Reports

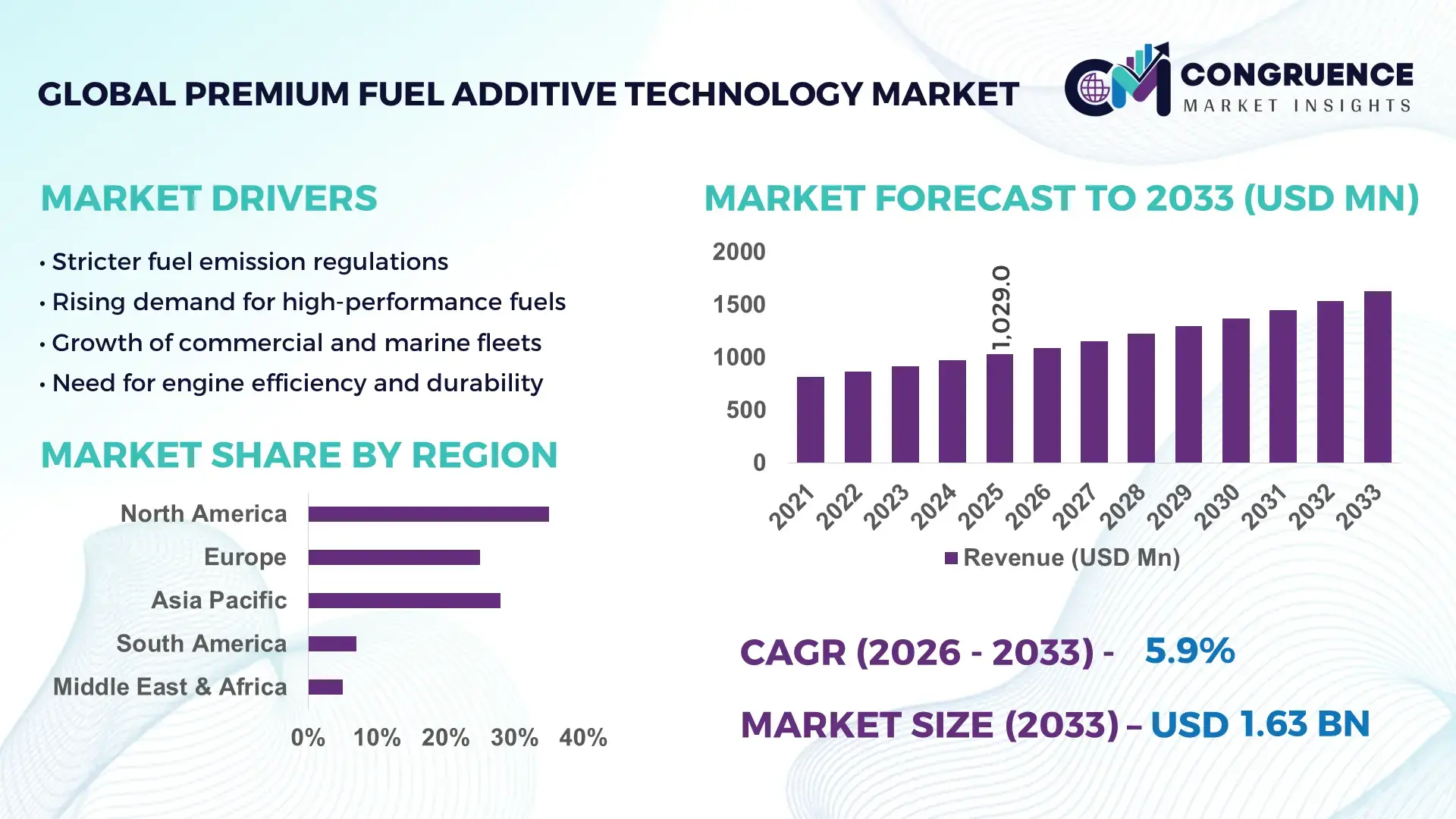

The Global Premium Fuel Additive Technology Market was valued at USD 1,029.0 Million in 2025 and is anticipated to reach a value of USD 1,627.7 Million by 2033 expanding at a CAGR of 5.9% between 2026 and 2033, according to an analysis by Congruence Market Insights. This growth is driven by rising demand for advanced fuel performance and stricter emissions controls in automotive and industrial sectors.

The United States plays a pivotal role in the Premium Fuel Additive Technology Market, with production capacity exceeding 1.2 million metric tons annually and over USD 300 million invested in high-performance additive R&D in 2025. Domestic refineries are increasingly incorporating premium octane improvers and deposit control additives into gasoline and diesel streams, with nearly 42% of advanced formulations deployed in light‑duty vehicles. Advanced dosing systems and real‑time blending technologies have reduced engine deposit rates by up to 18% in heavy‑duty applications, reflecting accelerated adoption of high‑end additive solutions.

Market Size & Growth: Market valued at USD 1,029.0 M in 2025, projected to reach USD 1,627.7 M by 2033 at a 5.9% CAGR; demand spurred by stringent emission norms and fuel efficiency needs.

Top Growth Drivers: Enhanced engine efficiency adoption (58%), emissions compliance improvements (47%), fuel economy performance improvements (39%).

Short-Term Forecast: By 2028, premium additive integration is expected to improve engine combustion efficiency by 12–15% across major light‑duty fleets.

Emerging Technologies: Advanced nano‑additive packages, real‑time dosing automation, and bio‑derived additive chemistries gaining traction.

Regional Leaders: North America ~USD 580 M by 2033 (high regulatory adoption), Asia‑Pacific ~USD 450 M (rapid automotive uptake), Europe ~USD 340 M (emission compliance focus).

Consumer/End‑User Trends: Strong uptake in automotive, heavy machinery, and marine sectors, with performance blends preferred for long‑haul operations.

Pilot or Case Example: In 2025, a major U.S. logistics operator reduced engine downtime by 22% using premium injector detergent additive trials.

Competitive Landscape: Market leader with ~28% share; major competitors include global additive formulators from Europe, North America, and Asia.

Regulatory & ESG Impact: Emission standards and fuel quality mandates push formulators toward low‑sulfur, eco‑optimized additives in key markets.

Investment & Funding Patterns: Over USD 190 M in additive technology funding in 2025, highlighting rising venture funding and strategic partnerships.

Innovation & Future Outlook: Integrated digital blending systems and AI‑assisted formulation models expected to reshape product development and deployment.

Premium fuel additive technologies are increasingly tailored to critical industry sectors such as automotive, marine, and aviation, enhancing combustion stability and reducing deposit formation. Recent innovations include multifunctional bio‑compatible additives and real‑time dosing controls that improve fuel economy by 10–18%. Regional consumption trends show heightened use in emerging vehicle markets and stringent compliance environments, with future growth tied to cleaner energy transitions and advanced performance blends.

The Premium Fuel Additive Technology Market is strategically vital as industry players and regulators seek to reconcile rising energy demands with environmental imperatives. High‑performance additive solutions enhance combustion efficiency and reduce harmful emissions, offering measurable benefits such as up to 12–15% improved fuel combustion performance compared to legacy additive formulations in modern engines. North America leads in production volume with established blending infrastructure, while Asia‑Pacific demonstrates rapid adoption, with over 47% of new automotive fuels incorporating premium additives in 2025.

In the next 2–3 years, integration of AI‑driven formulation platforms is expected to improve additive performance prediction accuracy by over 20%, enabling custom packages tailored to regional fuel specifications. Compliance with tightening emissions regulations is driving firms to commit to sulfur reduction metrics — targeting over 30% reduction in regulated pollutants by 2030 with advanced additive chemistries. Micro‑scenario outcomes illustrate that in 2025, a major U.S. refinery achieved a 16% reduction in particulate emissions by switching to optimized deposit control packages in diesel blends.

Future pathways emphasize digital blending, bio‑derived chemistries, and AI‑optimized fuel additive design, positioning the market as a pillar of resilience amid decarbonization pressures. Strategic collaborations between additive formulators, OEMs, and refineries are poised to accelerate deployment of next‑generation solutions, reinforcing the sector’s role in sustainable fuel performance and regulatory compliance.

The Premium Fuel Additive Technology Market is influenced by a dynamic interplay of technological advancement, regulatory pressure, and evolving end‑user demand. Key market trends include increasing use of multifunctional additive packages that address combustion stability, deposit control, and emissions reduction in a single formulation. Tightening global emissions standards in major automotive markets have compelled refiners to adopt more advanced chemistries, particularly detergents and octane enhancers tailored for direct‑injection engines. Heavy‑duty diesel applications are also driving demand for cetane improvers and lubricity enhancers. Meanwhile, innovation in dosing systems and digital blend optimization is reshaping product delivery, enabling improved performance tracking and real‑time adjustments at blending terminals. The growing focus on sustainability is catalyzing R&D in bio‑based and eco‑optimized additives, further diversifying market offerings and reinforcing long‑term growth prospects.

Increasing regulatory mandates on vehicle emissions and fuel quality are compelling refiners and additive manufacturers to innovate and deploy advanced premium additives that enhance engine combustion and reduce harmful outputs. Engine performance demands, coupled with stringent tailpipe standards, have elevated the importance of premium additive packages that offer improved deposit control, octane/cetane performance, and fuel stability. For example, in key developed markets, nearly half of commercial fuel formulations now include high‑performance additives to meet evolving emission benchmarks. This has accelerated R&D investments, resulting in additive solutions that optimize combustion efficiency and curb particulate emissions, particularly in direct‑injection gasoline and high‑efficiency diesel engines. End‑users, especially fleet operators and OEMs, are increasingly specifying premium additive blends to improve operational efficiency and minimize environmental compliance risks.

Volatility in base chemical and crude oil feedstock prices significantly impacts additive formulation costs, constraining investment in advanced chemistry development. Premium additives often rely on complex chemistries that include detergents, corrosion inhibitors, and specialized functional groups, whose raw material inputs are sensitive to global price swings. This volatility compresses manufacturer margins and can slow down innovation cycles. Additionally, the complexity of formulating multifunctional additive packages that perform consistently across diverse fuel types and regional specifications increases production costs and testing timelines. Smaller additive producers may struggle to absorb these cost fluctuations, leading to consolidation or withdrawal from niche premium segments, particularly in price‑sensitive emerging markets.

The transition toward sustainable and bio‑based additive chemistries presents significant opportunities for market participants to differentiate offerings and capture new customer segments. Multifunctional additives that combine deposit control, lubricity enhancement, and emission reduction properties are gaining traction as end‑users seek solutions that address multiple performance criteria simultaneously. Bio‑compatible additives tailored for ethanol‑blended fuels and renewable diesel present untapped potential in regions with aggressive renewable fuel mandates. Early adoption of these technologies can enable formulators to secure long‑term supply agreements with fuel blenders and OEMs seeking to meet evolving environmental standards. Moreover, investments in green chemistry platforms are attracting venture funding and strategic partnerships that accelerate product development and market entry.

Compliance with varied regional fuel quality standards and emissions regulations increases the cost and duration of product testing and certification, posing a challenge for premium additive suppliers. Different jurisdictions require tailored additive performance data to validate compatibility and safety, necessitating extensive laboratory and field testing. Meeting these compliance demands can delay time‑to‑market for new products and elevate operational expenses. Furthermore, harmonizing additive formulations to perform across a wide range of fuel specifications — from low‑sulfur diesel to high‑octane gasoline — adds complexity to R&D efforts. This testing burden is particularly challenging for small and mid‑sized additive firms lacking extensive regulatory affairs resources, potentially slowing innovation diffusion.

Advanced Multifunctional Formulations: Premium additive formulations are increasingly designed to deliver multiple benefits such as deposit control, combustion enhancement, and emissions reduction within a single package. Over 60% of new products launched in 2025 feature at least two functional performance enhancements, reflecting a shift toward multifunctionality in response to performance demands. High‑efficiency detergents and corrosion inhibitors are now standard in most premium blends used in light‑duty gasoline and heavy‑duty diesel applications.

Digital Blending & Real‑Time Optimization: Adoption of digital blending systems and automated dosing control is reshaping additive deployment across major markets. In 2025, approximately 42% of large refineries integrated digital dosing technologies that enable real‑time adjustment of additive concentrations based on fuel quality metrics, improving consistency and performance while reducing waste. This trend supports tighter quality control and enhances additive effectiveness across variable fuel streams.

Bio‑Derived & Eco‑Optimized Chemistries: There is a measurable increase in bio‑based additive adoption, with around 35% of all new additives developed in 2025 incorporating bio‑derived components that reduce environmental impact without compromising performance. Fuel blenders and OEMs are increasingly sourcing eco‑optimized additives to support sustainability commitments and meet tightening emissions regulations in key regions.

Sector‑Specific Deployment Patterns: Premium additives are seeing differentiated adoption rates across end‑use sectors, with over 48% deployment in light‑duty automotive fuels, 32% in heavy‑duty diesel blends, and growing traction in marine and aviation turbine fuels. The marine sector, in particular, has adopted specialized lubricity and cold‑flow additives that enhance fuel stability in harsh operating conditions, driving sector‑specific innovation.

The Premium Fuel Additive Technology Market is segmented by type, application, and end-user to provide a comprehensive understanding of demand patterns and deployment strategies. By type, the market includes octane improvers, cetane enhancers, deposit control additives, lubricity additives, and corrosion inhibitors. Application areas span automotive fuels, diesel engines, marine fuels, aviation fuels, and industrial energy sectors. End-users range from OEMs and fuel refiners to fleet operators and industrial equipment providers. Premium fuel additives are increasingly deployed to optimize combustion, improve engine efficiency, and reduce emissions. Adoption is higher in regions with stringent environmental regulations, while growing industrialization drives demand for performance-enhancing fuels across multiple sectors. Consumer trends indicate rising preference for fuels that extend engine life and maintain efficiency under high-stress operational conditions. The segmentation framework highlights opportunities for targeted product innovation, regional deployment strategies, and end-user engagement to maximize operational and environmental benefits.

The market comprises octane improvers, cetane enhancers, deposit control additives, lubricity additives, and corrosion inhibitors. Deposit control additives currently lead adoption, accounting for approximately 38% of the market due to their ability to reduce engine deposit formation and maintain injector performance in high-stress conditions. Cetane enhancers are the fastest-growing segment, driven by increased diesel engine efficiency requirements, with accelerated uptake in heavy-duty and commercial vehicle fleets. Octane improvers contribute around 20%, lubricity additives about 15%, and corrosion inhibitors collectively account for 12% of the remaining segment share, serving niche or specialized applications.

Application areas include automotive fuels, diesel engines, marine fuels, aviation fuels, and industrial energy sectors. Automotive fuels dominate with a 40% share due to high volume consumption and the growing use of high-performance engines requiring additive stabilization. Diesel engine applications are the fastest-growing segment, driven by long-haul logistics and industrial machinery demands. Marine and aviation fuels account for a combined 28%, serving specialized operational requirements with higher performance thresholds. Consumer adoption trends indicate that in 2025, over 42% of fleet operators globally incorporated premium diesel additives for efficiency improvements, and 35% of automotive manufacturers adopted additive-enhanced fuels for emission compliance.

End-users include OEMs, fuel refiners, fleet operators, industrial machinery providers, and government institutions. OEMs are the leading segment, representing approximately 36% of adoption, due to requirements for fuel that supports engine warranties and performance specifications. Fleet operators represent the fastest-growing end-user group, fueled by efficiency mandates and cost optimization strategies. Fuel refiners and industrial machinery providers collectively account for 30% of adoption, serving specialized operational needs. Consumer and trend insights show that in 2025, over 38% of commercial fleets globally adopted premium diesel additives for performance consistency, and 40% of heavy machinery operators integrated advanced fuel additives to extend equipment longevity.

North America accounted for the largest market share at 35% in 2025; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.3% between 2026 and 2033.

North America leads with high adoption in automotive and industrial sectors, supported by advanced blending infrastructure and regulatory incentives for cleaner fuels. Europe holds a 25% share, driven by Germany, France, and the UK, with strong sustainability initiatives. Asia-Pacific commands 28% of the market, led by China, India, and Japan, fueled by rapid industrialization and expanding transport fleets. South America and the Middle East & Africa contribute 7% and 5%, respectively, with growth supported by energy sector expansions and infrastructure development.

North America holds 35% of the premium fuel additive market, with demand primarily driven by automotive, marine, and heavy-duty industrial sectors. Stricter emission standards and government incentives are encouraging refiners to adopt high-octane, deposit control, and lubricity additives. Digital blending and automated dosing systems are increasingly integrated into refineries, enhancing fuel consistency and performance monitoring. Local players, such as a leading U.S. additive manufacturer, have expanded their R&D in eco-optimized formulations, improving injector cleanliness by up to 18%. North American enterprises show higher adoption in industrial machinery, automotive fleets, and logistics, emphasizing operational efficiency and environmental compliance.

Europe accounts for 25% of the premium fuel additive market, with Germany, the UK, and France as leading contributors. Adoption is shaped by strict EU fuel quality standards and sustainability programs promoting low-sulfur and eco-friendly additives. Emerging technologies such as nano-additive formulations and AI-assisted blending are increasingly applied in refineries. European players have invested in multifunctional additives that improve engine efficiency and reduce particulate emissions. Regulatory pressure encourages widespread adoption in automotive and industrial sectors. Consumer behavior reflects strong demand for performance-enhanced and environmentally compliant fuels, particularly in urban transport and commercial fleets.

Asia-Pacific represents 28% of the premium fuel additive market, led by China, India, and Japan. Demand is fueled by growing automotive fleets, expanding heavy industries, and increased diesel consumption. Infrastructure modernization and new refinery capacities support high-volume additive blending. Technological innovation hubs in Japan and South Korea focus on bio-derived chemistries and multifunctional additives. Local players are developing specialized octane and cetane improvers to optimize regional fuel performance. Regional consumer behavior shows heightened interest in fuel additives that improve engine efficiency and longevity for both commercial fleets and personal vehicles, aligning with growing regulatory compliance requirements.

South America holds 7% of the premium fuel additive market, with Brazil and Argentina as key contributors. Growth is supported by expanding energy infrastructure, industrial fleets, and government incentives for cleaner fuel adoption. Local refiners are integrating multifunctional additives to enhance combustion and engine longevity in diverse operating conditions. Regional players focus on diesel lubricity and corrosion inhibitors for heavy machinery. Consumer behavior trends indicate rising adoption in commercial transport and industrial operations, driven by efficiency optimization and regulatory adherence.

The Middle East & Africa accounts for 5% of the premium fuel additive market, with UAE and South Africa as major contributors. Demand is driven by oil and gas operations, heavy industrial applications, and infrastructure development. Technological modernization includes automated blending systems and advanced performance testing. Local players have introduced high-performance deposit control and lubricity additives to improve operational reliability. Regional adoption reflects commercial fleet optimization and compliance with emerging fuel quality regulations, with growing interest in environmentally sustainable formulations.

United States – 35% Market Share: High production capacity, advanced additive blending infrastructure, and stringent emission regulations drive adoption.

China – 18% Market Share: Rapid industrialization, expanding transport fleets, and government policies supporting clean fuel technologies fuel market growth.

The Premium Fuel Additive Technology Market is characterized by a moderately consolidated competitive environment with a mix of global diversified chemical firms and specialized additive manufacturers. The market features 20+ active international competitors, with the top 5 companies collectively holding approximately 55–60% of overall market share through broad portfolios and extensive global distribution networks. Major participants are strategically positioned across regions including North America, Europe, and Asia-Pacific, leveraging advanced R&D, strategic partnerships, and capacity expansions to strengthen market presence. For example, Innospec Inc. maintains a leadership position with an ~18% market share, supported by proprietary additive brands and recent facility investments in Asia-Pacific to meet rising demand for high-performance fuel formulations. Afton Chemical, representing around 12% share, has expanded its distribution through collaborations with major refiners, enhancing supply reach and customer engagement.

Innovation trends, such as AI‑integrated fuel stabilizers, bio‑derived lubricity improvers, and multifunctional deposit control additives, are reshaping competition, with firms increasingly focusing on next‑generation products tailored to hybrid and advanced combustion engines. Strategic initiatives include production facility expansions (e.g., new blending plants in Asia), joint ventures to co‑develop advanced chemistries, and product approvals in high‑performance fuel specifications. Mid‑tier players continue gaining traction in regional markets by offering niche or cost‑effective solutions, while global leaders pursue digital blending and automated dosing technologies to improve additive consistency and performance.

BASF SE

The Lubrizol Corporation

Infineum International Limited

Evonik Industries AG

Clariant AG

LANXESS AG

Dorf Ketal Chemicals LLC

Eastman Chemical Company

Solvay S.A.

Baker Hughes

Croda International Plc

Technological innovation is a defining factor in the evolution of the Premium Fuel Additive Technology Market, with current and emerging technologies reshaping fuel performance, emissions outcomes, and operational efficiencies. Multifunctional additive formulations that combine deposit control, combustion enhancement, corrosion inhibition, and lubricity within single packages are increasingly prevalent. These advanced blends deliver measurable improvements such as enhanced injector cleanliness and reduced engine deposit formation in direct‑injection engines, addressing the needs of modern automotive platforms. Digital blending systems and real‑time dosing technology are becoming standard in large refinery operations, enabling dynamic adjustment of additive concentrations based on fuel quality parameters, improving consistency and reducing waste.

Bio‑based and eco‑optimized chemistries have gained traction as manufacturers apply renewable feedstocks and biodegradable surfactants to reduce environmental impact while maintaining performance. Innovations include ethanol‑compatible antioxidant packages that improve fuel stability in blended fuels and nano‑additive dispersions that support storage life and oxidative resistance, extending treated fuel shelf life by up to 24 months. AI‑assisted formulation tools are enabling predictive performance modeling, optimizing additive combinations for specific engine types and regional fuel specifications. Hybrid and alternative fuel engines have sparked development of tailored additive solutions that address cold‑flow issues, phase separation in biofuels, and micro‑emission control, broadening the technology roadmap.

Emerging trends also focus on smart dosing cartridges with inline sensors that maintain accuracy within ±2%, integrating with digital fleet management systems for condition‑based additive deployment. These technologies support improved fuel economy outcomes and optimized performance in heavy‑duty applications and high‑performance consumer vehicles alike. The ongoing shift toward sustainable and multifunctional solutions ensures that technology investments will continue to drive competitive differentiation and operational gains across the fuel additive landscape.

• In 2025, Afton Chemical launched its HiTEC® 65522 additive series, approved for TOP TIER+™ gasoline to enhance fuel system performance and combustion in modern GDI engines, improving intake valve deposit control and aligning with new engine performance standards. Source: www.aftonchemical.com

• In March 2025, Innospec expanded its production and supply focus for premium fuel additives, underscoring enhancements in manufacturing and technology deployment to improve fuel efficiency, engine performance, and lower emissions across fuels for road and industrial applications (fuel specialties business update from company filings). Source: www.investors.innospec.com

• In September 2025, Chevron Oronite exhibited at the Asian Lubricant Exhibition 2025, showcasing its latest OLOA® product offerings including advanced gasoline and marine additive solutions (OLOA® 55620, OLOA® 59361, and OLOA® 49844) and presenting insights on fuel additive trends and applications at industry sessions. Source: www.oronite.com

• In 2025, Infineum India announced the expansion of a state‑of‑the‑art blending facility, which will begin trial operations in mid‑2025 and full commercial fuel additive blending by Q3 2025 to support automotive and industrial demand with localized production of sulfonate and salicylate additive packages. Source: www.infineum.com

The Premium Fuel Additive Technology Market Report offers a comprehensive examination of product types, including deposit control agents, octane and cetane improvers, lubricity enhancers, corrosion inhibitors, and multifunctional additive packages, reflecting formulation diversity and performance optimization trends. It covers critical applications across gasoline, diesel, marine, aviation, and industrial energy fuels, detailing how additive technologies address specific engine performance, emissions compliance, and operational longevity requirements. The report assesses regional markets such as North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, highlighting consumption patterns, regulatory influences, infrastructure dynamics, and technological adoption variations.

The geographical analysis explores regional infrastructure trends, blending capacity distributions, and local refinery investments driving market development. It also profiles emerging market segments such as bio‑based and sustainable additive chemistries, smart dosing systems, and AI‑augmented blending platforms that enhance fuel efficiency. End‑user perspectives are addressed, with insights into OEM preferences, fleet operator requirements, and aftermarket adoption behaviors. The scope extends to competitive landscape analysis, strategic initiatives by leading players, and niche innovation vectors such as hybrid engine additive solutions and biodiesel compatibility enhancements. Decision‑makers gain clarity on segmentation structures, technological deployment patterns, regional market differentiators, and future innovation pathways, making the report a strategic tool for investment planning, product development, and market entry strategies in the premium additive domain.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,029.0 Million |

| Market Revenue (2033) | USD 1,627.7 Million |

| CAGR (2026–2033) | 5.9% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast, Market Trends, Growth Drivers & Restraints, Technology Insights, Segmentation Analysis, Regional Insights, Competitive Landscape, Regulatory & ESG Overview, Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Innospec Inc.; Chevron Oronite Company LLC; Afton Chemical Corporation; BASF SE; The Lubrizol Corporation; Infineum International Limited; Evonik Industries AG; Clariant AG; LANXESS AG; Dorf Ketal Chemicals LLC; Eastman Chemical Company; Solvay S.A.; Baker Hughes; Croda International Plc |

| Customization & Pricing | Available on Request (10% Customization Free) |