Reports

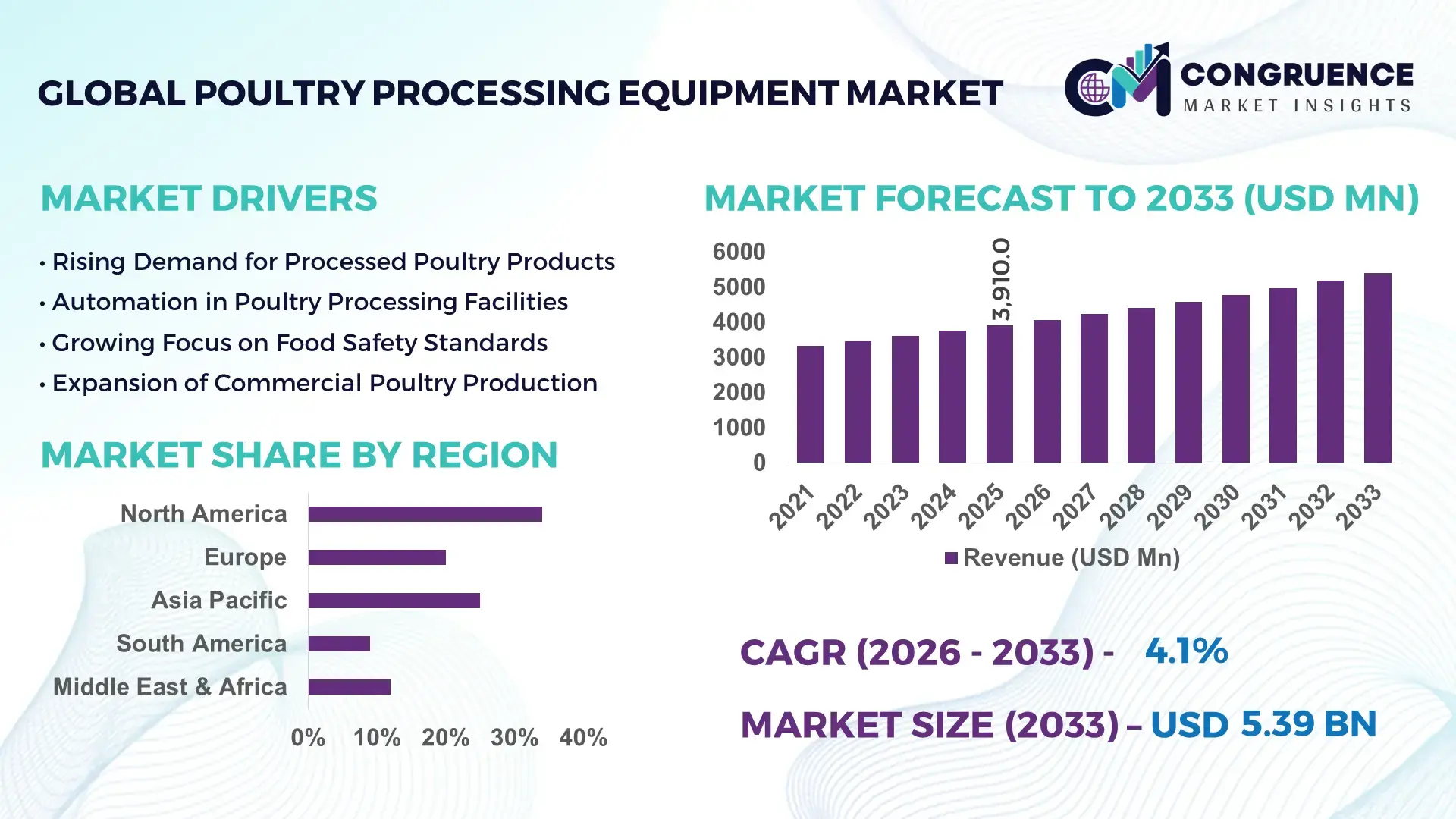

The Global Poultry Processing Equipment Market was valued at USD 3909.99 Million in 2025 and is anticipated to reach a value of USD 5392.4 Million by 2033 expanding at a CAGR of 4.1% between 2026 and 2033. Rising automation across high-capacity poultry plants, stricter food safety compliance standards, and labor optimization initiatives are accelerating investments in advanced deboning, evisceration, chilling, and robotic cut-up systems globally.

The United States dominates the global poultry processing equipment market with approximately 28% installed processing capacity, supported by over USD 1.4 billion in plant modernization investments between 2024 and 2026 and automation penetration exceeding 62% across large-scale facilities. Compared with Brazil, where export-focused processors operate at nearly 18% lower labor costs, U.S. manufacturers lead in AI-enabled inspection and yield optimization technologies. Trade disruptions linked to Red Sea shipping instability accelerated regional processing expansion strategies across North America and Europe during 2026.

Manufacturers prioritizing automated, energy-efficient poultry processing lines with integrated digital monitoring systems are securing stronger throughput efficiency, export compliance readiness, and long-term operating margin stability.

Market Size & Growth: USD 3909.99 Million in 2025 reaching USD 5392.4 Million by 2033 at 4.1% CAGR, driven by automated poultry deboning and smart processing upgrades.

Top Growth Drivers: Automation adoption rose 31%, chilled poultry demand increased 24%, and labor optimization investments expanded 19% globally.

Short-Term Forecast: By 2027, advanced processing lines improve throughput efficiency by 18% while reducing manual handling costs by 14%.

Emerging Technologies: AI vision inspection, robotic cut-up systems, and IoT-enabled monitoring improve yield accuracy by 11% across high-volume facilities.

Regional Leaders: North America exceeds USD 1.7 Billion with automation-led expansion, Asia-Pacific surpasses USD 1.5 Billion through capacity additions, and Europe crosses USD 1.2 Billion driven by compliance-focused upgrades.

Consumer/End-User Trends: Nearly 46% of integrated poultry processors prioritize automated hygienic handling systems to strengthen export-grade production consistency.

Pilot/Case Example: In 2026, a Southeast Asian poultry facility deployed robotic evisceration systems, increasing processing speed by 22% and reducing contamination incidents by 17%.

Competitive Landscape: The top five manufacturers control approximately 48% market share, led by integrated automation specialists and high-capacity equipment suppliers.

Regulatory & ESG Impact: Energy-efficient chilling systems lowered water usage by 16% as processors aligned with stricter sustainability and food safety regulations.

Investment & Funding: More than USD 2.1 Billion entered poultry processing infrastructure expansion projects amid global supply-chain diversification strategies.

Innovation & Future Outlook: Smart predictive maintenance, compact modular processing units, and AI-driven yield analytics are reshaping next-generation poultry processing operations.

Advanced poultry processing equipment demand is strengthening across automated slaughtering, deboning, chilling, and packaging applications as processors target higher throughput and export-grade hygiene standards. AI-enabled inspection systems and robotic handling technologies improved operational accuracy by nearly 15% in newly upgraded facilities during 2026. Southeast Asia and Latin America are emerging as high-growth installation hubs amid evolving food safety regulations, cold-chain investments, and regional supply-chain localization strategies, creating a strong foundation for broader strategic market expansion.

The poultry processing equipment market is becoming strategically critical as processors confront rising labor shortages, tighter export hygiene regulations, and growing pressure to increase throughput consistency. Large poultry integrators are restructuring supply chains through localized processing hubs and automated production lines to reduce logistics dependency and contamination risk. In 2026, automated cut-up and deboning installations increased by nearly 21% across high-volume facilities, while smart inspection systems reduced product rejection rates by approximately 13%, strengthening operational predictability and export compliance.

Advanced robotic evisceration systems now deliver nearly 18% faster processing speeds compared with legacy semi-automatic lines while lowering water and energy usage by around 11%. The United States continues leading high-capacity AI-integrated deployments, whereas Thailand and Poland are expanding mid-scale modular facilities focused on export-oriented poultry processing. Companies are accelerating partnerships with sensor and software providers to integrate predictive maintenance, digital yield analytics, and traceability platforms into processing operations over the next two to three years.

A leading poultry processor in Brazil recently upgraded its packaging and chilling operations using IoT-enabled monitoring systems, improving line uptime by 16% and reducing unplanned maintenance cycles. Companies prioritizing flexible automation, hygienic design standards, and digitally connected processing ecosystems are strengthening long-term competitiveness, operational resilience, and international supply-chain positioning.

Large poultry processors are accelerating investment in automated slaughtering, deboning, and packaging systems to offset labor shortages and improve throughput consistency. In 2026, automated poultry line penetration exceeded 58% across large U.S. facilities, while robotic cut-up deployment improved yield efficiency by nearly 14%. Rising export inspection requirements in Saudi Arabia, Japan, and the European Union are forcing processors to modernize hygiene and traceability systems. This operational pressure is driving equipment suppliers toward integrated AI inspection platforms and modular processing architectures. Brazilian poultry exporters expanded smart chilling infrastructure after shipping disruptions increased cold-chain handling risks by approximately 12% during peak trade cycles. Companies are responding through equipment localization partnerships, digital retrofitting programs, and multi-line automation investments to secure export reliability and improve operating margins under tighter processing timelines.

Volatile stainless-steel pricing and uneven cold-chain infrastructure remain major constraints for poultry processing equipment deployment. Industrial-grade steel input costs fluctuated between 9% and 14% across key manufacturing hubs during 2025–2026, directly increasing fabrication expenses for conveyors, cutters, and automated evisceration systems. Smaller processors in Indonesia and parts of Africa continue operating below 45% automation levels due to limited financing access and unstable utility infrastructure. Delayed equipment component deliveries linked to Red Sea shipping disruptions extended lead times by nearly 18% for some European manufacturers. These structural constraints reduce installation scalability and slow modernization cycles for mid-sized poultry operators. Companies are reducing exposure through regional supplier diversification, long-term procurement contracts, and localized assembly facilities while expanding lower-cost modular equipment offerings to penetrate infrastructure-constrained processing markets.

The strongest opportunity is emerging through modular automation systems designed for scalable poultry processing operations and mid-capacity facilities. Smart monitoring platforms integrated with AI vision inspection improved defect detection accuracy by nearly 17% during 2026 pilot deployments, while predictive maintenance systems reduced equipment downtime by approximately 15%. India and Vietnam are witnessing accelerated installation demand as domestic poultry consumption and export-oriented processing investments expand simultaneously. Governments supporting food safety modernization and traceability compliance are indirectly strengthening demand for digitally integrated processing lines. Equipment manufacturers are positioning through software partnerships, compact automation platforms, and cloud-based operational analytics tailored for regional processors. An emerging strategic advantage is the shift toward flexible processing configurations capable of switching between fresh, frozen, and value-added poultry production without extensive line restructuring, improving utilization rates and reducing idle capacity.

The market faces increasing execution challenges tied to software integration, workforce capability gaps, and operational synchronization across automated facilities. Nearly 37% of mid-sized poultry plants reported difficulties integrating AI-enabled inspection systems with legacy conveyor and cutting infrastructure during 2026 modernization programs. Cybersecurity risks linked to connected processing systems also intensified as remote equipment diagnostics and cloud monitoring adoption expanded by over 20%. Germany and the United States are experiencing shortages of skilled automation technicians capable of maintaining robotic deboning and digital traceability platforms, delaying commissioning schedules and increasing maintenance costs. These operational pressures directly affect throughput consistency, compliance reporting, and long-term productivity targets. Companies are addressing these challenges through technician training alliances, cybersecurity upgrades, and standardized software ecosystems while increasing investment in interoperable processing architectures that simplify multi-vendor equipment integration.

AI-Based Yield Optimization Poultry processors are deploying AI-enabled inspection and analytics systems to improve cut precision and reduce material waste. In 2026, intelligent yield-monitoring adoption increased by 24% across large U.S. facilities, while automated defect detection improved inspection accuracy by nearly 15%. Companies are integrating machine vision with processing software to stabilize throughput consistency amid labor shortages and stricter export compliance requirements.

Compact Modular Line Expansion Mid-capacity processors in Thailand, India, and Mexico are adopting modular slaughtering and packaging systems that reduce installation space requirements by approximately 18% and lower maintenance downtime by 12%. Rising urban poultry demand and regional cold-chain expansion are accelerating deployment of scalable processing units. Equipment suppliers are responding with flexible production configurations tailored for mixed fresh and frozen poultry operations.

Water and Energy Reduction Focus Sustainability-driven retrofitting programs are reshaping chilling and cleaning operations across poultry facilities. Advanced water recycling systems reduced plant-level water consumption by nearly 16% during recent modernization projects, while energy-efficient chilling technologies improved operational efficiency by 11%. Regulatory pressure surrounding wastewater discharge standards is pushing processors toward closed-loop sanitation infrastructure and automated hygiene control systems.

Digital Traceability System Adoption Export-oriented processors are expanding digital traceability platforms to strengthen compliance transparency and shipment reliability. RFID-integrated tracking systems improved batch monitoring speed by approximately 19% in newly upgraded European facilities during 2026. Companies are forming software partnerships and integrating cloud-based monitoring platforms to improve recall management, supply-chain visibility, and real-time operational coordination across processing networks.

Deboning Equipment represents the leading segment due to its direct impact on labor reduction, throughput optimization, and yield consistency in high-volume poultry operations. Automated deboning systems improved processing efficiency by nearly 18% across large integrated facilities during 2026, particularly in the United States and Brazil where export-focused processors prioritize uniform cut quality and reduced manual dependency. Companies are accelerating investment in AI-assisted blade control, robotic handling, and integrated vision inspection systems to improve recovery rates and minimize waste. Cutting Equipment remains strategically important for portion-controlled processing and retail-ready poultry products, especially as value-added poultry demand expands across urban foodservice channels.

Packaging Equipment is emerging as the fastest-growing segment as processors strengthen traceability, hygiene compliance, and cold-chain stability. Smart packaging line deployments increased by approximately 22% in Southeast Asia during 2025–2026 as exporters modernized operations for international trade requirements. Slaughtering Equipment continues benefiting from high-capacity facility upgrades, while Marinating Equipment is gaining traction among processors targeting premium ready-to-cook poultry products. Equipment manufacturers are prioritizing compact automation platforms, modular integration, and multi-line flexibility to strengthen competitive differentiation and long-term operational scalability.

Chicken Processing dominates the market due to its large-scale global consumption patterns, vertically integrated production systems, and extensive export infrastructure. More than 68% of newly installed poultry processing lines during 2026 were configured primarily for chicken operations, particularly across the United States, Brazil, and China. Automated chilling, cutting, and packaging systems are increasingly optimized for high-throughput chicken processing to improve consistency and reduce contamination risk. Meat Packaging also maintains strong strategic relevance as retailers and foodservice operators demand longer shelf life, traceability integration, and standardized portioning capabilities across frozen and fresh poultry supply chains.

Frozen Poultry Processing is emerging as the fastest-growing application segment as processors strengthen export logistics and cold-chain resilience. Advanced freezing and packaging automation improved operational efficiency by approximately 14% in newly upgraded facilities during 2026. Turkey Processing continues expanding steadily within North American industrial foodservice channels, while Duck Processing is gaining specialized investment momentum in China and Southeast Asia due to rising premium protein consumption. Companies are scaling integrated processing ecosystems and deploying flexible production lines capable of switching between chilled and frozen poultry output with minimal downtime.

Poultry Processing Plants remain the dominant end-user group due to continuous throughput requirements, automation intensity, and infrastructure dependency across slaughtering, deboning, chilling, and packaging operations. Large integrated facilities accounted for nearly 61% of advanced equipment deployments during 2026, particularly in the United States, Brazil, and Poland where export-oriented processors prioritize line efficiency and hygiene compliance. Companies are introducing customized multi-stage processing systems, predictive maintenance platforms, and AI-integrated monitoring tools tailored for large-scale industrial operations. Export Facilities also represent a strategically important segment as cross-border poultry trade increasingly depends on traceability integration and automated contamination control systems.

Retail Food Chains are emerging as the fastest-growing end-user segment as private-label poultry expansion and centralized packaging operations intensify. Automated packaging and labeling adoption increased by approximately 19% among large retail-linked processing networks during 2026. Food Processing Companies continue investing in portion-controlled and ready-to-cook poultry systems, while Restaurants and Hotels are gradually shifting toward pre-processed poultry sourcing models to reduce kitchen labor dependency. Equipment manufacturers are responding through modular leasing models, service-based maintenance contracts, and scalable automation packages targeting diverse buyer requirements.

North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 5.3% between 2026 and 2033.

Automation-Centric Capacity Modernization

North America maintains leadership in poultry processing equipment deployment due to large-scale vertically integrated poultry operations, advanced cold-chain infrastructure, and rapid automation adoption. The region contributes more than one-third of global automated poultry line installations, with the United States accounting for the highest concentration of AI-enabled deboning and packaging systems. In 2026, automated inspection deployment increased by approximately 23% across high-volume processing plants as labor shortages intensified operational restructuring efforts. Poultry processors are accelerating partnerships with robotics and software providers to improve throughput consistency, predictive maintenance, and export compliance. Canada is strengthening demand for energy-efficient chilling systems and digitally monitored sanitation equipment as sustainability regulations tighten across food processing operations.

United States Market Outlook: The United States remains the most strategically significant market due to its industrial-scale poultry production infrastructure and rapid deployment of intelligent processing systems. More than 62% of large poultry plants now operate partially automated deboning and packaging lines, while integrated processors continue investing in AI-driven quality inspection platforms. Expansion of domestic processing facilities across Arkansas, Georgia, and Alabama is strengthening demand for modular slaughtering systems, automated conveyors, and high-speed chilling equipment optimized for export-grade poultry operations.

Sustainability-Driven Processing Upgrades

Europe is advancing through hygiene-focused modernization, energy-efficient infrastructure deployment, and strict food traceability compliance standards. Germany, the Netherlands, and Poland remain key poultry equipment deployment hubs due to strong export-oriented poultry industries and advanced processing automation. In 2026, nearly 29% of newly installed processing systems across European facilities incorporated water-reduction and heat-recovery technologies to comply with tightening environmental standards. Poultry processors are prioritizing automated sanitation systems, smart packaging integration, and low-energy chilling infrastructure to improve operational efficiency and regulatory alignment. Equipment suppliers are expanding regional engineering partnerships to support retrofitting demand across mature poultry processing facilities operating with aging infrastructure.

Germany Market Outlook: Germany leads the European poultry processing equipment market through advanced industrial engineering capabilities and high adoption of digitally integrated processing systems. Poultry processors increasingly deploy sensor-enabled inspection technologies and automated traceability platforms to strengthen compliance efficiency and reduce contamination risk. In 2026, industrial poultry facilities in Germany expanded predictive maintenance integration by approximately 18%, improving equipment uptime and reducing operational interruptions across large-scale packaging and chilling operations.

Export Expansion and Mid-Scale Automation

Asia-Pacific is emerging as the fastest-transforming poultry processing equipment market due to rapid protein consumption growth, export-focused processing investments, and accelerated cold-chain expansion. China, Thailand, and India collectively account for a major share of new poultry processing facility construction across the region. In 2026, modular automation deployments increased by nearly 26% as mid-sized poultry processors upgraded production capabilities to meet food safety and export requirements. Poultry exporters are expanding high-speed packaging, automated evisceration, and freezing infrastructure to strengthen regional trade competitiveness. Equipment manufacturers are increasing localized assembly operations and strategic partnerships to reduce installation costs and improve servicing efficiency for emerging poultry processing clusters.

China Market Outlook: China dominates the Asia-Pacific poultry processing equipment market through large-scale poultry production capacity and aggressive processing modernization initiatives. Automated poultry handling systems and AI-assisted inspection technologies are expanding rapidly across integrated food processing enterprises. More than 38% of newly commissioned poultry processing facilities during 2026 incorporated intelligent monitoring systems and automated hygiene controls. Domestic manufacturers are also strengthening localized equipment innovation capabilities to reduce dependency on imported high-capacity poultry processing machinery.

Export-Oriented Processing Investments

South America remains a strategically important poultry processing equipment market due to its export-intensive poultry industry and expanding industrial processing infrastructure. Brazil and Argentina continue leading deployment activity through large-scale poultry slaughtering, deboning, and freezing operations focused on international trade. In 2026, automated packaging and freezing system installations increased by approximately 19% across export-focused facilities to strengthen shipment stability and hygiene compliance. Poultry processors are investing in energy-efficient chilling infrastructure and integrated monitoring systems to reduce operational waste and improve throughput consistency. However, logistics bottlenecks and fluctuating industrial input costs continue affecting equipment installation timelines and maintenance efficiency across several production hubs.

Brazil Market Outlook: Brazil remains the dominant South American market due to its large poultry export capacity and extensive vertically integrated poultry operations. Processing companies are prioritizing high-speed deboning lines, automated freezing systems, and digital yield analytics to strengthen export competitiveness. In 2026, several large poultry processors expanded automated packaging infrastructure across southern industrial clusters, improving processing line utilization by nearly 15% while reducing product handling inefficiencies during export preparation cycles.

Food Security and Infrastructure Expansion

The Middle East & Africa market is strengthening through government-backed food security initiatives, poultry infrastructure modernization, and rising investment in domestic protein processing capacity. Saudi Arabia, the United Arab Emirates, and South Africa are accelerating deployment of automated slaughtering and packaging systems to reduce import dependency and improve supply-chain resilience. In 2026, poultry processing modernization projects across Gulf countries increased smart chilling and traceability system installations by approximately 21%. Poultry operators are also investing in compact modular processing lines suited for rapidly expanding urban food distribution networks. Equipment manufacturers are entering regional partnerships to support localized servicing, workforce training, and faster deployment execution across developing poultry processing ecosystems.

Saudi Arabia Market Outlook: Saudi Arabia leads the regional market through aggressive investment in domestic poultry production infrastructure and advanced food processing modernization programs. Integrated poultry companies are deploying automated slaughtering, packaging, and hygiene monitoring systems to strengthen local production efficiency and reduce reliance on imported processed poultry products. In 2026, multiple industrial poultry facilities expanded high-capacity chilling and freezing infrastructure, improving domestic poultry handling efficiency by approximately 17% while supporting national food security objectives.

Global equipment leaders including Marel, BAADER, JBT Corporation, Middleby, and Meyn compete directly against regional automation manufacturers and cost-focused processing system suppliers across high-capacity poultry operations. The top five players collectively control nearly 48% of the market through integrated processing lines, software-enabled automation, and large-scale servicing capabilities. Competition increasingly centers on processing speed, hygiene compliance, energy efficiency, and digital integration rather than equipment pricing alone. AI-enabled inspection systems improved yield accuracy by nearly 15%, while predictive maintenance platforms reduced downtime by approximately 12%, intensifying technology-based differentiation. Companies are expanding through regional assembly facilities, automation partnerships, and vertically integrated processing ecosystems to secure long-term supply contracts. Consolidation pressure is increasing as processors prefer single-vendor automation platforms with integrated traceability systems. High capital intensity, engineering complexity, and after-sales servicing infrastructure remain major entry barriers. Winning requires scalable automation, rapid deployment capability, and strong lifecycle support networks.

Marel

BAADER Group

JBT Corporation

Meyn Food Processing Technology

Middleby Corporation

Prime Equipment Group

Bayle SA

Foodmate

CTB Inc.

Cantrell Gainco Group

Brower Equipment

Linco Food Systems

Systemate Numafa

Poultry Processing Equipment Ltd.

Advanced automation systems currently dominate poultry processing modernization strategies, particularly across deboning, evisceration, and packaging operations. AI-enabled vision inspection systems improved defect detection accuracy by nearly 15% during 2026 deployments, while automated cut-up lines reduced manual labor dependency by approximately 21%. More than 58% of large poultry processing plants now operate partially automated processing environments integrated with digital monitoring platforms. Compared with legacy semi-automatic systems, intelligent robotic deboning lines deliver nearly 18% higher throughput consistency and lower product waste. Global equipment leaders and integrated software providers benefit most as processors prioritize unified automation ecosystems over standalone machinery investments.

Emerging technologies between 2026 and 2028 are centered on predictive maintenance, cloud-based traceability, and modular smart processing architectures. IoT-enabled equipment monitoring reduced unplanned downtime by nearly 13% across newly upgraded poultry facilities, while digital sanitation systems lowered water usage by approximately 11%. Adoption of compact modular processing lines increased by 24% among mid-capacity processors in India, Thailand, and Brazil as companies targeted scalable expansion without full infrastructure replacement. Equipment suppliers are integrating AI analytics, sensor-based diagnostics, and flexible configuration capabilities to strengthen long-term operational adaptability.

Disruptive innovation is shifting toward autonomous processing workflows, digital twin simulation, and energy-optimized chilling technologies. Air-chilling systems improved energy efficiency by nearly 14% compared with traditional water-based chilling infrastructure while strengthening export-grade hygiene compliance. Companies acting early on integrated automation, intelligent traceability, and low-resource processing technologies are securing stronger operational resilience, faster regulatory alignment, and superior processing economics ahead of the next modernization cycle.

February 2024 – BAADER showcased AI-powered Smart Slaughtering and Smart Evisceration systems during IPPE Atlanta, integrating real-time diagnostics and flock reporting technologies across poultry processing operations. The company also strengthened Latin American expansion through its new Mexico hub, improving regional servicing efficiency and deployment responsiveness. Source: baader.com

March 2024 – BAADER advanced its digital poultry processing strategy through deployment of the AI-driven ClassifEYE 2.0 vision system, designed for real-time anomaly detection and production analytics. The technology improved processing monitoring precision across multiple line stages, strengthening operational transparency and predictive decision-making efficiency. Source: baader.com

December 2024 – Marel accelerated promotion of air-chilling technology for poultry processors, highlighting lower water consumption and improved processing efficiency compared with traditional immersion chilling systems. The operational shift supported sustainability-focused processing modernization and strengthened food safety positioning across export-oriented poultry production facilities. Source: meatpoultry.com

November 2025 – BAADER expanded strategic engagement with Indian poultry processors during Poultry India 2024 and subsequent regional processing initiatives, strengthening localized support partnerships and scalable automation deployment capabilities. The company intensified focus on high-speed processing factories and flexible plant layout optimization for emerging poultry infrastructure projects. Source: baader.com

The report provides comprehensive analysis of poultry processing equipment across slaughtering equipment, deboning equipment, marinating equipment, cutting equipment, and packaging equipment segments. It evaluates operational trends across chicken processing, turkey processing, duck processing, meat packaging, and frozen poultry processing applications while assessing demand patterns among poultry processing plants, export facilities, food processing companies, retail food chains, and hospitality operators. More than 55% of industrial deployment activity analyzed within the report is concentrated around automated deboning, chilling, and smart packaging systems integrated with digital monitoring technologies.

Regional assessment covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa with detailed focus on industrial modernization, automation adoption, export infrastructure, and processing capacity expansion between 2026 and 2033. The report also evaluates AI-enabled inspection systems, predictive maintenance platforms, modular automation lines, and energy-efficient chilling technologies shaping competitive positioning. Strategic insights support investment prioritization, expansion planning, partnership evaluation, technology adoption decisions, and long-term operational optimization across high-growth poultry processing ecosystems.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD 3909.99 Million |

|

Market Revenue in 2033 |

USD 5392.4 Million |

|

CAGR (2026 - 2033) |

4.1% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Type

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Marel, BAADER Group, JBT Corporation, Meyn Food Processing Technology, Middleby Corporation, Prime Equipment Group, Bayle SA, Foodmate, CTB Inc., Cantrell Gainco Group, Brower Equipment, Linco Food Systems, Systemate Numafa, Poultry Processing Equipment Ltd. |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |