Reports

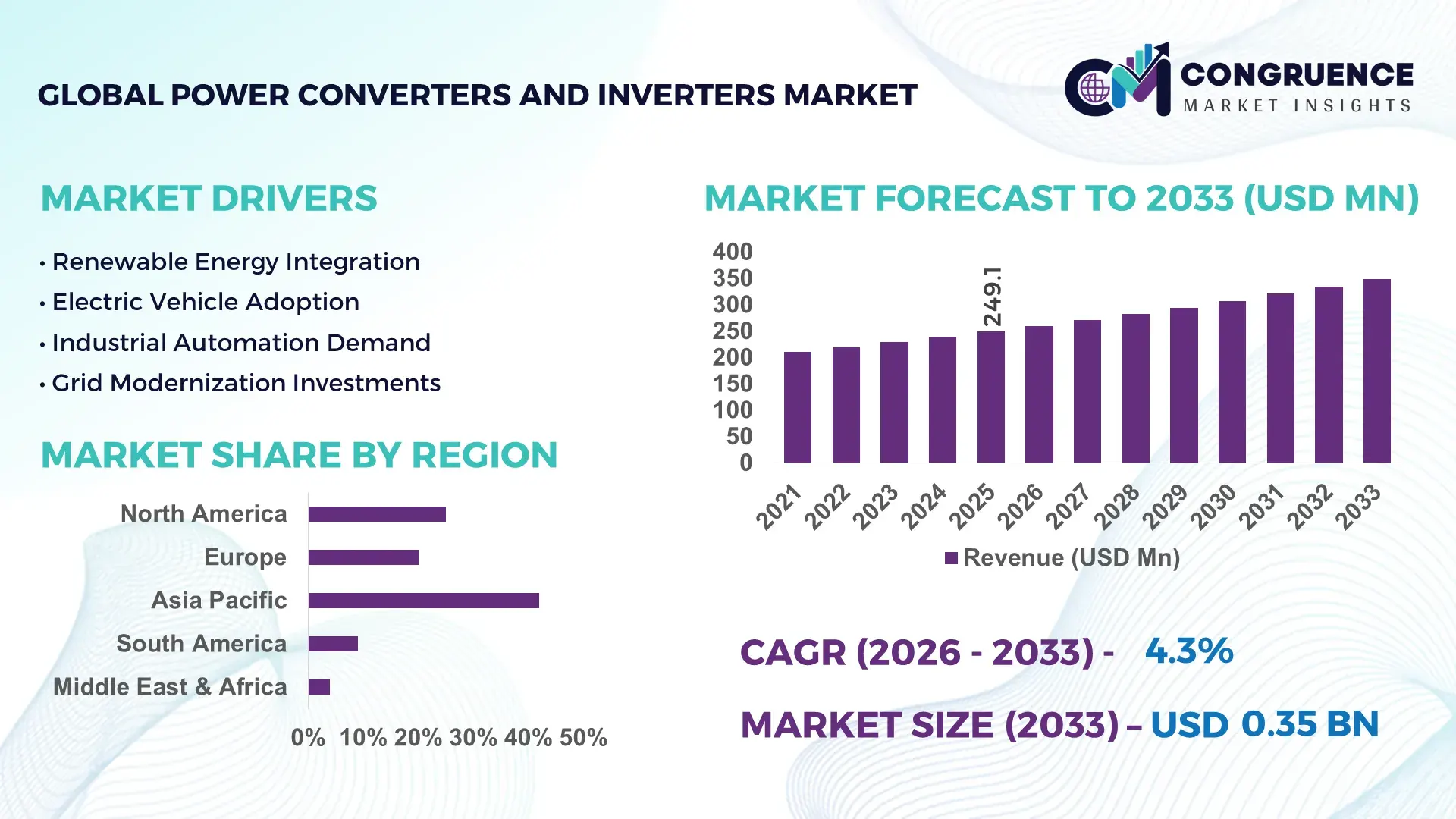

The Global Power Converters and Inverters Market was valued at USD 249.05 Million in 2025 and is anticipated to reach a value of USD 348.78 Million by 2033 expanding at a CAGR of 4.3% between 2026 and 2033. Growth is primarily supported by rising electrification, renewable energy integration, and efficiency-driven upgrades across industrial and utility-scale power systems.

China dominates the global Power Converters and Inverters landscape through large-scale manufacturing capacity, advanced power electronics ecosystems, and strong domestic demand across renewable energy, rail traction, electric vehicles, and industrial automation. The country accounts for over 55% of global inverter production capacity, with annual output exceeding 180 GW for solar and wind inverters combined. Investments in power semiconductor fabrication surpassed USD 25 billion between 2022 and 2025, accelerating adoption of SiC- and GaN-based converters. More than 70% of China’s new renewable installations utilize high-efficiency central and string inverters, while industrial motor drives and EV power electronics collectively contribute over 45% of domestic converter demand.

Market Size & Growth: Valued at USD 249.05 Million in 2025, projected to reach USD 348.78 Million by 2033, growing at a CAGR of 4.3% driven by electrification and renewable grid integration.

Top Growth Drivers: Renewable energy adoption +18%, power efficiency improvements +12%, industrial automation penetration +15%.

Short-Term Forecast: By 2028, average system efficiency is expected to improve by ~10% due to advanced power semiconductor adoption.

Emerging Technologies: Wide-bandgap semiconductors (SiC, GaN), smart digital power management ICs, bidirectional inverters for energy storage.

Regional Leaders: Asia-Pacific USD 145 Million by 2033 with EV and solar-driven demand; North America USD 92 Million with grid modernization focus; Europe USD 78 Million led by energy efficiency mandates.

Consumer/End-User Trends: Utilities, EV manufacturers, and industrial users account for over 65% of total demand, with rising preference for modular, high-efficiency systems.

Pilot or Case Example: A 2024 utility-scale solar project in India achieved a 14% reduction in conversion losses using advanced string inverters.

Competitive Landscape: ABB holds ~15% share, followed by Siemens, Schneider Electric, Huawei, and Delta Electronics.

Regulatory & ESG Impact: Grid efficiency standards and renewable integration mandates are accelerating inverter upgrades globally.

Investment & Funding Patterns: Over USD 9 billion invested globally since 2023 in power electronics manufacturing and R&D facilities.

Innovation & Future Outlook: Integration of AI-based power optimization and next-generation semiconductor materials will shape long-term competitiveness.

The Power Converters and Inverters Market is structurally supported by strong demand from renewable energy (approximately 38% of total usage), industrial motor drives (27%), electric vehicles and charging infrastructure (22%), and consumer electronics (13%). Technological progress in wide-bandgap semiconductors has enabled higher switching frequencies, compact designs, and efficiency levels exceeding 98% in premium systems. Regulatory frameworks promoting energy efficiency, grid stability, and carbon reduction continue to influence procurement decisions. Asia-Pacific leads consumption due to rapid industrialization and renewable deployment, while North America and Europe show steady growth driven by grid modernization and electrified transport. Looking ahead, bidirectional converters, solid-state transformers, and integrated power modules are expected to redefine system architectures and unlock new applications across smart grids and energy storage systems.

The Power Converters and Inverters Market holds strategic relevance as a core enabler of electrification, grid stability, and energy efficiency across industrial, transportation, and renewable energy ecosystems. As power systems shift toward decentralization and digitization, converters and inverters increasingly determine operational reliability, system efficiency, and compliance readiness. Silicon carbide (SiC)-based power converters deliver nearly 30% higher switching efficiency compared to conventional silicon-based designs, enabling smaller form factors, reduced thermal losses, and longer equipment lifecycles. Asia-Pacific dominates in production volume due to large-scale manufacturing and renewable installations, while Europe leads in adoption intensity, with over 62% of utilities and industrial enterprises deploying high-efficiency or smart inverter systems.

By 2028, AI-enabled power management and predictive diagnostics are expected to reduce unplanned downtime by approximately 20%, particularly in utility-scale solar farms and industrial motor drive systems. ESG and compliance considerations are increasingly shaping procurement strategies, with firms committing to 15–20% reductions in energy losses and material waste by 2030 through high-efficiency power electronics and recyclable component designs. In 2024, Germany-based industrial projects integrating AI-controlled inverters achieved a 12% improvement in conversion efficiency and measurable grid stability gains through adaptive load-balancing algorithms. Collectively, these developments position the Power Converters and Inverters Market as a critical pillar supporting infrastructure resilience, regulatory alignment, and sustainable long-term growth across global energy and industrial value chains.

Global renewable energy capacity additions exceeded 440 GW in 2024, driving parallel demand for advanced power converters and inverters capable of handling variable generation profiles. Solar photovoltaic systems alone require inverters for every installation, with utility-scale projects increasingly adopting high-voltage central and string inverters for efficiency gains exceeding 98%. Wind energy applications rely on power converters to stabilize frequency and voltage, particularly in offshore installations where grid synchronization is critical. Additionally, hybrid renewable-plus-storage projects are expanding, increasing demand for bidirectional inverters that manage charging and discharging cycles. These trends directly elevate equipment replacement rates, system upgrades, and new installations, reinforcing sustained demand across utility, commercial, and industrial segments of the Power Converters and Inverters Market.

Advanced power converters and inverters incorporating SiC and GaN components carry upfront costs 20–35% higher than conventional silicon-based systems, limiting adoption among cost-sensitive users. Semiconductor fabrication complexity and limited global foundry capacity also expose manufacturers to supply volatility, extended lead times, and pricing uncertainty. In emerging markets, grid operators and small industrial users often delay upgrades due to capital expenditure constraints, opting for legacy systems with lower efficiency. Additionally, skilled labor shortages for installation and maintenance of advanced power electronics increase total ownership costs. These factors collectively moderate near-term adoption rates despite strong long-term efficiency and lifecycle cost advantages.

Electric vehicle production surpassed 14 million units globally in 2024, significantly expanding demand for onboard chargers, DC-DC converters, and traction inverters. Fast-charging infrastructure further drives demand for high-power conversion systems capable of handling voltages above 800V. Simultaneously, grid-scale energy storage deployments exceeded 100 GWh, creating strong demand for bidirectional inverters that support grid balancing and peak shaving. Industrial microgrids and commercial energy storage systems are emerging as high-growth application areas, enabling suppliers to diversify portfolios and develop integrated power management solutions tailored to decentralized energy architectures.

Power converters and inverters must comply with diverse regional grid codes, safety standards, and electromagnetic compatibility requirements, increasing design complexity and certification timelines. In Europe and North America, evolving grid-forming and cybersecurity standards require continuous firmware updates and system validation. Integration challenges also arise when retrofitting advanced inverters into aging grid or industrial infrastructure, often necessitating additional protection, communication, and control systems. These factors increase deployment timeframes and engineering costs, placing pressure on manufacturers and system integrators to balance compliance, interoperability, and performance within competitive delivery schedules.

Modular and Prefabricated Infrastructure Driving Configurable Power Systems:

The rise of modular and prefabricated construction is reshaping demand patterns in the Power Converters and Inverters Market, particularly for compact, scalable, and plug-and-play power units. Around 55% of new infrastructure and industrial projects report measurable cost benefits from modular construction practices, accelerating deployment timelines by 20–30%. Off-site prefabrication and automated assembly increase demand for standardized inverter modules below 500 kW, especially in Europe and North America, where labor optimization and faster commissioning are critical business priorities.

Wide-Bandgap Semiconductors Accelerating Efficiency Benchmarks:

Adoption of silicon carbide (SiC) and gallium nitride (GaN) technologies continues to expand, with more than 40% of newly deployed industrial converters now integrating wide-bandgap components. These systems achieve 2–4% higher conversion efficiency and reduce switching losses by nearly 30% compared to conventional silicon-based designs. Power density improvements of up to 50% support smaller enclosures, lower cooling requirements, and improved reliability across EV charging, renewable energy, and industrial automation applications.

Digital and AI-Enabled Power Electronics Gaining Operational Preference:

Smart converters and inverters embedded with digital control and AI-based monitoring capabilities are increasingly specified by utilities and large industrial users. Nearly 60% of new utility-scale renewable installations now require digitally controlled inverter platforms capable of real-time grid response. Predictive diagnostics and condition monitoring have demonstrated 15–20% reductions in unplanned downtime and 10–12% improvements in asset utilization, strengthening operational efficiency and lifecycle management outcomes.

Expansion of Bidirectional Inverters for Storage and Mobility Applications:

Bidirectional power converters are gaining prominence to support energy storage systems, vehicle-to-grid infrastructure, and industrial microgrids. Over 70% of new grid-scale battery installations now require bidirectional inverter functionality to enable peak shaving and frequency regulation. In electric mobility applications, bidirectional onboard charging solutions are improving energy recovery efficiency by up to 18%, reinforcing their strategic role in flexible, grid-interactive power architectures.

The Power Converters and Inverters Market is segmented by type, application, and end-user, reflecting varied technical requirements and adoption behaviors across industries. Product segmentation highlights differences in voltage handling, directionality, and efficiency optimization, while application-based segmentation underscores the growing importance of renewable energy systems, transportation electrification, and industrial automation. End-user segmentation reveals concentrated demand from utilities and industrial operators, alongside rapidly increasing uptake from mobility and infrastructure players. Across all segments, the market shows a clear preference for high-efficiency, digitally controlled, and flexible power conversion systems that align with evolving grid standards, electrification targets, and operational resilience requirements.

The Power Converters and Inverters Market by type includes DC-AC inverters, DC-DC converters, AC-DC converters, and bidirectional converters. DC-AC inverters lead the segment, accounting for approximately 46% of total adoption, supported by their critical role in solar photovoltaic plants, wind power systems, and grid-connected energy assets requiring stable AC output. DC-DC converters represent nearly 28% of adoption, driven by voltage regulation needs in electric vehicles, data centers, and industrial electronics. Bidirectional converters currently hold around 16% share but are the fastest-growing type, expanding at an estimated 8.1% CAGR due to rising deployment in battery energy storage systems, vehicle-to-grid infrastructure, and microgrids. AC-DC converters and other specialized power modules collectively contribute about 10%, serving niche industrial and commercial applications.

By application, renewable energy systems dominate the Power Converters and Inverters Market with close to 41% of total usage, as power conversion is essential for integrating variable solar and wind generation into utility grids. Industrial automation and motor drive systems follow with roughly 26%, reflecting demand for precise speed control, reduced energy losses, and operational reliability. Electric vehicles and charging infrastructure account for about 21% and represent the fastest-growing application segment, expanding at an estimated 9.4% CAGR, supported by high-voltage vehicle architectures and fast-charging networks exceeding 800V. Other applications, including data centers, rail traction, and consumer electronics, together contribute approximately 12%, addressing performance-critical but application-specific requirements.

Utilities represent the leading end-user segment in the Power Converters and Inverters Market, accounting for around 38% of total demand, driven by grid expansion, renewable integration, and substation modernization programs. Industrial manufacturers follow with approximately 29%, supported by investments in automation, robotics, and energy optimization. The transportation sector, including electric vehicle manufacturers and rail operators, holds about 22% and is the fastest-growing end-user group, expanding at an estimated 8.7% CAGR due to electrification mandates and fleet transition programs. Commercial and residential users collectively contribute the remaining 11%, with adoption centered on distributed energy systems, backup power, and rooftop solar installations.

Asia-Pacific accounted for the largest market share at 42% in 2025; however, South America is expected to register the fastest growth, expanding at a CAGR of 6.2% between 2026 and 2033.

In 2025, Asia-Pacific’s market volume exceeded 105,000 units, driven by China’s industrial electrification, India’s renewable energy expansion, and Japan’s advanced EV infrastructure. North America followed with approximately 28,500 units, while Europe contributed around 24,700 units. Asia-Pacific leads in both production and consumption of DC-AC and bidirectional inverters, with over 60% of regional installations utilizing high-efficiency, digitally controlled systems. South America’s growth is supported by government incentives for renewable energy projects, growing energy storage adoption, and urban electrification. Emerging technologies such as SiC and GaN converters, modular inverters, and AI-enabled power management systems are being deployed regionally to optimize grid performance, reduce energy losses by up to 15%, and support industrial and commercial infrastructure.

How are industrial and utility sectors shaping the power conversion landscape?

North America holds approximately 27% of the global Power Converters and Inverters Market. Utilities and industrial manufacturers are primary drivers, with electricity transmission upgrades and industrial automation increasing demand for high-efficiency inverters. Regulatory initiatives, including grid modernization incentives and renewable integration policies, are encouraging adoption of digital and modular converter technologies. Technological advancements, such as AI-enabled predictive maintenance and wide-bandgap semiconductors, are improving system reliability and reducing downtime by 12–15%. Local players like ABB North America are deploying smart inverter solutions for utility-scale solar farms, achieving measurable efficiency gains. Enterprises in healthcare and finance demonstrate higher adoption rates for modular, scalable systems, while commercial infrastructure prioritizes energy management and operational resilience.

What factors are driving sustainable and regulated inverter adoption?

Europe accounts for around 23% of the global market. Germany, the UK, and France are leading adopters, driven by renewable energy integration and energy efficiency regulations. Sustainability mandates from bodies like the European Commission and local grid codes encourage advanced inverter deployment with explainable and compliant designs. Emerging technologies such as SiC inverters and AI-powered energy management systems are widely adopted across utility and industrial sectors. Schneider Electric in France has implemented modular inverter systems in industrial plants, achieving a 10% reduction in energy losses. Regulatory pressure leads to significant adoption in commercial and industrial applications, while utilities focus on grid stability and automated load balancing.

How is regional electrification driving power converter demand?

Asia-Pacific leads the global market with a 42% share in 2025, with China, India, and Japan as top consumers. Large-scale renewable installations, EV expansion, and industrial electrification contribute to high adoption. Infrastructure modernization, smart grid projects, and local semiconductor investments are enabling deployment of advanced DC-AC and bidirectional inverters. Huawei and Delta Electronics are introducing modular, high-efficiency inverters and AI-controlled power systems to support industrial and residential applications. Consumer behavior varies, with industrial sectors adopting high-voltage, high-capacity systems, while residential and commercial users focus on modular, scalable renewable solutions.

What are the emerging opportunities in energy storage and electrification?

South America holds approximately 8% of the global market, with Brazil and Argentina as key contributors. Growth is driven by renewable energy installations, microgrid expansion, and government incentives for distributed energy projects. Local players, including WEG Electric, are deploying high-efficiency inverters for industrial and solar PV applications. Infrastructure development and energy storage adoption support grid stability, while commercial enterprises increasingly integrate modular and digitally monitored systems. Consumer demand is influenced by localized energy solutions, with emphasis on cost efficiency and operational reliability in both urban and industrial settings.

How are energy transition and industrial modernization shaping adoption?

The Middle East & Africa market represents approximately 7% of the global share, with the UAE, Saudi Arabia, and South Africa driving growth. Regional demand is supported by oil & gas electrification, solar PV expansion, and industrial infrastructure modernization. Technological upgrades include modular inverters, AI-enabled monitoring, and SiC-based power electronics. Local companies are collaborating with international manufacturers to deploy utility-scale solar inverters and smart grid solutions, achieving measurable efficiency improvements. Consumer behavior varies, with industrial enterprises adopting high-capacity systems for operational reliability, while commercial and utility segments focus on regulatory compliance and energy management.

China – 28% share; dominance due to high production capacity, large-scale renewable energy deployment, and advanced industrial applications.

United States – 17% share; strong end-user demand in utilities and industrial sectors, supported by regulatory incentives and technological innovation in smart inverters.

The Power Converters and Inverters market is moderately consolidated, with approximately 85 active global competitors operating across utility, industrial, and mobility applications. The top five companies—ABB, Siemens, Schneider Electric, Huawei, and Delta Electronics—together hold nearly 47% of total market share, reflecting a significant but not dominant concentration. Competition is primarily driven by technological innovation, including wide-bandgap semiconductors, AI-enabled inverter control, and modular system architectures. Strategic initiatives such as partnerships with renewable energy developers, utility collaborations, and targeted product launches are shaping market positioning. For example, several firms have introduced high-voltage DC-DC converters for EV infrastructure and bidirectional inverters for energy storage projects. Mergers and acquisitions are being used to expand geographic reach and diversify product portfolios, with at least 12 cross-border strategic deals reported between 2023 and 2025. Smaller and regional players—over 60% of total competitors—focus on niche solutions, including microgrid inverters and industrial motor drives, emphasizing flexibility and specialized applications. Innovation trends, regulatory alignment, and localized production capabilities are increasingly becoming differentiators in this competitive landscape.

Huawei

Delta Electronics

Mitsubishi Electric

Eaton

Toshiba

General Electric

Hitachi Energy

The Power Converters and Inverters Market is experiencing rapid technological evolution, driven by efficiency demands, renewable integration, and electrification of industrial and transportation sectors. Wide-bandgap semiconductors, including silicon carbide (SiC) and gallium nitride (GaN), are being increasingly adopted, with over 42% of newly deployed industrial inverters in 2025 integrating these components. These technologies reduce switching losses by nearly 30% and enable higher operating temperatures, supporting compact designs and smaller cooling systems.

Digital and AI-enabled inverter platforms are also gaining traction, with predictive maintenance and grid-responsive control systems implemented in more than 60% of utility-scale renewable installations. These systems can reduce unplanned downtime by up to 20%, optimize load management, and improve energy conversion efficiency. Modular and prefabricated inverters are becoming standard in industrial and commercial deployments, accounting for roughly 35% of new installations, due to faster commissioning and simplified scalability.

Bidirectional converters are driving innovation in energy storage and vehicle-to-grid applications, with adoption in over 70% of new battery energy storage projects. Advanced thermal management techniques, including liquid cooling and integrated heat sinks, are improving system reliability and extending equipment life by 10–15%. Emerging trends also include the integration of IoT-enabled monitoring, cloud-based energy management, and real-time fault detection, enabling operators to remotely manage thousands of units across distributed networks.

These technological advancements collectively enhance system efficiency, operational reliability, and scalability, positioning power converters and inverters as a cornerstone for sustainable industrial operations, smart grids, and electrified transport infrastructure.

• In February 2024, Delta Electronics unveiled a three‑phase hybrid inverter designed for solar‑plus‑storage systems, enhancing performance in both residential and commercial environments and expanding its product lineup in hybrid power conversion solutions.

• In April 2024, Sungrow Power Supply announced a strategic partnership with Siemens to co‑develop high‑efficiency grid‑tied inverters and integrated storage solutions for utility‑scale solar projects, aiming to improve deployment speed and system performance.

• In June 2025, Schneider Electric launched its EcoX Inverter Series, a new line of grid‑tied and standalone inverters engineered for high‑efficiency solar‑plus‑storage applications and optimized for commercial and industrial power conversion needs.

• In March 2025, Siemens Energy secured a major contract to supply HVDC converter stations for a cross‑border European interconnector project, reinforcing its presence in high‑power grid conversion and advancing long‑distance renewable integration capabilities. (Knowledge Sourcing)

The Power Converters and Inverters Market Report provides a comprehensive examination of the power conversion ecosystem, covering segmentation across product types such as DC‑AC inverters, DC‑DC converters, AC‑DC converters, bidirectional converters, and hybrid systems. It analyzes application sectors including renewable energy integration, industrial motor drives, electric mobility infrastructure, data centers, and microgrid systems, with detailed insights into technology trends such as wide‑bandgap semiconductors, modular designs, and digital control platforms. Geographic scope spans North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, highlighting regional infrastructure dynamics, consumer behavior, and adoption patterns across utilities, commercial, and residential segments.

The report also addresses niche and emerging segments like smart inverters with IoT capabilities, grid‑forming converter technologies, and high‑power solutions suited to utility‑scale solar and energy storage deployments. It evaluates end‑user industries by usage characteristics and regulatory drivers, including electrification initiatives, grid stability requirements, and sustainability mandates. The analysis incorporates technological innovation areas such as AI‑enabled predictive maintenance, advanced thermal management, and integrated energy management systems. By synthesizing these dimensions, the scope of the report equips decision‑makers with detailed mapping of market structure, competitive positioning, technological pathways, and sector‑specific adoption trends to support strategic planning and investment decisions.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4.3% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

ABB, Siemens, Schneider Electric, Huawei, Delta Electronics, Mitsubishi Electric, Eaton, Toshiba, General Electric, Hitachi Energy |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |