Reports

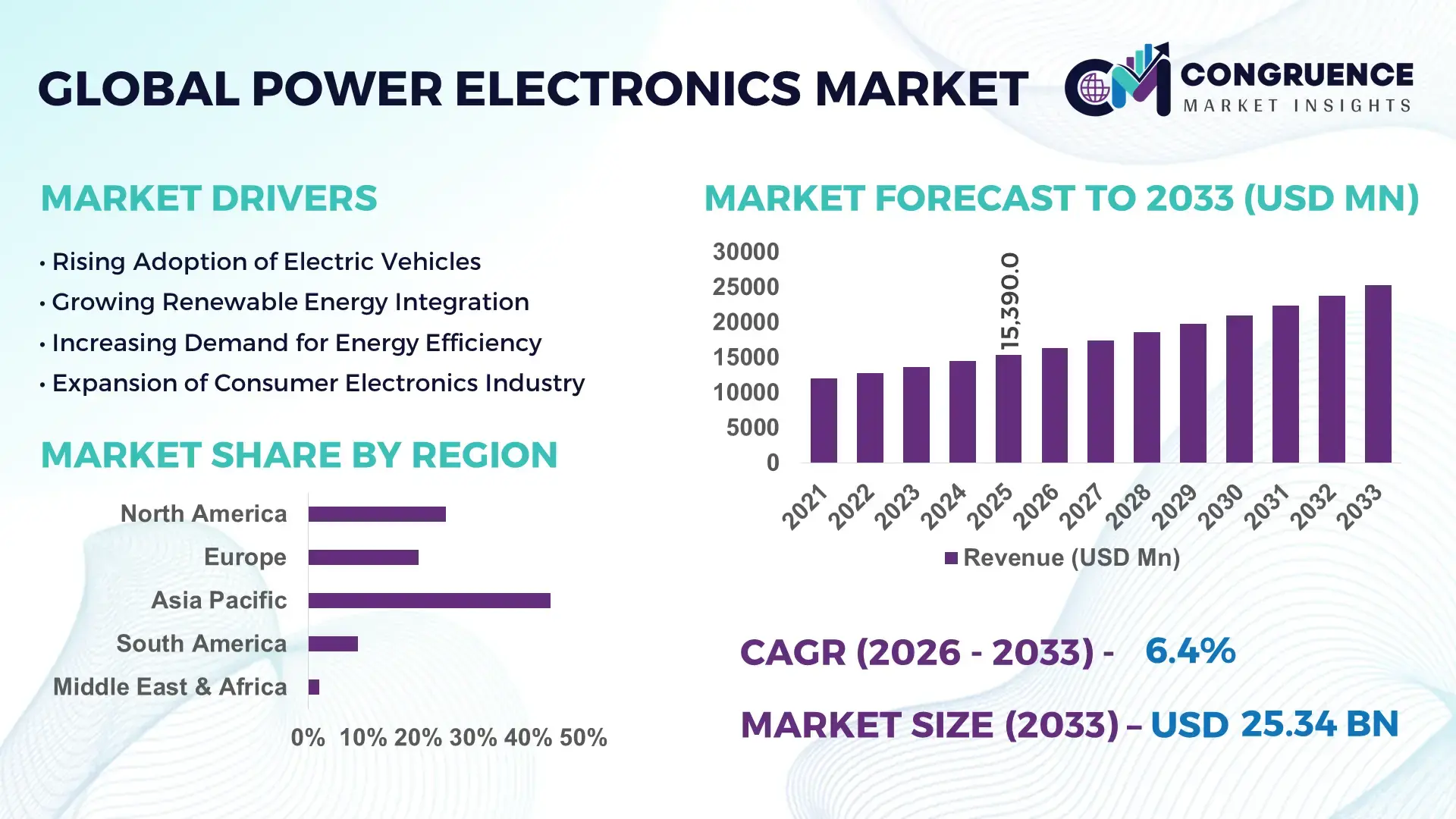

The Global Power Electronics Market was valued at USD 15390 Million in 2025 and is anticipated to reach a value of USD 25336.76 Million by 2033 expanding at a CAGR of 6.43% between 2026 and 2033. This growth is primarily driven by the accelerating adoption of energy-efficient power conversion technologies across electric vehicles, renewable energy systems, and industrial automation.

China continues to lead the global power electronics landscape with significant manufacturing capacity and aggressive infrastructure investments. The country produces over 60% of the world’s power semiconductor devices, supported by more than USD 40 billion in annual investments in semiconductor fabrication facilities and advanced packaging technologies. China’s electric vehicle ecosystem alone accounted for over 8 million units sold in 2024, driving substantial demand for inverters and power modules. Additionally, over 35% of global renewable energy installations are concentrated in China, boosting the deployment of high-efficiency power converters and grid integration systems. The nation’s rapid adoption of silicon carbide (SiC) and gallium nitride (GaN) technologies has further enhanced efficiency levels by up to 20% in industrial and automotive applications.

Market Size & Growth: USD 15390 Million in 2025 projected to reach USD 25336.76 Million by 2033 at 6.43% CAGR, driven by increasing electrification and energy efficiency demand.

Top Growth Drivers: Electric vehicle adoption rising by 28%, renewable energy integration increasing by 32%, industrial automation expansion by 24%.

Short-Term Forecast: By 2028, power conversion efficiency is expected to improve by 18% while system costs decline by 12% through advanced semiconductor adoption.

Emerging Technologies: Silicon carbide (SiC), gallium nitride (GaN), and advanced digital power control systems are transforming high-efficiency power conversion.

Regional Leaders: Asia-Pacific projected at USD 11000 Million by 2033 with strong manufacturing base; North America at USD 6200 Million driven by EV adoption; Europe at USD 5800 Million with strong renewable integration policies.

Consumer/End-User Trends: Automotive and industrial sectors account for over 55% of demand, with increasing adoption in smart grids and data centers.

Pilot or Case Example: In 2024, a large-scale EV manufacturing project achieved 22% efficiency gains using SiC-based inverters, reducing energy losses significantly.

Competitive Landscape: Infineon Technologies holds approximately 18% share, followed by STMicroelectronics, Mitsubishi Electric, ON Semiconductor, and Toshiba.

Regulatory & ESG Impact: Governments are targeting up to 40% emission reduction by 2030, encouraging adoption of high-efficiency power electronics systems.

Investment & Funding Patterns: Over USD 25 billion invested globally in semiconductor fabs and EV powertrain technologies between 2023 and 2025.

Innovation & Future Outlook: Integration of AI-driven power management and wide-bandgap semiconductors is expected to redefine system performance and reliability.

The power electronics market is heavily influenced by key industry sectors including automotive, renewable energy, consumer electronics, and industrial manufacturing, with automotive applications contributing nearly 30% of total demand. Technological innovations such as wide-bandgap semiconductors, high-frequency switching devices, and compact power modules are enabling higher efficiency and reduced thermal losses. Regulatory frameworks promoting carbon neutrality and energy efficiency standards are accelerating adoption across developed and emerging economies. Regional consumption patterns indicate strong growth in Asia-Pacific due to manufacturing expansion, while Europe is focusing on renewable integration and electrification initiatives. Emerging trends such as smart grid deployment, electrification of transportation, and AI-enabled energy management systems are expected to further reshape the market landscape, positioning power electronics as a critical component of modern energy infrastructure.

The power electronics market holds strategic importance in enabling energy transition, digital transformation, and industrial electrification across global economies. Advanced technologies such as silicon carbide (SiC) devices deliver up to 25% higher efficiency compared to traditional silicon-based components, significantly reducing energy losses in electric vehicles and renewable energy systems. Asia-Pacific dominates in production volume due to large-scale semiconductor manufacturing, while North America leads in adoption with over 45% of enterprises integrating advanced power management solutions in data centers and EV infrastructure.

In the short term, by 2028, AI-driven power optimization technologies are expected to improve system efficiency by approximately 20%, while reducing operational downtime by nearly 15% across industrial applications. Firms are increasingly aligning with ESG commitments, targeting up to 35% reduction in energy losses and enhanced recyclability of electronic components by 2030. In 2024, a leading automotive manufacturer in Germany achieved a 19% improvement in drivetrain efficiency through the integration of SiC-based inverter technology, demonstrating the tangible benefits of next-generation power electronics.

Strategically, the market is witnessing convergence between digital intelligence and hardware innovation, with embedded sensors and real-time monitoring systems enhancing reliability and predictive maintenance capabilities. Increasing electrification of transportation, expansion of renewable energy grids, and rising demand for high-performance computing infrastructure are reinforcing the importance of efficient power conversion systems. As industries prioritize resilience and sustainability, the power electronics market is positioned as a foundational pillar supporting regulatory compliance, operational efficiency, and long-term sustainable growth.

The rapid electrification of transportation, industrial systems, and residential infrastructure is a primary driver of the power electronics market. Electric vehicle adoption has grown by over 30% annually in recent years, significantly increasing the demand for efficient power conversion systems such as inverters and onboard chargers. In industrial sectors, over 70% of manufacturing facilities are transitioning toward automation and electrified processes, requiring advanced motor drives and power control systems. Renewable energy installations, particularly solar and wind, have surpassed 300 GW annually, necessitating high-performance power electronics for grid stability and energy conversion. Furthermore, data centers, which consume nearly 2% of global electricity, are increasingly deploying high-efficiency power supply units to reduce energy consumption by up to 15%. These trends collectively reinforce the critical role of power electronics in enabling energy-efficient and sustainable operations across multiple sectors.

The power electronics market faces significant restraints due to high manufacturing costs and complex production processes associated with advanced semiconductor materials. Wide-bandgap semiconductors such as silicon carbide and gallium nitride require specialized fabrication techniques, resulting in production costs that are 2 to 3 times higher than conventional silicon-based devices. Additionally, limited availability of high-quality raw materials and wafer substrates further constrains supply, leading to longer lead times and increased pricing pressures. The cost of setting up semiconductor fabrication plants can exceed USD 10 billion, creating high entry barriers for new players. Moreover, thermal management challenges and reliability concerns in high-power applications require advanced packaging and cooling solutions, further increasing system costs. These factors collectively hinder widespread adoption, particularly in cost-sensitive markets and small-scale applications.

The expansion of renewable energy infrastructure presents substantial opportunities for the power electronics market. Global renewable capacity additions have consistently exceeded 300 GW annually, with solar and wind projects accounting for a significant share. Power electronics play a crucial role in converting and managing energy from these sources, with modern inverters achieving efficiency levels above 98%. The increasing deployment of energy storage systems, particularly lithium-ion batteries, is further driving demand for advanced power conversion and management solutions. Smart grid development, supported by government investments exceeding USD 20 billion globally, is creating additional demand for intelligent power electronics systems capable of real-time monitoring and load balancing. Furthermore, the integration of distributed energy resources and microgrids is opening new avenues for innovation and market expansion, particularly in emerging economies seeking to enhance energy access and reliability.

Supply chain disruptions and technological complexities present significant challenges for the power electronics market. The semiconductor supply chain has experienced considerable volatility, with lead times for critical components extending beyond 40 weeks in certain cases. Dependence on a limited number of suppliers for key materials such as silicon carbide wafers increases vulnerability to geopolitical and logistical risks. Additionally, the rapid pace of technological innovation requires continuous investment in research and development, placing financial strain on manufacturers. Integration challenges, particularly in high-power and high-frequency applications, demand sophisticated design and testing processes to ensure reliability and performance. Thermal management issues and system-level compatibility further complicate product development. These challenges are compounded by evolving regulatory standards and the need for compliance with energy efficiency and environmental requirements, making it increasingly complex for companies to maintain competitiveness in the global market.

• Accelerated Adoption of Wide-Bandgap Semiconductors Improving Efficiency by 25%

The transition toward silicon carbide (SiC) and gallium nitride (GaN) devices is significantly transforming power electronics performance benchmarks. SiC-based power modules are delivering up to 25% higher energy efficiency and reducing switching losses by nearly 40% compared to traditional silicon devices. In electric vehicle applications, SiC inverters have improved driving range by approximately 10% while reducing system weight by 15%. More than 35% of newly designed EV powertrains in 2025 are integrating wide-bandgap semiconductors, indicating rapid industrial-scale adoption.

• Expansion of Electric Vehicle Infrastructure Driving 30% Increase in Power Module Demand

The rapid global expansion of electric vehicle infrastructure is boosting demand for high-performance power electronics components. EV charging stations have grown by over 45% globally between 2023 and 2025, requiring advanced converters and rectifiers to manage high loads efficiently. Power modules used in EVs have seen a 30% increase in demand, with onboard chargers achieving efficiency levels exceeding 95%. Fast-charging systems now operate at power levels above 350 kW, reducing charging times by nearly 50% compared to earlier systems.

• Integration of AI-Driven Power Management Enhancing System Efficiency by 20%

Artificial intelligence and digital control technologies are being integrated into power electronics systems to optimize energy consumption and operational performance. AI-enabled power management systems have demonstrated up to 20% improvement in efficiency across industrial and data center applications. Predictive maintenance capabilities powered by machine learning algorithms have reduced equipment downtime by 18% while extending component lifespan by 25%. Approximately 40% of large-scale industrial facilities have adopted intelligent power control systems to enhance operational reliability.

• Growth in Renewable Energy Integration Increasing Converter Deployment by 28%

The global push toward renewable energy is significantly increasing the deployment of power electronic converters and inverters. Solar and wind installations have driven a 28% increase in demand for grid-tied inverters, with modern systems achieving conversion efficiencies above 98%. Energy storage systems, particularly battery-based solutions, are expanding rapidly, with installation rates rising by 35% annually. Smart grid projects incorporating advanced power electronics have improved grid stability by up to 22%, supporting the seamless integration of distributed energy resources across both developed and emerging economies.

The power electronics market is segmented based on type, application, and end-user, each playing a crucial role in shaping demand patterns and technological adoption. By type, discrete components, modules, and integrated circuits dominate the landscape, with modules gaining traction due to their high efficiency and compact design. In terms of applications, automotive and renewable energy sectors collectively contribute over 50% of total demand, driven by electrification trends and clean energy initiatives. Industrial applications also hold a significant share, supported by automation and digital manufacturing systems. From an end-user perspective, automotive manufacturers, energy utilities, and industrial enterprises are the primary contributors, accounting for a substantial portion of market consumption. The increasing integration of advanced semiconductors and digital control technologies across these segments is further enhancing performance and operational efficiency.

The power electronics market by type includes power discrete devices, power modules, and power integrated circuits, each catering to specific performance and application requirements. Power modules currently account for approximately 45% of total adoption due to their superior thermal performance, compact design, and ability to handle high power loads efficiently. In comparison, discrete devices contribute around 30%, while integrated circuits hold close to 25%. However, power integrated circuits are emerging as the fastest-growing segment, expanding at an estimated CAGR of 8.5%, driven by increasing demand for miniaturization and integration in consumer electronics and automotive systems. Discrete devices remain critical in cost-sensitive and low-power applications, while modules are preferred in high-power sectors such as electric vehicles and industrial drives. Integrated circuits are gaining traction in applications requiring high switching frequency and reduced system complexity. Collectively, discrete devices and integrated circuits contribute nearly 55% of the market, highlighting their continued relevance.

The application segment of the power electronics market spans automotive, renewable energy, industrial, consumer electronics, and telecommunications. Automotive applications lead with approximately 35% share, driven by the rapid adoption of electric vehicles and hybrid systems. Renewable energy follows with around 25%, while industrial applications contribute close to 20%. However, renewable energy applications are the fastest-growing, expanding at an estimated CAGR of 9%, supported by increasing global installations of solar and wind energy systems. Consumer electronics and telecommunications together account for nearly 20% of the market, driven by demand for energy-efficient devices and high-performance power supplies. Automotive applications benefit from advancements in inverter and battery management systems, while renewable energy relies heavily on efficient converters and grid integration technologies.

The end-user segmentation of the power electronics market includes automotive, energy and utilities, industrial manufacturing, consumer electronics, and IT & telecommunications sectors. Automotive remains the leading end-user, accounting for approximately 30% of total demand, driven by electric vehicle production and electrification initiatives. Energy and utilities follow with around 25%, while industrial manufacturing contributes nearly 20%. However, the IT and telecommunications sector is the fastest-growing end-user, expanding at an estimated CAGR of 10%, fueled by increasing data center expansion and digital infrastructure investments. Consumer electronics and other sectors collectively account for about 25% of the market, supported by rising demand for portable and energy-efficient devices. Automotive and energy sectors dominate due to their high power requirements and reliance on efficient conversion systems, while industrial users focus on automation and process optimization.

Region Asia-Pacific accounted for the largest market share at 48% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 7.2% between 2026 and 2033.

Asia-Pacific’s dominance is supported by strong semiconductor manufacturing output exceeding 65% of global production capacity and over 70% of global electric vehicle production concentrated in China, Japan, and South Korea. North America, with a 22% market share in 2025, is witnessing accelerated adoption due to data center expansion and EV infrastructure investments exceeding 40% growth in charging networks. Europe holds approximately 20% share, driven by renewable energy installations surpassing 250 GW cumulative capacity. South America contributes around 6%, with Brazil accounting for over 55% of the regional demand due to energy modernization initiatives. The Middle East & Africa region holds nearly 4% share, supported by infrastructure investments exceeding USD 15 billion in smart grid and industrial electrification projects. Regional demand variations are influenced by industrialization levels, renewable energy penetration rates above 30% in Europe, and increasing electrification across emerging economies.

How is advanced digital infrastructure accelerating high-efficiency power systems adoption?

North America accounts for approximately 22% of the global power electronics market, driven by strong demand from data centers, electric vehicles, and industrial automation sectors. Over 45% of enterprises in sectors such as healthcare, finance, and cloud computing have adopted advanced power management systems to enhance energy efficiency and reduce operational costs. Government initiatives, including incentives for clean energy and EV adoption, have contributed to a 35% increase in infrastructure investments since 2023. Regulatory frameworks targeting up to 40% reduction in carbon emissions by 2030 are accelerating the deployment of high-efficiency power conversion technologies. Technological advancements such as AI-enabled power optimization and high-density power modules are improving system efficiency by up to 20%. A leading regional player has focused on expanding silicon carbide production capacity, increasing output by 25% to meet growing EV demand. Consumer behavior in this region reflects high enterprise adoption, particularly in data-driven industries prioritizing energy-efficient infrastructure.

What role do sustainability regulations play in accelerating high-performance energy systems?

Europe represents nearly 20% of the global power electronics market, with key countries such as Germany, the United Kingdom, and France leading adoption. The region is characterized by stringent sustainability regulations, including mandates targeting over 50% renewable energy integration in power grids by 2030. Regulatory bodies are promoting energy-efficient technologies, resulting in a 30% increase in deployment of advanced inverters and converters across industrial and renewable sectors. The adoption of wide-bandgap semiconductors has grown by 28%, improving efficiency and reducing energy losses significantly. Local companies are investing heavily in electrification technologies, with one major manufacturer expanding its EV powertrain component production capacity by 20% in 2024. Consumer behavior reflects strong preference for environmentally compliant solutions, with over 60% of industrial users prioritizing low-emission and energy-efficient systems.

Why is rapid industrial expansion driving large-scale deployment of advanced power solutions?

Asia-Pacific leads the global power electronics market in both volume and consumption, accounting for nearly 48% of total demand. Major economies such as China, India, and Japan contribute significantly, with China alone representing over 60% of regional production capacity. The region’s manufacturing sector accounts for more than 65% of global semiconductor output, supported by large-scale infrastructure and industrialization initiatives. Rapid urbanization and increasing electricity demand, growing at over 6% annually in key economies, are driving the need for efficient power conversion systems. Innovation hubs in Japan and South Korea are advancing technologies such as GaN-based devices, improving efficiency by up to 20%. A prominent regional manufacturer increased its production of EV power modules by 30% in 2025 to meet rising demand. Consumer behavior is heavily influenced by mobile-first economies and high adoption of electric mobility solutions, contributing to sustained market expansion.

How are energy modernization efforts reshaping demand for efficient power technologies?

South America accounts for approximately 6% of the global power electronics market, with Brazil and Argentina being the primary contributors. Brazil alone represents over 55% of regional demand, driven by investments in renewable energy and grid modernization projects. Hydropower remains a dominant energy source, accounting for nearly 60% of electricity generation, requiring efficient power conversion systems for grid stability. Government incentives supporting renewable energy adoption have increased installations by over 20% in recent years. Trade policies encouraging local manufacturing have also contributed to a 15% rise in domestic production of power electronic components. A regional company has expanded its inverter production capacity by 18% to support solar energy projects. Consumer behavior in this region is closely tied to energy access and affordability, with increasing demand for cost-effective and durable power solutions.

What drives the demand for high-performance systems in energy-intensive industries?

The Middle East & Africa region holds approximately 4% of the global power electronics market, driven by demand from oil & gas, construction, and infrastructure sectors. Countries such as the UAE and South Africa are leading adoption, supported by investments exceeding USD 10 billion in smart city and renewable energy projects. The region is witnessing a 25% increase in deployment of advanced power systems for industrial applications, particularly in energy-intensive sectors. Technological modernization efforts, including smart grid implementation and digital monitoring systems, are improving efficiency by up to 18%. Trade partnerships and government policies promoting industrial diversification are further boosting market growth. A local energy firm has implemented advanced power conversion systems in large-scale solar projects, improving output efficiency by 15%. Consumer behavior reflects a growing preference for reliable and high-capacity power systems to support infrastructure development.

China – 32% share in the Power Electronics market, driven by large-scale semiconductor production and strong electric vehicle manufacturing ecosystem.

United States – 18% share in the Power Electronics market, supported by advanced technology adoption and high demand from data centers and EV infrastructure.

The power electronics market is moderately fragmented, with over 120 active global and regional players competing across semiconductor manufacturing, module design, and system integration. The top five companies collectively account for approximately 45% of the total market share, indicating a balanced mix of competition and consolidation. Market leaders are focusing heavily on innovation, with more than 35% of their annual investments directed toward research and development of wide-bandgap semiconductors such as silicon carbide and gallium nitride. Strategic initiatives including mergers, acquisitions, and partnerships have increased by nearly 25% between 2023 and 2025, aimed at expanding technological capabilities and global presence.

Product launches are a key competitive strategy, with over 60 new high-efficiency power modules introduced in the past two years, offering up to 20% performance improvements. Companies are also investing in expanding manufacturing capacity, with semiconductor fabrication plants requiring investments exceeding USD 10 billion per facility. Digital transformation trends, including AI-enabled power management and predictive maintenance, are becoming critical differentiators, with adoption rates surpassing 40% among leading players. Additionally, vertical integration strategies are being implemented to secure supply chains and reduce dependency on external suppliers. These competitive dynamics highlight a rapidly evolving landscape focused on innovation, efficiency, and long-term sustainability.

Infineon Technologies AG

STMicroelectronics N.V.

Mitsubishi Electric Corporation

Toshiba Corporation

ON Semiconductor Corporation

Fuji Electric Co., Ltd.

Renesas Electronics Corporation

Texas Instruments Incorporated

NXP Semiconductors N.V.

ABB Ltd.

Siemens AG

ROHM Semiconductor

Wolfspeed, Inc.

Vishay Intertechnology, Inc.

Hitachi Energy Ltd.

The power electronics market is undergoing rapid technological transformation driven by advancements in semiconductor materials, digital control systems, and system integration architectures. Wide-bandgap semiconductors such as silicon carbide (SiC) and gallium nitride (GaN) are at the forefront, enabling switching frequencies above 100 kHz and reducing power losses by up to 40% compared to conventional silicon devices. SiC-based devices are increasingly used in electric vehicles and renewable energy systems, where they improve energy efficiency by approximately 20% and reduce cooling requirements by nearly 30%.

Advanced packaging technologies, including 3D packaging and chip-scale integration, are enhancing thermal performance and power density. Modern power modules now achieve power densities exceeding 50 kW per liter, compared to less than 20 kW per liter in traditional designs. Digital power control using microcontrollers and DSP-based systems has enabled real-time monitoring and adaptive control, improving system efficiency by up to 15% and reducing fault rates by 18%.

The integration of artificial intelligence and machine learning algorithms is further optimizing power conversion and distribution. AI-enabled predictive maintenance systems are reducing unplanned downtime by approximately 20% while extending equipment lifespan by up to 25%. In parallel, smart grid technologies are incorporating advanced power electronics to manage distributed energy resources, improving grid stability by over 22%.

Emerging trends such as wireless power transfer, solid-state transformers, and high-voltage direct current (HVDC) systems are expanding the application scope of power electronics. HVDC systems are capable of transmitting power over distances exceeding 1,000 km with losses below 3%, significantly improving long-distance energy transmission efficiency. These technological advancements are collectively redefining performance standards and enabling scalable, energy-efficient solutions across industrial, automotive, and energy sectors.

• In March 2025, Infineon Technologies expanded its silicon carbide semiconductor manufacturing capacity with a new 300 mm wafer facility in Germany, increasing production efficiency by over 30% and strengthening supply for electric vehicle and renewable energy applications. Source: www.infineon.com

• In September 2024, STMicroelectronics launched a new generation of silicon carbide MOSFETs designed for automotive applications, delivering up to 20% lower energy losses and enabling higher efficiency in electric vehicle powertrains. Source: www.st.com

• In April 2025, Mitsubishi Electric announced the development of advanced power semiconductor modules for industrial systems, improving thermal resistance by 15% and enhancing operational reliability in high-power applications such as factory automation. Source: www.mitsubishielectric.com

• In November 2024, ON Semiconductor introduced an integrated intelligent power module platform targeting EV and industrial markets, achieving efficiency improvements of up to 10% and reducing system size by nearly 25%. Source: www.onsemi.com

The scope of the power electronics market report encompasses a comprehensive evaluation of key segments, technologies, applications, and geographic regions shaping industry growth. The report covers a wide range of product categories, including power discrete devices, power modules, and integrated circuits, which collectively support diverse applications across automotive, industrial, renewable energy, consumer electronics, and telecommunications sectors. Automotive and renewable energy applications together account for over 50% of total demand, reflecting the increasing emphasis on electrification and sustainable energy solutions.

Geographically, the report analyzes major regions including Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, with Asia-Pacific contributing nearly half of global consumption due to its strong manufacturing base and high adoption of electric mobility solutions. The report also examines key end-user industries such as automotive manufacturing, energy utilities, industrial enterprises, and digital infrastructure providers, highlighting their respective adoption patterns and technological requirements.

Technological coverage includes advancements in wide-bandgap semiconductors, digital power management systems, smart grid integration, and high-efficiency power conversion technologies. Emerging segments such as wireless power transfer, solid-state transformers, and energy storage integration are also addressed, reflecting evolving industry dynamics. Additionally, the report evaluates regulatory frameworks, sustainability initiatives, and energy efficiency standards influencing market development. By combining quantitative insights with qualitative analysis, the report provides a structured understanding of the competitive landscape, innovation trends, and strategic opportunities within the power electronics market.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

6.43% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Infineon Technologies AG, STMicroelectronics N.V., Mitsubishi Electric Corporation, Toshiba Corporation, ON Semiconductor Corporation, Fuji Electric Co., Ltd., Renesas Electronics Corporation, Texas Instruments Incorporated, NXP Semiconductors N.V., ABB Ltd., Siemens AG, ROHM Semiconductor, Wolfspeed, Inc., Vishay Intertechnology, Inc., Hitachi Energy Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |