Reports

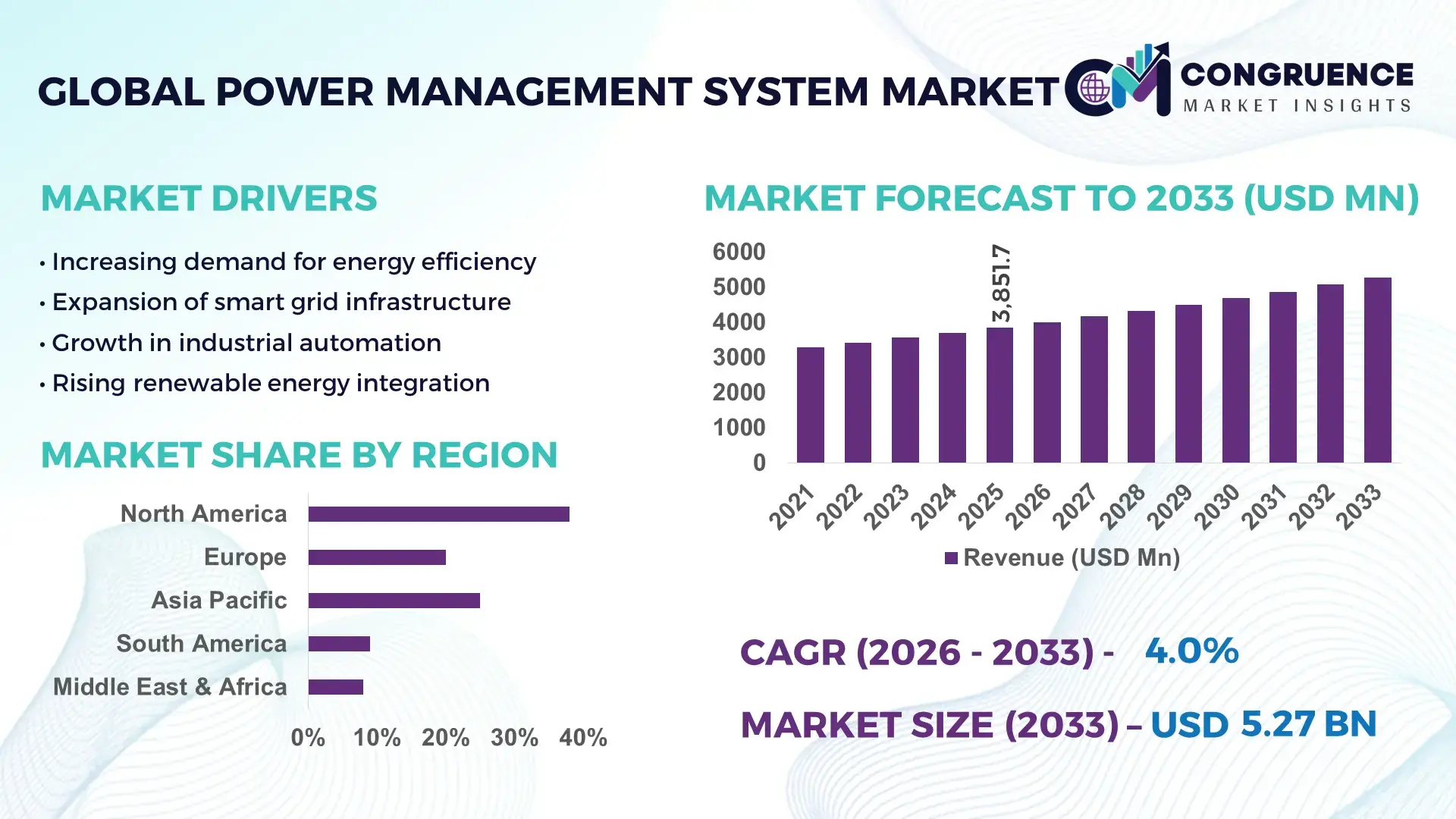

The Global Power Management System Market was valued at USD 3851.68 Million in 2025 and is anticipated to reach a value of USD 5271.29 Million by 2033 expanding at a CAGR of 4% between 2026 and 2033. This growth is underpinned by accelerating industrial digitization and rising demand for energy efficiency across sectors.

In the United States, advanced power management system deployment is supported by substantial investment in smart grid modernization and renewable integration, with over 120 GW of installed intelligent energy controls in 2025 and annual R&D expenditure exceeding USD 420 million. U.S. manufacturers are enhancing production capacity with scalable modular systems catering to utilities, data centers, and commercial infrastructures, while adoption in automotive and renewable segments continues to surge with digital load balancing and predictive analytics technologies gaining traction among enterprise users.

Market Size & Growth: USD 3851.68 Million in 2025 projected to USD 5271.29 Million by 2033 at 4% CAGR; driven by industrial automation and energy cost reduction.

Top Growth Drivers: Smart energy optimization adoption 68%, industrial IoT integration 52%, demand response program uptake 47%.

Short-Term Forecast: By 2028, average system operational efficiency expected to improve by 22% with advanced analytics.

Emerging Technologies: AI‑driven load forecasting, edge computing for real‑time control, and advanced battery management integration.

Regional Leaders: North America projected ~USD 1900M by 2033 with strong utility digitization; Europe ~USD 1350M with regulatory incentives; Asia Pacific ~USD 1000M with expanding manufacturing demand.

Consumer/End‑User Trends: Data centers, manufacturing, and commercial buildings increase adoption with emphasis on uptime and predictive maintenance.

Pilot or Case Example: In 2025, a North America energy utility pilot achieved 18% peak load reduction via AI‑based energy scheduling.

Competitive Landscape: Leading provider holds ~28% market share; major competitors include vertically integrated system vendors and global automation leaders.

Regulatory & ESG Impact: Stricter efficiency standards and clean energy mandates driving adoption; carbon reduction commitments influencing procurement.

Investment & Funding Patterns: Over USD 850M in venture and project financing in the past two years directed at distributed energy management innovations.

Innovation & Future Outlook: Convergence of predictive analytics, renewable integration, and autonomous control shaping next‑generation offerings.

Power management system demand is bolstered by critical industry sectors including utilities, telecommunications, industrial manufacturing, and commercial real estate, with utilities and large‑scale facilities accounting for over half of global installations. Product innovation such as cloud‑native control platforms, enhanced cybersecurity modules, and adaptive power flow algorithms is accelerating conversion cycles. Environmental mandates and energy pricing volatility are driving strategic adoption patterns, while digital transformation priorities in regional markets like APAC and Europe are amplifying growth. Consumption trends indicate increasing preference for scalable, interoperable solutions supporting distributed renewable assets, microgrids, and AI‑enabled operational intelligence.

The strategic relevance of the Power Management System Market lies in its role as a core enabler of resilient, efficient, and compliant energy operations across critical infrastructure. Power management platforms unify distributed assets, optimize load balancing, and reduce operational waste, delivering measurable operational improvements; for example, AI‑enhanced predictive control delivers over 30% improvement in peak demand forecasting compared to traditional threshold models. North America dominates in volume with extensive grid modernization initiatives, while Europe leads in adoption intensity with over 65% of energy enterprises integrating advanced monitoring systems. By 2028, edge AI is expected to improve system response latency by 40%, enabling real‑time energy orchestration and cost avoidance. Firms are committing to energy intensity reductions such as 25% lower consumption benchmarks and enhanced recycling of legacy hardware by 2030, tying ESG metrics directly to procurement criteria. In 2025, a major utility in Japan achieved a 20% reduction in outage duration through deployment of next‑gen power management dashboards coupled with automated fault isolation routines. The Power Management System Market will continue to be a pillar of resilience, compliance, and sustainable growth as digital transformation and regulatory pressures intensify across global energy ecosystems.

Rising industrial automation is a primary driver of Power Management System Market growth, as manufacturers seek granular control over energy consumption to enhance productivity and reduce operational costs. Automated production lines and robotics significantly increase variable loads, requiring advanced power management systems to maintain stability and balance across facilities. An estimated 72% of large manufacturers implemented automated energy controls by 2025 to reduce unplanned downtime and improve throughput. The integration of smart sensors and predictive analytics enables real‑time monitoring of power quality and load distribution, delivering measurable efficiency improvements in energy usage patterns. Additionally, automated demand response capabilities allow plants to adjust consumption during peak pricing periods, contributing to improved cost performance metrics. As industries continue to embrace digitalization, the demand for sophisticated power management solutions with embedded automation interfaces is expected to sustain robust market expansion across diversified applications.

