Reports

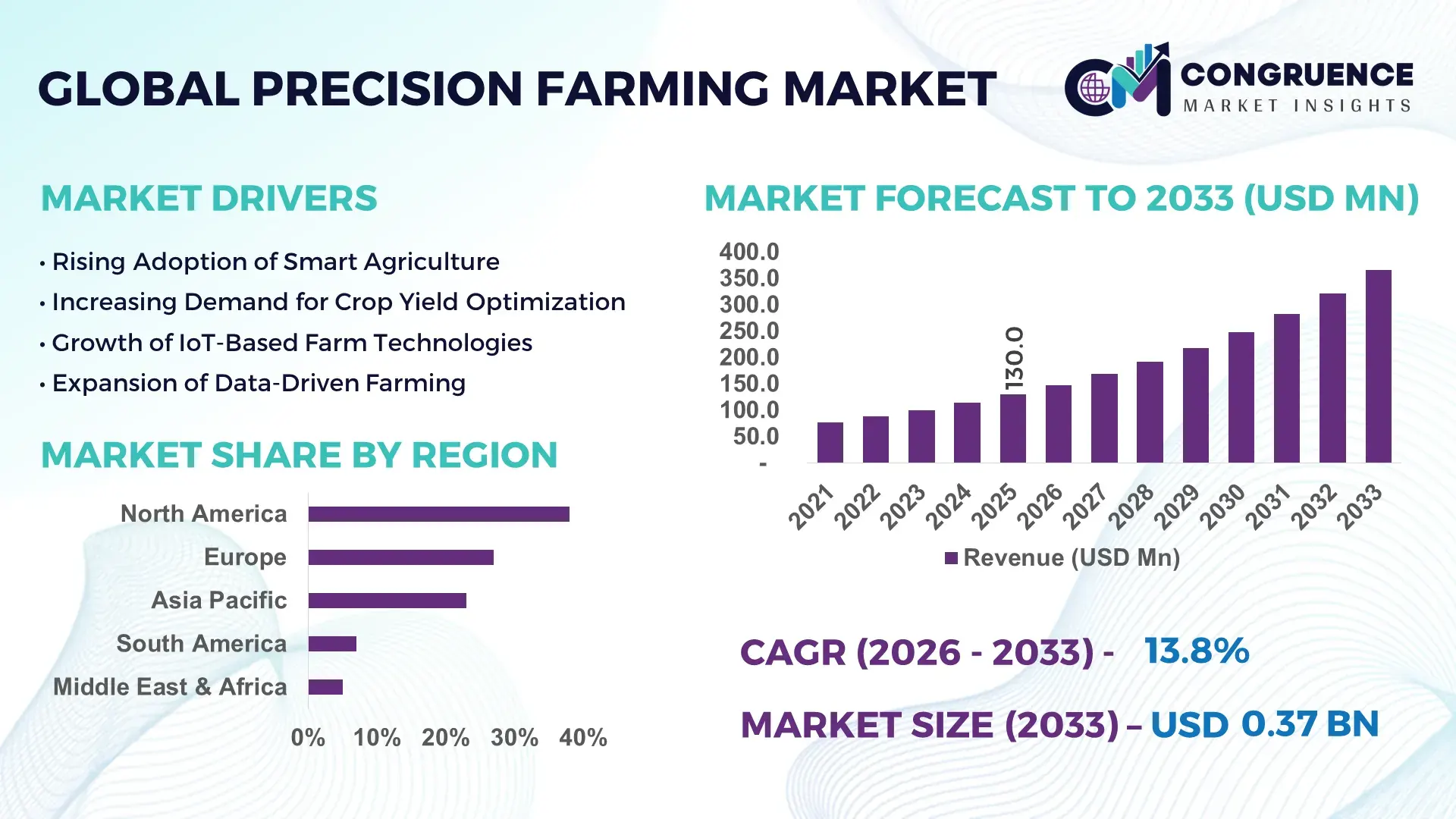

The Global Precision Farming Market was valued at USD 130.0 Million in 2025 and is anticipated to reach a value of USD 365.7 Million by 2033 expanding at a CAGR of 13.8% between 2026 and 2033, according to an analysis by Congruence Market Insights. The market expansion is largely driven by the growing adoption of data-driven agriculture technologies that optimize crop productivity, reduce input costs, and support sustainable farming practices.

The United Statesrepresents the most technologically advanced ecosystem in the precision farming industry. The country operates more than 370 million acres of farmland, with over 60% of large-scale farms already deploying GPS-guided tractors, satellite imaging, and IoT soil sensorsfor yield optimization. The U.S. Department of Agriculture reports that over 75% of corn and soybean farms utilize some form of precision agriculture technology, particularly variable-rate application systems and remote crop monitoring. Additionally, investments in agricultural technology exceeded USD 4.5 billion in venture funding across more than 500 ag-tech startups, accelerating the integration of AI-driven farm management systems and autonomous agricultural machinery.

Market Size & Growth:The market was valued at USD 130.0 Million in 2025 and is projected to reach USD 365.7 Million by 2033, expanding at 13.8% CAGR as farms increasingly adopt digital monitoring systems to improve crop yield efficiency and reduce fertilizer waste.

Top Growth Drivers:Precision agriculture adoption among large farms exceeds 65%, automated irrigation systems improve water efficiency by 30%, and AI-enabled crop analytics increase yield accuracy by 25%.

Short-Term Forecast:By 2028, precision analytics platforms are expected to improve farm operational efficiency by 22% while reducing fertilizer application costs by 18%.

Emerging Technologies:Key technologies include AI-driven crop monitoring, drone-based field analytics, and satellite-powered variable rate technology (VRT) integrated with farm management software.

Regional Leaders:North Americais projected to reach USD 145 Million by 2033 driven by large-scale digital farms; Europeis expected to exceed USD 105 Million with strong sustainability programs; Asia-Pacific may approach USD 82 Million due to rapid ag-tech adoption in China and India.

Consumer/End-User Trends:Large commercial farms increasingly adopt integrated farm management platforms, while mid-sized farms are rapidly adopting drone-based crop monitoring and soil health analytics.

Pilot or Case Example:In 2024, a precision irrigation pilot in California reduced water consumption by 27%while improving crop yield consistency by 14%through AI-based soil moisture monitoring.

Competitive Landscape:Deere & Companyleads the market with roughly 21% share, followed by Trimble Inc., AGCO Corporation, Raven Industries, and Topcon Positioning Systems.

Regulatory & ESG Impact:Governments are introducing smart farming subsidies and sustainability incentives, with several regions targeting 20–30% reductions in agricultural water usage by 2030.

Investment & Funding Patterns:Global ag-tech investment surpassed USD 7 billion in recent funding rounds, with venture capital focusing on AI farm analytics, robotics, and autonomous machinery.

Innovation & Future Outlook:Integration of AI decision platforms, satellite imaging, and autonomous tractorsis expected to transform farm operations, enabling fully data-driven crop management ecosystems.

Precision farming technologies are increasingly integrated across crop cultivation (about 45% of deployments), livestock monitoring (approximately 20%), and greenhouse farming (around 15%). Innovations such as AI-enabled crop health diagnostics and autonomous spraying drones are reshaping agricultural productivity. Environmental policies promoting reduced pesticide usage and optimized irrigationare accelerating adoption across Europe and North America, while Asia-Pacific markets are expanding rapidly due to digital agriculture initiatives and increasing mechanization.

The Precision Farming Market has become a cornerstone of modern agricultural transformation, enabling data-driven decision-making across large and medium-scale farming operations. Precision agriculture technologies—including satellite monitoring, IoT sensors, autonomous tractors, and AI-driven crop analytics—are improving agricultural productivity while reducing environmental impact. Studies indicate that AI-powered crop monitoring systems can improve yield prediction accuracy by nearly 35% compared to traditional field scouting methods, significantly enhancing operational efficiency for large agricultural enterprises.

One of the major strategic advantages of precision farming lies in its ability to optimize input usage. Variable rate technology (VRT)delivers 20–25% improvement in fertilizer efficiency compared to conventional uniform application methods, reducing both costs and environmental footprint. Similarly, smart irrigation systems are capable of decreasing water consumption by up to 30%, which is critical in regions facing increasing water scarcity.

Regionally, North America dominates in volume due to large mechanized farms, while Europe leads in adoption intensity, with nearly 58% of agricultural enterprises using digital farm management systemssupported by strong sustainability policies and environmental compliance regulations. Governments across several regions are integrating digital agriculture into national food security programs, further accelerating adoption.

Short-term technological projections are equally promising. By 2027, AI-based predictive farming tools are expected to reduce crop disease losses by nearly 28%through early detection using satellite imagery and machine learning algorithms. These solutions enable farmers to respond proactively to pests, nutrient deficiencies, and weather anomalies.

Environmental compliance and ESG commitments are also shaping the market trajectory. Agricultural firms are increasingly committing to sustainability goals such as 25% reductions in chemical pesticide use by 2030, supported by sensor-based crop monitoring and precision spraying technologies.

A practical example illustrates the potential impact of these technologies. In 2024, a large agricultural cooperative in the United States implemented AI-enabled soil monitoring and autonomous tractors across 50,000 acres, achieving 18% fertilizer reduction and 16% improvement in crop yield consistencywithin a single planting cycle.

Looking ahead, the Precision Farming Market will continue evolving as a strategic pillar for global food security, environmental sustainability, and operational efficiency. With growing investments in ag-tech innovation, digital agriculture infrastructure, and AI-enabled analytics platforms, precision farming will remain central to resilient, data-driven agricultural systems capable of meeting the food demands of a rapidly expanding global population.

The Precision Farming Market is experiencing rapid transformation as agriculture shifts from traditional manual practices toward technology-driven farm management systems. Increasing pressure on global food production—driven by population growth and climate variability—has accelerated the adoption of digital agriculture solutions capable of optimizing crop productivity and resource utilization. Precision farming technologies, including GPS-guided equipment, remote sensing, data analytics, and automated irrigation systems, are enabling farmers to monitor field conditions in real time and implement targeted interventions that improve operational efficiency.

The growing availability of satellite data and agricultural drones has significantly improved field monitoring accuracy, allowing farmers to detect crop stress and nutrient deficiencies earlier than conventional methods. At the same time, integration with cloud-based farm management platforms enables real-time data analysis, helping farmers make more informed planting and harvesting decisions. Governments and agricultural institutions are also promoting smart farming practices through subsidies and digital agriculture programs aimed at improving sustainability and reducing environmental impact.

In addition, the rapid expansion of agricultural technology startups has introduced innovative solutions such as AI-powered crop diagnostics and autonomous farm equipment. These technologies are reshaping farm productivity models by minimizing labor requirements and improving resource efficiency. As a result, precision farming is becoming a critical component of modern agricultural strategies focused on long-term sustainability and enhanced global food security.

The global demand for agricultural productivity is increasing as the world population is projected to exceed 9 billion by 2050, requiring nearly 60% more food production compared to current levels. Precision farming technologies provide farmers with advanced tools to monitor soil health, crop growth patterns, and environmental conditions, enabling optimized use of fertilizers, pesticides, and irrigation resources. Studies indicate that farms using GPS-guided machinery and automated planting systems can achieve yield improvements of up to 15–20%while simultaneously reducing operational costs. Another key factor driving adoption is the increasing availability of agricultural data analytics platforms. These platforms integrate information from drones, satellites, and IoT sensors to generate actionable insights for farmers. For instance, variable rate technology allows farmers to apply fertilizers only in areas that require additional nutrients, resulting in approximately 20% reduction in chemical usage. Additionally, automated irrigation systems supported by soil moisture sensors help conserve water resources by reducing irrigation waste by around 25–30%. Government support programs promoting digital agriculture are further strengthening market expansion. Several countries are introducing smart farming incentives, equipment subsidies, and agricultural modernization initiatives to encourage farmers to adopt precision technologies. As a result, large-scale farms and agricultural cooperatives are rapidly integrating advanced farm management platforms, positioning precision farming as a fundamental driver of agricultural productivity and sustainability worldwide.

Despite the operational benefits of precision farming technologies, high initial capital investment remains a major barrier for many farmers, particularly small and medium-scale agricultural enterprises. Advanced systems such as autonomous tractors, drone monitoring platforms, and satellite-based analytics require substantial upfront expenditures for equipment procurement, installation, and technical training. For example, GPS-guided agricultural machinery can cost 30–40% more than conventional farm equipment, making adoption financially challenging for farmers operating on limited budgets. In addition to hardware expenses, the implementation of precision agriculture solutions requires specialized software platforms and data integration systems. These digital tools often involve subscription-based service models for satellite imagery analysis, predictive analytics, and farm management software. The cumulative cost of these services can increase operational expenses, discouraging smaller farms from adopting advanced technologies. Another limitation involves technical knowledge and workforce readiness. Precision farming relies heavily on digital data interpretation, requiring farmers to develop new skills related to data analytics, software operation, and remote sensing technologies. In regions where agricultural education and digital infrastructure are limited, farmers may face difficulties in effectively utilizing these advanced systems. Connectivity challenges also pose a significant barrier in rural agricultural areas. Many farms are located in regions with limited internet coverage, restricting the real-time data transmission required for advanced monitoring systems. These infrastructure gaps slow the deployment of precision farming technologies and limit the scalability of digital agriculture solutions across developing markets.

The expansion of digital agriculture infrastructure is creating substantial opportunities for the Precision Farming Market, particularly in emerging economies where agricultural modernization initiatives are accelerating. Governments and agricultural organizations are investing in satellite monitoring networks, smart irrigation infrastructure, and farm data platforms designed to improve crop productivity and climate resilience. These initiatives are enabling farmers to access real-time environmental data that supports more efficient farming decisions. The integration of artificial intelligence and machine learning technologies is another key opportunity. AI-based predictive analytics systems can analyze large volumes of agricultural data to forecast crop diseases, weather impacts, and nutrient requirements. Early disease detection models, for example, can identify crop infections up to 10 days earlier than traditional field inspection methods, allowing farmers to take preventive action and minimize crop losses. Precision livestock monitoring is also emerging as an important application area. Smart sensors attached to livestock can track animal health, feeding patterns, and movement behavior, improving productivity and disease management. In addition, the growing adoption of autonomous agricultural machinery—including robotic harvesters and self-driving tractors—is expected to significantly enhance farm productivity while addressing labor shortages in the agricultural sector. As global food demand continues to increase and climate variability places additional pressure on agricultural systems, precision farming technologies offer a scalable solution capable of transforming agricultural production and improving global food security.

Data integration and interoperability represent one of the most significant challenges facing the Precision Farming Market. Modern precision agriculture relies on multiple digital technologies—including drones, satellite imagery, GPS equipment, IoT soil sensors, and farm management software platforms. However, these technologies are often developed by different vendors, resulting in compatibility issues that make it difficult for farmers to integrate and analyze data across systems. For example, agricultural drones generate high-resolution imagery data that must be processed using specialized analytics software. At the same time, soil sensors and GPS-enabled machinery generate separate datasets related to soil composition, nutrient levels, and field mapping. Without standardized data integration frameworks, farmers may struggle to combine these datasets into a unified operational strategy. Another challenge involves cybersecurity and data ownership concerns. As farms increasingly rely on digital data platforms, agricultural businesses must protect sensitive operational information from potential cyber threats. Concerns about data privacy and ownership rights can discourage farmers from sharing agricultural data with technology providers. Finally, the rapid pace of technological innovation creates uncertainty for farmers making long-term investment decisions. Many agricultural businesses hesitate to invest in expensive precision technologies due to concerns that current systems may quickly become obsolete. Addressing these interoperability and technology lifecycle challenges will be essential for enabling broader adoption of precision farming solutions worldwide.

Expansion of AI-Powered Crop Monitoring Platforms: Artificial intelligence is transforming crop monitoring systems by enabling automated analysis of satellite imagery and drone-captured field data. Studies indicate that AI-based crop monitoring platforms can analyze over 10,000 hectares of farmland within minutes, identifying nutrient deficiencies and pest infestations with up to 90% accuracy. In North America and Europe, nearly 45% of large agricultural enterprises have integrated AI-driven farm analytics systems, allowing real-time crop performance tracking and early intervention strategies.

Rapid Adoption of Agricultural Drones: Drone technology is becoming a central component of precision farming operations. Globally, more than 600,000 agricultural drones are estimated to be in operation, performing tasks such as aerial crop imaging, pesticide spraying, and yield estimation. Drone-based crop monitoring can reduce manual scouting labor by up to 70%while improving crop health analysis precision by approximately 25%. Adoption rates are particularly strong in Asia-Pacific, where drone-assisted pesticide spraying has increased by over 40% in recent years.

Increasing Integration of Autonomous Farm Machinery: Autonomous tractors, robotic harvesters, and GPS-guided planting systems are reshaping agricultural productivity. Autonomous machinery can operate continuously for 20–22 hours per day, improving field productivity by around 18% compared to conventional equipment. Additionally, automated planting systems can maintain row spacing accuracy above 95%, improving crop density optimization and yield consistency across large agricultural fields.

Growth in Precision Irrigation Systems: Smart irrigation technologies are becoming essential in regions facing water scarcity. Precision irrigation systems equipped with soil moisture sensors and weather analytics can reduce water consumption by 30–35%while maintaining optimal crop growth conditions. In several European agricultural regions, more than 50% of high-value crop farms have implemented sensor-based irrigation systems, improving water efficiency and reducing operational costs associated with traditional irrigation practices.

The Precision Farming Market is segmented based on technology type, application area, and end-user categories, each playing a distinct role in shaping the adoption of digital agriculture solutions. Technology-based segmentation primarily includes automation and control systems, sensing technologies, and data analytics platforms that enable farmers to monitor crop performance and optimize agricultural inputs. Among these, sensing technologies and satellite-enabled monitoring systems have gained strong adoption due to their ability to provide real-time environmental insights.

Application segmentation highlights how precision agriculture technologies are utilized across crop management, irrigation management, yield monitoring, and livestock monitoring systems. Crop management solutions represent the most widely adopted applications because they directly impact productivity and crop health monitoring. Meanwhile, irrigation management and soil analytics are gaining prominence in regions facing water scarcity and soil degradation challenges.

From an end-user perspective, large commercial farms represent the most active adopters of precision farming technologies due to their ability to invest in advanced equipment and digital infrastructure. However, medium-sized farms are increasingly adopting cloud-based farm management platforms and drone monitoring systems due to decreasing technology costs and improved accessibility. Overall, segmentation trends indicate that the adoption of precision farming technologies will continue expanding as digital agriculture solutions become more affordable and scalable.

Precision farming technologies can be categorized into automation and control systems, sensing and monitoring technologies, and data analytics platforms, each contributing to the efficiency and intelligence of modern agricultural operations. Automation and control systems currently represent the leading segment, accounting for approximately 40% of technology adoption, primarily due to the increasing use of GPS-guided tractors, automated irrigation equipment, and robotic planting systems. These technologies enable farmers to perform field operations with high accuracy while reducing labor requirements and operational variability. Sensing and monitoring technologiesform the second-largest segment, capturing nearly 35% of the adoption landscape. These technologies include soil sensors, satellite imagery systems, and drone-based monitoring tools capable of collecting real-time agricultural data. The integration of these systems allows farmers to monitor soil nutrient levels, moisture conditions, and crop health patterns, enabling targeted farming interventions that enhance productivity. The data analytics and farm management software segment is emerging as the fastest-growing technology category, projected to expand at approximately 16% CAGRdue to the increasing integration of artificial intelligence and predictive analytics in agriculture. These platforms combine data from multiple field sensors and remote sensing tools to generate actionable insights for farmers, helping them optimize planting schedules and resource allocation. Other specialized technologies—including precision irrigation controllers and livestock monitoring systems—collectively contribute nearly 25% of total adoption, serving niche agricultural applications that require specialized monitoring and automation solutions.

• In 2024, a large agricultural research program implemented satellite-enabled crop monitoring across more than 1.2 million acres of farmland, enabling farmers to identify crop nutrient deficiencies and optimize fertilizer usage with improved accuracy.

Precision farming technologies are applied across several agricultural operations including crop monitoring, yield mapping, irrigation management, soil monitoring, and livestock management. Crop monitoring and management represent the dominant application segment, accounting for nearly 45% of adoption across precision agriculture systems.Farmers rely on satellite imaging, drones, and soil sensors to track crop growth patterns, detect pest infestations, and evaluate nutrient deficiencies. These technologies enable targeted intervention strategies that improve crop productivity while reducing chemical inputs. Irrigation management systems represent the fastest-growing application segment, expanding at an estimated 15% CAGRas water scarcity and climate variability increase the demand for efficient water management solutions. Precision irrigation platforms use soil moisture sensors and weather analytics to deliver water only when required, reducing water consumption while maintaining optimal crop health. Other applications—including yield mapping, soil monitoring, and livestock tracking—collectively represent approximately 40% of the application landscape. Yield mapping technologies allow farmers to analyze productivity variations across fields, while livestock monitoring systems use wearable sensors to track animal health and feeding behavior. Consumer adoption trends further highlight the growing interest in precision agriculture solutions. Nearly 48% of commercial farms globally have adopted some form of crop monitoring technology, while more than 30% of medium-scale farms are experimenting with drone-based field analytics systems.

• In 2025, a large agricultural cooperative deployed drone-based crop monitoring systems across more than 80,000 hectares, enabling early pest detection and improving crop health monitoring efficiency by 22%.

The adoption of precision farming technologies varies significantly across different agricultural stakeholders including large commercial farms, medium-scale farms, agricultural cooperatives, and research institutions. Large commercial farms represent the leading end-user segment, accounting for approximately 50% of precision farming technology adoption. These operations typically manage extensive farmland areas and have the financial capacity to invest in advanced digital agriculture infrastructure such as autonomous tractors, satellite monitoring systems, and AI-based farm management platforms. Medium-scale farms are emerging as the fastest-growing end-user category, with adoption expected to expand at around 15% CAGR. The growth in this segment is largely driven by the increasing availability of affordable drone monitoring services and cloud-based farm analytics platforms. These solutions allow mid-sized farms to access precision agriculture capabilities without investing heavily in expensive equipment. Other end-users—including agricultural cooperatives and research organizations—collectively account for nearly 30% of adoption. Agricultural cooperatives play a crucial role in promoting digital farming practices by sharing equipment and data platforms among multiple farmers, while research institutions focus on developing innovative agricultural technologies. Consumer adoption trends demonstrate growing confidence in digital agriculture solutions. Approximately 42% of agricultural enterprises worldwide have integrated IoT-based soil monitoring sensors, while over 35% of farmers are experimenting with AI-driven crop analytics platformsto improve yield forecasting and resource management.

• In 2025, a national agricultural technology program equipped more than 25,000 farms with IoT soil sensors and smart irrigation systems, significantly improving water efficiency and crop productivity across multiple farming regions.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 15.6% between 2026 and 2033.

The regional distribution of the Precision Farming Market reflects differences in farm size, technology adoption levels, and government support for smart agriculture initiatives. North America leads the global market with more than 210 million hectares of farmland monitored using GPS-enabled systems and IoT-based soil sensors, supported by strong adoption among commercial farms. Europe follows with approximately 27% market share, driven by strict environmental policies and digital agriculture programs targeting 20–30% reductions in fertilizer and pesticide usage by 2030. The Asia-Pacific region represents roughly 23% of global adoption, with countries such as China and India rapidly deploying agricultural drones, satellite imaging, and automated irrigation systems across over 40 million hectares of farmland. South America contributes around 7% of global demand, primarily driven by Brazil and Argentina where large soybean and corn farms deploy precision seeding and yield mapping technologies. Meanwhile, the Middle East & Africa region accounts for nearly 5% of the market, with increasing adoption of smart irrigation technologies across water-scarce agricultural zones covering more than 12 million hectares.

North America represents the largest regional ecosystem in the Precision Farming Market, accounting for approximately 38% of global adoption. The region benefits from highly mechanized agriculture and large-scale farms, with the United States and Canada collectively operating more than 370 million acres of farmland. Advanced technologies such as satellite-guided tractors, automated irrigation systems, and drone-based crop analytics are widely integrated into farm operations. Government support programs aimed at sustainable agriculture and digital transformation further strengthen adoption. Major industries driving demand include corn, soybean, wheat, and specialty crop farming, where precision technologies help optimize fertilizer usage and crop monitoring. Technological advancements include AI-powered farm management platforms and autonomous agricultural machinery capable of operating for 20+ hours per day. A key example is Trimble Inc., which continues to expand its GPS-based agricultural guidance systems that improve field operation accuracy to within 2.5 centimeters. Regional consumer behavior reflects a strong shift toward technology-driven agriculture. More than 70% of large-scale farms in the United States utilize at least one precision agriculture technology, while nearly 50% of medium-sized farms are integrating drone monitoring or data analytics platforms.

Europe represents a technologically advanced market accounting for nearly 27% of global precision farming adoption. Countries such as Germany, France, the United Kingdom, and the Netherlandsare leading the deployment of digital agriculture platforms across both large and mid-sized farms. The region’s agricultural modernization strategy focuses heavily on sustainability, encouraging farmers to adopt technologies that reduce chemical inputs and environmental impact. Regulatory frameworks such as the European Green Deal and Farm-to-Fork strategyaim to reduce pesticide usage by 50% and fertilizer use by 20% by 2030, significantly increasing demand for variable-rate application systems and crop monitoring technologies. European farmers are also early adopters of autonomous agricultural machinery and AI-driven crop analytics platforms. Local players are actively innovating in this space. Topcon Positioning Systemshas expanded its precision agriculture solutions across European farms, enabling centimeter-level field guidance and automated crop mapping systems used in more than 25,000 agricultural machinesacross the region. Regional consumer behavior highlights strong regulatory influence. European agricultural enterprises prioritize technologies that support sustainable farming compliance, leading to increased adoption of soil health monitoring systems and precision spraying equipment.

Asia-Pacific ranks among the fastest expanding regions in the Precision Farming Market and currently accounts for roughly 23% of global adoption. Countries including China, India, Japan, and Australiaare rapidly deploying advanced agricultural technologies to improve food production efficiency and reduce labor dependency. The region collectively manages more than 500 million hectares of agricultural land, creating substantial demand for precision agriculture solutions. Infrastructure modernization programs are accelerating technology integration. China has deployed more than 200,000 agricultural drones for crop monitoring and pesticide spraying, while India is expanding drone-assisted agriculture programs covering over 1.5 million hectares of farmland. Japan and Australia are also investing in autonomous tractors and robotic harvesting technologies to address agricultural labor shortages. Regional innovation hubs are emerging in China and Japan where ag-tech startups are developing AI-driven crop analytics platforms capable of predicting crop diseases with 85–90% accuracy. A regional example includes Kubota Corporation, which has introduced autonomous tractor systems designed for rice and grain farming operations. Consumer behavior trends highlight strong mobile technology adoption. Many farmers rely on smartphone-based farm management applications, with nearly 40% of farmers in technologically advanced areas utilizing mobile crop monitoring platforms.

South America represents approximately 7% of the global Precision Farming Market, with adoption concentrated primarily in Brazil and Argentina, two of the world’s largest agricultural exporters. The region manages extensive soybean, corn, and sugarcane farms covering more than 160 million hectares, creating strong demand for yield monitoring systems, satellite imaging tools, and automated seeding technologies. Infrastructure expansion and trade-oriented agricultural policies have accelerated the adoption of modern farming technologies. Brazil alone operates over 35 million hectares of soybean cultivation, with precision seeding and GPS-guided tractors widely used to improve crop productivity and field efficiency. Government initiatives promoting agricultural innovation are also encouraging digital transformation in farming practices. Agricultural equipment manufacturers and technology providers are collaborating with local cooperatives to introduce precision irrigation and soil monitoring systems. A regional example includes AGCO Corporation, which has expanded precision planting technologies across Brazilian farms, enabling farmers to achieve row spacing accuracy above 95%. Consumer behavior in the region is closely tied to export-oriented agriculture, where farmers prioritize technologies that improve yield consistency and crop quality for global markets.

The Middle East & Africa region accounts for nearly 5% of global precision farming adoption, with increasing demand for technologies that support water-efficient agriculture. Countries such as United Arab Emirates, Saudi Arabia, Israel, and South Africaare investing in smart irrigation systems, sensor-based soil monitoring, and climate-controlled greenhouse technologies to enhance agricultural productivity. Agricultural modernization programs in the Middle East emphasize water conservation due to arid climate conditions. Precision irrigation technologies equipped with soil moisture sensors can reduce water usage by up to 35%, making them essential for sustainable farming operations in desert environments. Technological innovation hubs are emerging in Israel and the UAE, where ag-tech companies are developing AI-powered crop analytics and hydroponic farming systems designed for controlled-environment agriculture. A notable regional example includes Netafim, an Israeli company that pioneered drip irrigation systems used across over 110 countries, enabling farms to significantly improve water efficiency and crop yields. Regional consumer behavior shows a strong preference for controlled-environment agriculture technologies that maximize productivity in limited arable land conditions.

United States – 32% Market Share:supported by large mechanized farms, advanced agricultural technology infrastructure, and strong adoption of satellite-guided farm equipment.

Germany – 9% Market Share:driven by highly automated agricultural operations and strong regulatory emphasis on sustainable farming technologies.

The Precision Farming Market is characterized by a moderately fragmented competitive landscape, with a combination of global agricultural equipment manufacturers, satellite technology providers, and specialized ag-tech software companies competing for market share. The top five companies collectively account for approximately 42% of total global market presence, indicating a competitive environment where innovation and technological integration play a critical role in differentiation.

More than 120 technology providers and equipment manufacturersactively participate in the global precision agriculture ecosystem. These companies develop a broad range of solutions including GPS-guided tractors, AI-based crop analytics platforms, autonomous farm machinery, and drone-based monitoring systems. Large agricultural equipment manufacturers dominate hardware-based technologies, while software-focused ag-tech companies are driving innovation in farm management platforms and predictive analytics tools.

Strategic partnerships and acquisitions have become common as companies aim to integrate multiple digital agriculture technologies into unified platforms. For example, collaborations between agricultural equipment manufacturers and satellite data providers enable farmers to combine real-time field monitoring with automated machinery control systems. Product innovation also remains a key competitive factor, with companies launching new autonomous tractors, precision irrigation systems, and AI-powered crop health monitoring platforms.

Innovation trends indicate increasing convergence between IoT sensors, cloud-based analytics platforms, and autonomous machinery, enabling fully integrated digital agriculture ecosystems capable of optimizing farm productivity and sustainability. As competition intensifies, companies are investing heavily in research and development to introduce next-generation agricultural technologies designed to support large-scale precision farming operations.

Trimble Inc.

AGCO Corporation

Raven Industries

Topcon Positioning Systems

Kubota Corporation

CNH Industrial

AG Leader Technology

Climate LLC

PrecisionHawk

Taranis

Granular Inc.

DICKEY-john Corporation

Farmers Edge

Technological innovation forms the foundation of the Precision Farming Market, enabling farmers to collect, analyze, and utilize large volumes of agricultural data to optimize crop productivity and resource management. Modern precision agriculture systems combine several advanced technologies including satellite positioning systems, unmanned aerial vehicles (UAVs), Internet of Things sensors, artificial intelligence analytics, and autonomous agricultural machinery.

Satellite-based navigation systems remain one of the most widely used technologies in precision agriculture. GPS-enabled tractors and planting equipment allow farmers to maintain field operation accuracy within 2–3 centimeters, significantly improving planting consistency and fertilizer distribution efficiency. These systems also enable automated steering capabilities, reducing driver fatigue and enabling continuous field operations.

Agricultural drones represent another rapidly expanding technology segment. More than 600,000 agricultural drones are currently deployed worldwide, capturing high-resolution images used to detect crop diseases, soil moisture variations, and pest infestations. Drone-based crop monitoring can analyze hundreds of hectares within minutes, improving crop health detection accuracy and reducing manual field inspections.

The integration of IoT sensors is also transforming farm management systems. Soil sensors capable of measuring moisture, temperature, and nutrient levels provide real-time insights that enable farmers to optimize irrigation and fertilizer applications. In many farms, sensor-based irrigation systems have demonstrated the ability to reduce water usage by 30–35% while maintaining stable crop yields.

Artificial intelligence and machine learning technologies are further enhancing the capabilities of precision agriculture systems. AI-driven analytics platforms can process satellite imagery, weather data, and soil measurements to predict crop diseases and recommend targeted treatment strategies. Predictive crop models can identify pest infestations up to 10 days earlier than traditional scouting methods, enabling timely interventions that minimize crop damage.

Autonomous agricultural machinery is another emerging innovation shaping the future of precision farming. Self-driving tractors, robotic harvesters, and automated planting systems allow farms to operate continuously with minimal human supervision. These technologies improve operational efficiency and address labor shortages in agricultural regions.

Together, these technologies are transforming agricultural operations into highly data-driven ecosystems capable of improving productivity, sustainability, and resilience against climate variability.

• In January 2025, Deere & Companyunveiled its second-generation autonomous farming equipment at CES 2025, including the Autonomous 9RX tractor equipped with 16 cameras and advanced computer-vision AIto navigate fields and perform large-scale tillage tasks with minimal human supervision, improving operational efficiency and addressing labor shortages in agriculture.

• In March 2025, Deere & Companyhighlighted the continued development of autonomous farming platforms and autonomous tillage technologies, enabling farmers to monitor and control machines remotely through the John Deere Operations Center mobile platform, providing real-time machine data, video monitoring, and job-quality alerts for connected farms.

• In November 2023 (technology rollout continuing through 2024 deployments), Trimble Inc.introduced the Trimble Ag Software–Data license, enabling seamless connectivity between in-cab displays and cloud-based farm management platforms, allowing farmers to standardize, visualize, and manage agricultural field data across multiple equipment systems and digital workflows. Source: www.trimble.com

• In September 2023 (expanded globally through 2024 technology integration), AGCO Corporationand Trimble Inc.announced a strategic joint venture to accelerate mixed-fleet precision agriculture solutions, combining Trimble’s precision agriculture technology with AGCO’s autonomous machine software capabilities to deliver integrated smart-farming platforms for farmers worldwide.

The Precision Farming Market Report provides a comprehensive analysis of the global precision agriculture ecosystem, focusing on the technologies, applications, and end-user industries shaping the evolution of digital farming practices. The report evaluates a wide range of precision agriculture solutions including automation and control systems, satellite-based navigation technologies, drone monitoring platforms, soil and crop sensing devices, farm management software, and AI-driven analytics systems.

The scope of the report covers key agricultural applications such as crop monitoring, irrigation management, yield mapping, soil nutrient analysis, and livestock monitoring. These applications play a critical role in improving farm productivity and reducing resource waste by enabling farmers to implement targeted interventions based on real-time data insights. The report also evaluates the operational role of precision farming technologies across various farm sizes including large commercial farms, medium-scale agricultural enterprises, and cooperative farming systems.

Geographically, the report examines regional trends across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, analyzing differences in technology adoption, agricultural infrastructure, and government support programs for smart farming initiatives. It highlights the role of digital agriculture policies, environmental sustainability goals, and food security initiatives in shaping regional technology deployment.

In addition, the report evaluates the competitive ecosystem consisting of global agricultural equipment manufacturers, ag-tech software providers, and emerging technology startups. More than 120 companies globally are actively developing precision agriculture solutions, ranging from satellite-based crop monitoring platforms to fully autonomous farm machinery.

Emerging focus areas explored in the report include AI-driven crop analytics, robotic farming systems, smart irrigation technologies, and satellite-based agricultural monitoring networks. These innovations are expected to transform agricultural productivity models by enabling farms to operate as highly connected digital ecosystems capable of optimizing crop yields, reducing environmental impact, and improving long-term agricultural sustainability.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 130.0 Million |

| Market Revenue (2033) | USD 365.7 Million |

| CAGR (2026–2033) | 13.8% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Deere & Company; Trimble Inc.; AGCO Corporation; Raven Industries; Topcon Positioning Systems; Kubota Corporation; CNH Industrial; AG Leader Technology; Climate LLC; PrecisionHawk; Taranis; Granular Inc.; DICKEY-john Corporation; Farmers Edge |

| Customization & Pricing | Available on Request (10% Customization Free) |