Reports

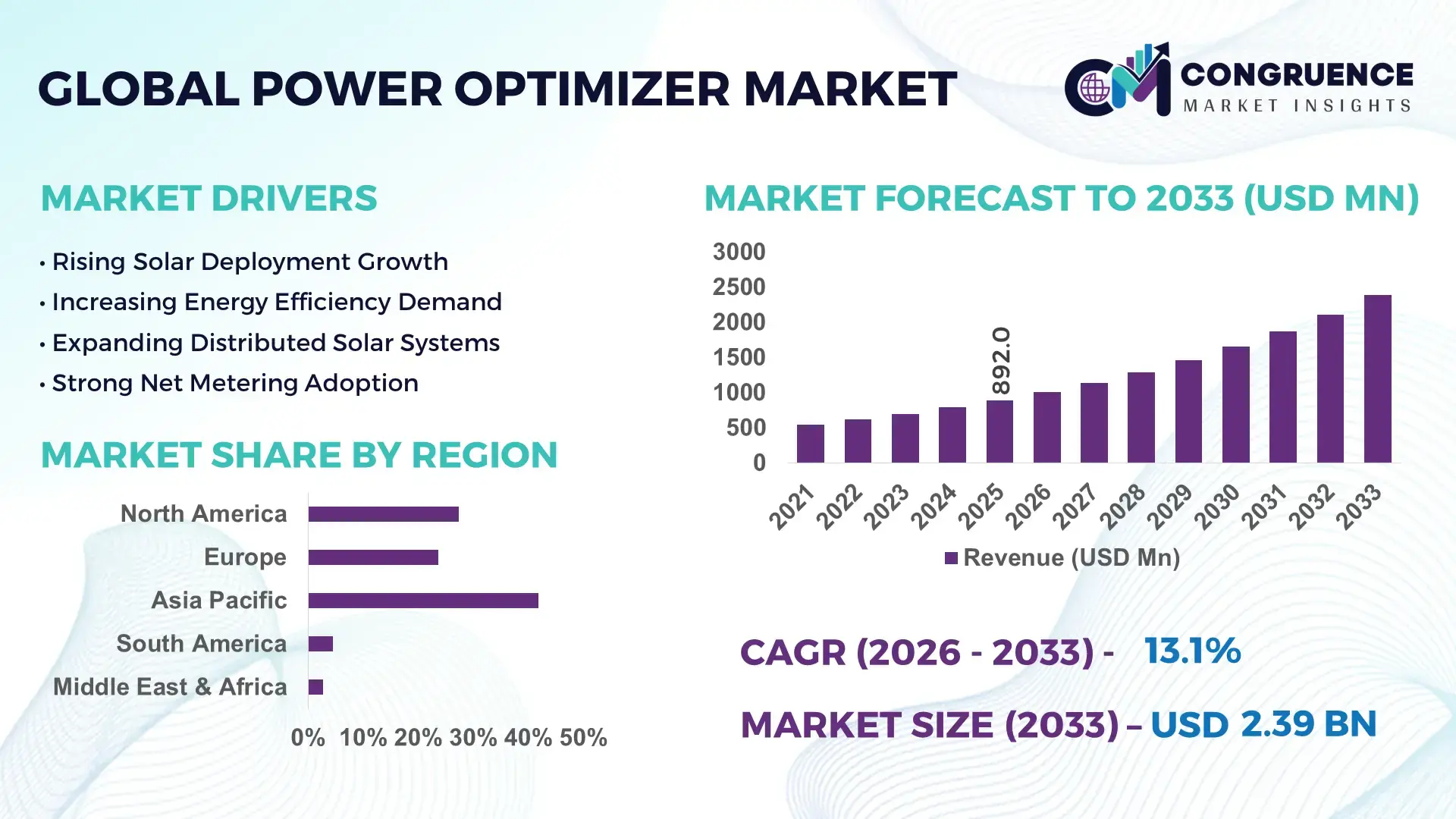

The Global Power Optimizer Market was valued at USD 892.0 Million in 2025 and is anticipated to reach a value of USD 2,389.9 Million by 2033 expanding at a CAGR of 13.11% between 2026 and 2033. Rapid deployment of module-level power electronics in utility-scale solar installations and rising adoption of high-efficiency photovoltaic architectures are accelerating demand for advanced power optimization systems.

China dominates the global power optimizer landscape, accounting for nearly 36% of installed solar manufacturing capacity and over 40% of global photovoltaic module output, supported by investments exceeding USD 50 billion across solar supply chains. In comparison, the United States contributes approximately 14% of annual solar deployments but leads in rapid adoption of module-level optimization technologies, with optimizer penetration exceeding 55% in residential rooftop systems. The energy transition momentum intensified following global supply-chain realignments and clean-energy security initiatives.

For market participants, securing partnerships across solar manufacturing, inverter ecosystems, and distributed energy networks remains critical for sustaining competitive differentiation.

Market Size & Growth: USD 892.0 Million in 2025, projected to reach USD 2,389.9 Million by 2033, driven by high-efficiency solar architecture adoption and module-level energy optimization deployment.

Top Growth Drivers: Rooftop solar installations up 28%, module-level electronics adoption above 35%, and smart energy management integration exceeding 30% across new projects.

Short-Term Forecast: By 2028, solar system energy yield is expected to improve by 8–15% while maintenance interventions decline by nearly 20%.

Emerging Technologies: AI-powered monitoring, advanced MPPT algorithms, and digital twin-based asset optimization are reshaping system performance management.

Regional Leaders: Asia Pacific surpasses USD 950 Million, North America exceeds USD 700 Million, and Europe approaches USD 500 Million, supported by distributed solar expansion and grid modernization.

Consumer/End-User Trends: More than 55% of new residential solar installations in advanced markets incorporate module-level optimization technologies.

Pilot/Case Example: A 2024 commercial solar deployment achieved 12% higher energy output and reduced mismatch losses by over 20% through power optimizer integration.

Competitive Landscape: Market leader controls approximately 40% share, with key participants including SolarEdge, Tigo Energy, Huawei, Sungrow, and Altenergy Power System.

Regulatory & ESG Impact: Distributed solar incentive programs improved project economics by 15–25% while supporting carbon reduction targets and energy resilience goals.

Investment & Funding: More than USD 6 billion in solar electronics and smart energy infrastructure investments supported manufacturing expansion and regional supply-chain diversification.

Innovation & Future Outlook: Bidirectional energy management, optimizer-enabled storage integration, and virtual power plant connectivity are strengthening next-generation energy ecosystems.

Power Optimizer Market demand is increasingly concentrated in residential solar, commercial rooftop installations, utility-scale photovoltaic projects, and distributed energy systems. Recent innovations include AI-enabled performance analytics, module-level diagnostics, and integrated rapid-shutdown capabilities that improve operational visibility. Optimizer-equipped systems can enhance energy harvest by 10–25% under shaded conditions. Ongoing supply-chain localization initiatives and grid modernization programs are also encouraging broader deployment, setting the stage for deeper strategic evaluation.

Power optimizers have become strategically important as solar asset owners prioritize energy yield maximization, grid compliance, and lifecycle performance optimization. The market is increasingly tied to infrastructure modernization, distributed generation expansion, and energy security initiatives. Governments and utilities are accelerating solar deployment targets, while manufacturers are restructuring supply chains to reduce component concentration risks and strengthen local production ecosystems.

Compared with conventional string-based architectures, power optimizer-enabled systems can improve energy production by 10–25% in environments affected by shading, module mismatch, or orientation differences. The United States leads adoption in residential deployments where optimizer penetration exceeds 55%, while China maintains scale advantages through extensive photovoltaic manufacturing infrastructure and large-volume solar installations. Europe continues emphasizing optimizer integration within smart-grid and energy-efficiency initiatives. Over the next two to three years, module-level monitoring adoption is expected to expand significantly as asset operators prioritize predictive maintenance and performance transparency.

Commercial rooftop operators increasingly deploy power optimizers to reduce energy losses and enhance fault detection across distributed assets. In response, technology providers are expanding software capabilities, strengthening inverter partnerships, and investing in intelligent energy management platforms. Organizations that successfully integrate optimization, monitoring, and storage compatibility will strengthen competitive positioning and capture greater value across evolving distributed energy ecosystems.

Distributed solar installations continue to accelerate as businesses and homeowners prioritize energy resilience and system performance. Power optimizers can improve module-level energy generation by 10–25% under partial shading conditions while reducing mismatch losses by nearly 15%. In the United States, optimizer attachment rates exceed 55% in residential rooftop projects, reflecting growing preference for module-level electronics. Simultaneously, commercial facilities are adopting advanced monitoring platforms to improve asset utilization and maintenance efficiency. This shift is reinforced by grid modernization programs and stricter safety requirements, including rapid-shutdown standards. In response, manufacturers are expanding production capacity, forming inverter integration partnerships, and enhancing software-driven diagnostics. A key strategic outcome is the transition from hardware-focused offerings toward integrated energy performance ecosystems.

Despite strong adoption momentum, the market faces structural limitations linked to semiconductor availability, electronics component costs, and manufacturing concentration. Power optimizer systems can increase upfront solar installation costs by 5–12% compared with conventional architectures, creating procurement challenges in price-sensitive markets. More than 70% of several critical photovoltaic electronic components remain concentrated within a limited supplier base, exposing projects to supply-chain disruptions. Geopolitical trade restrictions and logistics bottlenecks have periodically extended equipment lead times by over 20% in major importing countries. These pressures affect deployment schedules, profitability, and procurement planning. To mitigate risks, companies are localizing production, establishing long-term supply agreements, and diversifying sourcing strategies across multiple manufacturing hubs.

The convergence of distributed solar, battery storage, and digital energy management presents a significant opportunity for power optimizer providers. Integrated optimization platforms can improve system visibility by over 30% while reducing operational downtime through predictive analytics. In markets such as Germany and Australia, residential battery attachment rates for new solar systems exceed 35%, creating demand for interoperable module-level power electronics. Emerging AI-enabled monitoring technologies are enhancing fault detection accuracy and improving asset performance management. Companies are expanding R&D investment into bidirectional energy control, virtual power plant connectivity, and advanced optimization algorithms. A notable strategic opportunity lies in combining power optimizers with intelligent energy orchestration platforms capable of supporting grid services, energy trading, and decentralized energy ecosystems.

As deployments expand across residential, commercial, and utility-scale environments, integration complexity is becoming a critical execution challenge. Large distributed solar portfolios can contain thousands of monitored modules, increasing data management requirements by more than 40% compared with traditional system architectures. Cybersecurity risks are also rising as connected energy assets exchange operational data across cloud-based platforms. In Japan and several European markets, stricter cybersecurity and grid interoperability requirements are increasing compliance burdens for technology providers. Workforce shortages in advanced solar electronics installation and diagnostics further complicate deployment consistency. Companies must address these challenges through software standardization, cybersecurity investment, technician training programs, and stronger ecosystem partnerships to maintain long-term competitiveness and operational reliability.

AI-Driven Performance Monitoring Power optimizer deployments are increasingly integrating AI-enabled diagnostics and predictive maintenance platforms, reducing fault-detection time by nearly 40% and lowering service visits by 20–25%. More than 35% of newly installed commercial solar systems now include advanced analytics capabilities. Rising labor shortages across solar operations are accelerating automation adoption, prompting manufacturers to expand software partnerships and embed machine-learning algorithms directly into module-level electronics for faster asset management.

Storage-Ready System Architectures Battery-compatible optimizer configurations have gained significant traction, with storage attachment rates surpassing 35% in several mature solar markets. Installers are redesigning energy workflows around self-consumption and load balancing, improving energy utilization by 15–20%. Regulatory support for distributed energy resources and grid resilience programs is encouraging companies to launch interoperable platforms capable of coordinating solar generation, battery storage, and intelligent energy dispatch through a unified architecture.

Supply-Chain Localization Strategies Following recent geopolitical trade disruptions, solar electronics manufacturers have accelerated regional production expansion, reducing dependence on single-country sourcing models. Component localization initiatives increased by over 30% during the past two years, while procurement lead times improved by nearly 15% in selected markets. A notable shift involves optimizer suppliers securing long-term semiconductor agreements and establishing localized assembly operations to improve delivery reliability and operational continuity.

Commercial Rooftop Optimization Expansion Enterprise solar operators are increasingly deploying power optimizers across warehouses, logistics facilities, and manufacturing sites where module mismatch losses can exceed 10%. Optimizer penetration in large commercial rooftop projects has risen by approximately 25%, supported by stricter energy-efficiency targets and digital asset management requirements. Companies are responding through turnkey deployment models, inverter ecosystem collaborations, and remote monitoring capabilities that improve system uptime while reducing operational complexity.

Module-level power optimizers currently represent the leading segment due to their superior energy harvesting capability, granular monitoring functionality, and compatibility with modern photovoltaic systems. Their ability to mitigate mismatch losses, optimize individual panel performance, and support rapid-shutdown requirements has strengthened adoption across residential and commercial installations. Nearly 55% of advanced rooftop solar projects now incorporate module-level optimization technologies, while performance improvements ranging from 10–25% continue to support deployment decisions. Manufacturers are prioritizing software integration, advanced diagnostics, and inverter interoperability to reinforce competitive differentiation. The fastest-growing type is expected to be intelligent optimizer systems equipped with AI-enabled monitoring and predictive analytics capabilities. These solutions are gaining traction as asset owners seek improved operational visibility and maintenance efficiency. Traditional optimization products remain relevant in cost-sensitive installations, while emerging smart configurations increasingly attract investment due to their data-driven performance advantages. More than 30% of newly launched optimizer products now include enhanced communication and monitoring features. Companies are expanding product portfolios, forming technology alliances, and increasing R&D spending to address shifting customer requirements and strengthen lifecycle value propositions.

Residential solar installations remain the leading application segment due to high rooftop deployment volumes, increasing consumer preference for energy independence, and strong demand for panel-level performance monitoring. Optimizer penetration exceeds 55% in several developed residential markets, supported by rapid-shutdown compliance requirements and growing adoption of smart energy management systems. Homeowners increasingly prioritize visibility into individual module performance, prompting manufacturers to integrate advanced monitoring platforms and user-friendly analytics tools into optimization solutions. Commercial and industrial solar applications represent the fastest-growing segment as enterprises focus on reducing energy costs and improving asset efficiency. Large rooftop facilities can experience mismatch losses exceeding 10%, making optimizer deployment operationally attractive. Utility-scale installations continue expanding selectively where terrain conditions, module orientation differences, or performance monitoring requirements justify module-level control. More than 25% of newly commissioned commercial rooftop projects now integrate optimizer technology. Companies are responding through scalable deployment models, remote monitoring solutions, and strategic partnerships with EPC contractors to strengthen adoption across large energy-intensive facilities.

Utility operators constitute the dominant end-user segment due to their large-scale solar asset portfolios, performance optimization requirements, and increasing focus on grid reliability. Utility projects account for a substantial share of optimizer-enabled deployments where energy yield improvements and monitoring precision directly affect operational performance. Performance optimization can improve electricity generation by 10–20% under challenging site conditions, encouraging utilities to incorporate advanced module-level technologies into selected projects. Vendors continue developing utility-focused solutions featuring centralized monitoring, predictive diagnostics, and enhanced grid integration capabilities. Commercial and industrial organizations represent the fastest-growing end-user category as energy-intensive businesses pursue operational efficiency and sustainability objectives. Manufacturing facilities, logistics centers, and data-driven enterprises increasingly deploy optimized solar systems to reduce operating costs and improve energy resilience. Residential consumers remain an important buyer group, particularly in markets emphasizing self-generation and energy independence. More than 35% of enterprise solar procurement programs now evaluate advanced monitoring functionality as a core purchasing criterion. Companies are strengthening channel partnerships, introducing customized offerings, and expanding service ecosystems to capture emerging demand across diverse customer categories.

Asia-Pacific accounted for the largest market share at 41.8% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 14.2% between 2026 and 2033.

North America represents approximately 27.4% of global market demand, supported by strong residential solar adoption, commercial rooftop modernization, and increasing deployment of intelligent energy systems. The region has emerged as a major adopter of module-level power electronics, with optimizer penetration exceeding 55% in new residential installations across several states. Utility operators are increasingly integrating panel-level monitoring capabilities to improve asset visibility and operational efficiency. Recent grid modernization investments and distributed energy resource programs continue supporting optimizer deployment. Technology providers are strengthening partnerships with EPC contractors and inverter manufacturers to streamline installation workflows and enhance long-term system performance management.

United States Market Outlook: The United States remains the dominant market due to its extensive rooftop solar ecosystem, advanced installer network, and strong adoption of module-level optimization technologies. More than half of newly installed residential photovoltaic systems incorporate power optimizers to improve energy harvest and comply with rapid-shutdown requirements. Utility operators are increasingly utilizing advanced monitoring platforms to enhance system diagnostics and reduce maintenance costs. Strong investment activity in distributed energy infrastructure and intelligent grid technologies continues reinforcing long-term deployment momentum.

Europe accounts for nearly 23.6% of global market activity, supported by energy transition initiatives, decentralized power generation, and stringent energy-efficiency objectives. The region is witnessing increasing integration of optimizer technologies within residential and commercial solar systems to maximize output from limited rooftop space. More than 40% of new distributed solar projects in several leading markets now include advanced monitoring and optimization functionality. Regulatory emphasis on energy resilience and grid flexibility is encouraging broader deployment of intelligent photovoltaic infrastructure. Companies are responding through localized service networks, software-enhanced optimization platforms, and strategic collaborations focused on smart energy management.

Germany Market Outlook: Germany maintains a leading position through its mature solar infrastructure, advanced energy-transition framework, and widespread adoption of distributed generation technologies. Residential and commercial solar operators increasingly prioritize module-level performance optimization to improve self-consumption rates and maximize rooftop productivity. Battery-integrated solar installations continue expanding across the country, strengthening demand for interoperable optimization technologies. Strong engineering expertise, established installer networks, and ongoing grid modernization efforts position Germany as a key innovation center within the European power optimizer ecosystem.

Asia-Pacific commands the largest share of the market at approximately 41.8%, supported by extensive photovoltaic manufacturing capacity, large-scale solar deployment, and expanding distributed generation investments. China, India, Japan, and Australia collectively account for a significant portion of global solar installations, creating substantial demand for optimization technologies. More than 60% of global photovoltaic module production originates from the region, strengthening supply-chain advantages and accelerating technology adoption. Large utility-scale projects increasingly utilize optimizer solutions in complex deployment environments where performance consistency is critical. Manufacturers continue expanding production facilities and investing in advanced power electronics capabilities to support evolving market requirements.

China Market Outlook: China remains the most strategically important market due to its dominant photovoltaic manufacturing base and large-scale solar deployment activity. The country contributes over 40% of global solar module output and continues investing heavily in smart energy infrastructure. Utility developers are increasingly incorporating advanced monitoring and optimization technologies to improve generation efficiency across expansive solar assets. Strong domestic supply chains, extensive manufacturing expertise, and sustained renewable-energy investment provide China with a significant competitive advantage in the power optimizer value chain.

South America accounts for an estimated 4.5% of global market demand and is benefiting from increasing commercial solar adoption, favorable solar irradiation conditions, and rising energy cost pressures. Businesses across mining, agriculture, and industrial sectors are investing in photovoltaic systems to improve operational efficiency and energy resilience. Optimizer deployment is gaining traction within commercial installations where shading, environmental variability, and system monitoring requirements influence performance outcomes. Infrastructure limitations and financing constraints continue affecting deployment speed in some markets, yet solar investment pipelines remain active. Technology suppliers are expanding distributor networks and local partnerships to strengthen market accessibility.

Brazil Market Outlook: Brazil serves as the region’s primary growth engine due to its expanding distributed solar sector and increasing commercial photovoltaic installations. Industrial facilities and agricultural enterprises are adopting advanced optimization technologies to maximize generation efficiency under diverse environmental conditions. Distributed generation capacity continues to expand rapidly, supported by favorable solar resources and growing electricity demand. Local developers are increasingly prioritizing monitoring-enabled solutions that improve operational visibility and enhance long-term system productivity across decentralized energy assets.

The Middle East & Africa region represents approximately 2.7% of global market activity, driven by large-scale renewable-energy projects, infrastructure diversification programs, and national energy-transition strategies. Utility operators are increasingly deploying advanced solar technologies to optimize electricity generation under high-temperature operating conditions. Several countries are investing heavily in solar parks and grid modernization initiatives, creating opportunities for module-level performance optimization solutions. Deployment remains concentrated within major infrastructure programs, while emerging distributed solar projects are gradually expanding market participation. Companies are pursuing regional partnerships and technology localization strategies to strengthen long-term competitiveness.

Saudi Arabia Market Outlook: Saudi Arabia is emerging as the region’s most influential market through extensive renewable-energy investments and ambitious infrastructure development programs. Large utility-scale solar projects are creating demand for advanced performance optimization technologies capable of operating efficiently in harsh environmental conditions. National diversification initiatives continue accelerating renewable-energy deployment, while grid modernization investments support integration of intelligent energy systems. Strategic partnerships between global technology providers and local stakeholders are strengthening project execution capabilities and supporting broader adoption of advanced solar electronics solutions.

The Power Optimizer Market is led by technology-focused global players including SolarEdge Technologies, Tigo Energy, Huawei Digital Power, Altenergy Power System (APsystems), and Sungrow. Competition primarily occurs between global technology leaders and regional solar electronics suppliers, while integrated inverter-optimizer vendors compete directly against standalone optimization specialists. The top five players collectively control approximately 68–72% of market activity, reflecting a moderately concentrated structure. Competition centers on energy yield improvement, software intelligence, safety compliance, and ecosystem integration rather than price alone. Advanced optimizer platforms deliver 10–25% higher energy harvest in challenging conditions, while AI-enabled monitoring can reduce fault-detection time by nearly 40%. Leading companies are expanding through software-driven innovation, installer partnerships, manufacturing localization, and vertical integration across inverters, storage, and energy management platforms. The competitive landscape is shifting toward intelligent energy ecosystems, where monitoring, storage compatibility, and grid services create differentiation. High certification requirements, installer relationships, and product reliability remain major entry barriers. Winning requires superior system performance, integrated software capabilities, scalable supply chains, and strong channel partnerships.

Tigo Energy

Huawei Digital Power

Sungrow Power Supply

Altenergy Power System (APsystems)

Fronius International

SMA Solar Technology

Ginlong Technologies (Solis)

GoodWe Technologies

Enphase Energy

Fimer

Growatt

Hoymiles

Power optimizer technology is rapidly evolving from basic maximum power point tracking toward intelligent module-level energy management. Current deployments increasingly integrate advanced MPPT algorithms, panel-level monitoring, and rapid-shutdown functionality. Modern optimizer-enabled systems improve energy yield by 10–25% under shading and mismatch conditions while reducing diagnostic time by nearly 40%. More than 55% of new residential solar installations in advanced markets now incorporate module-level optimization capabilities, creating measurable operational advantages for installers and asset owners.

Emerging technologies focus on AI-enabled predictive maintenance, digital twin-based performance analytics, and storage-ready optimization platforms. Compared with conventional string-based architectures, intelligent optimizer systems can improve fault identification speed by over 30% while enhancing asset visibility across thousands of modules. Technology leaders such as SolarEdge, Huawei, and Tigo benefit from integrated software ecosystems that combine optimization, monitoring, storage coordination, and energy management within a single platform. This integration strengthens customer retention and increases lifecycle value.

Between 2026 and 2028, disruptive innovation will center on virtual power plant connectivity, bidirectional energy control, and autonomous energy orchestration. Optimizer platforms integrated with battery systems can improve self-consumption efficiency by 15–20%. Companies investing now in AI-driven diagnostics, interoperability standards, and grid-interactive functionality will secure stronger competitive positioning as distributed energy networks become increasingly intelligent and interconnected.

June 2024 – Huawei Digital Power launched its next-generation FusionSolar Smart PV+ESS platform featuring integrated optimizers, digitalization, and grid-forming capabilities. The new intelligent cooling architecture reduced auxiliary losses by 50% while strengthening utility-scale renewable integration and operational efficiency. Source: www.solar.huawei.com

April 2025 – SolarEdge Technologies introduced its ONE Controller solution for Germany's residential solar market, enabling integration with third-party EV chargers and heat pumps under new regulatory requirements. The platform expands controllable energy load management and strengthens smart-home energy optimization capabilities.

January 2026 – Tigo Energy released the next-generation GO Battery platform integrated with its optimization ecosystem. The system enables installations twice as fast while requiring 40% less space, improving installer productivity and supporting broader distributed energy resource deployment.

March 2026 – Tigo Energy and CELTEC established a strategic distribution partnership across Central America and the Caribbean to expand access to optimizer and rapid-shutdown technologies. The initiative strengthens regulatory compliance capabilities and accelerates deployment of safer distributed solar infrastructure.

The report provides comprehensive analysis of market performance, technology evolution, competitive dynamics, and deployment trends across the global power optimizer ecosystem. Coverage spans major product types, key application areas, and diverse end-user segments, including residential, commercial, industrial, and utility-scale solar installations. Regional assessment covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, highlighting adoption patterns, manufacturing concentration, and infrastructure development. The study evaluates advanced technologies including AI-enabled monitoring, module-level power electronics, storage integration, predictive diagnostics, and intelligent energy management platforms.

The report examines market participation across leading technology providers, inverter manufacturers, optimization specialists, and emerging energy software companies. More than 55% optimizer penetration in advanced residential solar markets and increasing adoption across commercial installations are assessed to identify strategic opportunities. Insights support investment planning, product development, geographic expansion, partnership evaluation, supply-chain optimization, and competitive positioning while outlining key market shifts expected to influence deployment priorities and technology adoption between 2026 and 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 892.0 Million |

| Market Revenue (2033) | USD 2,389.9 Million |

| CAGR (2026–2033) | 13.11% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | SolarEdge Technologies; Tigo Energy; Huawei Digital Power; Sungrow Power Supply; Altenergy Power System (APsystems); Fronius International; SMA Solar Technology; Ginlong Technologies (Solis); GoodWe Technologies; Enphase Energy; Fimer; Growatt; Hoymiles |

| Customization & Pricing | Available on Request (10% Customization Free) |