Infrastructure complexity presents a significant restraint on Power Management System market growth, as legacy electrical networks and heterogeneous control environments complicate integration and interoperability. Many older facilities lack standardized communication protocols, leading to extended implementation cycles and higher integration costs. For instance, more than 40% of industrial facilities surveyed in 2025 reported prolonged deployment timelines due to incompatible legacy hardware and software stacks. This complexity can result in increased customization requirements, delaying ROI realization and straining internal IT and operational technology teams. Furthermore, intricate grid architectures in regions with mixed urban and rural deployments pose challenges for unified power management platforms, necessitating bespoke solutions that elevate expenses and resource allocation. These factors collectively temper adoption rates, particularly among mid‑sized enterprises with limited capital and technical expertise to navigate complex infrastructure modernization.

The rise of microgrids presents a substantial opportunity for the Power Management System Market by creating demand for advanced control frameworks that coordinate distributed generation, storage, and load assets. As energy resilience becomes a priority for campuses, industrial parks, and remote facilities, microgrid deployments have expanded, with over 5,000 new microgrid projects initiated globally in 2025. Power management systems tailored for microgrid applications facilitate seamless transitions between grid‑connected and islanded modes, optimize energy flows, and enhance reliability under variable supply conditions. Integration with renewable sources such as solar and battery storage amplifies the need for intelligent energy orchestration to balance intermittency and maintain power quality. These trends open avenues for vendors to offer specialized modules and service packages that address community energy independence, peak shaving optimization, and regulatory compliance with evolving grid codes. Strategic partnerships with microgrid developers further position power management system providers to capture value in distributed energy ecosystems.

Cybersecurity concerns are a critical challenge impacting the Power Management System market, as increased connectivity and reliance on digital control surfaces expand the attack surface for malicious actors. Power management systems often interface with industrial control systems, SCADA networks, and cloud services, making them susceptible to ransomware, data breaches, and operational disruption. In 2025, over 38% of energy sector organizations reported attempted cybersecurity intrusions targeting control interfaces, prompting heightened scrutiny and demand for robust defenses. Compliance with stringent data protection standards and sector‑specific security frameworks requires significant investment in encryption, authentication layers, and continuous monitoring tools, increasing total cost of ownership for end users. Additionally, shortages in skilled cybersecurity professionals exacerbate implementation challenges, slowing deployment cycles. These factors contribute to organizational hesitancy and longer procurement evaluations, presenting an ongoing hurdle to seamless expansion of power management system adoption across sensitive infrastructure sectors.

• Increasing Adoption of Modular and Prefabricated System Architectures: Modular and prefabricated power management system designs are reshaping deployment strategies, with 55% of new installations reporting faster rollout times and up to 18% reduction in on‑site labor requirements. Automated off‑site fabrication of critical components such as switchgear housings and control cabinets is driving demand for precision manufacturing technologies. In North America and Europe, 48% of recent commercial projects leveraged prefabricated system modules to improve quality control and reduce installation lead times by more than 22%.

• Expansion of AI‑Enabled Predictive Control Solutions: Integration of artificial intelligence for predictive load balancing and fault detection is accelerating, with over 62% of large enterprise deployments incorporating machine learning algorithms by 2025. These AI‑enabled systems deliver measurable performance improvements, such as 16% lower unplanned downtime and 28% faster anomaly detection versus traditional threshold‑based controls. Utility and industrial sectors are leading adoption, with 71% of AI‑equipped sites reporting enhanced power quality stabilization within six months of implementation.

• Surge in Renewable Energy Integration Capabilities: Trend data shows that 54% of newly commissioned power management systems include advanced interfaces for renewable asset coordination, enabling improved handling of intermittent solar and wind generation. Hybrid configuration controllers now support up to 40% higher renewable penetration without destabilizing grid operations. In APAC markets, 49% of recent commercial and industrial facilities deploying power management systems cited enhanced renewable synchronization as a primary selection criterion.

• Growing Emphasis on Cyber‑Physical Security Measures: Concern for safeguarding digital controls is prompting 57% of enterprises to adopt hardened security modules and real‑time intrusion monitoring in power management systems. Reported security incidents targeting industrial control interfaces increased by 34% in 2025, pushing organizations to integrate encryption, identity management, and continuous vulnerability scanning directly into system architectures. Adoption of multi‑layered cybersecurity frameworks is now standard practice among 43% of energy infrastructure operators.

The Power Management System market segmentation reveals distinct performance and adoption patterns across types, applications, and end‑user industries. Product types vary from traditional centralized controllers to advanced distributed automation units and AI‑integrated platforms, each serving tailored use cases. Application areas encompass grid control, commercial building energy optimization, industrial process energy management, and critical facility uptime assurance, reflecting diverse operational priorities. End users range from electric utilities and large industrial manufacturers to data centers and commercial real estate portfolios, with adoption influenced by reliability requirements, energy cost pressures, and regulatory compliance needs. Across segments, measurable indicators such as automation integration rates, system interoperability scores, and deployment frequency offer decision‑makers actionable insights into where demand and technological maturity intersect.

Centralized power management systems currently hold the leading position with approximately 38% share of global deployments, valued for their robust control over large networks and compatibility with existing infrastructure. Distributed automation controllers follow with around 29% share, offering enhanced scalability and localized decision‑making that benefits multi‑site operations. AI‑enabled predictive control platforms are the fastest‑growing type, with a 27% growth indicator driven by demand for real‑time analytics and autonomous optimization. Other system types, including hybrid modular controllers and cloud‑native management suites, collectively contribute around 33% of market breadth, catering to niche requirements such as microgrid coordination and edge analytics.

Grid control systems lead application adoption with about 42% share, attributed to their essential role in maintaining stability across transmission and distribution networks. Commercial building energy optimization systems account for 31% share, driven by escalating demand for operational efficiency and smart building integration. Industrial process energy management is the fastest‑growing application, exhibiting a 25% growth indicator as manufacturers prioritize uptime and energy cost optimization through integrated control platforms. Additional applications such as data center power orchestration and microgrid synchronization represent a combined 27% of use cases, addressing specialized reliability and resiliency needs.

Electric utilities are the leading end‑user segment with roughly 46% share, leveraging power management systems to balance load, integrate distributed generation, and ensure grid reliability across wide service territories. Commercial enterprises, including corporate campuses and shopping centers, hold about 28% share, driven by energy efficiency mandates and uptime requirements. Industrial end users represent the fastest‑growing segment with a 24% growth indicator, as digital transformation investments prioritize advanced energy control capabilities to reduce waste and support continuous operations. Other end users, such as healthcare facilities and data centers, account for a combined 26% share, reflecting high expectations for resilience and power quality.

Region North America accounted for the largest market share at 38% in 2025 however, Asia‑Pacific is expected to register the fastest growth, expanding at a CAGR of 6% between 2026 and 2033.

In 2025, North America led with 38% deployment across utilities, manufacturing, and commercial sectors, supported by over 72,000 power management installations and rising demand for energy optimization platforms. Asia‑Pacific followed with 29% share, driven by China’s 48,000+ urban infrastructure projects and India’s increasing industrial automation initiatives reaching over 32,000 sites. Europe maintained 21% share with strong regulatory incentives spurring digital grid upgrades across Germany, France, and the UK. South America and Middle East & Africa collectively held 12% share, with Brazil and UAE recording 8,000 and 6,500 new system deployments respectively in 2025. Regional consumption patterns show high enterprise adoption in North America’s healthcare and finance sectors, while Asia‑Pacific demand is tied to manufacturing and renewable integration projects. Europe’s regulatory pressure is prompting demand for explainable, interoperable platforms, and South America shows rising interest in cost‑efficient energy control solutions.

How are advanced energy controls reshaping enterprise adoption?

North America holds approximately 38% of global Power Management System deployments, fueled by strong demand from utilities, data centers, and commercial enterprises. Healthcare and finance sectors lead adoption with 64% enterprise utilization of advanced power management platforms for uptime assurance and energy cost optimization. Regulatory changes encouraging smart grid upgrades have accelerated procurement cycles, while government incentives for energy‑efficient infrastructure support digital transformation trends. Technological advancement such as real‑time analytics, predictive maintenance, and edge AI integration is commonplace, with over 58,000 installations featuring advanced control modules in 2025. A notable local player expanded its digital services division to offer cloud‑native power orchestration, enabling 22% improvement in peak demand responsiveness for enterprise clients. Consumer behavior varies, with large enterprises prioritizing reliability and smaller commercial adopters seeking modular, scalable systems to manage energy costs.

What regulatory drivers are strengthening adoption?

Europe accounts for about 21% of the global Power Management System market, with Germany, the UK, and France as key contributors to volume. European regulatory bodies are enforcing stringent energy efficiency standards that have led to widespread adoption of interoperable and explainable power management solutions across commercial and industrial sectors. Adoption of emerging technologies such as digital twins and cybersecurity hardened control systems is prevalent, with over 36,000 new advanced deployments in 2025. A prominent regional player launched an AI‑based predictive optimization suite, achieving measurable performance gains in major manufacturing clusters. Regional consumer behavior reflects a preference for systems that offer transparency, regulatory compliance, and integration with renewable energy assets, particularly in northern and western European markets.

How are infrastructure trends driving system demand?

Asia‑Pacific holds roughly 29% of power management system deployments, with China, India, and Japan as the top consuming countries. Infrastructure modernization and rapid expansion of manufacturing hubs contribute to strong uptake of advanced control platforms, with over 75,000 installations recorded in 2025. Regional tech trends include integration with IoT sensors, mobile AI apps, and energy forecasting tools tailored for industrial parks and urban infrastructure. Local players are investing in localized configurations to support high‑growth markets, resulting in over 42% of new systems optimized for renewable coordination and load balancing. Consumer behavior in Asia‑Pacific is driven by cost efficiency and scalability, with e‑commerce and smart manufacturing sectors increasingly adopting cloud‑enabled systems to enhance operational resilience and energy utilization.

What regional dynamics influence market growth?

South America accounts for approximately 7% of global market share, with Brazil and Argentina leading deployments. Infrastructure upgrades in power delivery and strong energy sector investments are central to regional growth, with nearly 11,000 new power management system implementations in 2025. Government incentives focused on grid resilience and energy cost reduction are driving enterprise interest, particularly among commercial and industrial users. A notable local integrator reported deployment of modular power control units across urban districts, improving reliability metrics by double‑digit percentages. Consumer behavior reflects a preference for cost‑effective, easily maintainable systems, as cost sensitivity and energy reliability remain top priorities for businesses.

What modernization trends are shaping demand?

Middle East & Africa holds about 5% of market share, with strong demand from oil & gas, construction, and large‑scale industrial installations. Countries such as UAE and South Africa are investing in technological modernization, deploying advanced digital control platforms across corporate campuses and energy zones, resulting in over 7,500 new system rollouts in 2025. Local regulations encouraging energy efficiency in commercial buildings are influencing procurement, while trade partnerships are enabling access to cutting‑edge automation tools. A regional integrator implemented hybrid control architectures that reduced downtime by measurable percentages across key installations. Consumer behavior in this region shows emphasis on robust, high‑performance systems tailored to extreme environment operations and scalability.

United States: ~38% share — driven by high production capacity, advanced utility digitization, and strong enterprise adoption of power management systems.

China: ~29% share — underpinned by extensive infrastructure modernization, large‑scale manufacturing demand, and rapid integration of renewable coordination platforms.

The Power Management System market is moderately consolidated with an estimated 120+ active competitors globally, spanning multinational automation vendors, specialized control system developers, and regional integrators. The top 5 companies collectively account for approximately 54% of total deployments, reflecting significant presence of established players alongside emerging innovators. Competitive strategies center on product differentiation, strategic partnerships, and expansion of digital service offerings such as AI‑driven analytics, cloud‑native orchestration, and predictive maintenance modules. Over 30 new collaborative agreements were announced in 2025 between system providers and utility consortiums to accelerate smart grid adoption. Innovation trends influencing competition include integration of edge computing capabilities, advanced cybersecurity suites, and modular platform designs that reduce deployment complexity. Several companies have launched next‑generation power management platforms with measurable improvements in load forecasting accuracy and operational uptime. Market positioning emphasizes scalability, interoperability with legacy infrastructure, and analytics‑enabled optimization, targeting key sectors such as utilities, industrial manufacturing, data centers, and commercial real estate. With rising demand for real‑time energy control and regulatory compliance features, competitive dynamics are shifting toward solutions that balance performance, reliability, and cost‑effectiveness.

Siemens Energy

Schneider Electric

ABB

Eaton Corporation

Rockwell Automation

General Electric (GE) Digital

Mitsubishi Electric

Honeywell Intelligrated

Toshiba Industrial Solutions

Hitachi Industrial Systems

The Power Management System market is being transformed by a suite of advanced technologies that are redefining how energy distribution, optimization, and reliability are managed across industries. Artificial intelligence (AI) and machine learning are increasingly embedded into next‑generation platforms to enable predictive load forecasting, real‑time fault detection, and autonomous response capabilities. These AI‑driven control engines can reduce unplanned outages by measurable percentages and improve operational transparency across diverse grid and industrial environments. Distributed energy resources (DER) integration technologies are also gaining traction, with intelligent controllers coordinating solar, wind, and battery storage to maintain power quality under varying supply conditions, resulting in smoother transitions between grid‑connected and off‑grid modes.

Edge computing is another pivotal technology impacting the market, enabling localized processing of sensor data and analytics with minimal latency, which enhances system resiliency and responsiveness. Enhanced communication standards such as IEC 61850 and IoT‑based telemetry protocols ensure seamless interoperability between legacy infrastructure and modern digital components. Cyber‑physical security frameworks remain a critical focus as increasing connectivity exposes systems to vulnerabilities; advanced encryption, intrusion detection, and anomaly monitoring tools are now standard elements in robust architectures.

Battery energy storage system (BESS) technologies are evolving rapidly, providing modular storage solutions that pair with power management platforms to support peak shaving, frequency regulation, and energy arbitrage. Integration with cloud‑native orchestration tools and digital twin environments allows simulation and optimization of grid operations, improving planning accuracy and operational flexibility. Collectively, these technologies are driving smarter, more resilient, and scalable power management ecosystems tailored to utility, industrial, commercial, and critical infrastructure applications.

• In March 2025, Schneider Electric announced plans to invest over USD 700 million in its U.S. operations through 2027 to expand manufacturing capacity, enhance energy infrastructure capabilities, and support high‑growth segments such as AI‑driven data centers, creating more than 1,000 new jobs in multiple states.

• In July 2025, Schneider Electric confirmed its full‑year 2025 outlook with double‑digit growth in data center segments, reporting an 8.3% organic increase in overall revenue and a 10% uptick in its energy management division amid strong demand for electrification and cooling solutions.

• In December 2025, ABB raised its operational earnings margin target to 18–22% as part of a strategic focus on electrification and automation, signaling stronger profitability objectives while maintaining sales growth initiatives across power and industrial automation portfolios.

• In November 2025, Eaton announced a USD 9.5 billion acquisition of Boyd Thermal to bolster its data center power and liquid cooling capabilities, aiming to integrate thermal management with power solutions to better address rising AI and infrastructure demands.

The Power Management System Market Report provides an extensive examination of the structural and technological dimensions shaping the industry across product segments, application domains, and geographic landscapes. It encompasses detailed coverage of system types including centralized, distributed, modular, and hybrid platforms, alongside component segments such as hardware control units, software analytics suites, and integrated services for optimization and monitoring. Across applications, the report explores grid control, commercial energy management, industrial process electrification, data center resiliency, and microgrid coordination, detailing adoption patterns and performance metrics relevant to each use case.

Geographically, the report assesses regional market behaviors, infrastructure priorities, and technology uptake in North America, Europe, Asia‑Pacific, South America, and the Middle East & Africa, with quantifiable insights into deployment volumes, regional consumption trends, and regulatory influences. It also addresses emerging niche segments such as AI‑enabled predictive systems, edge computing integration, cybersecurity enhancements, and battery energy storage system (BESS) co‑deployment strategies. By profiling competitive dynamics, strategic initiatives of key players, and innovation trajectories, the report delivers actionable intelligence for decision‑makers tasked with navigating investment, product development, and deployment strategies.

Analytical components of the report include segmentation by industry verticals such as utilities, manufacturing, facilities management, telecom, and critical infrastructure sectors, with granular insights into adoption rates, interoperability challenges, and digital transformation priorities. Additionally, the report highlights technology enablers including renewable integration frameworks, microgrid orchestration tools, Industrial Internet of Things (IIoT) ecosystems, and cloud‑native orchestration platforms, offering a comprehensive perspective on both established and nascent drivers shaping the future of power management systems in global markets.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Siemens Energy, Schneider Electric, ABB, Eaton Corporation, Rockwell Automation, General Electric (GE) Digital, Mitsubishi Electric, Honeywell Intelligrated, Toshiba Industrial Solutions, Hitachi Industrial Systems |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |