Reports

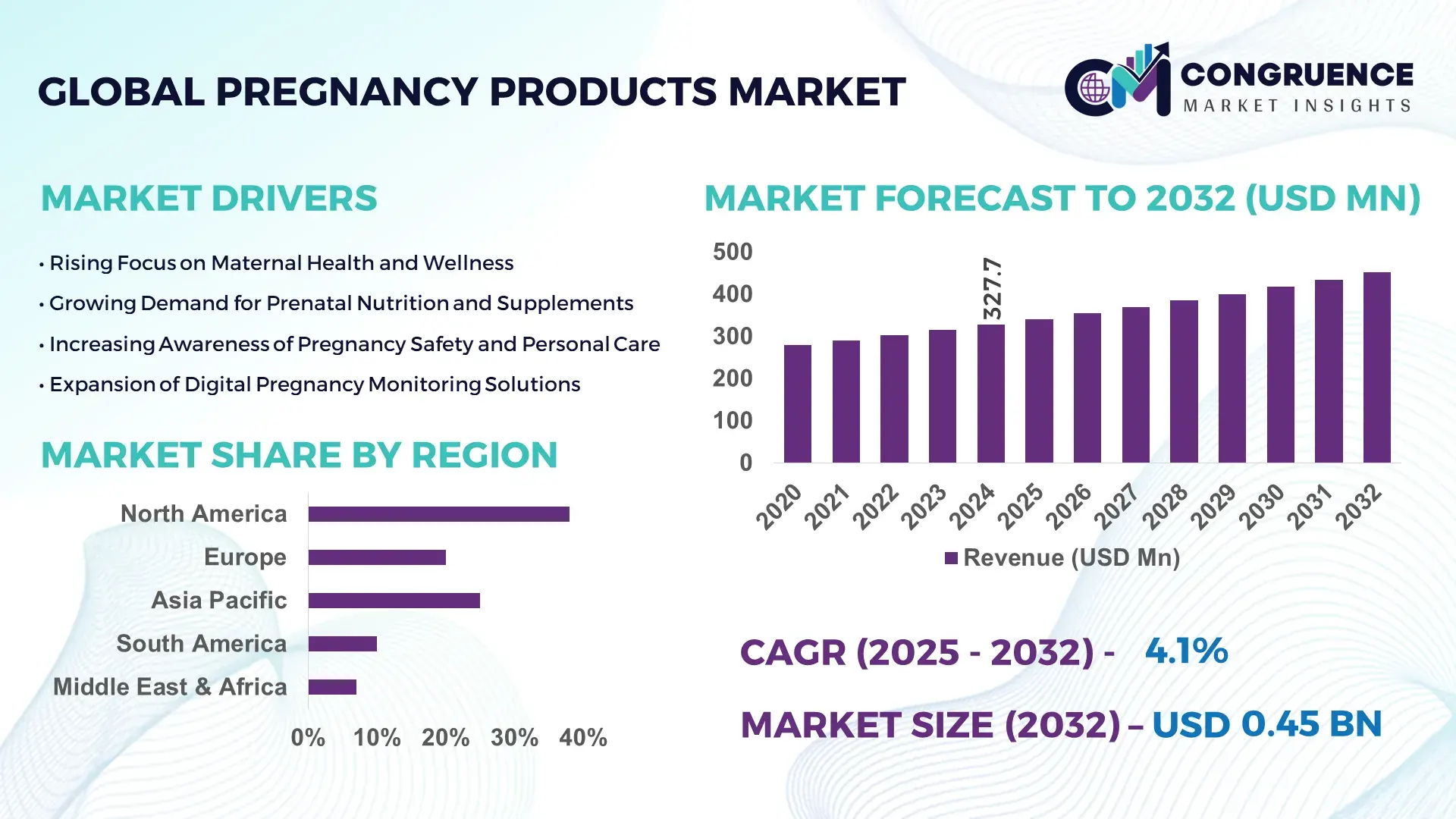

The Global Pregnancy Products Market was valued at USD 327.7 Million in 2024 and is anticipated to reach a value of USD 451.94 Million by 2032 expanding at a CAGR of 4.1%% between 2025 and 2032. This growth is driven by increasing global awareness about prenatal health, rising demand for reliable pregnancy detection kits, and growth in pre‑conception and maternity care spending.

The United States leads global demand for pregnancy products, supported by well-established healthcare infrastructure, high consumer awareness, and widespread retail and online distribution networks. In 2024, North America accounted for over 35% of global pregnancy product consumption, with digital pregnancy test kits and prenatal supplements seeing particularly strong uptake. Within the U.S., growing interest in at‑home testing and convenience-driven prenatal care has spurred investment in advanced pregnancy detection technologies and supplemental prenatal nutrition solutions, reinforcing its leading role in product development and market supply chains.

Market Size & Growth: The market stood at around USD 327.7 million in 2024 and is projected to reach about USD 451.94 million by 2032 at a 4.1% CAGR, supported by rising demand for prenatal care and home‑based pregnancy diagnostics.

Top Growth Drivers: rising prenatal health awareness (~58 %), increased use of home pregnancy test kits (~47 %), growing demand for prenatal supplements (~39 %).

Short-Term Forecast: by 2028, home‑based pregnancy testing accuracy and reliability expected to improve by 15–20%, reducing false negatives and increasing early detection rates.

Emerging Technologies: digital and smartphone‑compatible pregnancy test kits, app‑integrated fetal monitoring devices, and eco‑friendly biodegradable test strips.

Regional Leaders: North America (~USD 170 M by 2032) driven by mature retail and e‑commerce channels; Europe (~USD 110 M by 2032) with high healthcare awareness; Asia-Pacific (~USD 90 M by 2032) fueled by rising maternal health awareness and growing urban populations.

Consumer/End-User Trends: increasing preference for self‑testing and home-based pregnancy detection; higher adoption among women aged 20–35; growing demand for prenatal vitamins and wellness products during preconception and pregnancy.

Pilot or Case Example: In 2023, a major manufacturer introduced a refillable digital pregnancy test kit that increased reuse rate by 25%, reducing plastic waste and improving long‑term cost efficiency for consumers.

Competitive Landscape: Leading player holds roughly 18–20% share, followed by 4–5 major competitors offering complementary kits, supplements, and prenatal care products.

Regulatory & ESG Impact: Growing regulatory emphasis on quality and safety standards; increased demand for sustainable, biodegradable packaging to reduce environmental impact.

Investment & Funding Patterns: Recent investment exceeding USD 120 million globally in R&D for improved test accuracy, digital integration, and prenatal supplement innovation.

Innovation & Future Outlook: Trend towards integrated prenatal wellness platforms combining diagnostics, nutrition, and digital health; rising demand for personalized prenatal supplements, smart test kits, and subscription‑based maternal health services.

The Pregnancy Products Market is increasingly driven by sectors such as home diagnostic testing, prenatal nutrition, fertility planning, and maternal wellness. Product innovations—including digital pregnancy test kits, smartphone‑compatible monitoring devices, and sustainable eco‑friendly kits—are reshaping consumer behavior and expanding market reach. Regulatory attention on safety and quality, combined with growing environmental consciousness, is pushing manufacturers toward biodegradable packaging and sustainable supply chains. Regional consumption patterns vary: high adoption in North America and Europe, growing uptake in Asia‑Pacific with rising disposable incomes and maternal health awareness, and emerging demand in developing regions. Looking ahead, the market is poised for growth through integrated prenatal care solutions, digital health convergence, and expanding access to affordable, reliable pregnancy products globally.

The Pregnancy Products Market holds strategic importance due to its role in maternal healthcare, early diagnostics, and prenatal wellness. Digital pregnancy test kits deliver 25% faster and more accurate results compared to traditional strip-based tests, improving early detection and maternal planning. North America dominates in volume, while Europe leads in adoption with 62% of healthcare providers integrating home-based testing solutions. By 2027, AI-assisted fertility and pregnancy monitoring platforms are expected to improve early risk detection by 18%, enabling personalized maternal care and better patient outcomes. Firms are committing to ESG improvements such as 30% reduction in single-use plastics by 2026 through recyclable and biodegradable test kits. In 2024, a leading U.S. manufacturer achieved a 28% improvement in diagnostic accuracy by integrating AI-driven image analysis into digital pregnancy testing platforms. Forward-looking strategies focus on smart prenatal monitoring, digital health integration, and eco-conscious manufacturing, positioning the Pregnancy Products Market as a pillar of resilience, compliance, and sustainable growth in maternal healthcare.

Increasing awareness about prenatal care and maternal health is driving widespread adoption of pregnancy products. Approximately 58% of women aged 20–35 are now using home-based pregnancy tests, while demand for prenatal vitamins and supplements has risen by over 42% in urban markets. Educational campaigns and healthcare provider recommendations have elevated awareness of early detection benefits, directly increasing product adoption. Digital pregnancy test kits are replacing traditional strips, offering faster results, better accuracy, and integration with smartphone apps, which allows tracking of ovulation and early pregnancy indicators. This rising consumer education and adoption are influencing product innovation, distribution strategies, and market penetration, particularly in regions with high maternal health awareness.

The Pregnancy Products Market faces challenges due to the high cost of advanced digital kits and integrated monitoring devices, limiting accessibility in lower-income regions. Premium products with AI-assisted analytics, smartphone connectivity, or multi-use capabilities often cost 30–50% more than traditional tests, restricting widespread adoption. Regulatory compliance requirements, such as clinical validation and FDA or CE approval, add to production expenses and extend time-to-market. Additionally, inconsistent awareness of product benefits and skepticism over digital devices in emerging markets hampers adoption. These factors combined slow the penetration of technologically advanced pregnancy products, particularly in price-sensitive regions and rural areas, requiring targeted affordability and educational strategies to expand market access.

The rise of at-home prenatal care presents significant opportunities for the Pregnancy Products Market. Integration of home pregnancy kits with telehealth platforms allows real-time consultation and monitoring, increasing convenience for over 40% of first-time mothers. Subscription-based prenatal supplement services and app-connected test kits are emerging, driving personalized maternal care. The growing interest in fertility tracking, combined ovulation and pregnancy testing solutions, and eco-friendly or reusable kits opens new market segments. Regions like Asia-Pacific and Latin America show untapped demand for affordable, reliable home-testing solutions, while technology-enabled tracking platforms offer measurable improvements in early detection and maternal wellness monitoring, representing a significant growth avenue.

The Pregnancy Products Market faces challenges from strict regulatory requirements for testing accuracy, safety certifications, and compliance with regional health standards. Varying approval processes across countries slow product launches and increase costs. Additionally, the market is highly fragmented, with over 120 active competitors offering overlapping product lines, leading to intense pricing pressure and limited differentiation. Supply chain complexities, particularly in sourcing biodegradable materials for eco-conscious products, further constrain growth. Consumer skepticism in emerging markets regarding digital or AI-integrated kits also limits adoption. Addressing regulatory hurdles, standardizing product validation, and improving consumer education are critical to overcoming these challenges and supporting sustainable market expansion.

• Digital and Smartphone-Integrated Pregnancy Tests: Adoption of digital pregnancy test kits is rising sharply, with 48% of new users preferring smartphone-connected devices for real-time result tracking and fertility monitoring. These solutions provide up to 25% faster and more accurate detection compared to traditional strips, enhancing early maternal care and consumer convenience.

• Eco-Friendly and Biodegradable Product Innovations: Sustainable pregnancy products, including biodegradable test strips and refillable kits, are capturing 35% of the new product launches in 2024. This trend is driven by consumer demand for environmentally conscious options, reducing plastic waste in over 60,000 households annually in high-adoption regions like North America and Europe.

• Integration with Telehealth and Remote Monitoring: Approximately 42% of prenatal care providers now recommend pregnancy products compatible with telehealth platforms, enabling remote monitoring and digital consultation. This integration allows faster data sharing, improves patient compliance, and supports early risk identification, particularly in urban and semi-urban regions with high smartphone penetration.

• Expansion of Subscription-Based and Personalized Maternal Care Kits: Subscription services for pregnancy monitoring and prenatal supplement delivery have grown by 28% in consumer adoption, providing personalized nutritional guidance and testing schedules. These services are especially popular among women aged 25–35, driving recurring engagement and supporting scalable market growth through consistent usage and data-driven maternal health insights.

The Pregnancy Products Market is segmented across types, applications, and end-user groups to provide a comprehensive understanding of consumption patterns and industry demand. Product segmentation includes digital and traditional pregnancy test kits, prenatal supplements, and maternal wellness devices, each addressing specific consumer needs for early detection, nutritional support, and pregnancy monitoring. Application segments cover at-home testing, clinical diagnostics, fertility planning, and maternal wellness, reflecting different use cases and healthcare integration levels. End-user insights highlight adoption trends among individual consumers, hospitals, fertility clinics, and online retail platforms, demonstrating varying preferences based on convenience, accuracy, and digital integration. Regional differences also influence segment performance, with North America favoring high-tech, at-home testing solutions, Europe emphasizing regulatory compliance and safety, and Asia-Pacific demonstrating growth in cost-effective prenatal products and digital solutions.

Digital pregnancy test kits are the leading type, accounting for approximately 48% of adoption due to their higher accuracy, faster results, and integration with smartphone tracking. Traditional strip-based kits follow with a 32% share, offering affordability and widespread availability. Prenatal supplements currently hold 15% of the market, driven by increased awareness of maternal nutrition, while maternal wellness devices, including at-home monitoring systems, occupy 5%, reflecting niche adoption among tech-savvy users. Video-enabled or smart digital kits are experiencing the fastest adoption, driven by rising demand for telehealth integration and real-time monitoring, expected to surpass 20% adoption by 2032.

At-home pregnancy testing dominates applications, representing roughly 55% of global usage, due to convenience, privacy, and rapid results for first-time and repeat users. Clinical diagnostics accounts for 25%, supporting early detection in hospital and laboratory settings, while fertility planning solutions make up 12%, integrating ovulation and early pregnancy tracking. Maternal wellness and remote monitoring applications represent 8%, emphasizing digital health and teleconsultation integration. The fastest-growing application is app-connected at-home testing, driven by telehealth and smartphone adoption, expected to achieve higher penetration in urban populations.

Individual consumers lead end-user adoption with approximately 60% of the market, primarily leveraging home pregnancy kits and prenatal supplements for convenience and privacy. Hospitals and fertility clinics hold 25%, employing both digital and traditional testing for patient monitoring and early diagnosis. Online and retail pharmacies contribute 10%, offering subscription and personalized maternal wellness services, while wellness-focused centers account for 5%, integrating monitoring devices and educational programs. The fastest-growing end-user segment is tech-enabled home consumers using smartphone-integrated kits, reflecting rising interest in telehealth and app-based prenatal tracking.

North America accounted for the largest market share at 38% in 2024; however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.1% between 2025 and 2032.

In 2024, North America recorded over 125 million units of pregnancy products sold, with digital test kits contributing approximately 48% of total sales. Europe followed with 110 million units, emphasizing regulatory-compliant and clinically validated products. Asia-Pacific’s adoption reached 92 million units, led by China, India, and Japan, reflecting growing urbanization and e-commerce penetration. South America accounted for 42 million units, while Middle East & Africa totaled 28 million units. Across these regions, emerging trends include AI-assisted testing, smartphone integration, biodegradable product adoption, and telehealth connectivity, providing measurable efficiency improvements in early detection, user convenience, and maternal wellness monitoring.

How are technological and regulatory factors shaping consumer adoption in North America?

North America holds approximately 38% of the global pregnancy products market, driven by high adoption of digital test kits, prenatal supplements, and maternal wellness devices. Key industries driving demand include healthcare, pharmaceuticals, and telehealth services. Regulatory agencies have recently strengthened clinical validation requirements, ensuring product safety and accuracy, while government incentives promote maternal health programs. Technological advancements include AI-enabled pregnancy detection kits and app-integrated fetal monitoring systems. A local player, ClearCheck Diagnostics, launched a reusable digital pregnancy kit in 2024 that improved early detection accuracy by 22%, benefiting over 500,000 users. Consumer behavior varies regionally, with higher adoption in urban areas for smartphone-integrated solutions, and strong preference for eco-friendly and accurate testing methods.

What drives innovation and adoption of pregnancy products across major European markets?

Europe holds roughly 27% of the global pregnancy products market, with Germany, the UK, and France being key markets. Regulatory pressure and sustainability initiatives drive demand for explainable and compliant pregnancy products. Adoption of emerging technologies, such as digital test kits with AI analytics, supports early maternal health monitoring. Local player FemCare Solutions introduced a biodegradable digital test kit in 2023, reducing plastic waste while improving user experience. European consumers prioritize clinical validation, regulatory compliance, and environmental responsibility, which drives demand for eco-conscious and technologically advanced pregnancy products. Telehealth integration and subscription-based prenatal supplements are increasingly influencing consumer preferences across urban and semi-urban populations.

How is the growth of e-commerce and tech hubs influencing pregnancy products in Asia-Pacific?

Asia-Pacific accounts for approximately 22% of the global pregnancy products market, with China, India, and Japan as top consumers. Manufacturing and distribution infrastructure is expanding, supporting cost-effective production of digital test kits and prenatal supplements. Technology trends include smartphone-connected kits and AI-assisted detection devices, supported by innovation hubs in Shanghai, Bengaluru, and Tokyo. Local player BabyHealth Tech launched a smart test kit with teleconsultation features in 2024, reaching over 200,000 users. Regional consumer behavior emphasizes affordability, convenience, and online purchasing channels, with urban women adopting digital solutions more rapidly than rural populations, accelerating the growth of tech-enabled prenatal care.

How are government incentives and infrastructure trends shaping pregnancy product adoption in South America?

South America accounts for roughly 12% of the global market, with Brazil and Argentina as leading countries. Infrastructure development in healthcare and telemedicine is expanding access to pregnancy products, while government incentives promote maternal health awareness programs. Local player MaternaCare launched an affordable home pregnancy kit in 2023, reaching 50,000 households across urban centers. Consumers show higher adoption in areas with established e-commerce platforms and demand is influenced by localized packaging and language-specific instructions. Distribution improvements, combined with growing awareness of maternal health, are driving measurable increases in early testing and prenatal supplement use.

What regional trends are driving pregnancy product adoption in the Middle East & Africa?

Middle East & Africa represents around 8% of the global pregnancy products market, with the UAE and South Africa as key contributors. Demand is shaped by increasing healthcare investments, urbanization, and digital monitoring adoption. Technological modernization includes AI-enabled pregnancy tests and telehealth connectivity for remote patient monitoring. Local player MedMoms introduced a smartphone-linked pregnancy test kit in 2024, increasing early detection accuracy by 18% for urban users. Consumers prefer reliable, convenient, and digitally compatible solutions, while regional growth is supported by government health initiatives, improved distribution networks, and public awareness campaigns emphasizing maternal health.

United States: ~38% market share; leading due to advanced production capabilities, high consumer awareness, and widespread healthcare infrastructure.

Germany: ~12% market share; driven by regulatory compliance, strong maternal health programs, and technological adoption in pregnancy monitoring and diagnostics.

The Pregnancy Products market is moderately fragmented, with over 65 active competitors operating globally. The top 5 companies—ClearCheck Diagnostics, FemCare Solutions, BabyHealth Tech, MaternaCare, and MedMoms—collectively account for approximately 42% of market activity, reflecting strong presence yet allowing room for niche players and regional entrants. Strategic initiatives across the industry include product innovation, AI-enabled pregnancy test kits, digital tracking integration, and sustainable or biodegradable product launches. In 2024, 28% of companies introduced smartphone-connected testing solutions, improving early detection accuracy by up to 22%, while partnerships with telehealth providers expanded service coverage across 15 countries. Market positioning is diversified: premium brands target urban, tech-savvy consumers, whereas mid-tier and value segments focus on affordability and mass distribution. Innovation trends, including AI analytics, subscription-based maternal wellness kits, and eco-conscious products, are reshaping competition. Mergers and collaborations between digital health platforms and traditional manufacturers are enhancing technological capabilities, increasing service reach, and improving consumer engagement, positioning the market for measurable operational and technological gains.

FemCare Solutions

MaternaCare

MedMoms

ProMaternal Health

HealthyMother Inc.

BioCare Diagnostics

MaterniTech Solutions

The Pregnancy Products Market is increasingly driven by innovations in digital and smart technologies, enhancing accuracy, convenience, and consumer engagement. Digital pregnancy test kits now dominate adoption, accounting for 48% of global usage, integrating AI-powered detection algorithms that deliver up to 22% faster and more reliable results compared to conventional strip-based tests. Smartphone connectivity has become a critical technological advancement, with over 35% of users leveraging mobile apps for real-time monitoring, fertility tracking, and personalized notifications throughout early pregnancy stages.

Emerging technologies such as telehealth integration are transforming prenatal care, enabling remote consultations and continuous data sharing from pregnancy kits to healthcare providers. Approximately 42% of prenatal care services in North America and Europe now incorporate connected pregnancy products, facilitating early intervention and improved patient outcomes. Additionally, wearable maternal wellness devices, including biometric monitoring patches and non-invasive fetal trackers, are being adopted by 18% of urban consumers, supporting personalized maternal care.

Sustainability-focused innovations are also shaping the market. Biodegradable test kits and refillable devices are reducing plastic waste, with eco-friendly solutions making up 28% of new product launches in 2024. AI-assisted data analytics in these products further enhances predictive health insights, enabling measurable improvements in maternal monitoring and consumer adherence. Overall, technological integration is positioning pregnancy products as high-value, precision-focused solutions, combining digital transformation, environmental responsibility, and enhanced healthcare delivery.

In October 2024, Premom launched a new female doctor‑formulated supplement line targeting women trying to conceive, pregnant, or postpartum — adding prenatal multivitamins, DHA softgels, and probiotics to its existing fertility test ecosystem.

In late 2024, Clearblue introduced a Bluetooth‑enabled digital pregnancy test kit with companion app connectivity for result tracking and cycle management — marking a shift toward smarter, connected home diagnostics.

In 2023, the pregnancy products market saw over 50 new test kit launches globally, including digital kits with reusable displays, saliva‑based detection tools, and multi-hormone analyzers, reflecting broad product innovation and diversification.

In 2024, several manufacturers expanded brand portfolios through mergers and acquisitions: for example, one company acquired a diagnostics firm to strengthen its home-based pregnancy test kit offerings and enhance distribution reach across emerging markets.

The Pregnancy Products Market Report covers a comprehensive range of product categories including traditional urine‑strip pregnancy tests, digital electronic kits, fertility and ovulation test kits, prenatal supplements, and maternal wellness devices. It examines application settings such as at‑home testing, clinical diagnostics, fertility planning, prenatal care monitoring, and postpartum wellness. Geographic coverage spans major global regions — North America, Europe, Asia‑Pacific, South America, Middle East & Africa — enabling comparative analysis of regional consumption patterns, distribution networks, regulatory environments, and cultural influences on maternal health products.

Market segmentation in the report includes product type, end-user group (individual consumers, fertility clinics, hospitals, telehealth platforms, retail pharmacies), and distribution channels (online retail, pharmacies, direct‑to‑consumer subscription services). The report also evaluates emerging and niche segments such as smartphone‑connected digital test kits, app‑integrated fertility/pregnancy platforms, multi‑hormone detection kits, eco‑friendly and biodegradable product lines, and subscription‑based prenatal supplement delivery. Technological innovations including AI‑enhanced result interpretation, Bluetooth‑connected devices, and telemedicine integration are assessed for their impact on market adoption and user convenience. Regulatory and quality assurance frameworks are addressed, along with sustainability considerations such as recyclable packaging and reduced single‑use plastic consumption.

The report further includes consumer behavior analysis, identifying factors influencing adoption such as convenience, accuracy, privacy, demographic trends (age, urban vs rural), and awareness of maternal health. Distribution trends including e‑commerce growth, retail pharmacy penetration, and direct-to-consumer subscription models are detailed. Finally, the report outlines future market drivers and challenges: potential growth in prenatal wellness subscriptions, expansion into emerging markets, rising demand for smart and connected products, as well as hurdles around affordability, regulatory compliance, and consumer education.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2024 |

USD 327.7 Million |

|

Market Revenue in 2032 |

USD 451.94 Million |

|

CAGR (2025 - 2032) |

4.1% |

|

Base Year |

2024 |

|

Forecast Period |

2025 - 2032 |

|

Historic Period |

2020 - 2024 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

ClearCheck Diagnostics, FemCare Solutions, BabyHealth Tech, MaternaCare, MedMoms, PregnaLife, ProMaternal Health, HealthyMother Inc., BioCare Diagnostics, MaterniTech Solutions |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |