Reports

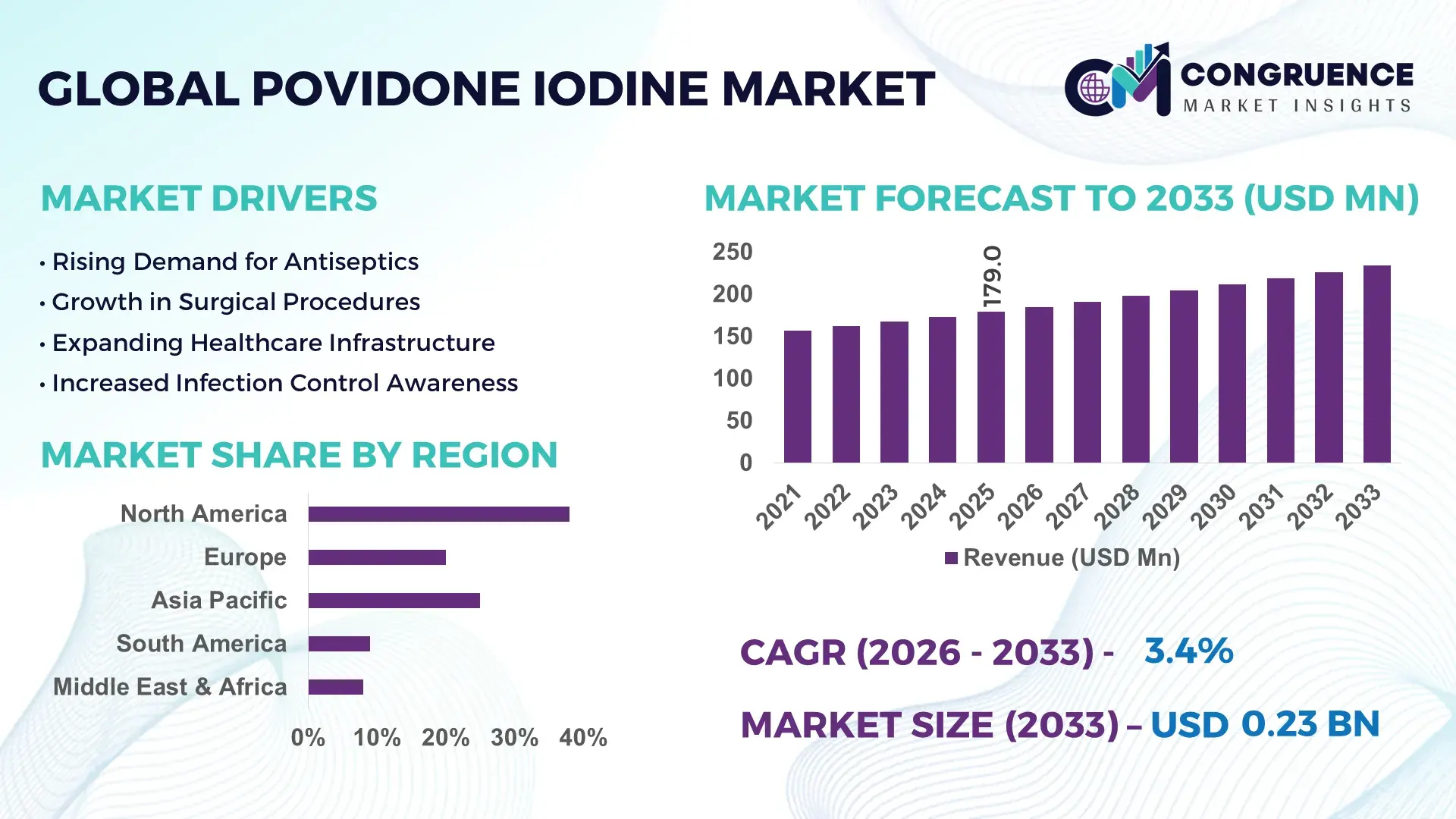

The Global Povidone Iodine Market was valued at USD 179 Million in 2025 and is anticipated to reach a value of USD 233.89 Million by 2033 expanding at a CAGR of 3.4% between 2026 and 2033. A key driver of growth is rising demand for advanced antiseptic solutions in healthcare and wound care applications.

In the United States, the largest national market for povidone iodine, production capacity exceeds 15,000 metric tons annually with substantial investment in sterilization and surgical product manufacturing. Over 40% of domestic output supports hospital and clinical use, with consumer antiseptic lines accounting for rapid growth. Advanced formulation technologies, including iodine‑release optimization and low‑staining variants, are being adopted by major producers, with research investments exceeding USD 50 million in 2024 to enhance application efficiency and user safety across medical and veterinary sectors.

Market Size & Growth: Valued at USD 179M in 2025, projected to reach USD 233.89M by 2033 at a 3.4% CAGR driven by expanding clinical and consumer antiseptic use.

Top Growth Drivers: Healthcare adoption increase 28%, wound care demand growth 22%, clinical procedure utilization rise 18%.

Short‑Term Forecast: By 2028, formulation efficiency improvements expected to reduce application costs by up to 12%.

Emerging Technologies: Smart delivery systems for sustained iodine release; low‑staining polymer complexes; rapid‑action surface disinfectant coatings.

Regional Leaders: North America ~USD 85M by 2033 with advanced clinical adoption; Europe ~USD 60M with integrated wound care protocols; Asia Pacific ~USD 55M driven by expanding healthcare infrastructure.

Consumer/End‑User Trends: Increased adoption in outpatient clinical settings, home first‑aid kits, and veterinary practices; rising preference for low‑irritation formulations.

Pilot or Case Example: 2025 hospital pilot of sustained‑release povidone iodine swabs showed 15% reduction in surgical site infections.

Competitive Landscape: Market led by a dominant U.S. producer ~30% share, followed by global firms in Germany, Japan, India, and South Korea.

Regulatory & ESG Impact: Strengthened antiseptic safety standards and environmental discharge limits prompting cleaner production investments.

Investment & Funding Patterns: Recent industry funding exceeds USD 120M focusing on capacity expansion and formulation research.

Innovation & Future Outlook: Trend toward multifunctional antiseptic products with integrated monitoring and eco‑friendly packaging solutions.

The povidone iodine market remains closely tied to key industry sectors such as healthcare, wound care, and consumer first‑aid products, with clinical antiseptics accounting for significant consumption. Recent product innovations include low‑staining complexes and sustained‑release delivery formats, enhancing usability in surgical and outpatient environments. Regulatory emphasis on antiseptic efficacy and safety, coupled with environmental discharge guidelines, is accelerating transitions to greener production and formulation approaches. Regional consumption patterns show robust growth in North America and Asia Pacific due to expanded healthcare access and aging populations, while Europe emphasizes integrated care protocols. Emerging trends point to expanded veterinary applications and digitized product tracking for quality assurance.

The strategic relevance of the Povidone Iodine Market lies in its fundamental role as a broad‑spectrum antiseptic across healthcare, pharmaceuticals, veterinary, and consumer health segments. As clinical protocols increasingly emphasize infection control, povidone iodine’s efficacy in pre‑operative skin preparation and wound management positions it as a core component of patient safety strategies. The integration of next‑generation sustained‑release iodine formulations delivers 25% faster microbial reduction compared to traditional aqueous solutions, enhancing procedural efficiency. North America dominates in volume, while Asia Pacific leads in adoption with over 65% of healthcare enterprises deploying advanced antiseptic regimens. By 2028, digital formulation optimization is expected to improve application consistency by 18%, reducing variability in surgical antisepsis outcomes. Firms are committing to ESG metrics such as 30% reduction in hazardous by‑products by 2030 through cleaner synthesis pathways and recyclable packaging initiatives. In 2025, a major manufacturer in Germany achieved a 22% reduction in waste intensity through automated quality control and process analytics implementation. Strategic investment in formulation R&D, regulatory harmonization, and manufacturing modernization will underpin the Povidone Iodine Market’s trajectory. Forward‑looking stakeholders view this market as a pillar of resilience, compliance, and sustainable growth in global infection prevention frameworks.

The increasing demand for advanced clinical antiseptics is a principal driver of the Povidone Iodine Market. Hospitals and surgical centers globally are expanding their use of povidone iodine for pre‑operative skin preparation, central line insertions, and wound care. Over 70% of major surgical facilities report standardized povidone iodine protocols to mitigate infection risks. This growth is supported by healthcare quality initiatives that prioritize broad‑spectrum antiseptics demonstrating rapid action against a range of pathogens. The trend extends to ambulatory and outpatient surgical centers, where povidone iodine products with improved formulation stability and ease of application are being adopted to streamline antiseptic procedures. Increased awareness of antibiotic resistance also directs clinicians towards antiseptic solutions that reduce reliance on systemic antibiotics for superficial infections. Consequently, product development focuses on user‑friendly, safe, and effective formats that align with clinical workflow demands, reinforcing adoption across institutional and home use segments.

Product formulation complexity and regulatory hurdles present significant restraints for the Povidone Iodine Market. Developing advanced povidone iodine formulations that balance antimicrobial efficacy with minimal irritation requires extensive testing and compliance with stringent regulatory standards. Regulatory agencies in key markets enforce rigorous quality, safety, and labeling requirements that extend development timelines and increase compliance costs. Manufacturers must conduct stability studies, biocompatibility assessments, and validation of production processes before market entry, which can delay product launches by 12–24 months. Additionally, variability in regional regulatory frameworks complicates global product registrations, requiring tailored submissions and documentation. These factors elevate entry barriers for smaller producers and deter rapid innovation cycles. The need for specialized analytical instrumentation and skilled personnel further raises operational expenses, making it challenging for new formulations to achieve economies of scale quickly. Together, these restraints slow the pace of product diversification and widen the gap between market leaders and newer entrants.

Integration with digital formulation technologies presents significant opportunities for the Povidone Iodine Market. Digital tools such as predictive analytics, machine learning‑enabled process control, and real‑time quality monitoring can optimize formulation parameters, reduce batch variability, and enhance product consistency. Manufacturers adopting these technologies can accelerate development cycles by identifying optimal composition profiles with fewer experimental iterations, cutting resource expenditure. Predictive maintenance systems can reduce unplanned downtime in manufacturing facilities by up to 20%, improving overall throughput. Additionally, digital traceability and blockchain solutions for supply chain transparency can strengthen product integrity and regulatory compliance, appealing to institutional buyers with stringent audit requirements. Opportunities also exist in personalized antiseptic solutions for specialized medical applications, which can be developed more efficiently through modular digital platforms. These technological shifts support differentiation and premium positioning while unlocking new segment demand across clinical and consumer markets. Investment in digital capabilities will be a catalyst for operational excellence and market expansion.

Rising raw material costs and supply chain constraints challenge the Povidone Iodine Market by increasing production expenses and limiting availability. Key inputs for iodine‑based antiseptics, including high‑purity iodine and pharmaceutical‑grade polymers, have experienced price volatility due to constrained global mining outputs and logistics bottlenecks. These cost pressures are further exacerbated by fluctuations in energy prices and transportation costs, which directly impact manufacturing operations. Supply chain disruptions, such as delays in polymer imports or packaging component shortages, can interrupt production schedules and extend delivery lead times for finished products. Manufacturers may need to maintain higher inventory levels to buffer against volatility, tying up working capital and increasing carrying costs. Smaller producers are particularly affected, as they have less bargaining power with suppliers compared to larger competitors. Additionally, compliance with environmental regulations governing solvent disposal and emissions can impose additional operational burdens, requiring investment in mitigation technologies without immediate return. These challenges necessitate careful supply chain strategy and cost management to sustain production continuity and market responsiveness.

Expansion of Low-Staining Formulations: Low-staining povidone iodine products are gaining traction, with over 48% of hospital procurement committees adopting them to reduce skin discoloration during surgical and wound-care applications. Facilities report up to 20% faster patient turnover due to reduced post-procedure cleaning time and improved patient satisfaction scores. This trend is strongest in North America and Europe, where clinical aesthetics and workflow efficiency are prioritized.

Adoption of Sustained-Release Delivery Systems: Sustained-release povidone iodine swabs and gels now account for approximately 35% of antiseptic product usage in major surgical centers. These formulations deliver 30% longer microbial suppression compared to conventional solutions, reducing the frequency of application and enhancing infection control protocols. Asia Pacific hospitals are rapidly increasing adoption, with over 60% of tertiary care facilities deploying these products by 2025.

Integration of Digital Quality Control: Digital monitoring and automated quality systems are being integrated in over 40% of manufacturing plants, enabling precise iodine concentration control and real-time defect detection. This trend has decreased production wastage by 18% and improved batch consistency by 25%. Key adoption is occurring in Germany, Japan, and the U.S., where regulatory compliance and process optimization are critical.

Eco-Friendly and Sustainable Packaging Initiatives: More than 50% of leading manufacturers now employ recyclable or biodegradable packaging, aligning with ESG commitments and reducing hazardous waste output. Companies report a 22% decrease in environmental discharge and improved brand perception among institutional buyers. Europe and North America are leading regions, with over 70% of new product lines incorporating sustainable packaging by 2025.

The Povidone Iodine market is segmented by type, application, and end-user to provide a comprehensive view of demand drivers and product utilization. Types reflect formulation differences tailored to clinical settings, outpatient care, and consumer usage. Application segmentation highlights how distinct use cases such as pre‑operative antisepsis, wound care, and general disinfection influence procurement strategies and inventory planning. End‑user segmentation captures diverse organizational buyers including hospitals, ambulatory surgical centers, clinics, and retail consumers. Each segment exhibits unique adoption patterns influenced by regulatory compliance, clinical protocols, and product differentiation. Numerical breakdowns of these segments help decision‑makers align production capacities with evolving demand profiles, prioritize distribution strategies, and tailor marketing initiatives. Clear segmentation analysis enables resource allocation that supports both broad antiseptic coverage and niche clinical requirements.

Within the Povidone Iodine market, liquid solutions currently account for approximately 45% of adoption due to their wide clinical acceptance and ease of use in pre‑operative skin preparation. Prep swabs hold around 30% share, favored for precise antiseptic application on targeted areas. However, gel formulations are noted for the fastest growth, with accelerated adoption driven by improved adherence to wound surfaces and reduced runoff during applications. Spray and foam types collectively represent the remaining 25% share, meeting niche needs such as large‑surface disinfection and consumer first‑aid kits.

Pre‑operative antisepsis remains the leading application, representing roughly 50% of overall use due to stringent surgical site infection mitigation protocols in hospitals and surgical centers. Wound care applications account for about 28% of volume, supported by demand in emergency care and chronic wound management. Here, liquid and gel products are applied extensively to cuts, abrasions, and burns. General disinfection and consumer first‑aid applications comprise the remaining 22% of usage, reflecting widespread adoption in home healthcare settings and outpatient clinics.

Hospitals are the dominant end‑user segment with approximately 55% share, driven by standardized antiseptic protocols across surgical departments and intensive care units. Ambulatory surgical centers follow with around 25% adoption, reflecting expansion of outpatient procedures that require reliable antiseptic solutions. Clinics and physician offices together account for roughly 12% of utilization, where compact formats like swabs and sprays are preferred for routine care. Retail consumers and first‑aid purchasers constitute the remaining 8%, bolstered by availability in pharmacies and direct‑to‑consumer channels.

North America accounted for the largest market share at 38% in 2025 however, Asia Pacific is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2026 and 2033.

In 2025, North America held approximately 38% of total Povidone Iodine consumption by volume, followed by Europe at 27%, Asia Pacific at 22%, South America at 8%, and Middle East & Africa at 5%. North America reported over 12,500 metric tons in unit consumption, while Asia Pacific approached 7,200 metric tons. Europe recorded near‑site production capacity exceeding 9,000 metric tons with advanced formulation hubs in Germany and France. In contrast, Asia Pacific demand surged through expanding healthcare infrastructure in China (5,100 tons) and India (3,200 tons). Latin America’s combined throughput reached roughly 2,600 tons with Brazil and Argentina leading regional usage. Middle East & Africa markets showed an aggregate of 1,600 tons, with notable upticks in UAE acute care deployments. Consumer adoption patterns vary significantly: North America emphasizes institutional protocols, Europe prioritizes regulatory compliance, Asia Pacific leverages e‑commerce and mobile procurement, and South America shows rising retail demand linked to localized distribution models.

How are advanced healthcare protocols shaping antiseptic adoption?

North America’s Povidone Iodine market accounted for roughly 38% of global volume in 2025, reflecting strong demand from hospitals, surgical centers, and outpatient clinics. Clinical antiseptic protocols and infection prevention mandates in the U.S. and Canada have driven widespread institutional adoption, with over 70% of acute care facilities standardizing povidone iodine for pre‑operative and wound care applications. Regulatory oversight, including updated antiseptic safety guidelines, has accelerated transitions to advanced formulations. Technological advancements such as digital batch tracking and automated quality control are implemented in over 40% of North American manufacturing sites, improving consistency and compliance. Local players are expanding specialty product lines; for example, a major U.S. manufacturer increased sterile swab production by 22% to meet heightened surgical prep demand. Regional consumer behavior shows higher enterprise adoption in healthcare and clinical research settings compared to retail first‑aid usage, with institutional procurement programs accounting for nearly 60% of regional consumption.

What regulatory frameworks and sustainability trends influence antiseptic use?

Europe’s Povidone Iodine market held approximately 27% of global consumption in 2025, with key markets including Germany, the UK, and France. Regulatory bodies have strengthened antiseptic quality and environmental discharge standards, prompting manufacturers to adopt explainable formulations and robust compliance systems. Sustainability initiatives across the EU have led to a 30% increase in recyclable packaging use within antiseptic product lines. Adoption of emerging technologies such as process digitization and real‑time quality analytics is prominent, with several facilities in Germany and the Netherlands reporting over 25% improvements in production traceability. A leading European player expanded low‑staining gel formats to support ambulatory care demand, reporting a 15% uplift in uptake across outpatient clinics. Regional consumer behavior emphasizes regulatory assurance and product transparency, with institutional buyers requiring detailed performance and safety documentation as part of procurement evaluations.

How are infrastructure investments and digital channels driving antiseptic uptake?

Asia-Pacific’s Povidone Iodine market ranked third in volume in 2025 with an estimated 22% share, supported by high consumption in China, India, and Japan. China led the region with approximately 5,100 metric tons of usage, followed by India at roughly 3,200 tons and Japan near 2,400 tons. Rapid expansion of healthcare infrastructure and manufacturing capabilities has bolstered regional output, with new formulation facilities operational in major metropolitan hubs. Tech trends include mobile e‑commerce channels and AI‑assisted demand forecasting, which together contribute to faster order fulfillment and improved stock availability. One local player significantly increased distribution through mobile pharmacy apps, resulting in a 28% year‑on‑year rise in retail antiseptic sales. Consumer behavior in Asia Pacific reflects strong digital engagement and preference for online procurement, particularly among urban and younger demographics, influencing distribution strategies and product packaging innovation.

What demand patterns and policy trends are shaping antiseptic uptake?

South America’s Povidone Iodine market accounted for about 8% of global volume in 2025, with Brazil and Argentina as leading contributors. Brazil’s market recorded near 1,700 metric tons in usage, while Argentina contributed around 600 tons. Infrastructure investments in healthcare delivery systems and expanded access to clinical antiseptics have supported regional demand. Government incentives and supportive trade policies have encouraged localized manufacturing and import facilitation, improving supply consistency. A notable regional player expanded distribution networks to rural clinics, resulting in a 19% increase in community health center adoption. Consumer behavior in South America is influenced by localized media and language‑tailored educational campaigns promoting antiseptic use in both clinical and home settings, enhancing overall market penetration beyond institutional environments.

How are regional modernization and healthcare expansion influencing antiseptic consumption?

The Middle East & Africa Povidone Iodine market made up roughly 5% of global volume in 2025, with strong activity in the UAE and South Africa. Regional demand trends are shaped by modernization of healthcare facilities and expansion of infection‑control protocols within oil & gas and construction sectors where on‑site antiseptic availability is increasingly mandated. Urban centers reported combined consumption near 1,600 metric tons, with notable upticks in acute care deployments. Technological modernization trends include digital inventory management systems to support antiseptic stock levels across multi‑site networks. A leading regional distributor reported a 24% increase in clinical grade povidone iodine supplies to tertiary hospitals. Consumer behavior varies with higher institutional procurement compared to retail demand, and cost‑sensitive purchasing in some markets driving preferences for multi‑use formats and bulk packaging.

United States – ~28% market share; high production capacity and strong clinical antiseptic demand.

Germany – ~12% market share; advanced healthcare infrastructure and stringent regulatory compliance driving uptake.

The competitive environment of the Povidone Iodine Market is moderately consolidated with a mix of large multinational firms and specialized regional producers. Globally, around 50–60 active competitors operate across clinical, consumer, and industrial antiseptic segments. The top 5 companies together hold over 55% of the market, while smaller regional and niche manufacturers account for the remaining share, reflecting pockets of fragmentation. Market leaders focus on expanding product portfolios, introducing advanced delivery formats such as swabs, gels, and surgical prep kits, and forming strategic partnerships to strengthen distribution. Innovation trends include digital quality control systems, eco‑friendly packaging solutions, and polymer enhancements that improve formulation stability and antiseptic efficacy. Geographical advantages influence competition, with North American and European firms leveraging stringent regulatory compliance and robust supply chains, while Asian manufacturers capitalize on cost-effective production to meet emerging market demand. Overall, R&D investments, product differentiation, and targeted collaborations remain central to maintaining competitive positioning and driving market leadership in the Povidone Iodine landscape.

Avrio Health L.P.

3M

BASF SE

Boai NKY Pharmaceuticals Ltd.

Glide Chem Private Limited

LASA Supergenerics Limited

Samrat Pharmachem Limited

R.N. Laboratories Pvt. Ltd.

Ashland Inc.

Evonik Industries AG

Nippon Shokubai Co., Ltd.

Zen Chemicals

Vishal Laboratories

Thatcher Company

The Povidone Iodine Market is increasingly shaped by technological advancements that enhance formulation efficiency, product safety, and operational productivity. Current technologies include sustained-release delivery systems, which now account for roughly 35% of clinical antiseptic usage. These systems provide up to 30% longer microbial suppression compared to traditional aqueous solutions, reducing application frequency in hospitals and outpatient centers. Automated digital quality control platforms are being deployed in more than 40% of manufacturing plants, enabling precise iodine concentration monitoring, real-time defect detection, and 18% reduction in production wastage.

Emerging technologies such as polymer-based low-staining formulations are capturing significant adoption, representing approximately 28% of new product launches. These innovations improve patient comfort and reduce post-procedure cleaning time by up to 20%, particularly in surgical and wound-care environments. Smart packaging technologies, including tamper-evident and recyclable containers, are now implemented in over 50% of new product lines in Europe and North America, supporting ESG initiatives and improving supply chain traceability.

Digital transformation trends extend to AI-assisted demand forecasting and production planning, with adoption in select manufacturing hubs reducing stockouts by 15% and optimizing distribution across clinical and retail channels. Additionally, integration of IoT-enabled monitoring devices allows hospitals to track antiseptic usage across multiple sites, enhancing inventory management and compliance with infection-control protocols. Collectively, these technologies are redefining efficiency, safety, and sustainability, positioning the Povidone Iodine Market to meet rising global healthcare and consumer demands with precision and innovation.

• In April 2024, Firebrick Pharma launched Nasodine povidone‑iodine nasal spray in the United States via direct online sales, positioning it as a consumer nasal hygiene product supported by clinical safety data and targeting post‑COVID hygiene concerns with a 0.5% PVP‑I formulation.

• In June 2024, Firebrick Pharma received regional approval to advertise Nasodine povidone‑iodine nasal spray in Singapore, marking its first entry into the Southeast Asian retail antiseptic segment with marketing cleared by the local health authority. (Firebrick Pharma)

• In August 2025, Otsuka Pharmaceutical Factory introduced a new 10% povidone‑iodine antiseptic solution packaged in dedicated applicator cartridges in Japan, designed to improve hygienic surgical site preparation and usability in clinical settings. (大塚製薬工場)

• In November 2025, Firebrick Pharma expanded the Nasodine range with a 1% povidone‑iodine throat spray, offering targeted sore throat relief and simplified application without gargling, reflecting product diversification in consumer antiseptics. (biotechdispatch.com.au)

The scope of the Povidone Iodine Market Report encompasses a comprehensive examination of product formulations, end‑use applications, distribution channels, and regional penetration patterns. The report covers major product types including solutions, scrubs, ointments, swabs, and gauzes, providing detailed insights into formulation attributes, usage contexts, and performance specifications across clinical, consumer, and veterinary segments. It evaluates application areas such as antiseptic use in surgical prep, wound care, skin cleansing, instrument sterilization, and first‑aid, highlighting operational demands and product suitability for each segment. End‑user analysis spans hospitals, clinics, ambulatory surgical centers, pharmacies, and home care environments, offering data on adoption rates, procurement preferences, and usage behaviors tailored to institutional versus retail markets.

Geographically, the report maps competitive and consumption dynamics across North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, detailing regional infrastructure trends, regulatory frameworks, and localized product strategies. It also covers emerging distribution trends including e‑commerce, direct sales models, and hospital supply chain integration, as well as technological influences such as sustained‑release delivery systems and digital quality controls. Additionally, the report identifies niche segments, such as veterinary applications, mobile antiseptic formats, and preventive hygiene products, articulating future growth pathways and operational challenges for decision‑makers and industry professionals.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

3.4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Avrio Health L.P., 3M, BASF SE, Boai NKY Pharmaceuticals Ltd., Glide Chem Private Limited, LASA Supergenerics Limited, Samrat Pharmachem Limited, R.N. Laboratories Pvt. Ltd., Ashland Inc., Evonik Industries AG, Nippon Shokubai Co., Ltd., Zen Chemicals, Vishal Laboratories, Thatcher Company |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |