Reports

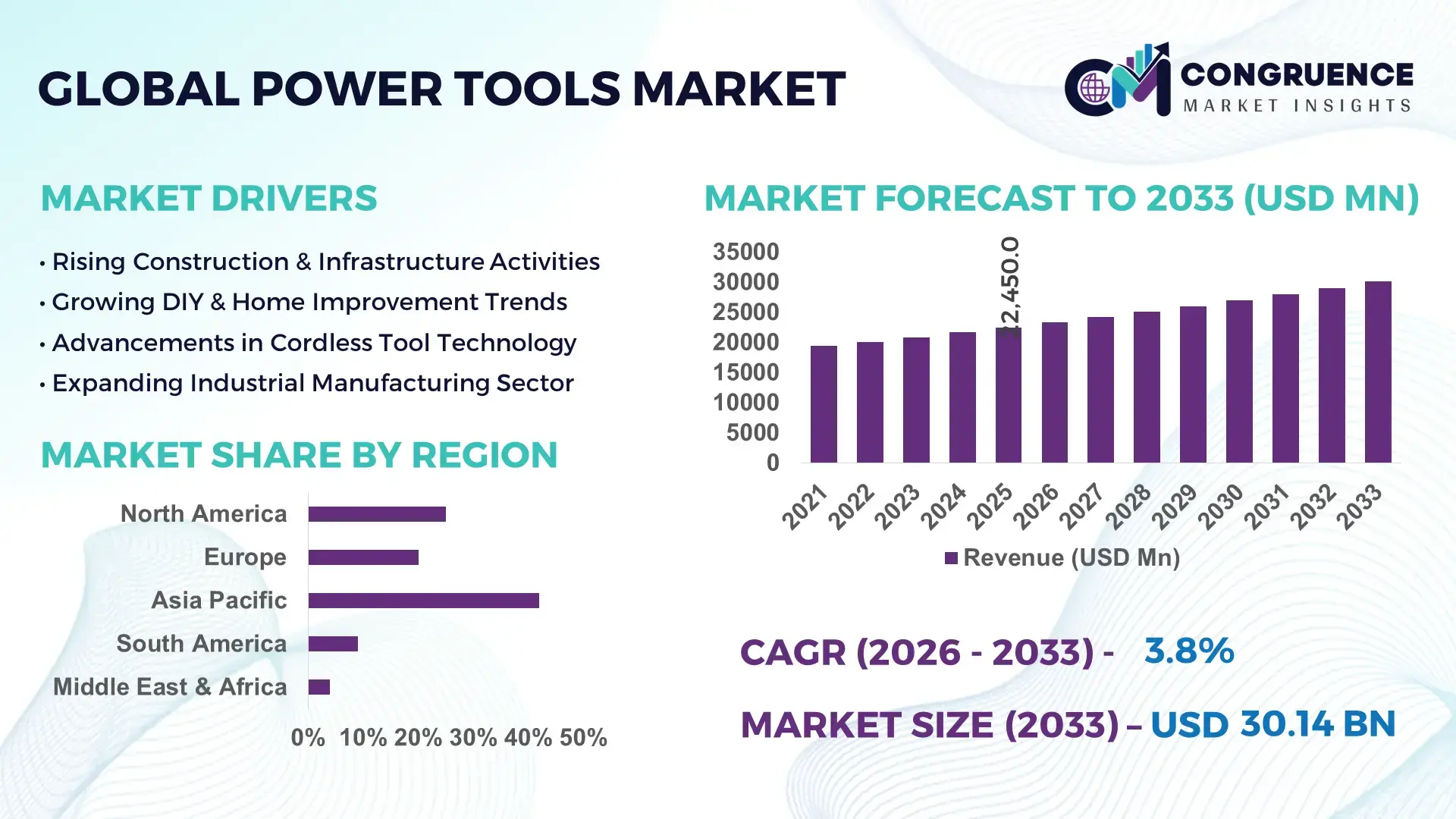

The Global Power Tools Market was valued at USD 22450 Million in 2025 and is anticipated to reach a value of USD 30138.46 Million by 2033 expanding at a CAGR of 3.75% between 2026 and 2033. This growth is primarily driven by rising construction activity and increased adoption of cordless and energy-efficient tools across industrial and residential applications.

China continues to lead the global power tools market with extensive manufacturing capacity exceeding 40% of global production output, supported by large-scale industrial clusters in provinces such as Guangdong and Zhejiang. The country has witnessed annual investments surpassing USD 3 billion in advanced manufacturing facilities, particularly for lithium-ion battery-powered tools. Industrial applications such as automotive assembly, infrastructure development, and electronics manufacturing account for over 55% of domestic tool consumption. Additionally, over 60% of urban households in major cities have adopted basic power tools for home improvement, reflecting strong consumer penetration. Continuous advancements in brushless motor technology and smart tool integration further strengthen China’s position as a hub for innovation and production efficiency.

Market Size & Growth: Valued at USD 22450 Million in 2025, projected to reach USD 30138.46 Million by 2033, growing at 3.75% CAGR due to increased infrastructure development and DIY tool adoption.

Top Growth Drivers: 45% rise in cordless tool adoption, 30% improvement in operational efficiency from automation, 25% increase in construction activity globally.

Short-Term Forecast: By 2028, productivity in industrial tool applications is expected to improve by 18% through smart tool integration and battery advancements.

Emerging Technologies: Brushless motor systems, IoT-enabled smart tools, and advanced lithium-ion battery platforms are transforming performance and durability.

Regional Leaders: Asia-Pacific projected at USD 13500 Million by 2033 with strong manufacturing demand; North America at USD 7800 Million driven by DIY culture; Europe at USD 6200 Million with sustainability-focused adoption.

Consumer/End-User Trends: Construction and automotive sectors account for over 50% of usage, while residential DIY adoption has increased by 35% in urban regions.

Pilot or Case Example: In 2024, a major industrial manufacturer improved operational efficiency by 22% through AI-enabled predictive maintenance tools.

Competitive Landscape: Market leader holds approximately 18% share, followed by several global manufacturers competing in innovation and pricing strategies.

Regulatory & ESG Impact: Energy efficiency standards and recycling mandates have led to a 20% increase in eco-friendly tool production.

Investment & Funding Patterns: Over USD 5 billion invested globally in R&D and smart manufacturing technologies in recent years.

Innovation & Future Outlook: Integration of AI diagnostics, wireless connectivity, and lightweight materials is expected to reshape future product offerings.

The power tools market is characterized by strong contributions from construction, automotive, aerospace, and electronics industries, collectively accounting for over 70% of total demand. Recent innovations such as high-efficiency brushless motors, compact cordless systems, and AI-enabled diagnostics are significantly improving tool performance and lifespan. Regulatory frameworks promoting energy-efficient equipment and reduced carbon emissions are influencing product design and manufacturing practices. Regionally, Asia-Pacific leads in production and consumption, while North America demonstrates strong growth in DIY and residential applications. Emerging trends such as smart connected tools, ergonomic designs, and sustainable materials are shaping future market evolution, offering long-term opportunities for manufacturers and stakeholders.

The power tools market holds significant strategic relevance as it directly supports global industrial productivity, infrastructure expansion, and technological modernization. Advanced cordless tools powered by lithium-ion batteries are increasingly replacing traditional corded systems, delivering up to 35% higher operational efficiency compared to older electric tools. This transition is enabling faster project completion timelines across construction and manufacturing sectors.

From a regional perspective, Asia-Pacific dominates in production volume, while North America leads in adoption with over 65% of enterprises utilizing advanced cordless and smart tools in industrial workflows. Europe continues to emphasize sustainability, with stringent energy efficiency regulations driving innovation in eco-friendly tool design. By 2028, integration of AI-driven predictive maintenance is expected to reduce equipment downtime by approximately 20%, enhancing overall operational efficiency.

Companies are increasingly aligning with ESG commitments, targeting reductions of up to 25% in carbon emissions through energy-efficient manufacturing processes and recyclable materials. In 2024, a leading manufacturer in Germany achieved a 15% reduction in energy consumption by integrating smart manufacturing systems and automated tool calibration technologies. Strategically, the market is evolving toward connected ecosystems where tools, software, and analytics platforms operate seamlessly to improve productivity and safety. The power tools market is positioned as a critical pillar of industrial resilience, regulatory compliance, and sustainable growth, with continued innovation driving its long-term expansion trajectory.

Rapid global urbanization and infrastructure expansion are significantly boosting demand for power tools across construction and engineering projects. Over 55% of global tool usage is attributed to construction activities, with large-scale infrastructure investments exceeding USD 10 trillion annually worldwide. Power tools enable faster project execution, improving productivity by nearly 30% compared to manual tools. Emerging economies are witnessing a surge in residential and commercial construction, increasing demand for drilling, cutting, and fastening tools. Additionally, government-backed infrastructure programs are accelerating adoption of advanced equipment. The shift toward modular construction techniques and prefabrication further amplifies the need for high-performance power tools, ensuring consistent demand growth across the sector.

The high cost of technologically advanced power tools, particularly cordless and smart-enabled devices, remains a key restraint in the market. Premium tools equipped with brushless motors and IoT features can cost up to 40% more than conventional models, limiting adoption among small and medium-sized enterprises. Additionally, the cost of lithium-ion batteries contributes significantly to overall product pricing. Maintenance and replacement costs further add to the financial burden, especially in price-sensitive markets. While developed regions can absorb these costs due to higher purchasing power, emerging markets face slower adoption rates. This pricing challenge restricts market penetration and creates a gap between advanced and basic tool usage across industries.

The emergence of smart and connected power tools presents significant growth opportunities, particularly in industrial and commercial applications. IoT-enabled tools allow real-time monitoring, predictive maintenance, and usage optimization, improving efficiency by up to 25%. Industries such as manufacturing and automotive are increasingly adopting connected tools to enhance operational control and reduce downtime. The integration of cloud-based platforms and data analytics further expands capabilities, enabling centralized management of tool fleets. Additionally, the growing demand for automation and digitalization in construction projects creates opportunities for advanced tool deployment. As smart infrastructure projects gain traction globally, the demand for intelligent power tools is expected to rise substantially.

Supply chain disruptions and fluctuations in raw material prices present significant challenges for the power tools market. Key components such as steel, aluminum, and lithium used in batteries have experienced price volatility of up to 20% in recent years, impacting production costs. Global logistics constraints and geopolitical uncertainties further complicate supply chain stability, leading to delays in manufacturing and distribution. Additionally, dependency on specific regions for raw material sourcing increases vulnerability to external shocks. Manufacturers are compelled to adjust pricing strategies or absorb costs, affecting profitability. These challenges require strategic sourcing, inventory management, and investment in alternative materials to maintain consistent production and market competitiveness.

• 60% Shift Toward Cordless and Battery-Powered Tools: The global transition to cordless power tools has accelerated significantly, with over 60% of newly purchased tools now powered by lithium-ion batteries. These tools deliver up to 35% higher efficiency and 25% longer runtime compared to older nickel-cadmium systems. Industrial users are increasingly prioritizing portability and flexibility, especially in construction and maintenance environments. Battery innovations, including fast-charging systems capable of reaching 80% capacity within 30 minutes, are further enhancing adoption rates across both professional and residential segments.

• 45% Adoption of Smart and Connected Tool Systems: The integration of IoT-enabled features in power tools has grown rapidly, with approximately 45% of large-scale industrial users implementing connected tool solutions. These systems enable real-time monitoring, predictive maintenance, and usage analytics, reducing equipment downtime by up to 20%. Smart torque control and automated calibration technologies are also improving precision levels by nearly 15%, particularly in automotive assembly lines and aerospace manufacturing applications.

• 55% Increase in Demand from Modular Construction Projects: The adoption of modular and prefabricated construction methods has led to a 55% increase in demand for precision power tools. Automated fabrication processes require tools capable of delivering consistent accuracy within tolerance levels of less than 1 mm. In regions such as Europe and North America, over 50% of large-scale infrastructure projects now incorporate prefabrication techniques, driving demand for high-performance drilling, cutting, and fastening equipment that supports faster project completion timelines.

• 30% Growth in Ergonomic and Lightweight Tool Design: Manufacturers are focusing on ergonomic design improvements, resulting in a 30% increase in demand for lightweight and user-friendly tools. Modern designs reduce operator fatigue by up to 25%, improving productivity in long-duration tasks. Tools weighing less than 2.5 kg are gaining traction among professionals and DIY users alike, particularly in residential renovation projects. Enhanced grip technologies and vibration reduction systems are also contributing to improved safety and operational efficiency.

The power tools market segmentation is defined by diverse product types, applications, and end-user industries, each contributing to overall demand dynamics. By type, cordless tools dominate due to their flexibility and efficiency, while corded tools continue to serve heavy-duty industrial applications requiring uninterrupted power supply. In terms of applications, construction remains the largest segment, accounting for over 50% of total usage, driven by global infrastructure expansion and urban development. Automotive and manufacturing sectors also represent significant adoption, leveraging precision tools for assembly and maintenance operations. From an end-user perspective, industrial users lead with strong demand from large-scale production facilities, while residential users are increasingly adopting compact tools for DIY projects. This segmentation highlights the evolving demand patterns shaped by technological advancements, operational efficiency requirements, and shifting consumer preferences across global markets.

The power tools market is segmented into cordless tools, corded tools, pneumatic tools, and hydraulic tools, each serving distinct operational requirements. Cordless tools currently account for approximately 48% of total adoption, driven by their portability, ease of use, and advancements in lithium-ion battery technology that deliver up to 30% longer runtime. In comparison, corded tools hold around 32% share, primarily used in heavy-duty industrial environments where continuous power supply is critical. However, pneumatic and hydraulic tools collectively contribute about 20%, offering specialized applications in high-force industrial tasks such as automotive assembly and construction drilling. Cordless tools represent the fastest-growing segment, expanding at an estimated CAGR of 5.8%, supported by ongoing battery innovation and increasing demand for flexible work environments. These tools are particularly gaining traction in construction and maintenance activities where mobility is essential.

Application-wise, the power tools market is categorized into construction, automotive, manufacturing, aerospace, and residential sectors. Construction dominates with a 52% share, reflecting extensive use of drilling, cutting, and fastening tools in infrastructure and building projects. Automotive applications account for around 20%, driven by precision assembly requirements and increasing vehicle production volumes. Manufacturing and aerospace sectors collectively contribute approximately 18%, leveraging advanced tools for high-precision operations. Residential applications, including DIY and home improvement, make up the remaining 10% but are steadily growing. Residential applications are the fastest-growing segment, with an estimated CAGR of 6.2%, supported by rising DIY culture and increased availability of affordable, compact tools. Consumers are increasingly investing in multi-functional tools for home maintenance, contributing to higher adoption rates in urban regions.

End-user segmentation in the power tools market includes industrial, commercial, and residential users. Industrial users dominate with approximately 58% share, driven by high demand from manufacturing plants, automotive facilities, and construction companies. Commercial users, including contractors and service providers, account for about 27%, relying on durable and high-performance tools for professional applications. Residential users contribute around 15%, reflecting growing adoption of DIY tools among homeowners. The residential segment is the fastest-growing, expanding at an estimated CAGR of 6.5%, fueled by increased consumer interest in home improvement and the availability of user-friendly, cost-effective tools. Industrial users continue to invest heavily in advanced tools with smart features, achieving productivity improvements of up to 20% through automation and connected systems.

Region Asia-Pacific accounted for the largest market share at 42% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 4.6% between 2026 and 2033.

Asia-Pacific’s dominance is supported by high manufacturing output and infrastructure investments exceeding USD 8 trillion across key economies such as China, India, and Japan. The region contributes over 50% of global power tool production volume, with China alone accounting for more than 35% of total exports. North America holds approximately 26% share, driven by advanced tool adoption and strong DIY culture, with over 65% of households owning at least one power tool. Europe represents nearly 22% of the market, with Germany, the UK, and France leading industrial demand and sustainability-driven innovation. South America and the Middle East & Africa collectively account for around 10%, supported by expanding construction activities and energy sector investments. Increasing urbanization rates above 55% globally and rising industrial automation continue to influence regional demand patterns.

How are advanced technologies reshaping industrial and residential tool adoption?

North America accounts for approximately 26% of the global power tools market, driven by strong demand from construction, automotive, and residential renovation sectors. The region sees over 70% adoption of cordless tools, reflecting a preference for mobility and efficiency. Government initiatives supporting infrastructure development, including investments exceeding USD 1.5 trillion in public projects, are accelerating demand. Regulatory frameworks emphasizing workplace safety and energy efficiency are influencing product innovation, leading to increased adoption of smart and ergonomic tools. Technological advancements such as IoT-enabled tools and AI-based diagnostics are improving productivity by nearly 20%. A notable regional player has focused on expanding its cordless tool portfolio, increasing product launches by over 25% in the last two years. Consumer behavior reflects high DIY participation, with nearly 60% of households engaging in home improvement activities annually.

What role does sustainability and regulation play in shaping advanced tool demand?

Europe holds around 22% of the global power tools market, with Germany, the UK, and France collectively contributing over 65% of regional demand. Strict environmental regulations and sustainability initiatives are driving the adoption of energy-efficient and low-emission tools, with over 40% of manufacturers focusing on eco-friendly product lines. Regulatory bodies enforcing carbon reduction targets have led to a 20% increase in the production of recyclable and battery-powered tools. The region is witnessing strong adoption of brushless motor technology, improving tool efficiency by up to 30%. A leading European manufacturer has invested heavily in smart tool systems, enhancing operational precision and reducing maintenance needs by 15%. Consumer behavior in the region is influenced by regulatory compliance, with businesses prioritizing certified and energy-efficient equipment across industrial applications.

How is large-scale industrialization accelerating demand for advanced tools?

Asia-Pacific represents the largest market by volume, contributing over 42% of global demand. China, India, and Japan are the top consuming countries, collectively accounting for more than 70% of regional usage. Rapid infrastructure development and manufacturing expansion, with industrial output growth exceeding 6% annually in key economies, are driving demand. The region is a hub for innovation, with increasing investments in smart manufacturing and automation technologies. A major regional manufacturer has expanded production capacity by 30% to meet rising global demand for cordless tools. Consumer behavior is shifting toward affordable and multifunctional tools, with e-commerce platforms contributing to over 35% of retail sales. The growing adoption of digital tools and mobile applications is further enhancing market penetration.

How are infrastructure investments influencing equipment demand patterns?

South America accounts for approximately 6% of the global power tools market, with Brazil and Argentina leading regional demand. Infrastructure and energy sector projects, including investments exceeding USD 500 billion, are key growth drivers. Government incentives aimed at boosting construction and manufacturing activities have increased equipment adoption by nearly 15% over recent years. Trade policies promoting local manufacturing are also supporting market expansion. A regional manufacturer has focused on cost-effective tool solutions, increasing accessibility for small and medium enterprises. Consumer behavior in the region is influenced by price sensitivity, with demand concentrated on durable and affordable tools. Localization strategies, including language-specific product support, are enhancing market reach and user engagement.

What factors are driving modernization and equipment demand across industries?

The Middle East & Africa region holds around 4% of the global power tools market, with demand driven primarily by oil & gas, construction, and infrastructure sectors. Major growth countries such as the UAE and South Africa are investing heavily in large-scale projects, with construction spending exceeding USD 300 billion. Technological modernization efforts, including the adoption of advanced drilling and cutting tools, are improving operational efficiency by up to 18%. Trade partnerships and regulatory reforms are facilitating the import of high-performance equipment. A local distributor has expanded its product portfolio by 20% to meet growing industrial demand. Consumer behavior reflects a preference for high-durability tools suited for extreme environmental conditions, particularly in oil and gas operations.

China – 35% share: Power Tools market dominance driven by large-scale manufacturing capacity and high export volumes.

United States – 22% share: Power Tools market leadership supported by strong industrial demand and widespread residential tool adoption.

The power tools market is moderately fragmented, with over 150 active global and regional competitors operating across various segments. The top five companies collectively account for approximately 45% of the total market share, indicating a competitive yet consolidated structure among leading players. Market leaders are focusing heavily on product innovation, with over 60% of new product launches featuring cordless and smart-enabled technologies. Strategic initiatives such as mergers, acquisitions, and partnerships have increased by nearly 20% in recent years, enabling companies to expand their geographic presence and technological capabilities.

Innovation remains a key competitive factor, with manufacturers investing over USD 5 billion annually in research and development to enhance battery performance, tool efficiency, and digital integration. Companies are also prioritizing sustainability, with more than 35% of product portfolios now incorporating eco-friendly materials and energy-efficient designs. Pricing strategies, product differentiation, and brand reputation play critical roles in maintaining market position. Additionally, the rise of e-commerce platforms has intensified competition, with online sales contributing to over 30% of total distribution channels. This dynamic competitive environment encourages continuous innovation and strategic expansion across the global power tools market.

Robert Bosch GmbH

Stanley Black & Decker, Inc.

Makita Corporation

Hilti Corporation

Techtronic Industries Co. Ltd.

Emerson Electric Co.

Atlas Copco AB

Snap-on Incorporated

Panasonic Corporation

Hitachi Industrial Equipment Systems Co., Ltd.

Technological advancements are playing a transformative role in the power tools market, with a strong shift toward cordless, smart, and energy-efficient solutions. Lithium-ion battery technology dominates over 70% of newly developed cordless tools, offering up to 40% higher energy density and enabling longer operational cycles. Fast-charging innovations now allow batteries to reach 80% capacity within 25–30 minutes, significantly reducing downtime in industrial applications. Brushless motor technology has also become standard in over 60% of professional-grade tools, delivering up to 30% greater efficiency and extending tool lifespan by nearly 50% due to reduced friction and heat generation.

The integration of IoT and digital connectivity is reshaping tool performance and asset management. Approximately 45% of large-scale industrial users have adopted connected tools equipped with sensors that monitor usage patterns, torque output, and maintenance needs in real time. These smart systems reduce unplanned downtime by up to 20% and improve operational accuracy by 15%, particularly in automotive and aerospace manufacturing environments. Cloud-based platforms further enable centralized fleet management, allowing enterprises to track tool utilization across multiple job sites.

Ergonomic and safety-focused innovations are also gaining prominence, with vibration reduction systems lowering operator fatigue by up to 25% and advanced grip designs improving handling precision. Additionally, the use of lightweight composite materials has reduced tool weight by nearly 20%, enhancing usability without compromising durability. Emerging technologies such as AI-driven diagnostics, augmented reality-assisted maintenance, and automated torque calibration are expected to further optimize performance and safety standards, positioning advanced power tools as critical assets in modern industrial ecosystems.

• In March 2025, Robert Bosch GmbH expanded its professional cordless portfolio by introducing new 18V brushless tools integrated with smart connectivity features. These tools enable real-time diagnostics and usage tracking, improving maintenance efficiency by over 15% and supporting digital workflow integration. Source: www.bosch-professional.com

• In September 2024, Stanley Black & Decker, Inc. launched an upgraded range of DEWALT XR cordless tools featuring enhanced lithium-ion battery systems with extended runtime of up to 25% and improved durability for heavy-duty industrial applications. Source: www.stanleyblackanddecker.com

• In April 2025, Makita Corporation introduced advanced XGT 40Vmax cordless tools designed for high-demand applications, delivering increased power output comparable to corded tools while reducing energy consumption by approximately 20%. Source: www.makita.com

• In November 2024, Hilti Corporation rolled out its Nuron battery platform expansion, enabling compatibility across more than 100 tools while improving jobsite productivity through centralized battery data tracking and enhanced performance analytics. Source: www.hilti.group

The scope of the power tools market report encompasses a comprehensive analysis of product categories, applications, end-user industries, and regional markets, providing a structured view of industry dynamics. The report covers key product segments including cordless tools, corded tools, pneumatic tools, and hydraulic systems, with cordless tools accounting for nearly 48% of total product adoption due to their portability and efficiency. It also evaluates application areas such as construction, automotive, manufacturing, aerospace, and residential usage, where construction alone contributes over 50% of overall demand.

Geographically, the report spans major regions including Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, collectively representing 100% of global market activity. Asia-Pacific leads with over 40% of production and consumption, while North America and Europe together contribute nearly 48% of advanced tool adoption driven by technological innovation and regulatory compliance. The analysis also includes country-level insights for key markets such as China, the United States, Germany, and India, highlighting variations in industrial demand and consumer behavior.

Technological scope within the report focuses on lithium-ion battery advancements, brushless motor integration, IoT-enabled smart tools, and ergonomic design innovations. Over 60% of new product developments incorporate at least one advanced technology feature, reflecting the industry’s shift toward digitalization and efficiency. Additionally, the report examines emerging niches such as AI-enabled diagnostics, connected tool ecosystems, and sustainable manufacturing practices, offering a forward-looking perspective on innovation and competitive positioning across the global power tools market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

3.75% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Robert Bosch GmbH, Stanley Black & Decker, Inc., Makita Corporation, Hilti Corporation, Techtronic Industries Co. Ltd., Emerson Electric Co., Atlas Copco AB, Snap-on Incorporated, Panasonic Corporation, Hitachi Industrial Equipment Systems Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |