Reports

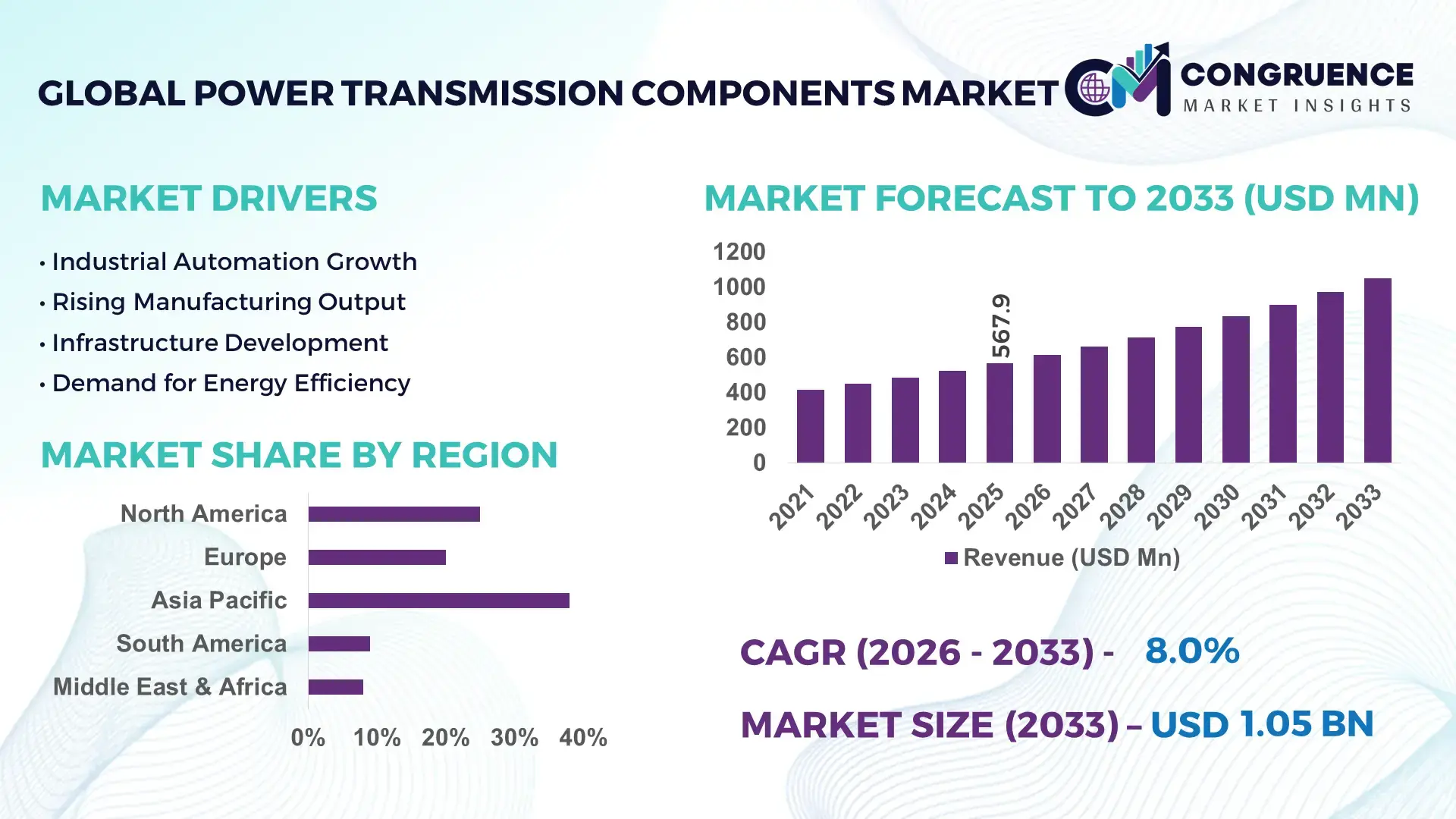

The Global Power Transmission Components Market was valued at USD 567.92 Million in 2025 and is anticipated to reach a value of USD 1051.18 Million by 2033 expanding at a CAGR of 8% between 2026 and 2033. This growth is supported by rising industrial automation, expanding manufacturing capacity, and increasing demand for energy-efficient mechanical systems across multiple industries.

China represents the most influential country in the Power Transmission Components Market, supported by its large-scale industrial base and advanced manufacturing ecosystem. The country produces over 35% of the world’s industrial machinery components annually, with power transmission elements such as gears, bearings, couplings, and belts forming a critical segment. In 2024, China’s industrial equipment investment exceeded USD 210 billion, with heavy allocation toward smart factories and robotics integration. Power transmission components are extensively deployed across automotive manufacturing, wind power installations, mining operations, and high-speed rail systems exceeding 45,000 km in operational length. The country has also accelerated adoption of precision gearboxes, low-friction bearings, and digitally monitored transmission systems, with over 40% of new industrial installations incorporating sensor-enabled or condition-monitoring components.

Market Size & Growth: Valued at USD 567.92 Million in 2025, projected to reach USD 1051.18 Million by 2033 at a CAGR of 8%, driven by rising automation intensity and equipment modernization.

Top Growth Drivers: Industrial automation adoption ~32%, energy-efficiency improvement ~27%, machinery replacement rate ~21%.

Short-Term Forecast: By 2028, predictive maintenance integration is expected to reduce unplanned downtime by approximately 18%.

Emerging Technologies: Smart bearings with IoT sensors, high-torque lightweight composite gears, digitally integrated mechatronic drive systems.

Regional Leaders: Asia-Pacific projected at USD 412 Million by 2033 with rapid factory automation; Europe at USD 296 Million driven by efficiency mandates; North America at USD 241 Million supported by advanced manufacturing upgrades.

Consumer/End-User Trends: Automotive, manufacturing, and energy sectors increasingly favor modular, low-maintenance, high-load transmission systems.

Pilot or Case Example: A 2024 smart factory pilot using sensor-enabled gearboxes achieved a 22% maintenance cost reduction.

Competitive Landscape: Siemens holds approximately 18% share, followed by ABB, SKF, Rexnord, Timken, and Regal Rexnord.

Regulatory & ESG Impact: Energy-efficiency standards and carbon-reduction mandates are accelerating adoption of low-loss transmission components.

Investment & Funding Patterns: Over USD 6.5 Billion invested globally since 2022 in advanced manufacturing equipment and drivetrain modernization.

Innovation & Future Outlook: Integration of digital twins, AI-based wear prediction, and fully integrated electromechanical drive platforms is shaping future deployments.

The Power Transmission Components Market serves critical industry sectors including automotive manufacturing, industrial machinery, energy generation, mining, and material handling, with automotive and industrial equipment accounting for over half of total demand. Recent innovations such as condition-monitoring bearings, precision planetary gear systems, and high-efficiency couplings are improving reliability and lifecycle performance. Regulatory emphasis on energy efficiency and emissions reduction is influencing component design and material selection. Asia-Pacific leads consumption due to manufacturing scale, while Europe emphasizes efficiency-driven upgrades and North America focuses on digitalized production systems. Emerging trends include smart transmission systems, lightweight materials, and integration with Industry 4.0 platforms, supporting long-term market expansion and technological advancement.

The Power Transmission Components Market holds strategic relevance as a foundational enabler of industrial productivity, operational reliability, and energy efficiency across manufacturing, automotive, energy, and infrastructure sectors. These components—ranging from gears and bearings to couplings and drive systems—directly influence equipment uptime, torque efficiency, and lifecycle costs, making them critical to enterprise-level operational strategy. Advanced technologies such as sensor-enabled smart bearings deliver nearly 25% efficiency improvement compared to conventional mechanical bearings, while reducing friction-related energy losses by measurable margins. Asia-Pacific dominates in production volume due to large-scale manufacturing clusters, while Europe leads in adoption, with over 42% of industrial enterprises deploying high-efficiency or digitally monitored transmission systems.

By 2028, AI-driven predictive maintenance and digital twin integration are expected to cut unplanned downtime by approximately 20%, improving asset utilization and maintenance planning accuracy. Firms are increasingly committing to ESG performance improvements, including a 30% reduction in energy losses from mechanical systems and up to 25% recyclable material usage in component manufacturing by 2030. In 2024, a Germany-based industrial automation initiative achieved an 18% reduction in maintenance costs through AI-enabled gearbox monitoring across automotive production lines. Looking ahead, the Power Transmission Components Market is positioned as a pillar of industrial resilience, regulatory compliance, and sustainable growth, supporting long-term competitiveness through efficiency-led innovation and data-driven operational models.

Industrial automation is a primary driver of demand for advanced power transmission components, as automated systems require precise, reliable, and high-efficiency motion control solutions. Over 60% of newly installed industrial robots rely on precision gearboxes and high-load bearings to maintain accuracy and repeatability. Automated production lines operate at higher speeds and duty cycles, increasing wear on mechanical systems and driving replacement demand. Additionally, automation-intensive sectors such as automotive manufacturing and electronics assembly are adopting modular transmission components to reduce maintenance intervals by up to 15%. This shift toward automation-centric production environments continues to expand the installed base of power transmission components globally.

The Power Transmission Components Market faces restraints from fluctuating raw material prices, particularly steel alloys, copper, and specialty composites used in high-performance components. Material cost volatility of 10–18% annually complicates long-term pricing strategies for manufacturers and procurement planning for end users. Supply chain disruptions have also extended lead times for precision components by several weeks in certain regions, delaying equipment upgrades and new installations. Smaller manufacturers are disproportionately affected due to limited sourcing flexibility, while end users may defer replacement cycles, impacting overall market momentum.

Smart manufacturing presents significant opportunities for the Power Transmission Components Market through the adoption of intelligent, connected mechanical systems. Sensor-integrated bearings and gearboxes enable condition monitoring and predictive analytics, reducing maintenance-related downtime by up to 20%. Governments and industrial bodies are actively promoting Industry 4.0 adoption, accelerating investments in digitally enabled machinery. Retrofitting existing equipment with smart transmission components is gaining traction, especially in mature industrial regions, creating a large aftermarket opportunity. These developments support value-added offerings and long-term service-based revenue models for component suppliers.

Increasing regulatory requirements related to energy efficiency, noise reduction, and material sustainability pose challenges for manufacturers in the Power Transmission Components Market. Compliance often necessitates redesigning components to meet stricter performance thresholds, increasing engineering and testing costs. Advanced components incorporating sensors and electronics also raise technical complexity, requiring specialized skills for installation and maintenance. In regions with limited technical workforce availability, adoption rates may slow despite clear efficiency benefits. Balancing regulatory compliance, cost control, and performance optimization remains a persistent challenge for industry participants.

• Acceleration of Modular and Prefabricated Construction Adoption: The rise of modular and prefabricated construction is reshaping demand patterns in the Power Transmission Components market by increasing the need for precision-driven, high-reliability mechanical systems. Around 55% of newly developed industrial and infrastructure projects report measurable cost benefits from modular and prefabricated construction practices, primarily due to reduced on-site labor and shortened project timelines. Pre-bent, pre-cut, and pre-assembled elements are increasingly manufactured off-site using automated machinery, where power transmission components such as precision gearboxes, linear drives, and bearings play a critical role. In Europe and North America, over 48% of construction equipment manufacturers have upgraded machinery to support prefabrication workflows, driving higher demand for compact, high-torque transmission systems capable of continuous operation.

• Integration of Smart and Sensor-Enabled Transmission Components: Smart power transmission components equipped with sensors and connectivity features are gaining rapid traction across industrial sectors. Nearly 38% of newly installed industrial gearboxes and bearings now include condition-monitoring capabilities, enabling real-time tracking of vibration, temperature, and load. These systems have demonstrated up to 20% improvement in maintenance efficiency by enabling predictive servicing instead of reactive repairs. Manufacturing facilities adopting sensor-enabled transmission systems report up to 15% longer component lifespan, supporting operational continuity and reducing equipment replacement frequency.

• Shift Toward Lightweight and High-Strength Materials: Material innovation is emerging as a key trend, with manufacturers increasingly adopting lightweight alloys and advanced composites in power transmission components. High-strength aluminum alloys and composite materials reduce component weight by 18–25% while maintaining comparable torque capacity to traditional steel-based systems. This shift supports energy efficiency goals, as lighter components can lower overall machine energy consumption by approximately 10–12%, particularly in high-speed and automated equipment applications such as robotics and material handling.

• Expansion of Automation in Heavy Industries and Energy Applications: Automation adoption in heavy industries such as mining, cement, and renewable energy is driving demand for durable, high-load power transmission components. More than 45% of new wind turbine installations now use advanced gearbox systems with enhanced torque density and wear resistance. In mining operations, automated conveyor and crushing systems equipped with upgraded transmission components have achieved productivity gains of nearly 14%, reflecting the growing importance of robust mechanical systems in harsh operating environments.

The Power Transmission Components market is segmented based on type, application, and end-user, each reflecting distinct demand drivers and adoption patterns across industrial ecosystems. By type, mechanical components such as gears, bearings, couplings, chains, and belts dominate due to their essential role in torque transfer, motion control, and load management. Application-wise, industrial machinery and manufacturing systems account for the largest usage, supported by automation upgrades and equipment replacement cycles, while energy and infrastructure applications are expanding steadily. From an end-user perspective, automotive, industrial manufacturing, and energy sectors remain primary consumers, driven by high equipment utilization rates and strict performance requirements. Segmentation trends highlight increasing preference for high-efficiency, digitally enabled components and growing diversification of demand across both heavy and precision-driven industries.

The Power Transmission Components market by type includes gears, bearings, couplings, chains, belts, clutches, and other mechanical drive elements. Bearings represent the leading type, accounting for approximately 34% of total adoption, as they are indispensable across virtually all rotating machinery and are replaced frequently due to wear. Gears follow closely with around 28% share, driven by demand for precision torque control in automated and high-load applications. Smart and sensor-integrated bearings and gear systems are the fastest-growing type, expanding at an estimated 9.6% CAGR, supported by predictive maintenance adoption and reduced downtime requirements. Chains, belts, and couplings together contribute a combined share of nearly 30%, serving niche and cost-sensitive applications in conveyors, packaging, and material handling.

By application, industrial machinery and manufacturing equipment lead the Power Transmission Components market, representing roughly 41% of total usage due to continuous operation cycles and high mechanical load demands. Energy and power generation applications account for approximately 27%, supported by wind turbines, hydroelectric systems, and thermal power plants requiring durable transmission systems. The fastest-growing application segment is renewable energy installations, expanding at an estimated 10.2% CAGR, driven by increased deployment of wind and solar systems that rely on high-torque gearboxes and precision bearings. Automotive, mining, and construction equipment collectively contribute around 24% of application demand, supported by fleet upgrades and automation trends.

End-user analysis shows that industrial manufacturing remains the largest segment, holding approximately 38% share, as factories rely heavily on power transmission components for production lines, robotics, and material handling systems. The automotive sector follows with about 26% adoption, driven by high-volume machinery usage and precision requirements. The fastest-growing end-user segment is the renewable energy sector, advancing at an estimated 10.8% CAGR, fueled by wind turbine installations and grid modernization initiatives. Mining, construction, and oil & gas industries collectively represent nearly 28% of end-user demand, supported by heavy-duty equipment usage and replacement cycles.

Asia-Pacific accounted for the largest market share at 38% in 2025 however, Middle East & Africa is expected to register the fastest growth, expanding at a CAGR of 9.4% between 2026 and 2033.

Asia-Pacific dominance is supported by high industrial output, accounting for over 45% of global manufacturing equipment installations, with China, India, and Japan as primary contributors. Europe followed with approximately 26% share, driven by regulatory-led upgrades and energy-efficient machinery adoption. North America held nearly 24% share, supported by advanced automation, predictive maintenance adoption exceeding 40% of large enterprises, and steady replacement of legacy systems. South America and Middle East & Africa together accounted for about 12%, with demand concentrated in energy, mining, and infrastructure projects. Regional consumption patterns vary significantly, with Asia-Pacific leading in volume deployment, Europe prioritizing compliance-driven upgrades, and the Middle East & Africa focusing on capacity expansion linked to construction and energy diversification initiatives.

How is advanced industrial automation reshaping component demand patterns?

North America accounts for approximately 24% of the global Power Transmission Components market, supported by strong demand from automotive manufacturing, aerospace, energy, and advanced industrial machinery sectors. Over 52% of large manufacturing facilities in the region have implemented automation upgrades requiring high-precision gears, bearings, and couplings. Regulatory support for energy efficiency and workplace safety standards has accelerated the replacement of legacy mechanical systems. Digital transformation is evident, with nearly 46% of enterprises integrating sensor-enabled transmission components for predictive maintenance. A leading regional manufacturer has expanded smart bearing production lines, reporting a 20% improvement in equipment uptime for customers. Consumer behavior reflects higher enterprise adoption in capital-intensive industries, with preference for high-reliability, long-life components over low-cost alternatives.

Why are compliance-driven upgrades accelerating technology adoption?

Europe represents around 26% of the Power Transmission Components market, with Germany, the UK, and France collectively contributing over 60% of regional demand. Strict sustainability and energy-efficiency frameworks have pushed more than 48% of industrial firms to adopt low-friction, high-efficiency transmission systems. Regulatory bodies emphasize reduced mechanical losses and recyclability, influencing procurement strategies. Adoption of digitally monitored gearboxes and bearings has reached nearly 44% across large manufacturing sites. A major European industrial group has introduced recyclable steel-alloy gears, reducing material waste by 18%. Consumer behavior in the region shows strong preference for compliant, explainable, and efficiency-certified power transmission components.

What makes large-scale manufacturing the core growth engine?

Asia-Pacific leads the global market by volume, accounting for roughly 38% of total installations. China, India, and Japan dominate consumption due to expansive manufacturing bases and infrastructure investment. The region accounts for more than 50% of global industrial machinery output, driving sustained demand for gears, bearings, and drive systems. Manufacturing automation, smart factories, and robotics adoption are accelerating, with over 42% of new factories integrating digitally enabled transmission components. A prominent regional supplier expanded high-torque gearbox capacity by 30% in 2024 to support robotics and renewable energy applications. Consumer behavior is volume-driven, emphasizing durability, scalability, and cost-efficient performance.

How are energy and infrastructure projects shaping demand momentum?

South America holds approximately 7% of the global Power Transmission Components market, led by Brazil and Argentina. Infrastructure modernization and energy sector investments account for nearly 58% of regional demand. Mining and hydropower projects are key drivers, with mechanical system upgrades improving equipment availability by up to 16%. Government incentives supporting domestic manufacturing and import substitution have encouraged local sourcing. A regional manufacturer reported a 22% increase in demand for heavy-duty gear assemblies used in mining conveyors. Consumer behavior is closely tied to project-based procurement, with emphasis on rugged components capable of operating in harsh environments.

Why is capacity expansion driving accelerated adoption?

Middle East & Africa contributes about 5% of the global market but shows the fastest expansion trajectory. Demand is concentrated in oil & gas, construction, mining, and renewable energy sectors. UAE and South Africa together represent over 55% of regional consumption. Industrial modernization programs have increased adoption of advanced transmission systems by nearly 28% since 2023. Trade partnerships and localization policies support regional assembly of mechanical components. A Gulf-based industrial supplier introduced corrosion-resistant bearings for offshore energy projects, improving operational life by 19%. Consumer behavior prioritizes durability, load tolerance, and climate-resistant designs.

China – 22% market share: High production capacity and extensive manufacturing infrastructure supporting large-scale industrial deployment of Power Transmission Components.

United States – 17% market share: Strong end-user demand driven by automation-intensive industries and widespread adoption of advanced, digitally enabled Power Transmission Components.

The Power Transmission Components market is characterized by a moderately fragmented competitive structure, with more than 120 active global and regional manufacturers competing across mechanical, electromechanical, and smart transmission categories. The top 5 companies collectively account for approximately 46% of total market activity, indicating strong competition beyond leading players. Market positioning is increasingly defined by technological differentiation, product reliability, lifecycle efficiency, and the ability to support predictive maintenance and digital integration. Over 35% of leading manufacturers have launched sensor-enabled or condition-monitoring transmission components since 2023, reflecting a shift toward value-added and service-oriented offerings. Strategic initiatives such as cross-border partnerships, localized manufacturing expansion, and targeted acquisitions are accelerating, with nearly 28% of major players engaging in joint ventures to strengthen regional presence. Product innovation cycles have shortened, with new gearbox, bearing, and coupling designs introduced every 18–24 months to meet efficiency and compliance demands. Competition is also influenced by sustainability goals, as over 40% of companies have committed to reducing mechanical energy losses by more than 15% through advanced materials and precision engineering. Overall, competitive intensity remains high as players balance cost efficiency, technological leadership, and regulatory alignment.

Siemens AG

ABB Ltd.

SKF Group

Timken Company

Regal Rexnord Corporation

Rexnord Corporation

Schaeffler Group

NSK Ltd.

NTN Corporation

Emerson Electric Co.

Altra Industrial Motion Corp.

Dana Incorporated

Bonfiglioli Riduttori S.p.A.

Sumitomo Heavy Industries

Nord Drivesystems

Technological advancement is reshaping the Power Transmission Components Market through the convergence of mechanical engineering, digital intelligence, and materials science. One of the most impactful developments is the integration of sensor-enabled and IoT-ready components, including smart bearings, gearboxes, and couplings capable of monitoring vibration, temperature, and load in real time. Nearly 40% of newly installed industrial transmission systems now incorporate embedded sensing, enabling predictive maintenance strategies that have demonstrated up to 20% reductions in unplanned downtime and 15% improvements in asset utilization.

Material innovation is another key technology driver. Advanced steel alloys, surface-hardened gears, and hybrid ceramic bearings are increasingly deployed to improve wear resistance and thermal stability. These materials extend component service life by 18–25% compared to conventional designs, particularly in high-speed and high-load environments such as robotics, wind energy, and automated manufacturing lines. Lightweight aluminum and composite-based transmission elements are also gaining traction, reducing system weight by up to 22% and lowering energy consumption in dynamic applications.

Digital engineering tools, including digital twins and simulation-driven design, are improving performance validation and accelerating product development cycles. Over 30% of large manufacturers now use digital twin models to simulate stress, fatigue, and efficiency under real-world operating conditions, reducing physical prototyping time by approximately 25%. Additive manufacturing is emerging as a complementary technology for producing complex gear geometries and customized couplings, shortening lead times by nearly 35% for low-volume or specialized components.

Electromechanical integration represents another transformative trend, with power transmission components increasingly embedded within compact drive systems combining motors, sensors, and control electronics. More than 28% of new industrial drive installations now feature integrated mechatronic solutions, enhancing precision control and simplifying system architecture. Together, these technologies are positioning the Power Transmission Components Market for higher efficiency, reliability, and adaptability across industrial sectors.

• In March 2025, Regal Rexnord announced the completion of the acquisition of Gates Corporation’s Power Transmission Solutions unit, expanding its mechanical power transmission portfolio and strengthening its position in gear drives, couplings, and bearing systems for industrial applications.

• In April 2025, SKF Group launched a new family of high-efficiency bearings engineered for electric drive applications, offering reduced friction and extended service life for wind turbines and industrial gearboxes, enhancing durability and performance metrics in demanding environments.

• In June 2024, SKF introduced its X-Tracker series of bearings for heavy machinery, delivering higher operational efficiency and prolonged service life in wind energy and industrial applications, reflecting rising focus on advanced material and design technologies.

• In August 2025, SKF unveiled advanced Infinium bearings featuring Laser Metal Deposition (LMD) technology designed for circular use, enabling bearings to be reclad and reused repeatedly, marking a significant innovation in sustainability and lifecycle extension for core power transmission components. (Power Transmission)

The Power Transmission Components Market Report encompasses a comprehensive analysis of mechanical and electromechanical transmission systems used across industrial, automotive, energy, and infrastructure sectors. The report examines a wide range of product segments including gears, bearings, couplings, chains, belts, clutches, and integrated drive assemblies, detailing performance criteria, material specifications, and design innovation. It provides region-wise insights into demand patterns across North America, Europe, Asia-Pacific, South America, and Middle East & Africa, outlining how deployment varies by manufacturing intensity, regulatory frameworks, and technological adoption. Individually profiled segments highlight key applications such as industrial machinery, renewable energy equipment, automotive powertrains, material handling systems, and construction equipment, with analysis of usage metrics, equipment integration trends, and retrofit cycles.

The report also evaluates technology themes shaping future power transmission components, including sensor-enabled predictive maintenance systems, digitally integrated gearbox platforms, additive manufacturing use cases, and lightweight material adoption. End-user behavior is assessed for leading sectors such as heavy manufacturing, energy generation, automotive, and precision automation environments, with quantified adoption rates and technology upgrade cycles. Niche segments such as high-speed robotics, renewable energy infrastructure, and electric vehicle drivetrain components are explored to identify emerging demand nodes. Coverage includes industry challenges such as supply chain variability, raw material constraints, and compliance pressures, while also detailing competitive positioning, strategic initiatives, and innovation roadmaps that influence market evolution. The report is designed to support decision-makers with clear segmentation, regional prioritization, performance benchmarks, and forward-looking insights.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

8% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Siemens AG, ABB Ltd., SKF Group, Timken Company, Regal Rexnord Corporation, Rexnord Corporation, Schaeffler Group, NSK Ltd., NTN Corporation, Emerson Electric Co., Altra Industrial Motion Corp., Dana Incorporated, Bonfiglioli Riduttori S.p.A., Sumitomo Heavy Industries, Nord Drivesystems |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |