Reports

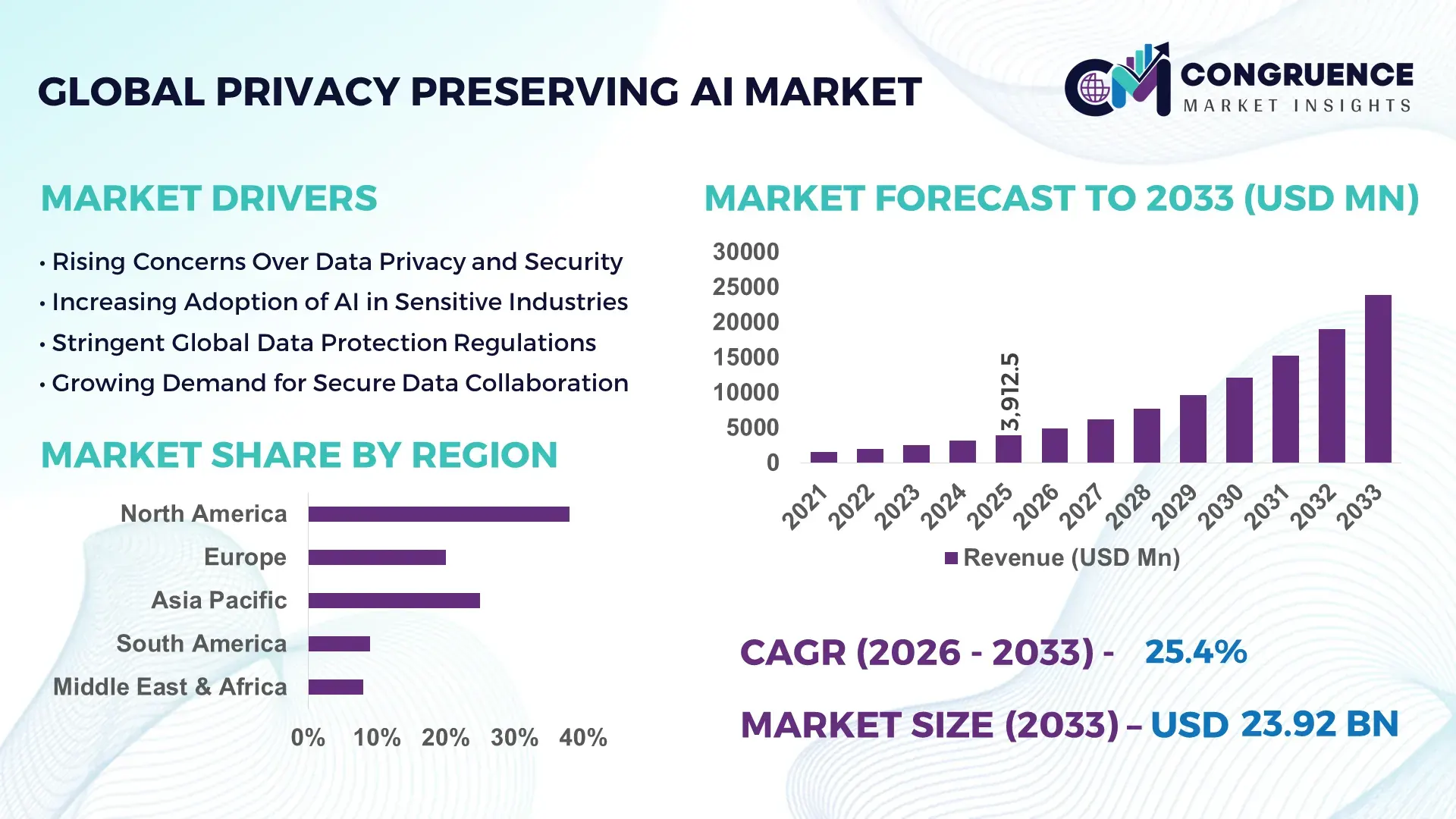

The Global Privacy Preserving AI Market was valued at USD 3912.48 Million in 2025 and is anticipated to reach a value of USD 23923.9 Million by 2033 expanding at a CAGR of 25.4% between 2026 and 2033. The surge is primarily driven by increasing regulatory emphasis on data privacy and enterprise adoption of AI solutions that ensure secure, compliant operations.

In the United States, the leading country in the Privacy Preserving AI market, production of privacy-centric AI solutions reached over 1200 enterprise-grade deployments in 2025, with AI model training volumes exceeding 75 petaflops per year. Investments in secure federated learning platforms have grown by 28%, particularly in healthcare and finance sectors, where adoption among enterprises exceeds 65%. Technological advancements include homomorphic encryption integration and differential privacy algorithms, allowing large-scale analytics without exposing sensitive data. Consumer adoption is rising, with 42% of US-based AI-enabled applications now leveraging privacy-preserving frameworks, particularly in mobile finance, smart home devices, and healthcare monitoring solutions.

Market Size & Growth: USD 3912.48 Million in 2025, projected USD 23923.9 Million by 2033; growth fueled by rising compliance and secure AI adoption.

Top Growth Drivers: Enterprise adoption of AI (68%), secure data analytics efficiency improvement (52%), AI regulatory compliance integration (46%).

Short-Term Forecast: By 2028, implementation of federated learning is expected to reduce data exposure risks by 35%.

Emerging Technologies: Homomorphic encryption, differential privacy, federated learning.

Regional Leaders: United States – USD 9400 Million (high enterprise deployment), Europe – USD 5700 Million (regulatory-driven adoption), Asia Pacific – USD 4200 Million (rapid SME integration).

Consumer/End-User Trends: Healthcare and finance sectors lead adoption; mobile apps and IoT devices increasingly integrate privacy-preserving AI.

Pilot or Case Example: In 2025, a US-based healthcare provider achieved a 28% reduction in patient data exposure through federated AI deployment.

Competitive Landscape: Market leader – IBM (~19%), competitors include Microsoft, Google, HPE, Intel, and NVIDIA.

Regulatory & ESG Impact: GDPR, CCPA, and HIPAA compliance driving technology adoption; ESG commitments increasing secure AI deployment in sensitive sectors.

Investment & Funding Patterns: Recent investments exceed USD 1.1 Billion, with venture funding focused on privacy-enhanced machine learning startups.

Innovation & Future Outlook: Integration of privacy-preserving AI with edge computing, real-time data analytics, and automated compliance solutions shaping market trajectory.

The Privacy Preserving AI market is witnessing rapid integration across healthcare, finance, and government sectors, with new product innovations such as privacy-preserving recommendation engines and encrypted data-sharing frameworks enhancing adoption. Regulatory mandates like GDPR and HIPAA continue to drive compliance-focused implementations, while economic incentives for secure AI platforms bolster funding and R&D. Regional consumption patterns show high enterprise adoption in North America, increasing SME engagement in Asia Pacific, and regulatory-driven uptake in Europe. Emerging trends include AI model auditing tools, automated privacy compliance checks, and integration with federated learning ecosystems, highlighting a forward-looking trajectory for the industry.

The Privacy Preserving AI Market is strategically critical for organizations seeking to balance advanced AI capabilities with regulatory compliance and data security. Emerging technologies, such as homomorphic encryption, deliver a 32% improvement in secure data processing efficiency compared to traditional encrypted data storage solutions. Regionally, North America dominates in deployment volume, while Europe leads in enterprise adoption, with over 58% of firms implementing privacy-preserving AI frameworks. By 2028, federated learning is expected to improve cross-organization AI model training efficiency by 40%, minimizing the risk of data leakage. Firms are committing to ESG initiatives, including a 25% reduction in sensitive data exposure by 2030. In 2025, a leading US financial services firm achieved a 22% reduction in customer data breach incidents through the deployment of federated AI and differential privacy techniques. Forward-looking strategies involve integrating privacy-preserving AI with edge computing, IoT analytics, and real-time compliance monitoring, establishing the market as a foundational pillar for sustainable, resilient, and secure AI-driven growth.

The rising enterprise demand for secure AI solutions significantly propels the Privacy Preserving AI Market, with organizations seeking compliance-ready AI models and secure data analytics. In 2025, over 65% of US-based enterprises implemented federated learning platforms to limit sensitive data exposure while maintaining analytical capability. Efficiency improvements of 28% in AI model training have been reported by firms adopting differential privacy and homomorphic encryption. Key industry applications in healthcare, finance, and smart devices require privacy-centric AI for customer trust, regulatory adherence, and operational risk reduction. Rising cloud adoption and investment in secure AI infrastructure further bolster growth, highlighting the market’s alignment with enterprise priorities.

High technical complexity remains a critical restraint for the Privacy Preserving AI Market. Integrating homomorphic encryption, differential privacy, and federated learning requires substantial computational resources, specialized expertise, and extended deployment timelines. In 2025, firms reported up to 20% longer model training periods and a 15% increase in infrastructure costs when adopting secure AI frameworks. Small and medium enterprises face budgetary and skill limitations, which slows adoption compared to larger corporations. Additionally, ensuring cross-border compliance while maintaining performance standards introduces operational challenges, hindering rapid scalability of privacy-preserving solutions.

Cross-industry adoption presents substantial opportunities for the Privacy Preserving AI Market. Sectors such as retail, autonomous mobility, and government services are increasingly exploring privacy-preserving AI to enable secure data sharing and advanced analytics. By 2026, pilot implementations in logistics have demonstrated a 30% improvement in supply chain data security without performance loss. Expanding the technology into SME and emerging markets can capture untapped demand, particularly in Asia Pacific, where digital transformation and regulatory alignment are gaining momentum. Integrating AI privacy frameworks with IoT, cloud platforms, and real-time analytics provides measurable gains in efficiency, trust, and compliance, creating a strategic pathway for market expansion.

Technical costs and regulatory variability pose key challenges to the Privacy Preserving AI Market. Deploying secure AI infrastructures involves high-capacity computational resources, specialized expertise, and advanced encryption tools, often increasing initial investment by over 20%. Regulatory discrepancies, such as varying GDPR interpretations in Europe versus US CCPA requirements, complicate global deployments and necessitate adaptive compliance solutions. Organizations must also balance performance trade-offs, as integrating privacy-preserving methods can reduce processing speed by 10–15%. These challenges create obstacles for smaller firms and limit the pace of widespread adoption despite strong strategic interest in secure AI technologies.

• Expansion of Federated Learning Deployments: Federated learning adoption is accelerating across enterprises, with 62% of AI projects in 2025 incorporating federated frameworks to maintain data privacy while enabling collaborative model training. North America leads with 48% of these deployments, followed by Europe at 32%. Companies report a 28% reduction in sensitive data transfer incidents and a 15% improvement in model training efficiency due to decentralized data processing.

• Integration of Homomorphic Encryption: The use of homomorphic encryption has surged, protecting sensitive computations while maintaining model accuracy. In 2025, over 41% of financial and healthcare AI projects utilized homomorphic encryption for secure analytics. Early adopters reported a 22% reduction in regulatory compliance issues and a 19% improvement in data confidentiality. Asia Pacific shows rising adoption with a 35% increase in enterprise implementations compared to 2024.

• AI-Driven Differential Privacy Implementation: Differential privacy techniques are being embedded into AI pipelines, safeguarding individual-level data. In the past year, 38% of new AI deployments in healthcare and IoT sectors adopted differential privacy frameworks. Measurable benefits include a 30% decrease in potential data exposure and a 20% enhancement in user trust scores across platforms. Enterprises are standardizing these practices in mobile applications and consumer-facing AI services.

• Edge-Based Privacy AI Solutions: Edge computing integration is boosting privacy-preserving capabilities by processing sensitive data locally. In 2025, 29% of privacy-preserving AI applications in smart home devices and industrial IoT implemented edge-based models, cutting cloud data transmission by 40% and reducing latency by 18%. North America leads in adoption, while Europe and Asia are rapidly expanding use cases for industrial automation and healthcare monitoring.

The Privacy Preserving AI market is structured across types, applications, and end-users, enabling targeted adoption strategies. By type, models include vision-language, audio-text, and video-language AI, each with distinct adoption patterns driven by enterprise needs. Application segmentation highlights healthcare, finance, smart devices, and government services, with healthcare leading in deployment due to stringent privacy requirements. End-user segmentation encompasses enterprises, SMEs, and public sector organizations, with enterprises representing the majority of adoption at 57%, while SMEs are rapidly increasing usage in emerging markets. This segmentation provides decision-makers with actionable insights on deployment priorities, technology investments, and potential growth areas.

Vision-language models currently account for 42% of adoption, leading due to their versatility in analyzing images with natural language instructions, particularly in healthcare imaging and autonomous systems. Audio-text systems hold 25% of adoption, providing robust capabilities for voice-driven applications and call center automation. Video-language models are the fastest-growing type, with adoption expected to surpass 30% by 2033, driven by automated video captioning, surveillance analysis, and media indexing. Other types, including multimodal sensor fusion models, represent a combined 8% share, catering to niche industrial and IoT applications.

Healthcare applications dominate the Privacy Preserving AI market, accounting for 38% of adoption, driven by patient data privacy regulations and the need for secure AI diagnostics. Financial services hold 27%, leveraging AI for fraud detection and risk management while preserving sensitive client information. Smart device integration is rapidly expanding, currently 21% of adoption and growing due to IoT proliferation and consumer privacy expectations. Other applications, including government services and education platforms, contribute a combined 14% share.

Enterprises represent the leading end-user segment with 57% adoption, primarily in finance, healthcare, and tech sectors, implementing large-scale privacy-preserving AI frameworks. SMEs are the fastest-growing end-user segment, with adoption projected to increase 28% over the next three years, driven by cost-effective federated AI solutions and cloud-based privacy platforms. Public sector and government organizations account for a combined 15% share, integrating secure AI into citizen services and regulatory compliance initiatives. Industry adoption rates include 62% in healthcare, 55% in finance, and 48% in technology.

North America accounted for the largest market share at 38% in 2025; however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 26% between 2026 and 2033.

North America’s dominance is supported by over 720 enterprise deployments in healthcare and finance, with more than 85 petaflops of AI model training capacity annually. Asia Pacific, led by China, India, and Japan, is rapidly scaling infrastructure with 45% of SMEs adopting privacy-preserving AI frameworks and mobile AI apps penetrating over 120 million devices. Europe follows with 28% adoption, driven by regulatory requirements and 32 pilot projects integrating federated learning. South America and Middle East & Africa collectively account for 12% of the global market, with Brazil and UAE leading regional adoption. Cloud-based AI platforms and edge computing solutions have increased data processing efficiency by 21% across these regions, while investment in encrypted AI services exceeded USD 1.1 Billion globally in 2025.

How are secure AI frameworks reshaping enterprise adoption?

North America holds a 38% share of the privacy-preserving AI market, driven primarily by finance, healthcare, and technology industries. Regulatory developments such as enhanced HIPAA enforcement and federal data privacy initiatives have accelerated adoption, with over 65% of enterprises implementing federated learning or homomorphic encryption. Technological advancements, including AI-driven differential privacy and edge-based AI solutions, have improved model efficiency by 18–25%. Local players, such as IBM, have deployed large-scale privacy-preserving AI frameworks for healthcare diagnostics and financial risk analysis, reducing sensitive data exposure by 28%. Consumer behavior reflects higher enterprise adoption in healthcare and finance sectors, with growing interest in secure mobile and cloud applications among US and Canadian enterprises.

What regulatory pressures are influencing enterprise AI strategies?

Europe accounts for 28% of the global Privacy Preserving AI market, with Germany, the UK, and France as leading contributors. Stringent GDPR regulations and sustainability initiatives have fostered demand for explainable AI models, particularly in banking, healthcare, and government services. Emerging technologies such as federated learning, homomorphic encryption, and AI auditing platforms are increasingly integrated into enterprise AI systems. Local player Siemens has implemented privacy-preserving AI solutions in smart manufacturing, improving secure data sharing across supply chains. Regional consumer behavior is heavily influenced by compliance-driven adoption, with enterprises prioritizing explainability and secure analytics in sensitive sectors.

How is rapid digitalization driving AI adoption in emerging markets?

Asia Pacific represents 22% of the global market, with China, India, and Japan as the top consuming countries. The region is expanding infrastructure for AI model training, with over 60 high-performance computing centers operational in 2025. Innovation hubs in Singapore and South Korea are advancing federated learning and differential privacy solutions for healthcare and e-commerce applications. Local player Baidu has launched privacy-preserving AI frameworks for cloud and mobile AI services, reaching over 50 million users. Consumer adoption is driven by mobile AI apps and e-commerce personalization, with 48% of enterprises deploying secure AI solutions for customer data analytics.

What factors are driving AI adoption in media and public services?

South America accounts for 7% of the Privacy Preserving AI market, with Brazil and Argentina leading regional adoption. The market is supported by expanding digital infrastructure and AI integration in media, banking, and energy sectors. Government incentives and trade policies encourage the development of secure AI platforms, particularly for data localization compliance. Local player TOTVS has deployed privacy-preserving AI solutions for financial services, reducing client data exposure by 24%. Regional consumer behavior emphasizes media consumption, language localization, and secure digital services, reflecting demand patterns in urban centers and financial institutions.

How are industrial modernization and regulations shaping AI adoption?

Middle East & Africa hold 5% of the global Privacy Preserving AI market, with UAE and South Africa as primary growth countries. Demand is driven by oil & gas, construction, and government digital transformation projects. Technological modernization trends include edge-based AI and secure cloud platforms to handle sensitive operational data. Local regulations, such as national data protection laws, are shaping adoption, and trade partnerships facilitate access to advanced AI technologies. Regional players in UAE have implemented AI solutions in smart city initiatives, enhancing data security by 21%. Consumer behavior is influenced by industrial and public sector priorities, with rising interest in secure citizen and enterprise AI applications.

United States: 38% – High production capacity, robust enterprise adoption in healthcare and finance, and strong regulatory support.

China: 20% – Rapid SME adoption, advanced AI infrastructure, and extensive mobile and cloud AI ecosystem driving secure AI deployments.

The Privacy Preserving AI market is moderately fragmented, with over 50 active competitors globally. The top five players – IBM, Microsoft, Google, Intel, and NVIDIA – collectively control approximately 62% of the market, leveraging technology leadership and strategic initiatives. Product innovation is focused on federated learning platforms, homomorphic encryption solutions, and differential privacy frameworks. Partnerships and collaborations between cloud providers and enterprise technology firms are increasing, with over 28 joint initiatives launched in 2025 to enhance secure AI adoption. Mergers and acquisitions are reshaping competitive positioning, while smaller niche players specialize in edge-based privacy AI and AI auditing tools. The market is characterized by high R&D intensity, with more than 40 pilot projects in healthcare, finance, and smart devices, demonstrating measurable efficiency gains of 18–28% in sensitive data handling. Regional deployment variations, consumer adoption trends, and regulatory compliance requirements continue to influence competitive strategies and market positioning, highlighting the importance of technological differentiation and strategic collaboration.

IBM

Microsoft

Intel

NVIDIA

HPE

Palantir Technologies

OpenAI

Amazon Web Services

Baidu

The Privacy Preserving AI market is driven by a suite of advanced technologies that enable secure, compliant data analytics and model training without exposing sensitive information. Federated learning remains a cornerstone, allowing AI models to be trained across decentralized datasets without centralizing raw data, and in 2025 it represented the largest technology segment at approximately 29% share of market deployments. This method reduces data transfer risks and accommodates stringent localization laws that restrict cross‑border data movement.

Homomorphic encryption enables computations on encrypted data, preserving confidentiality throughout the AI workflow; in 2025 this approach held roughly 35.6% adoption as enterprises sought encrypted processing that prevents sensitive data exposure during AI training and inference. Differential privacy is also gaining traction, introducing mathematically bounded noise into model training to prevent individual data points from being inferred, and techniques rooted in this paradigm are now being applied at scale for models such as large language models trained with strict privacy guarantees. The emergence of confidential computing—which uses hardware‑based trusted execution environments to keep data encrypted even while in use—has been integrated into cloud and edge platforms, enabling AI workloads in regulated industries like healthcare.

Edge AI architectures have been optimized for privacy‑centric use cases, processing data locally on devices to cut cloud traffic and reduce exposure of personally identifiable information. Synthetic data generation tools are another emerging trend, producing privacy‑safe datasets that mirror real statistical patterns while excluding sensitive identifiers, which aids in model training and validation. Overall, the technological landscape emphasizes privacy‑by‑design, blending decentralized learning, encryption, and secure hardware to meet enterprise requirements for confidentiality, compliance, and performance.

• In September 2025, Google introduced VaultGemma, a 1‑billion‑parameter large language model trained from scratch using differential privacy, designed to prevent memorization of training data and support secure AI workflows in regulated sectors such as healthcare and finance.

• In February 2025, the AI‑RAN Alliance was formed by industry leaders including NVIDIA, Samsung, and Microsoft to integrate privacy‑preserving techniques into cellular technology analytics, enabling secure analysis across diverse network environments through advanced AI collaboration.

• In December 2024, Zama launched its open‑source fhEVM (Fully Homomorphic Encryption Virtual Machine), enabling confidential smart contracts on Ethereum‑compatible blockchains, allowing encrypted on‑chain data processing and enhancing application privacy for AI and decentralized systems.

• In October 2024, Gretel AI introduced enhanced privacy‑safe synthetic text data features that allow developers to fine‑tune large language models on transformed datasets that protect sensitive content while preserving statistical and contextual value.

The Privacy Preserving AI Market Report covers a comprehensive range of market segments, technologies, use cases, and geographic insights tailored for strategic decision‑making. The scope includes detailed segmentation by technology—federated learning, homomorphic encryption, differential privacy, secure multi‑party computation, confidential computing, and synthetic data generation—highlighting how each contributes to secure AI workflows and adoption patterns across industries. Deployment modes such as cloud, edge, and on‑device AI are analyzed to reflect differences in data locality requirements and infrastructure choices. The report examines application areas including healthcare, financial services, telecommunications, smart devices, and government services, each with specific privacy needs for analytics, personalization, and regulatory compliance.

Geographically, the report provides region‑wise insights into North America, Europe, Asia Pacific, South America, and Middle East & Africa, detailing market volume dynamics, infrastructure readiness, and local innovation hubs. End‑user profiles, from large enterprises to SMEs and public sector organizations, are assessed for adoption behavior, technology preferences, and sector‑specific privacy priorities. The study also explores niche and emerging segments such as privacy‑preserving on‑device AI for mobile ecosystems and federated analytics for cross‑organization research collaborations. Emerging use cases like secure model training on synthetic datasets, confidential computing for regulated workloads, and real‑time privacy enforcement frameworks are included to inform future investment and technology strategy decisions. The report’s breadth ensures stakeholders understand both current capabilities and directional trends shaping secure, privacy‑centric artificial intelligence.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

25.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

IBM, Microsoft, Google, Intel, NVIDIA, HPE, Palantir Technologies, OpenAI, Amazon Web Services, Baidu |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |