Reports

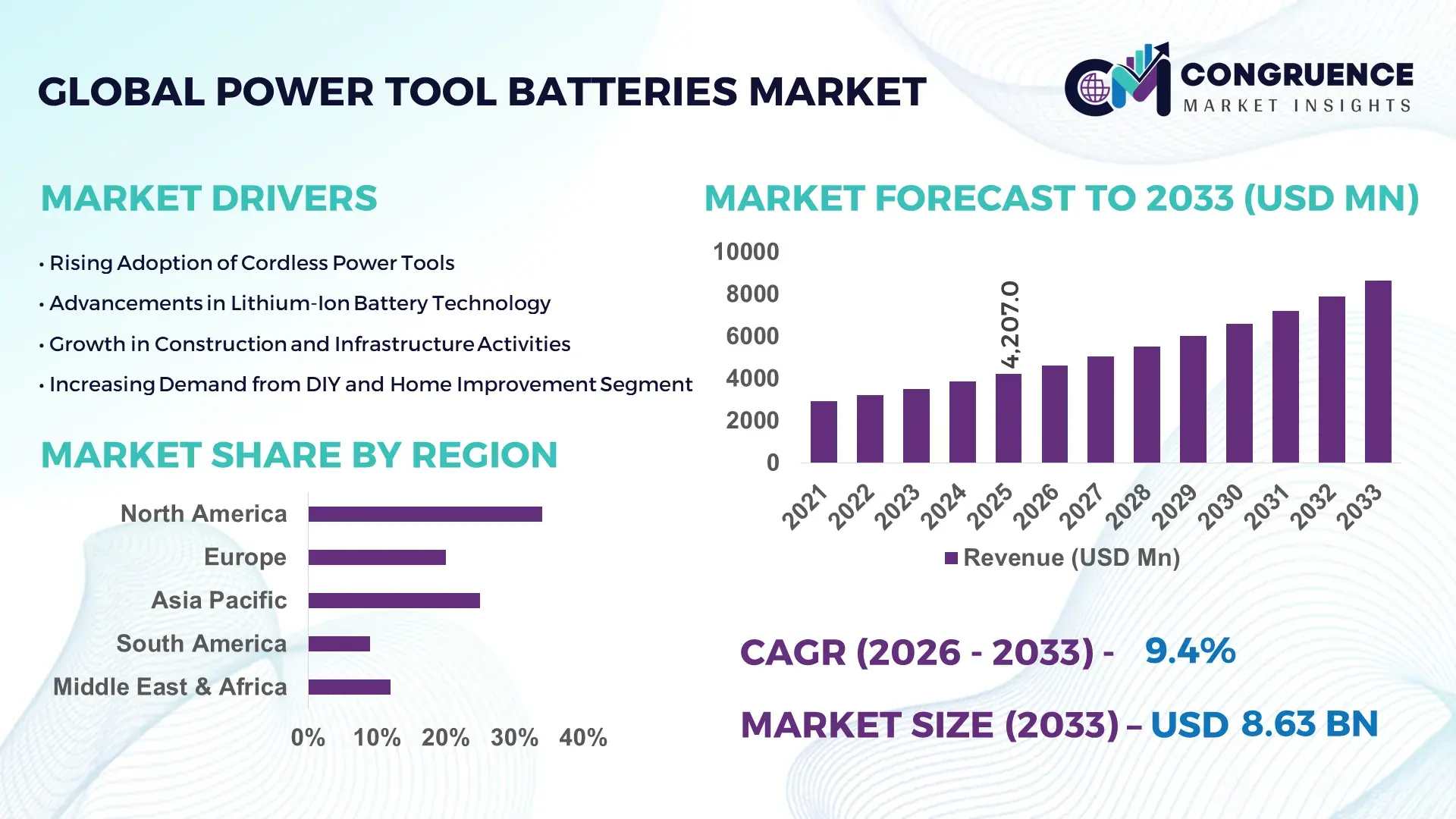

The Global Power Tool Batteries Market was valued at USD 4206.99 Million in 2025 and is anticipated to reach a value of USD 8631.98 Million by 2033 expanding at a CAGR of 9.4% between 2026 and 2033. Growth is primarily driven by rapid cordless tool adoption across construction, automotive, and industrial maintenance sectors.

The United States represents the most influential country in the Power Tool Batteries market, supported by advanced manufacturing infrastructure and high industrial demand. The country hosts more than 35 large-scale lithium-ion battery assembly facilities dedicated to portable and industrial applications, with annual production capacity exceeding 8 GWh for tool-grade battery packs. Over 70% of professional contractors in the U.S. construction industry now rely on cordless platforms, accelerating demand for high-capacity 18V and 20V battery systems. Investments exceeding USD 6 billion in battery cell manufacturing and pack integration facilities between 2022 and 2025 have strengthened domestic supply chains. Additionally, the automotive aftermarket and residential DIY segments contribute significantly, with cordless tool penetration in households surpassing 60%, reinforcing sustained consumption of high-performance power tool batteries.

Market Size & Growth: Valued at USD 4206.99 Million in 2025, projected to reach USD 8631.98 Million by 2033 at 9.4% CAGR, driven by accelerating cordless tool penetration and lithium-ion battery innovation.

Top Growth Drivers: 65% contractor shift to cordless tools, 40% improvement in lithium-ion energy density over a decade, 30% reduction in charging time with fast-charge systems.

Short-Term Forecast: By 2028, next-generation battery management systems are expected to improve cycle life by 25% and reduce overheating incidents by 20%.

Emerging Technologies: Solid-state battery prototypes, AI-enabled battery management systems, and graphene-enhanced anodes for higher discharge efficiency.

Regional Leaders: North America projected at USD 2.9 Billion by 2033 with strong contractor adoption; Asia-Pacific at USD 3.4 Billion driven by manufacturing scale; Europe at USD 1.8 Billion supported by sustainability mandates.

Consumer/End-User Trends: Professional contractors account for over 55% of demand, while DIY consumers increasingly prefer compact 12V lithium-ion systems for home renovation.

Pilot Case Example: In 2024, a U.S.-based manufacturer reduced tool downtime by 18% through AI-integrated battery diagnostics deployment.

Competitive Landscape: Stanley Black & Decker holds approximately 22% share, followed by Bosch, Makita, Milwaukee Tool, and Hilti.

Regulatory & ESG Impact: Battery recycling mandates target 50% material recovery by 2030, accelerating closed-loop battery systems.

Investment & Funding Patterns: Over USD 8 Billion invested globally in lithium-ion cell expansion and pack assembly automation since 2022.

Innovation & Future Outlook: Integration of IoT-enabled battery tracking and modular high-capacity battery platforms is shaping the next generation of cordless power ecosystems.

The Power Tool Batteries market is strongly influenced by construction, automotive repair, woodworking, aerospace maintenance, and infrastructure development sectors. Construction accounts for over 45% of total battery demand, followed by industrial manufacturing at nearly 25%. Recent advancements include high-energy-density lithium-ion cells exceeding 250 Wh/kg, ultra-fast charging systems capable of 80% charge within 30 minutes, and modular battery platforms compatible across multiple tool ranges. Environmental regulations encouraging reduced emissions in job sites are accelerating cordless adoption across Europe and North America. Asia-Pacific demonstrates rising consumption driven by expanding urbanization projects and localized battery manufacturing capacity. Emerging trends such as smart battery diagnostics, predictive maintenance integration, and recyclable cell chemistries are expected to enhance lifecycle performance and sustainability, positioning advanced power tool batteries as essential components in next-generation industrial productivity systems.

The strategic relevance of the Power Tool Batteries Market lies in its central role within the global transition toward cordless, high-efficiency industrial and construction equipment. Lithium-ion battery platforms have become critical to operational mobility, safety compliance, and energy optimization. Advanced lithium-ion cells deliver 35% higher energy density compared to traditional nickel-cadmium batteries, while brushless motor integration improves runtime efficiency by nearly 30%. Solid-state battery technology delivers 20% improvement in safety performance compared to conventional liquid electrolyte systems.

Asia-Pacific dominates in volume due to large-scale battery cell production, while North America leads in adoption with over 70% of professional contractors relying on cordless platforms. By 2028, AI-enabled battery analytics is expected to improve predictive maintenance accuracy by 25%, reducing equipment downtime across commercial job sites.

Firms are committing to ESG metrics such as 50% battery material recycling by 2030 and 40% reduction in carbon intensity across manufacturing facilities. In 2024, a leading U.S. manufacturer achieved 18% improvement in operational efficiency through AI-driven battery monitoring systems integrated into contractor fleets. Strategically, manufacturers are investing in modular battery ecosystems that support cross-platform compatibility, enabling users to operate 100+ tools on a single battery architecture. Over the next decade, digital integration, higher energy density chemistries, and circular economy compliance will position the Power Tool Batteries Market as a pillar of resilience, regulatory alignment, and sustainable industrial growth.

Cordless power tool penetration has exceeded 65% among professional contractors globally, significantly boosting demand for high-capacity lithium-ion battery packs. Construction firms report up to 30% productivity gains when transitioning from corded to cordless platforms due to improved mobility and reduced setup time. Industrial maintenance operations increasingly rely on 18V and 20V battery systems that deliver consistent torque output and extended runtime exceeding 1,000 charge cycles. Residential DIY adoption has also surged, with over 60% of households in developed economies owning at least one cordless tool. Enhanced fast-charging technology reducing charge time by 30% further strengthens operational efficiency. This sustained transition toward cordless ecosystems directly amplifies demand for durable, lightweight, and high-performance power tool batteries.

Lithium carbonate prices have experienced volatility exceeding 40% within short cycles, directly impacting battery cell manufacturing costs. Cobalt and nickel supply chain constraints create additional procurement risks for battery producers. Since raw materials account for nearly 50% of lithium-ion battery production costs, sudden price shifts pressure margins and limit pricing flexibility. Additionally, geopolitical trade restrictions and mining capacity bottlenecks contribute to supply uncertainty. Smaller manufacturers face greater exposure to cost instability, reducing competitiveness. Environmental compliance requirements for mining and processing also increase operational expenses. These combined factors challenge stable production planning and long-term investment predictability within the Power Tool Batteries Market.

Emerging solid-state battery prototypes promise 20–30% higher energy density and improved thermal stability compared to conventional lithium-ion cells. Fast-charging platforms capable of reaching 80% capacity within 30 minutes enhance job-site productivity. Integration of IoT-enabled battery tracking systems provides real-time performance analytics, improving asset utilization by up to 25%. Expanding infrastructure projects across Asia-Pacific and the Middle East create strong demand for durable, high-cycle batteries. Additionally, battery recycling technologies recovering up to 60% of critical materials present opportunities for closed-loop supply chains. Modular battery architectures compatible with multiple tool categories allow manufacturers to expand ecosystem offerings, unlocking cross-selling potential and strengthening long-term customer retention.

Governments are implementing stricter battery recycling regulations targeting material recovery rates of 50% or higher by 2030. Compliance requires investment in collection networks, reverse logistics, and advanced recycling technologies. Extended producer responsibility programs increase operational accountability for manufacturers. Achieving safe disposal and material recovery from lithium-ion batteries involves complex chemical processes and significant capital expenditure. Additionally, evolving transportation regulations for hazardous battery shipments raise logistical costs. Manufacturers must also ensure adherence to international safety certifications, adding testing and quality assurance expenses. These regulatory complexities increase operational burdens and require strategic capital allocation within the competitive Power Tool Batteries Market landscape.

• 48% Increase in High-Capacity Lithium-Ion Battery Adoption Above 5.0Ah: Professional contractors are increasingly shifting toward high-capacity lithium-ion power tool batteries exceeding 5.0Ah, with adoption rising by 48% between 2022 and 2025. These advanced battery packs deliver up to 35% longer runtime and support high-torque brushless tools operating above 1,200W output. Over 60% of newly launched cordless platforms now support 18V–40V battery architectures, enabling cross-compatibility across 50+ tool categories. The push toward longer duty cycles in infrastructure and industrial projects is directly increasing demand for durable, high-energy-density battery solutions.

• 32% Reduction in Charging Time Through Ultra-Fast Charging Systems: Manufacturers have introduced rapid charging technologies capable of achieving 80% charge in under 30 minutes, reducing downtime by nearly 32%. More than 55% of premium power tool batteries now integrate advanced battery management systems (BMS) with thermal control sensors that cut overheating incidents by 20%. Smart chargers equipped with digital diagnostics are being deployed across contractor fleets, improving battery lifecycle performance by 25% and extending usable charge cycles beyond 1,200 cycles.

• 41% Growth in Sustainable and Recyclable Battery Programs: Sustainability mandates are accelerating the adoption of recyclable lithium-ion chemistries, with 41% of large manufacturers implementing closed-loop battery recycling initiatives. Material recovery rates have improved to 60% for lithium and nickel components. Over 50% of European tool manufacturers now offer battery take-back programs aligned with environmental directives, contributing to reduced landfill waste and improved ESG performance metrics.

• 37% Expansion in Modular and Multi-Platform Battery Ecosystems: Modular battery platforms compatible with 80–100 tools per ecosystem have expanded by 37% since 2023. Approximately 70% of professional users prefer unified battery systems to reduce equipment costs and inventory complexity. Interoperable battery designs are lowering fleet management costs by 22% while improving operational flexibility across construction, automotive repair, and heavy maintenance sectors.

The Power Tool Batteries Market is segmented by type, application, and end-user, each demonstrating distinct performance dynamics and adoption trends. Lithium-ion technology dominates the product landscape due to superior energy density and lifecycle performance, while nickel-based chemistries maintain niche relevance in cost-sensitive segments. Applications are primarily concentrated in construction, manufacturing, and automotive maintenance, with construction accounting for the largest share due to high cordless tool penetration exceeding 65% among contractors. From an end-user perspective, professional contractors and industrial enterprises represent the majority of demand, driven by productivity optimization and operational mobility. Meanwhile, residential DIY users contribute significantly through rising home renovation activity, particularly in North America and Europe, where cordless tool ownership surpasses 60% of households. Strategic procurement decisions increasingly focus on battery durability, fast-charging capabilities, and cross-platform compatibility, reinforcing long-term ecosystem adoption within the Power Tool Batteries industry.

Lithium-ion power tool batteries account for approximately 72% of total adoption, driven by energy densities exceeding 250 Wh/kg and cycle life surpassing 1,000 charge cycles. In comparison, nickel-metal hydride (NiMH) systems hold 16%, while nickel-cadmium (NiCd) batteries represent 7%. However, solid-state battery variants, currently below 5% adoption, are projected to grow at a CAGR of 14.8% due to enhanced safety performance and 20–30% higher thermal stability. Lithium-ion remains the leading segment due to lightweight architecture, 35% improved runtime over legacy chemistries, and compatibility with brushless motor systems. NiMH batteries retain relevance in mid-tier tools requiring moderate discharge rates, while NiCd solutions are increasingly limited to specialized industrial environments due to environmental regulations. The combined share of these remaining traditional chemistries totals approximately 23%.

Construction applications account for 46% of total Power Tool Batteries usage, reflecting cordless tool penetration above 65% in professional contracting environments. Manufacturing and industrial maintenance represent 28%, while automotive repair contributes 15%. However, aerospace and heavy infrastructure maintenance, currently at 11%, is expanding fastest with a CAGR of 12.6% due to increased demand for high-performance cordless torque systems. Construction leads due to high tool turnover rates, continuous runtime requirements, and large fleet deployments averaging 40–60 cordless units per site. Manufacturing facilities increasingly deploy battery-powered fastening and drilling systems to improve safety compliance and reduce cable-related hazards by 30%. Automotive workshops report a 25% productivity gain when transitioning to advanced lithium-ion battery platforms.

Professional contractors account for 54% of total Power Tool Batteries demand, while industrial enterprises represent 27%. Residential DIY users hold 14%, and specialized sectors such as utilities and aerospace comprise 5%. However, residential DIY adoption is rising fastest at a CAGR of 11.2%, fueled by home renovation growth and increased cordless tool accessibility. Contractors dominate due to frequent battery cycling, with average annual battery replacements exceeding 3–4 units per worker. Industrial enterprises prioritize high-capacity 20V–40V battery systems to sustain continuous operations across assembly lines. Residential users increasingly adopt compact 12V systems, with household cordless tool ownership surpassing 60% in developed markets.

North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 10.8% between 2026 and 2033.

Europe follows with a 27% share, while Asia-Pacific currently holds 29% and South America and Middle East & Africa collectively contribute 10%. North America benefits from cordless penetration exceeding 70% among contractors, while Europe demonstrates over 50% compliance-driven adoption of recyclable battery systems. Asia-Pacific leads in battery cell manufacturing volume, producing over 60% of global lithium-ion cells used in power tools. Infrastructure expansion projects exceeding 15% annual growth in select Asian economies are increasing battery consumption rates. Regional diversification strategies, localized production facilities, and supply chain investments exceeding USD 8 billion globally are reshaping competitive positioning across the Power Tool Batteries Market.

How Is Advanced Cordless Adoption Transforming Industrial Productivity?

North America holds 34% of the global Power Tool Batteries market, supported by strong construction, automotive, and manufacturing sectors. Over 70% of contractors rely on cordless platforms, with 20V lithium-ion batteries representing the most widely deployed systems. Federal infrastructure investments exceeding USD 1 trillion are accelerating tool fleet upgrades across transportation and utilities projects. Regulatory emphasis on workplace safety has encouraged a 30% reduction in corded equipment usage in commercial settings. Technological advancements include AI-enabled battery diagnostics and IoT-based fleet tracking improving asset utilization by 22%. A leading regional manufacturer, Milwaukee Tool, expanded its high-output battery platform in 2024, delivering 50% more power output in compact designs. Consumer behavior reflects strong DIY engagement, with more than 60% of households owning at least one cordless tool, reinforcing sustained replacement demand.

How Are Sustainability Mandates Driving Battery Innovation and Compliance?

Europe accounts for 27% of the global Power Tool Batteries market, with Germany, the UK, and France leading adoption. Over 50% of regional manufacturers have implemented battery recycling programs aligned with circular economy directives targeting 50% material recovery by 2030. Lithium-ion platforms dominate with 68% penetration across professional tool fleets. Emerging technologies include recyclable cathode materials and smart battery monitoring systems that extend cycle life by 20%. Bosch has intensified development of ProCORE battery systems delivering higher amperage output with improved thermal management. Regional consumer behavior shows heightened sensitivity to environmental compliance, with 58% of enterprise buyers prioritizing recyclable and energy-efficient battery solutions in procurement processes.

What Factors Are Accelerating Manufacturing-Driven Battery Demand?

Asia-Pacific represents 29% of the global Power Tool Batteries market and ranks first in lithium-ion cell production volume. China, Japan, and India are the largest consuming and manufacturing countries, collectively accounting for over 65% of regional battery output. Urban infrastructure growth above 12% annually in select economies is increasing cordless tool deployment. Manufacturing hubs integrate automated battery pack assembly lines improving production efficiency by 25%. A major regional manufacturer, Makita, expanded high-capacity battery production facilities in 2024 to support rising 40V platform demand. Consumer trends indicate strong growth in e-commerce tool sales, with online cordless tool purchases increasing by 35% year-over-year, accelerating battery replacement cycles.

How Is Infrastructure Modernization Stimulating Cordless Tool Expansion?

South America contributes 6% to the global Power Tool Batteries market, led by Brazil and Argentina. Infrastructure development and energy projects are expanding industrial cordless tool usage by 18% annually. Government trade incentives supporting equipment imports have improved battery availability across regional markets. Construction firms increasingly deploy lithium-ion systems to reduce downtime by 20% compared to corded alternatives. Regional consumer behavior reflects growing adoption among small contractors and independent workshops, with portable tool usage rising by 25% in urban centers. Local distributors are strengthening supply chains to reduce lead times by 15%, supporting steady market penetration.

What Role Do Mega Infrastructure Projects Play in Battery Demand?

Middle East & Africa accounts for 4% of global Power Tool Batteries demand, driven by oil & gas maintenance and large-scale construction projects in the UAE and Saudi Arabia, alongside industrial expansion in South Africa. Cordless adoption in commercial construction has increased by 22% over three years due to efficiency gains. Technological modernization includes deployment of high-temperature-resistant lithium-ion batteries suitable for harsh climates. Trade partnerships are improving battery import efficiency by 12%. Industrial contractors increasingly prefer modular battery platforms supporting 30+ tool categories, enhancing operational mobility across energy and infrastructure projects.

United States – 31% share: High production capacity, strong contractor demand, and large-scale infrastructure investments drive sustained Power Tool Batteries adoption.

China – 24% share: Dominant lithium-ion cell manufacturing capacity and expanding construction sector reinforce leadership in the Power Tool Batteries market.

The Power Tool Batteries market is moderately consolidated, with the top 5 companies accounting for approximately 58% of total global market share. More than 40 active international and regional manufacturers compete across lithium-ion, solid-state prototype, and specialty battery segments. Leading participants focus heavily on vertical integration, with over 65% of tier-1 companies controlling both battery pack assembly and advanced battery management system (BMS) development to ensure supply chain resilience and performance differentiation.

Strategic initiatives between 2023 and 2025 include over 25 major product launches centered on high-output 18V–40V lithium-ion platforms and cross-compatible modular battery ecosystems supporting 80–100 tools per battery architecture. Around 30% of leading firms have expanded automated battery assembly lines to improve production efficiency by up to 20%. Partnerships between battery cell manufacturers and tool OEMs have increased by 35%, enabling faster commercialization of high-density cells exceeding 250 Wh/kg.

Innovation competition is primarily driven by ultra-fast charging systems capable of achieving 80% charge within 30 minutes, AI-enabled battery diagnostics improving lifecycle management by 25%, and recyclable cell technologies achieving 60% material recovery. Smaller players compete in niche industrial and specialty voltage categories, collectively holding 42% of the fragmented segment, particularly in emerging markets where localized production reduces logistics costs by 15%.

Stanley Black & Decker

Robert Bosch GmbH

Makita Corporation

Milwaukee Tool

Hilti Group

Techtronic Industries Co. Ltd.

Snap-on Incorporated

Metabo

Festool GmbH

Panasonic Energy Co., Ltd.

Technological advancement in the Power Tool Batteries market is centered on energy density optimization, lifecycle extension, digital integration, and sustainability compliance. Modern lithium-ion cells used in professional-grade batteries now exceed 250 Wh/kg energy density, representing nearly 40% improvement compared to early-generation lithium-ion systems. Advanced 21700 and 4680 cylindrical cell formats are being increasingly adopted due to 15–20% higher capacity within similar footprint dimensions.

Battery management systems (BMS) have evolved with integrated microcontrollers capable of real-time temperature, voltage, and current monitoring across 8–12 cell configurations. AI-enabled predictive diagnostics can improve battery lifespan by up to 25% by preventing over-discharge and thermal stress. Fast-charging platforms now support charging currents exceeding 8A, enabling 80% recharge in less than 30 minutes while maintaining thermal stability.

Solid-state battery prototypes are demonstrating 20–30% higher safety performance due to non-flammable electrolytes. Additionally, silicon-dominant anodes are increasing theoretical energy storage capacity by nearly 10–15% compared to graphite-based systems. Recycling technologies are recovering up to 60% of lithium and nickel content, aligning with regulatory targets requiring 50% material recovery by 2030.

Digital integration trends include IoT-enabled battery tracking for fleet management, improving asset utilization by 22% in large contractor operations. Modular battery ecosystems supporting 100+ compatible tools are becoming industry standard, enhancing cross-platform compatibility and reducing total cost of ownership by 18% for enterprise users.

• In January 2024, Stanley Black & Decker expanded its U.S. battery manufacturing capacity by opening a new 1.2 million-square-foot facility in Tennessee to support its DEWALT cordless platform, strengthening localized lithium-ion pack assembly and improving supply chain efficiency. Source: www.stanleyblackanddecker.com

• In March 2024, Bosch Power Tools introduced the ProCORE18V+ battery series featuring advanced tabless cell technology, delivering up to 71% more power compared to standard 18V batteries while enhancing thermal management performance. Source: www.bosch-professional.com

• In September 2024, Makita announced expansion of its 40Vmax XGT battery production capacity in Japan to meet increasing global demand for high-output cordless systems, enhancing manufacturing automation and efficiency across battery pack assembly lines. Source: www.makita.biz

• In April 2025, Hilti launched its Nuron battery platform updates, integrating enhanced digital connectivity features that allow fleet managers to monitor battery health and usage data in real time, improving productivity tracking across large construction projects. Source: www.hilti.group

The Power Tool Batteries Market Report provides a comprehensive analysis of lithium-ion, nickel-metal hydride, nickel-cadmium, and emerging solid-state battery technologies across voltage categories including 12V, 18V, 20V, 36V, and 40V platforms. The study evaluates performance metrics such as energy density exceeding 250 Wh/kg, charge cycle durability above 1,000 cycles, and ultra-fast charging capabilities reaching 80% within 30 minutes. It covers modular battery ecosystems compatible with up to 100 tools per platform, reflecting industry-wide standardization trends.

The report examines applications across construction, manufacturing, automotive repair, aerospace maintenance, utilities, and residential DIY sectors, where construction accounts for approximately 46% of usage. It analyzes end-user segments including professional contractors (54%), industrial enterprises (27%), and residential users (14%), highlighting procurement behavior and replacement frequency patterns averaging 3–4 batteries annually per professional worker.

Geographically, the scope spans North America (34% share), Europe (27%), Asia-Pacific (29%), South America (6%), and Middle East & Africa (4%), detailing infrastructure expansion, manufacturing output, and regulatory compliance frameworks influencing adoption. Emerging areas such as recyclable battery systems achieving 60% material recovery and AI-enabled battery diagnostics improving lifecycle efficiency by 25% are also assessed. The report further evaluates supply chain investments exceeding USD 8 billion globally in battery manufacturing expansion, digital fleet integration trends, and evolving ESG mandates shaping long-term strategic positioning within the global Power Tool Batteries ecosystem.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

9.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Stanley Black & Decker, Robert Bosch GmbH, Makita Corporation, Milwaukee Tool, Hilti Group, Techtronic Industries Co. Ltd., Snap-on Incorporated, Metabo, Festool GmbH, Panasonic Energy Co., Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |