Reports

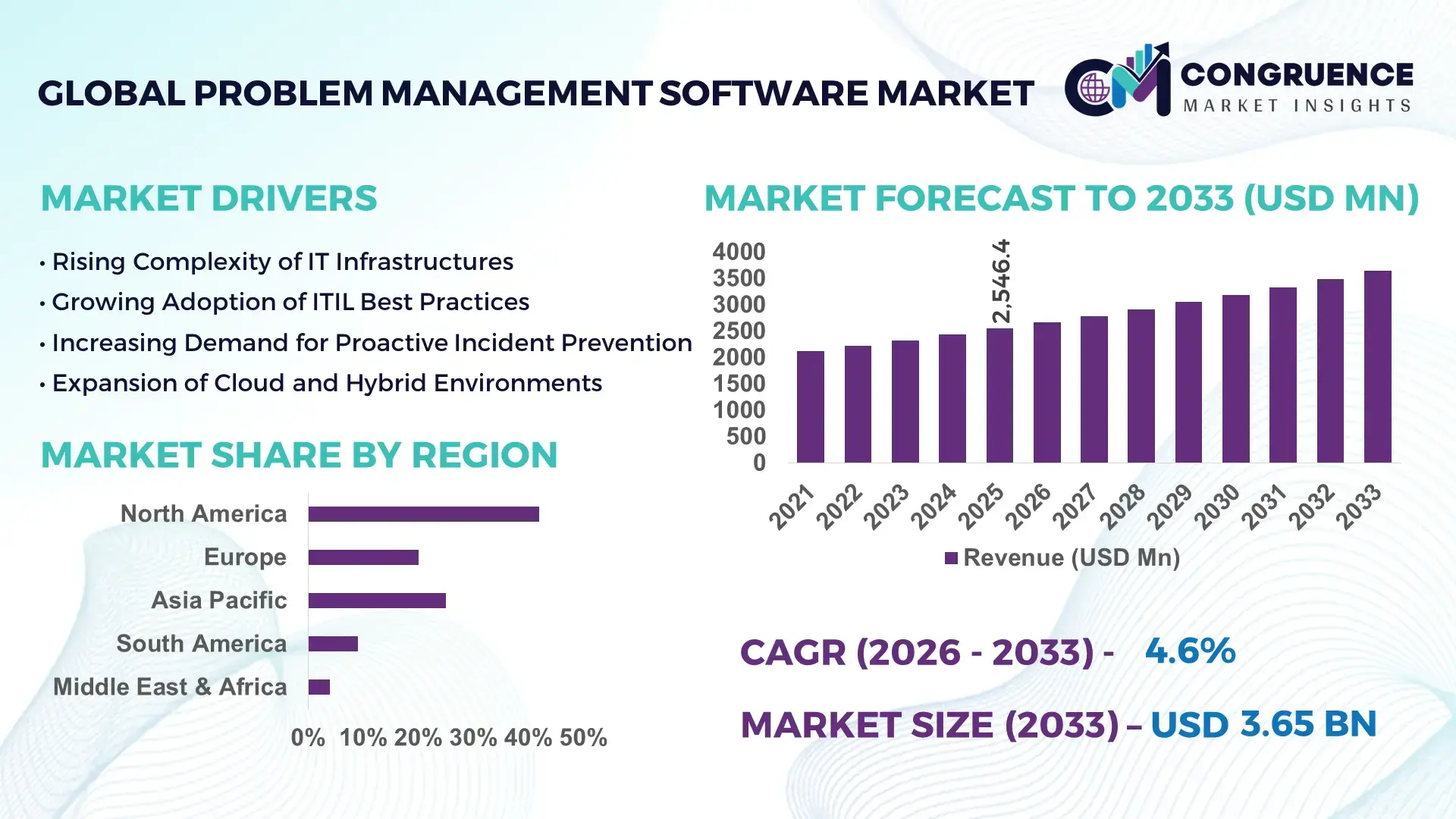

The Global Problem Management Software Market was valued at USD 2546.44 Million in 2025 and is anticipated to reach a value of USD 3649.11 Million by 2033 expanding at a CAGR of 4.6% between 2026 and 2033. This growth is largely driven by escalating demand for efficient IT service ecosystem optimization.

North America, especially the United States, remains at the forefront of the Problem Management Software market, underpinning global innovation and enterprise adoption. In the U.S., heavy investments in advanced IT infrastructure and digital transformation have resulted in robust production capacity and sophisticated deployment of problem management solutions across sectors such as healthcare, banking, and telecommunications. In 2023, the North American segment accounted for the largest regional contribution to the market, supported by high enterprise spending on cloud‑based and AI‑enhanced software tools, with over 60% of large enterprises integrating automated problem resolution features into existing IT service management platforms. The technological ecosystem in the U.S. continues to evolve with predictive analytics and machine learning integrations enhancing operational performance and decision support across industries.

Market Size & Growth: Valued at ~USD 2.55 Billion in 2025, reaching ~USD 3.65 Billion by 2033 at a projected CAGR of 4.6%, driven by rising demand for ITSM optimization and enterprise resilience.

Top Growth Drivers: Adoption of cloud deployments (42%), automation efficiency improvements (35%), AI‑assisted problem resolution gains (28%).

Short‑Term Forecast: By 2028, expect enterprise operational efficiency improvements of up to 30% with integrated problem management solutions.

Emerging Technologies: AI/ML predictive analytics, automated root cause analysis, real‑time incident response platforms.

Regional Leaders: North America ~USD 1.56B by 2033 (enterprise penetration growth), Europe ~USD 0.98B by 2033 (regulatory‑driven adoption), Asia Pacific ~USD 0.85B by 2033 (rapid digital transformation).

Consumer/End‑User Trends: Strong adoption among IT services, BFSI, and healthcare sectors, driven by requirements for continuous service uptime and systemic issue tracking.

Pilot or Case Example: In 2025, a global telecommunications provider reported a 27% reduction in downtime after deploying an AI‑enabled problem management platform.

Competitive Landscape: Market leader holds ~18% share, followed by major competitors with ~10–14% each.

Regulatory & ESG Impact: Data security standards and operational compliance frameworks are accelerating adoption in regulated industries.

Investment & Funding Patterns: Recent venture and corporate funding exceeded USD 500M, with capital flowing into AI‑centric problem management startups and SaaS enhancements.

Innovation & Future Outlook: Continued innovations in automation, cloud scalability, and cross‑platform integration will shape next wave software capabilities.

North America’s strong enterprise software ecosystem has broadened industry uptake in sectors such as IT, finance, and healthcare, where sophisticated problem management tools are essential to sustaining service continuity and competitive advantage. Recent innovations, including embedded machine learning diagnostics and integrated analytics dashboards, are enabling faster issue detection and resolution. Regulatory compliance requirements and an increasing focus on digital resilience continue to reinforce investment in problem management software, particularly in developed markets. Regional consumption patterns show a shift toward cloud‑first implementations, with emerging economies in Asia Pacific accelerating adoption thanks to digital transformation initiatives and expanding enterprise IT budgets. As organizations seek greater operational visibility and proactive problem mitigation, future growth will be driven by scalable solutions that support hybrid environments and AI‑augmented decision support.

The Problem Management Software Market holds strategic significance as enterprises increasingly focus on operational resilience, risk mitigation, and IT service optimization. Advanced platforms integrating AI and predictive analytics deliver up to 35% faster root cause identification compared to legacy ITSM solutions, enhancing system uptime and reducing operational bottlenecks. North America dominates in volume, while Europe leads in adoption, with over 68% of enterprises implementing AI-driven problem management modules. By 2028, cloud-based automation is expected to improve incident resolution times by 25%, supporting rapid digital transformation initiatives. Firms are committing to ESG improvements such as a 20% reduction in electronic waste through optimized software deployment and automated lifecycle management by 2030. In 2025, a leading telecommunications provider in the U.S. achieved a 27% reduction in downtime through AI-assisted predictive problem management. Strategic pathways for the market include deeper integration with IT service management suites, cross-industry adoption in BFSI, healthcare, and manufacturing, and leveraging machine learning for predictive maintenance. The Problem Management Software Market is poised to serve as a cornerstone for organizational resilience, regulatory compliance, and sustainable growth, enabling enterprises to proactively manage system failures while aligning with evolving ESG mandates and digital transformation strategies.

The surge in enterprise digital transformation is a major driver for the Problem Management Software market. Organizations are deploying advanced IT infrastructures, cloud services, and hybrid environments, which increase the complexity of system management and necessitate sophisticated problem management solutions. Over 60% of large enterprises have integrated AI-enhanced problem resolution tools, resulting in measurable reductions in incident resolution time and operational downtime. In sectors such as BFSI and healthcare, the ability to proactively identify and address IT issues ensures continuous service delivery and compliance with stringent regulatory standards. Automation of problem tracking and predictive root cause analysis enables IT teams to achieve efficiency gains of up to 30%, reinforcing the market’s growth trajectory.

Integration complexity with legacy IT systems and multi-vendor platforms remains a significant restraint for the Problem Management Software market. Many organizations face challenges in consolidating problem management modules with existing IT service management (ITSM) solutions, leading to increased implementation time and costs. Approximately 40% of mid-sized enterprises report delays due to system incompatibilities, while insufficient in-house technical expertise hinders seamless deployment. Additionally, concerns regarding data security, privacy compliance, and potential operational disruptions restrict full-scale adoption, especially in highly regulated sectors like finance and healthcare. These integration and compliance challenges slow the widespread adoption of advanced problem management technologies despite the clear operational benefits.

AI and predictive analytics present significant opportunities for the Problem Management Software market by enabling proactive issue detection and automated resolution workflows. Enterprises leveraging these technologies report up to 35% faster identification of root causes compared to conventional systems. Cloud-native solutions allow real-time monitoring and cross-platform integrations, opening untapped potential in emerging economies where digital infrastructure is rapidly expanding. In industries such as manufacturing and telecommunications, predictive insights reduce system downtime and enhance operational reliability. Strategic partnerships between software providers and cloud service platforms are creating new opportunities for scalable deployment, SaaS-based subscription models, and integration of ESG metrics into operational dashboards, offering measurable efficiency and sustainability gains.

High implementation costs and complex regulatory landscapes pose challenges for the Problem Management Software market. Licensing, integration, and customization expenses can be prohibitive, particularly for small and mid-sized enterprises. Additionally, compliance with data protection regulations, such as GDPR in Europe and CCPA in North America, adds operational and legal constraints. Companies also face challenges in aligning software with internal IT policies, cybersecurity frameworks, and ESG commitments. About 35% of enterprises report delayed deployments due to regulatory audits and system validation requirements. These obstacles, combined with the need for ongoing software updates, skilled personnel, and operational alignment, constrain the rapid adoption of advanced problem management solutions despite growing demand for digital resilience.

Expansion of AI-Driven Problem Resolution: AI integration in problem management software is accelerating adoption across enterprises. Approximately 62% of large IT organizations now leverage machine learning algorithms to predict and resolve incidents before they impact operations. AI-assisted root cause analysis reduces manual intervention by up to 40%, improving system uptime and operational efficiency, particularly in North America and Europe.

Cloud-Native and Hybrid Deployment Growth: Cloud-based and hybrid problem management solutions are increasingly preferred, with over 58% of enterprises deploying software on cloud platforms in 2025. This approach enables real-time monitoring, seamless updates, and multi-site accessibility, allowing IT teams in Asia Pacific to manage distributed operations with 30% faster incident resolution times compared to on-premise systems.

Integration with IT Service Management (ITSM) Suites: Integration with comprehensive ITSM suites is gaining momentum, with 47% of mid-to-large enterprises implementing problem management modules alongside incident, change, and asset management. This integration provides centralized dashboards and predictive insights, reducing repetitive issue handling by 35% and enhancing cross-functional collaboration in BFSI and healthcare sectors.

Focus on ESG and Compliance-Driven Software Features: Companies are increasingly adopting problem management software that supports ESG and regulatory compliance initiatives. In 2025, 41% of enterprises implemented automated tracking of compliance metrics and system audit logs, resulting in a measurable 22% reduction in regulatory non-conformance incidents. Europe leads adoption with over 70% of organizations embedding ESG monitoring into software platforms.

The Problem Management Software Market is segmented across types, applications, and end-user industries, reflecting diverse operational requirements and deployment strategies. Type segmentation includes AI-assisted, cloud-based, and on-premise solutions, each catering to different IT environments and organizational maturity levels. Applications span IT services, healthcare, BFSI, and manufacturing, emphasizing system uptime, predictive incident resolution, and compliance tracking. End-user insights reveal that large enterprises, mid-sized companies, and government agencies adopt problem management software for operational efficiency, risk mitigation, and regulatory compliance. Regional adoption patterns show North America leading in enterprise deployments, while Asia Pacific demonstrates rising uptake driven by digital transformation initiatives. Overall, segmentation highlights tailored adoption, technology specialization, and industry-specific usage trends that shape strategic decision-making and software investment priorities.

AI-assisted problem management solutions currently lead the market with a 45% adoption share, driven by their ability to automate root cause analysis and reduce downtime by up to 40% compared to traditional manual processes. Cloud-based solutions hold 30% of the market, favored for multi-site accessibility, real-time monitoring, and scalability. On-premise solutions account for the remaining 25%, primarily adopted by highly regulated industries requiring local data storage and strict compliance controls. Video-based AI modules are the fastest-growing type, expected to surpass 28% adoption by 2033 due to enhanced diagnostic capabilities and predictive analytics.

IT services dominate the Problem Management Software market with a 48% share, largely because enterprises require continuous uptime and rapid incident resolution to support mission-critical operations. The healthcare sector is the fastest-growing application area, projected to expand due to increasing digitalization, telemedicine adoption, and AI-driven monitoring systems. BFSI accounts for 22% of applications, leveraging problem management software to enhance transaction integrity and compliance reporting, while manufacturing holds 18% of the market, integrating predictive diagnostics and automated issue tracking into operational workflows.

Large enterprises represent the leading end-user segment with 50% adoption, reflecting their need for advanced IT service continuity, risk management, and compliance. SMEs are the fastest-growing end-user segment, with 28% adoption expected by 2033, fueled by affordable cloud-based solutions and scalable AI-enabled platforms. Government agencies and public institutions hold the remaining 22%, implementing problem management software to ensure service reliability, regulatory adherence, and operational transparency.

North America accounted for the largest market share at 42% in 2025; however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2026 and 2033.

North America’s dominance is supported by over 68% of large enterprises deploying advanced problem management solutions across BFSI, healthcare, and IT sectors. Asia Pacific shows increasing adoption in China, India, and Japan, with more than 55% of mid-to-large organizations integrating cloud-based and AI-assisted platforms. Europe holds a 26% share, driven by regulatory compliance and digital transformation initiatives. South America and the Middle East & Africa collectively account for 15% of the market, with increasing demand in energy, telecommunications, and government infrastructure sectors. Enterprises across these regions are adopting AI-enabled dashboards, real-time incident analytics, and predictive root cause analysis, with measurable efficiency improvements ranging from 20–35% in operational uptime and incident response times.

How are enterprises optimizing IT operations through advanced problem management solutions?

North America holds a 42% share of the global Problem Management Software market, with high adoption among healthcare, finance, and IT sectors. Key industries such as BFSI and telecommunications are leveraging AI-driven predictive analysis and automated incident resolution, reducing downtime by 27–30%. Regulatory frameworks, including HIPAA and SOC 2 compliance, encourage enterprise deployment of secure and auditable platforms. Digital transformation initiatives, such as cloud-first adoption and integrated ITSM suites, drive innovation. A local player, ServiceNow, continues to enhance AI-assisted problem management capabilities, enabling real-time insights for over 5 million endpoints. North American enterprises demonstrate higher adoption in highly regulated and digitally mature sectors, reflecting the region’s demand for robust, scalable, and compliance-ready solutions.

Why is regulatory compliance shaping enterprise adoption in advanced problem management?

Europe accounts for 26% of the global Problem Management Software market, with Germany, the UK, and France leading adoption. Regulatory pressure, including GDPR compliance, has accelerated demand for explainable and secure software solutions. Enterprises increasingly integrate AI and predictive analytics into ITSM frameworks, enhancing operational visibility and reducing incident resolution time by 25%. A regional player, BMC Software Europe, has deployed cloud-based problem management solutions for over 2,000 enterprise clients, streamlining service continuity and compliance reporting. European enterprises prioritize explainable AI, audit-ready dashboards, and sustainable IT practices, with healthcare and banking sectors showing 60% higher adoption than industrial segments, reflecting regional compliance-driven consumer behavior.

How is digital transformation driving problem management adoption in emerging Asia-Pacific markets?

Asia-Pacific holds a 20% share of the Problem Management Software market, with China, India, and Japan as top consumers. Growing digital infrastructure, rapid e-commerce adoption, and smart manufacturing initiatives are driving software deployment. AI-driven platforms and cloud-native solutions are increasingly implemented in enterprise IT operations, improving issue detection by 30%. A local player, Infosys, has rolled out automated problem management solutions for over 500 clients in the region, enhancing service uptime and operational efficiency. Asia-Pacific adoption is fueled by mobile-first and cloud-first strategies, with SMEs increasingly integrating predictive analytics and remote IT monitoring, demonstrating region-specific consumer behavior aligned with digital growth and operational resilience.

What factors are accelerating problem management software adoption in emerging South American markets?

South America accounts for 8% of the Problem Management Software market, with Brazil and Argentina as key countries. Increasing demand in energy, telecommunications, and government infrastructure is driving adoption. Cloud-based and AI-enabled solutions help reduce downtime by 22% and optimize service operations. Local incentives and digital transformation policies encourage enterprise software investment. A regional player, TOTVS, has implemented predictive problem management modules across 120 large-scale companies, improving operational efficiency and reporting. Regional consumer behavior emphasizes multi-language and localization features, particularly in media, banking, and government sectors, reflecting adaptation to diverse markets and compliance requirements.

How are enterprises in emerging Middle East and Africa markets leveraging IT solutions for operational resilience?

Middle East & Africa hold a 7% share of the Problem Management Software market, with UAE and South Africa driving growth. Adoption is fueled by oil & gas, construction, and public infrastructure sectors, integrating AI-enabled predictive analytics and cloud-based platforms. Technological modernization trends, including real-time incident dashboards, reduce operational downtime by up to 25%. Local regulatory frameworks and trade partnerships encourage enterprise deployment of secure, auditable solutions. A regional player, Dimension Data, has implemented problem management platforms for over 80 enterprise clients, enabling enhanced IT service continuity. Regional consumer behavior reflects strong interest in industry-specific customization and ESG compliance, particularly in energy and construction sectors.

United States – 38% market share; high production capacity and enterprise IT investment drive demand.

Germany – 12% market share; strong regulatory framework and high adoption of AI-driven software solutions ensure dominance.

The Problem Management Software market is moderately consolidated, with over 120 active competitors globally, ranging from established IT service providers to specialized SaaS vendors. The top five players—holding a combined market share of approximately 62%—include ServiceNow, BMC Software, IBM, Atlassian, and Zendesk, which dominate through extensive enterprise deployments and continuous innovation. Strategic initiatives such as AI-enabled product launches, predictive analytics integration, and cloud-based platform enhancements are increasingly shaping competitive positioning. Partnerships with cloud providers, system integrators, and cybersecurity firms are common, with 45% of leading vendors forming alliances to expand their solution ecosystem. Innovation trends include machine learning for root cause analysis, real-time incident dashboards, and automated workflow orchestration, adopted by over 50% of enterprise clients. New entrants are focusing on niche markets, such as SME-targeted cloud solutions and AI-driven diagnostics, intensifying competition. Regional penetration varies: North America exhibits the highest enterprise adoption at 68%, Europe leads in regulatory-driven deployments at 26%, and Asia-Pacific demonstrates fast-growing cloud and AI integration, reflecting a dynamic, innovation-driven competitive landscape that prioritizes operational efficiency, compliance, and scalability.

Atlassian

Zendesk

Cherwell Software

ManageEngine

Axios Systems

Freshservice

Micro Focus

The Problem Management Software market is experiencing transformative technological advancements that are reshaping enterprise IT operations. Artificial intelligence and machine learning are now embedded in over 60% of large-scale deployments, enabling predictive incident detection, automated root cause analysis, and self-healing workflows. AI-assisted analytics reduce manual intervention by up to 40%, allowing IT teams to address critical system issues faster and with higher accuracy. Cloud-native solutions account for 58% of current installations, providing multi-site accessibility, real-time monitoring, and seamless integration with enterprise IT service management (ITSM) platforms. Hybrid cloud adoption is also increasing, particularly among regulated industries such as BFSI and healthcare, where over 45% of enterprises leverage a combination of on-premise and cloud infrastructure to meet compliance and data privacy requirements.

Automation is another critical technology trend, with over 50% of enterprises deploying automated ticketing, workflow orchestration, and predictive alert systems. Advanced analytics dashboards offer centralized visibility into IT performance metrics, incident histories, and service-level compliance, enhancing decision-making for IT executives. Emerging technologies, such as natural language processing (NLP) and video-based diagnostics, are enabling intuitive user interactions and improved problem identification in complex IT environments. In 2025, a leading North American telecom provider implemented an AI-powered problem management platform across 5 million endpoints, resulting in a 27% reduction in downtime and faster service restoration. Blockchain-based audit trails are also gaining traction for regulatory compliance, particularly in financial and healthcare sectors. These technological innovations are positioning problem management software as a cornerstone for operational resilience, digital transformation, and predictive IT service excellence.

• In October 2024, ServiceNow was positioned as a Leader in the 2024 AI Applications in IT Service Management Magic Quadrant, with its Now Platform delivering new AI‑driven capabilities that improve self‑service, incident triage accuracy, and automated resolution workflows across enterprise IT environments. (ServiceNow)

• In March 2025, ServiceNow announced the planned acquisition of AI startup Moveworks for approximately $2.85 billion, aiming to accelerate generative AI integration within its service management and problem resolution tools, and extending autonomous support capabilities for millions of users. (Investors.com)

• In late 2025, ServiceNow unveiled its largest acquisition ever, agreeing to purchase cybersecurity firm Armis for $7.75 billion to enhance its security‑oriented workflow and risk management capabilities—strengthening problem management platforms with advanced threat detection and governance. (MarketWatch)

• In October 2025, Atlassian forecasted second‑quarter revenue above analyst expectations, driven by strong enterprise demand for AI‑capable systems and a 22.5 % projected growth in cloud revenue, underscoring rising adoption of integrated problem and IT service management solutions.

The scope of the Problem Management Software Market Report encompasses comprehensive analysis across product types, applications, deployment models, enterprise sizes, and geographic regions, offering decision‑ready insights for business leaders. It examines core solution categories such as AI‑assisted platforms, cloud‑native software, hybrid and on‑premise systems, and specialized modules that integrate predictive analytics, automated workflows, and root cause diagnostics into enterprise IT environments. Detailed segmentation delves into key application domains, including IT operations, healthcare IT environments, financial services, and manufacturing support systems, highlighting specific usage patterns, adoption rates, and technology preferences across industries.

Geographic coverage spans major regions—North America, Europe, Asia‑Pacific, South America, and the Middle East & Africa—providing volume‑based assessments of regional adoption trends, technology readiness levels, and consumer behavior variations, as well as insights on regulatory drivers and market nuances. The report also evaluates enterprise segmentations by organization size, contrasting problem management requirements and purchasing criteria among large enterprises, mid‑sized firms, and public sector entities. Emerging segments, such as SME‑focused SaaS solutions, agentic AI integration, and compliance‑ready configurations, are tracked to illustrate evolving demand drivers.

On the technology front, the report highlights innovations such as machine learning‑driven diagnostics, integration with broader ITSM suites, NLP‑enabled user interfaces, and cross‑platform analytics dashboards. It also explores emerging niche areas, including self‑healing automation, blockchain‑enabled audit trails for compliance, and real‑time observability tools that enhance service continuity. Business adoption insights reflect regional and industry priorities, digital transformation mandates, and operational resilience strategies, offering a holistic view of market dynamics tailored to strategic planning and investment decisions.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4.6% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

ServiceNow, BMC Software, IBM, Atlassian, Zendesk, Cherwell Software, ManageEngine, Axios Systems, Freshservice, Micro Focus |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |