated deployment and strengthening adoption of inline process analytical technologies across GMP production environments. Source: European Pharmacopoeia

This report provides comprehensive analysis of the Process Analytics System Market across major product types, applications, end-users, and global regions. The study evaluates online, at-line, inline, and offline analytical systems deployed across pharmaceutical, chemical, food and beverage, oil and gas, water treatment, energy, and other industrial sectors. Coverage includes spectroscopy, chromatography, electrochemical sensing, industrial IoT integration, AI-enabled analytics, cloud connectivity, and digital process optimization. Regional assessment spans North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, supported by operational adoption patterns, deployment intensity, and competitive positioning.

The report analyzes segment-level market dynamics, technology penetration, enterprise adoption trends, and strategic activities of leading industry participants. It highlights measurable deployment patterns, process automation priorities, industrial digitalization strategies, and evolving analytical workflows between 2026 and 2033. The assessment supports investment planning, product development, geographic expansion, partnership evaluation, competitive benchmarking, and long-term business strategy by identifying high-value growth segments, emerging industrial applications, and technology-driven competitive opportunities.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 9,307.4 Million |

|

Market Revenue in 2033 |

USD 17,613.9 Million |

|

CAGR (2026 - 2033) |

8.3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Siemens AG, ABB Ltd., Emerson Electric Co., Yokogawa Electric Corporation, Endress+Hauser Group, Thermo Fisher Scientific Inc., Agilent Technologies Inc., Mettler-Toledo International Inc., HORIBA Ltd., AMETEK Inc., Danaher Corporation, SUEZ Group, Bruker Corporation, Metrohm AG |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |