Reports

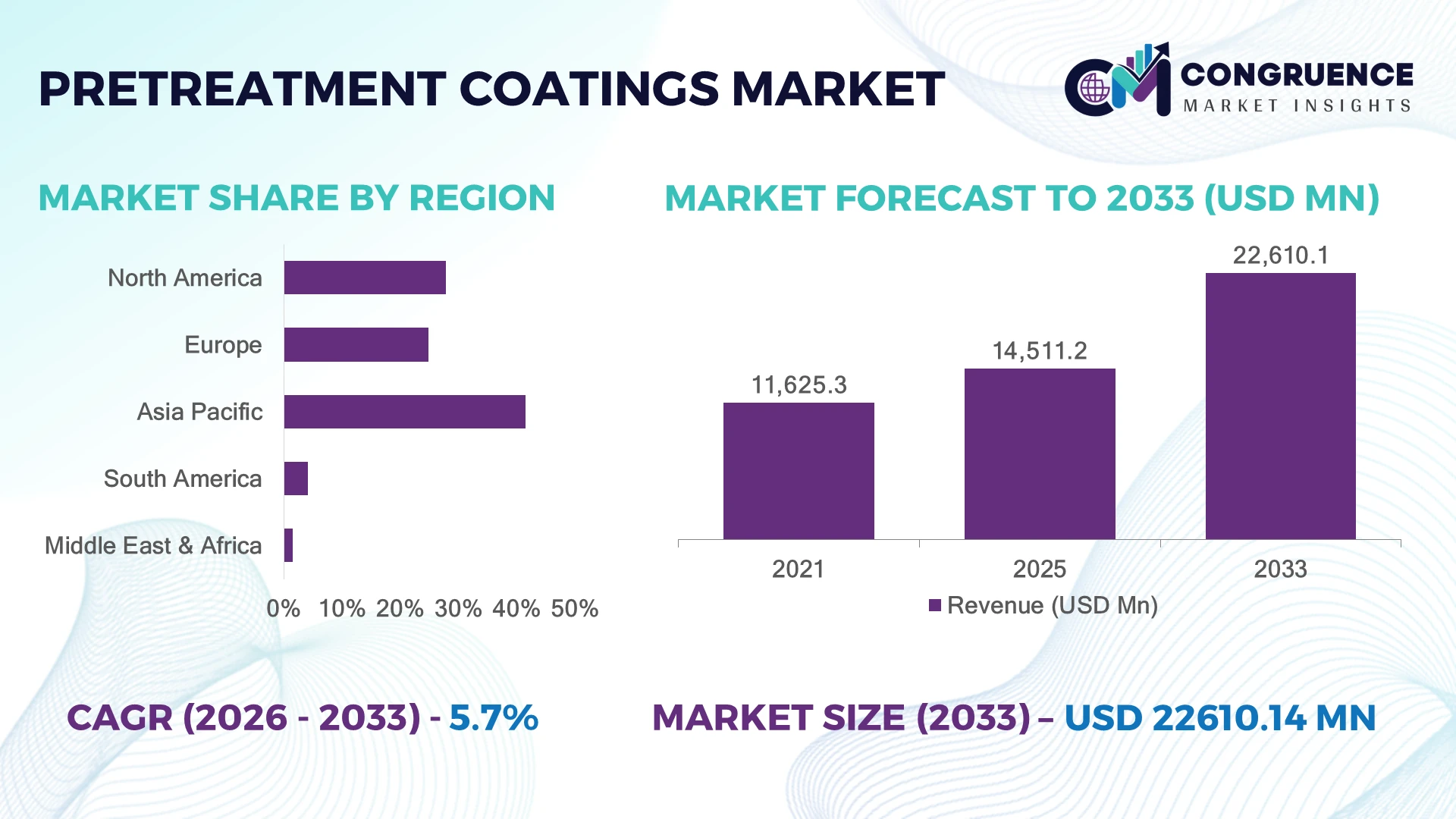

The Global Pretreatment Coatings Market was valued at USD 14,511.2 Million in 2025 and is anticipated to reach a value of USD 22,610.1 Million by 2033 expanding at a CAGR of 5.7% between 2026 and 2033. Growing adoption of corrosion-resistant coatings, lightweight materials, sustainable surface treatment technologies, and advanced manufacturing processes is driving demand for high-performance pretreatment coating solutions.

China dominated the Pretreatment Coatings Market with nearly 32% share in 2025, supported by large-scale automotive production, industrial manufacturing, and metal processing infrastructure. China accounted for over 30% of global vehicle production, compared with approximately 12% contribution from the United States. Supply-chain restructuring and stricter environmental regulations following global industrial shifts are accelerating investments in low-emission coating technologies and localized production capabilities.

Manufacturers adopting advanced pretreatment coating technologies are strengthening product durability, regulatory compliance, and long-term competitive positioning.

• Market Size & Growth: The market reached USD 14,511.2 Million in 2025 and is projected at USD 22,610.1 Million by 2033 with 5.7% CAGR, driven by sustainable coating technologies.

• Top Growth Drivers: Automotive coating demand increased 35%, industrial surface protection adoption rose 30%, and lightweight material usage expanded 28%.

• Short-Term Forecast: By 2028, advanced pretreatment technologies are expected to improve coating adhesion performance by nearly 25%.

• Emerging Technologies: Nanocoatings, chrome-free pretreatments, and automated surface treatment systems are transforming coating performance.

• Regional Leaders: Asia-Pacific, North America, and Europe are projected to reach USD 10 Billion, USD 6 Billion, and USD 5 Billion respectively through industrial modernization.

• Consumer/End-User Trends: Over 50% of manufacturers are shifting toward environmentally compliant surface treatment solutions.

• Pilot/Case Example: In 2025, advanced pretreatment implementation reduced coating defects by nearly 22% across automated production facilities.

• Competitive Landscape: Leading companies hold nearly 42% share, including PPG Industries, AkzoNobel, Henkel, and BASF.

• Regulatory & ESG Impact: Low-VOC and chrome-free technologies reduced hazardous chemical dependency by approximately 30%.

• Investment & Funding: Over USD 3 Billion investments target coating innovation, sustainable chemistry, and production expansion.

• Innovation & Future Outlook: Smart surface technologies and sustainable formulations are reshaping next-generation coating ecosystems.

Pretreatment Coatings are increasingly used across automotive, aerospace, construction, appliances, and industrial equipment sectors to improve corrosion resistance and surface durability. Advanced chemical conversion technologies and eco-friendly formulations are improving coating performance by nearly 25%. Increasing environmental compliance requirements and manufacturing automation are driving the shift toward cleaner, high-efficiency pretreatment solutions.

The Pretreatment Coatings Market is becoming strategically important as manufacturers prioritize durability, sustainability, and regulatory compliance across global production ecosystems. Automotive, aerospace, and industrial equipment companies are transitioning toward advanced surface treatment solutions to improve material protection and production efficiency. Environmental regulations in Europe, the United States, and China are accelerating replacement of conventional chemical processes with safer alternatives.

Compared with traditional phosphate-based systems, next-generation zirconium and nanotechnology-based pretreatments reduce chemical consumption by nearly 35% and improve processing efficiency by approximately 25%. Asia-Pacific leads through manufacturing scale and industrial expansion, while Europe focuses on sustainable chemistry innovation and stricter environmental performance standards.

Automotive plants and metal fabrication facilities are deploying automated pretreatment systems to enhance coating consistency and reduce operational waste. Companies are investing in R&D, low-impact chemistries, and partnerships with OEMs to improve application-specific solutions. Future competitiveness will depend on delivering efficient, compliant, and high-performance surface protection technologies.

Rising automotive production and increasing durability requirements are driving adoption of advanced pretreatment coatings across vehicle manufacturing and metal processing applications. Nearly 45% of automotive coating operations use enhanced surface preparation technologies to improve adhesion and corrosion resistance, while lightweight material adoption has increased pretreatment requirements by approximately 30%. Stricter environmental regulations are encouraging manufacturers to replace traditional chemical systems with sustainable alternatives. Companies are responding through chrome-free technology development, capacity expansion, and partnerships with automotive OEMs to improve coating performance and compliance.

Pretreatment coating manufacturers face challenges from evolving chemical regulations, raw material volatility, and conversion costs associated with sustainable alternatives. Nearly 35% of coating producers are modifying formulations to meet stricter environmental requirements, while technology transitions increase operational complexity by around 25%. Restrictions on hazardous substances are reshaping supply chains and production processes. Companies are reducing risks through green chemistry investments, alternative material sourcing, and advanced process optimization to maintain performance while meeting regulatory expectations.

Growing adoption of sustainable manufacturing is creating opportunities for next-generation pretreatment coatings with improved efficiency and reduced environmental impact. Nearly 40% of industrial manufacturers are increasing investment in eco-friendly surface treatment solutions. Nanotechnology-based coatings, smart surface treatments, and low-temperature processing technologies are improving protection performance while reducing energy consumption. Companies are expanding innovation pipelines, collaborating with OEMs, and developing customized solutions for electric vehicles, aerospace materials, and advanced manufacturing applications.

Expanding use of mixed materials and advanced manufacturing processes creates challenges in achieving consistent pretreatment coating performance across diverse substrates. Nearly 30% of manufacturers report difficulties optimizing surface treatments for multi-material assemblies. Electric vehicles, lightweight alloys, and automated production lines require higher precision and process control. Companies must strengthen testing capabilities, digital monitoring systems, and application engineering expertise to ensure reliable coating performance and maintain competitiveness in evolving industrial environments.

• Chrome-Free Technology Transition: Manufacturers are accelerating adoption of environmentally safer pretreatment formulations due to stricter chemical regulations. Nearly 42% of industrial coating users are shifting toward chrome-free alternatives. Companies are expanding sustainable chemistry portfolios and reformulating products to maintain corrosion resistance while reducing environmental impact.

• Nanotechnology Surface Enhancement: Advanced nano-based pretreatment solutions are improving coating adhesion, durability, and material compatibility. These technologies are increasing surface protection efficiency by nearly 28% and reducing chemical usage by approximately 20%. Manufacturers are investing in research partnerships and specialized formulations for high-performance applications.

• Automated Pretreatment Integration: Industrial facilities are adopting automated coating preparation systems to improve consistency and production efficiency. Around 35% of modern manufacturing lines include digitally controlled surface treatment processes. Companies are integrating sensors, monitoring tools, and automation platforms to reduce defects and improve throughput.

• Multi-Material Coating Solutions: Lightweight manufacturing trends are increasing demand for pretreatments compatible with aluminum, composites, and advanced alloys. Nearly 30% of automotive material strategies now involve mixed-material designs. Suppliers are developing flexible coating technologies and customized solutions to support next-generation product engineering.

Conversion coatings dominate the Pretreatment Coatings Market due to their strong corrosion resistance, cost efficiency, and compatibility with large-scale automotive, industrial, and metal fabrication processes. Conversion coatings account for nearly 46% of adoption, supported by extensive use of phosphate, zirconium, and advanced chemical treatment systems that enhance coating adhesion and product durability. Nanotechnology-based pretreatment coatings are witnessing the fastest adoption growth as manufacturers transition toward high-performance, low-chemical solutions with improved environmental compliance.

Blast cleaning, chemical cleaning, and other pretreatment coating types continue supporting specialized industrial applications where surface preparation quality and substrate compatibility are critical. Nearly 38% of manufacturers are shifting toward advanced and eco-friendly pretreatment technologies to improve process efficiency and reduce chemical dependency. Companies are responding through sustainable formulation development, automated coating systems, and partnerships with automotive and industrial manufacturers to strengthen performance-focused solutions.

• A 2025 industrial coatings technology assessment highlighted that manufacturers adopting advanced surface pretreatment solutions improved corrosion protection performance by nearly 30%, supporting wider deployment across automotive, aerospace, and precision manufacturing operations.

Automotive applications represent the leading segment in the Pretreatment Coatings Market due to extensive requirements for corrosion prevention, paint adhesion improvement, and long-term vehicle durability. The segment accounts for nearly 42% of demand as manufacturers integrate advanced surface treatment technologies across body structures, components, and lightweight materials. Aerospace applications are emerging as the fastest-growing segment, supported by increasing use of aluminum alloys, composites, and high-performance materials requiring specialized pretreatment solutions.

Construction, appliances, industrial machinery, and other applications continue adopting pretreatment coatings to improve product lifespan, surface quality, and environmental resistance. Nearly 35% of industrial manufacturers are upgrading surface preparation processes to support higher durability standards and regulatory requirements. Companies are adapting through automated treatment lines, customized coating chemistries, and material-specific innovation to address evolving performance expectations.

• A 2026 manufacturing technology review indicated that advanced pretreatment coating implementation reduced coating defects by approximately 25%, improving production consistency across automotive, aerospace, and industrial equipment manufacturing environments.

Manufacturing industries represent the dominant end-user group in the Pretreatment Coatings Market due to large-scale adoption across automotive production, machinery, metal fabrication, and component manufacturing operations. This segment accounts for approximately 52% of demand as companies prioritize corrosion resistance, product reliability, and improved finishing quality. Aerospace and transportation industries are witnessing the fastest expansion due to increasing adoption of lightweight materials and stricter performance requirements.

Construction companies, electronics manufacturers, and other industrial users continue integrating pretreatment coatings to improve material protection and operational efficiency. Around 40% of large manufacturers are increasing investment in advanced surface treatment systems to enhance productivity and compliance. Coating suppliers are targeting these sectors through customized formulations, technical support partnerships, and sustainable chemistry solutions aligned with changing industrial requirements.

• A 2025 industrial manufacturing survey reported that companies deploying advanced pretreatment technologies achieved nearly 28% improvement in coating consistency and process efficiency, accelerating adoption across high-performance production environments.

Asia-Pacific accounted for the largest market share at 41.5% in 2025 moreover, Asia-Pacific is also expected to register the fastest growth, expanding at a CAGR of 6.6% between 2026 and 2033.

North America Pretreatment Coatings Market is driven by strong demand across automotive production, aerospace manufacturing, industrial equipment, and advanced metal processing operations. The region accounted for 27.8% market share in 2025, supported by increasing replacement of conventional chemical processes with environmentally compliant surface treatment technologies. Nearly 45% of manufacturing facilities are adopting advanced pretreatment solutions to improve corrosion resistance, coating durability, and production efficiency. Automotive and aerospace companies are accelerating implementation of chrome-free coatings, automated pretreatment lines, and high-performance surface technologies. Manufacturers are investing in sustainable chemistry innovation and technical partnerships to address stricter environmental standards and evolving material requirements.

United States Market Outlook: The United States leads regional adoption through its advanced automotive, aerospace, and industrial manufacturing ecosystem. Companies are expanding use of low-VOC and chrome-free pretreatment technologies to improve regulatory compliance and product performance. Nearly 50% of major industrial coating operations are transitioning toward advanced surface preparation systems, supporting stronger demand for innovative pretreatment coating solutions.

Europe’s Pretreatment Coatings Market is shaped by strict environmental regulations, automotive innovation, and increasing demand for sustainable industrial coating technologies. The region accounted for nearly 24.9% market share in 2025, with Germany, France, and Italy driving adoption across automotive manufacturing, aerospace components, and precision engineering sectors. Around 42% of industrial manufacturers are shifting toward environmentally optimized pretreatment processes to reduce chemical usage and improve operational sustainability. Companies are focusing on nanotechnology-based coatings, recyclable materials, and energy-efficient treatment processes to maintain competitive advantages.

Germany Market Outlook: Germany represents the strongest European market due to its automotive manufacturing leadership, advanced engineering capabilities, and focus on sustainable production technologies. Automotive OEMs and component suppliers are increasing adoption of next-generation pretreatment systems for lightweight materials. Nearly 45% of advanced manufacturing plants are implementing improved surface treatment solutions to enhance coating quality and durability.

Asia-Pacific dominates the Pretreatment Coatings Market due to extensive automotive production, electronics manufacturing, construction activity, and industrial expansion. The region accounted for 41.5% market share in 2025, supported by strong production ecosystems across China, Japan, South Korea, and India. More than 50% of regional metal finishing operations are adopting improved pretreatment technologies to enhance corrosion protection and surface performance. Companies are expanding manufacturing capacity, strengthening supplier networks, and introducing cost-efficient sustainable coating solutions to serve growing industrial demand.

China Market Outlook: China leads regional demand through large-scale automotive production, industrial manufacturing capacity, and expanding surface treatment technology adoption. Domestic manufacturers are investing in advanced coating lines and environmentally compliant processes. The country contributes more than 30% of global vehicle production, creating significant demand for high-performance pretreatment coatings across automotive and component manufacturing sectors.

South America’s Pretreatment Coatings Market is expanding through automotive manufacturing, infrastructure development, and increasing adoption of industrial surface protection solutions. The region accounted for nearly 4.2% market share in 2025, with demand concentrated across transportation equipment, construction materials, and machinery production. Around 30% of industrial manufacturers are upgrading coating processes to improve durability and reduce maintenance requirements. Limited availability of advanced processing infrastructure remains a challenge, while coating suppliers are strengthening distribution networks and technical support services.

Brazil Market Outlook: Brazil represents the leading regional market due to its automotive production base, metal fabrication industry, and expanding industrial sector. Manufacturers are increasing adoption of advanced pretreatment technologies for vehicle components, machinery, and infrastructure applications. Nearly 35% of major manufacturing operations are investing in improved surface protection systems to enhance product reliability and competitiveness.

Middle East & Africa Pretreatment Coatings Market is supported by infrastructure expansion, industrial diversification, and increasing demand for corrosion-resistant materials in harsh operating environments. The region accounted for nearly 1.6% market share in 2025, with adoption focused across construction, energy facilities, and manufacturing operations. More than 28% of large industrial projects are integrating advanced coating solutions to improve asset durability and lifecycle performance. Companies are expanding regional partnerships, technical services, and specialized coating solutions designed for extreme environmental conditions.

United Arab Emirates Market Outlook: The United Arab Emirates leads regional adoption through infrastructure development, manufacturing expansion, and investment in advanced industrial technologies. Construction, transportation, and energy sectors are adopting high-performance pretreatment coatings for improved material protection. Around 40% of major infrastructure projects emphasize durable and sustainable materials, supporting demand for advanced surface treatment solutions.

The Pretreatment Coatings Market is led by PPG Industries, AkzoNobel, Henkel, BASF, and Sherwin-Williams, where global coating manufacturers compete with specialty chemical suppliers and regional surface treatment providers. The top five players collectively hold approximately 42% share, reflecting a technology-focused structure driven by formulation expertise and industrial relationships. Competition is based on corrosion performance, sustainability, process efficiency, and customization, with advanced pretreatment technologies improving coating durability by nearly 30% and reducing chemical consumption by around 25%. Companies are competing through sustainable chemistry development, production expansion, OEM partnerships, and application-specific innovation. The competitive shift is moving toward chrome-free technologies, nanotechnology-based solutions, and automated surface treatment systems. Strict regulatory requirements, technical validation processes, and formulation complexity create strong entry barriers. Winning against established players requires advanced coating technologies, sustainability leadership, and strong industrial application expertise.

• PPG Industries, Inc.

• Akzo Nobel N.V.

• Henkel AG & Co. KGaA

• BASF SE

• The Sherwin-Williams Company

• Axalta Coating Systems Ltd.

• Nippon Paint Holdings Co., Ltd.

• Kansai Paint Co., Ltd.

• Chemetall GmbH

• 3M Company

• Troy Chemical Industries Inc.

• Houghton International Inc.

• Wacker Chemie AG

• Solvay S.A.

Pretreatment coating technologies are advancing through chrome-free formulations, nanotechnology-based coatings, zirconium conversion systems, and automated surface treatment processes. Modern pretreatment solutions are improving adhesion strength, corrosion resistance, and environmental performance, with nearly 45% of advanced manufacturing facilities adopting sustainable surface treatment technologies for regulatory compliance and operational efficiency.

Compared with conventional phosphate-based systems, next-generation nanotechnology and zirconium pretreatment solutions reduce chemical usage by approximately 35% and improve processing efficiency by nearly 25% through lower operating temperatures and simplified application processes. Automated monitoring systems enhance coating consistency by around 20%, allowing automotive, aerospace, and industrial manufacturers to improve quality control. Companies with sustainable chemistry platforms and advanced application engineering capabilities are gaining stronger competitive advantages.

Between 2026 and 2028, pretreatment coating innovation will focus on smart surface technologies, multi-material compatibility, and low-impact chemical systems. Manufacturers adopting next-generation pretreatment technologies will improve productivity, sustainability compliance, and competitiveness across high-performance manufacturing industries.

• February 2025 – PPG Industries expanded its sustainable coating technology portfolio with advanced surface treatment solutions, improving corrosion protection performance by nearly 25%. The development strengthened support for automotive and industrial manufacturers transitioning toward environmentally efficient pretreatment systems. Source: ppg.com

• September 2024 – Henkel introduced advancements across its BONDERITE surface treatment solutions, enhancing process efficiency and reducing resource consumption by approximately 30%. The innovation supported automotive and metal processing manufacturers adopting sustainable pretreatment technologies. Source: henkel.com

• May 2025 – AkzoNobel accelerated development of sustainable coating technologies with improved industrial application performance, increasing coating process efficiency by nearly 20%. The initiative strengthened customer transition toward lower-impact surface protection solutions. Source: akzonobel.com

• April 2024 – Axalta expanded its industrial coatings innovation strategy with enhanced surface preparation and coating technologies designed for improved durability and operational reliability. The development supported manufacturers requiring higher-performance finishing systems and advanced material protection. Source: axalta.com

The Pretreatment Coatings Market Report provides detailed analysis across coating types, applications, end-users, regional dynamics, technology innovation, and competitive strategies. The study covers conversion coatings, blast cleaning, chemical cleaning, nanotechnology-based pretreatments, and other surface preparation technologies used across automotive, aerospace, construction, appliances, and industrial manufacturing applications. More than 45% of adoption is concentrated across transportation and advanced manufacturing sectors requiring high-performance corrosion protection.

The report evaluates North America, Europe, Asia-Pacific, South America, and Middle East & Africa with insights into sustainability trends, manufacturing transformation, and regulatory-driven technology shifts. It examines chrome-free coatings, automated treatment systems, smart surface technologies, and advanced material compatibility shaping market direction between 2026 and 2033. The analysis supports investment planning, product innovation, competitive benchmarking, and expansion strategies across the evolving surface treatment industry.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 14,511.2 Million |

|

Market Revenue in 2033 |

USD 22,610.1 Million |

|

CAGR (2026 - 2033) |

5.7% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

PPG Industries, Inc., Akzo Nobel N.V., Henkel AG & Co. KGaA, BASF SE, The Sherwin-Williams Company, Axalta Coating Systems Ltd., Nippon Paint Holdings Co., Ltd., Kansai Paint Co., Ltd., Chemetall GmbH, 3M Company, Troy Chemical Industries Inc., Houghton International Inc., Wacker Chemie AG, Solvay S.A. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |