Reports

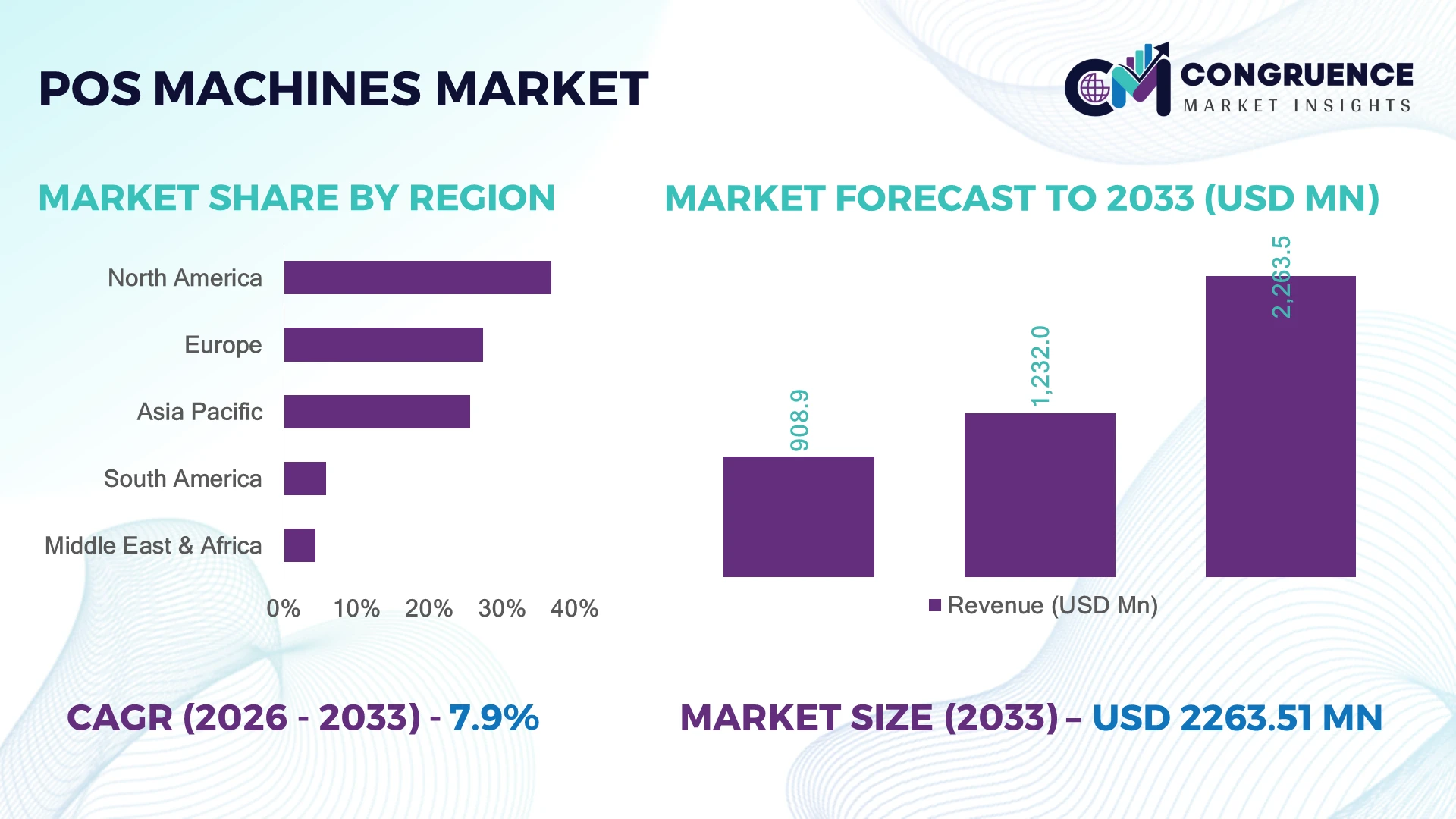

The Global POS Machines Market was valued at USD 1,232.0 Million in 2025 and is anticipated to reach a value of USD 2,263.5 Million by 2033 expanding at a CAGR of 7.9% between 2026 and 2033. The market is primarily driven by rapid contactless payment adoption, cloud-based retail management platforms, omnichannel commerce integration, and government-backed digital payment initiatives accelerating terminal modernization across retail, hospitality, healthcare, and transportation sectors.

The United States dominates the global POS Machines Market with approximately 31% market share, supported by over 9 million merchant locations, continued investments in digital payment infrastructure, and widespread adoption across retail, restaurants, and healthcare. Compared with India, where UPI-led merchant digitization is accelerating terminal deployment, the U.S. maintains higher penetration of AI-enabled and cloud-connected POS ecosystems. The modernization of payment infrastructure following post-pandemic digital commerce expansion further strengthens its leadership.

The market landscape favors vendors that prioritize software-centric POS ecosystems, secure payment technologies, and scalable cloud integration to strengthen long-term competitive positioning.

Market Size & Growth: USD 1,232.0 Million (2025) projected to reach USD 2,263.5 Million (2033) at 7.9% CAGR, supported by rapid digital payment infrastructure modernization.

Top Growth Drivers: Contactless payment adoption (+40%), cloud POS deployment (+32%), and omnichannel retail integration (+28%) continue accelerating installations.

Short-Term Forecast: By 2028, checkout efficiency improves by nearly 30% while transaction processing time declines by approximately 25% through intelligent automation.

Emerging Technologies: AI-powered analytics, cloud-native POS platforms, and NFC-enabled smart terminals redefine high-performance retail operations.

Regional Leaders: North America (~USD 760 Million), Asia-Pacific (~USD 620 Million), and Europe (~USD 500 Million) lead through retail digitalization, regional expansion, and payment ecosystem upgrades.

Consumer/End-User Trends: More than 70% of urban consumers prefer contactless or mobile-based payments, driving advanced POS deployments.

Pilot/Case Example: In 2024, large retail modernization programs reduced checkout waiting time by nearly 35% through AI-assisted POS optimization.

Competitive Landscape: The leading supplier holds approximately 18% market share, while Verifone, Ingenico, PAX Technology, NCR Voyix, and Toshiba Tec remain major competitors.

Regulatory & ESG Impact: Digital invoicing mandates and electronic payment regulations improved transaction transparency by over 30% while reducing paper receipt usage.

Investment & Funding: More than USD 3 Billion in investments supports payment technology partnerships, cloud migration, and regional manufacturing diversification amid global supply-chain realignment.

Innovation & Future Outlook: AI-driven self-service checkout, biometric authentication, and unified commerce platforms continue reshaping next-generation POS ecosystems.

The POS Machines Market continues expanding across organized retail, quick-service restaurants, hospitality, healthcare, and transportation as businesses prioritize integrated payment and operational management platforms. Vendors are introducing AI-powered analytics, Android-based smart terminals, and cloud-native software that simplify inventory, loyalty, and payment management. Nearly 65% of newly deployed terminals now support contactless transactions, while stricter digital payment compliance and semiconductor supply-chain stabilization are accelerating enterprise technology refresh cycles, setting the stage for broader strategic transformation.

The POS Machines Market has become a strategic enabler of digital commerce as retailers, hospitality operators, healthcare providers, and transportation networks modernize customer engagement and payment infrastructure. Competitive differentiation increasingly depends on integrated software ecosystems, secure payment capabilities, and real-time business intelligence rather than standalone payment hardware. Continued expansion of digital payment regulations and retail infrastructure modernization is accelerating enterprise-wide replacement of legacy terminals.

Cloud-connected POS platforms process transactions and synchronize inventory significantly faster than conventional standalone systems while reducing software maintenance costs by approximately 25% through centralized updates and remote device management. North America remains focused on AI-enabled omnichannel commerce and advanced analytics, whereas Asia-Pacific records faster deployment volumes due to rapid merchant digitization and expanding cashless payment ecosystems. Over the next two to three years, contactless-enabled terminals are expected to account for more than 80% of new commercial installations across developed retail environments.

Large retail chains are increasingly deploying unified POS platforms that combine payment processing, customer loyalty, inventory visibility, and workforce management into a single operational environment. Technology providers are expanding strategic partnerships with fintech companies, payment processors, and cloud software vendors to strengthen integrated service offerings. Organizations investing in scalable, secure, and software-defined POS ecosystems will establish stronger operational resilience, improve customer experience, and secure lasting competitive advantage in the evolving digital commerce landscape.

The rapid expansion of digital payment ecosystems and cloud-enabled retail platforms remains the primary structural driver for the POS Machines Market. More than 70% of new retail payment terminals now support contactless transactions, while cloud-based POS deployments have increased by nearly 35% among multi-store enterprises seeking centralized management and real-time analytics. India's nationwide digital payment expansion through UPI and government-backed merchant digitization has significantly accelerated terminal installations, while the United States continues upgrading enterprise payment infrastructure with AI-enabled POS platforms. This transition improves operational visibility, reduces checkout time by approximately 25%, and strengthens customer engagement. In response, leading vendors are expanding Android-based product portfolios, investing in software ecosystems, and forming partnerships with fintech providers to deliver integrated commerce solutions that extend beyond payment processing.

Despite sustained deployment momentum, infrastructure disparities and component dependency continue limiting large-scale POS implementation. Nearly 30% of small merchants in developing economies still operate with inconsistent broadband connectivity, reducing the effectiveness of cloud-based POS platforms. Semiconductor and secure-chip procurement costs remain 15–20% above pre-disruption levels in several manufacturing hubs, increasing production complexity and replacement expenses. The dependence on certified payment modules and country-specific compliance standards also slows cross-border product standardization, delaying enterprise rollouts. To reduce operational risk, manufacturers are diversifying component sourcing, expanding localized assembly operations in countries such as India and Vietnam, and negotiating long-term supplier agreements. Companies prioritizing modular hardware architectures are better positioned to manage cost volatility while maintaining deployment continuity.

The strongest emerging opportunity lies in intelligent POS ecosystems that combine payment acceptance, inventory optimization, customer analytics, and business automation within a unified platform. More than 60% of small and medium-sized businesses are prioritizing digital business management tools, while AI-powered transaction analytics can improve inventory forecasting accuracy by nearly 30%. Brazil and Indonesia are experiencing rapid merchant digitization supported by expanding fintech ecosystems and digital payment incentives, creating untapped deployment potential beyond traditional retail chains. Companies are accelerating R&D investments in embedded AI, subscription-based POS software, and open API ecosystems that simplify third-party integration. A particularly valuable opportunity is transforming POS terminals into multifunction business hubs, generating recurring software and service revenues alongside hardware sales.

Long-term competitiveness increasingly depends on the ability to integrate POS platforms securely across fragmented digital commerce environments. More than 55% of enterprise retailers operate multiple legacy retail applications, making system interoperability and migration significantly more complex. At the same time, payment-related cyberattacks continue increasing, with retail organizations reporting over 20% higher security monitoring requirements as transaction volumes expand. In the United States, evolving payment security and data privacy requirements require continuous software certification and lifecycle updates, extending implementation timelines. Vendors must strengthen cybersecurity architectures, invest in cloud-native software engineering, and deepen partnerships with payment processors and cybersecurity specialists. Organizations that deliver seamless interoperability with robust security capabilities will establish stronger operational resilience and long-term customer retention.

Android Smart POS Expansion Android-based POS terminals are becoming the preferred deployment platform, with nearly 52% of newly installed smart terminals operating on Android ecosystems and over 65% supporting third-party business applications. Enterprises are replacing proprietary systems with flexible software environments that simplify device management and application deployment. This transition reduces implementation complexity, shortens software update cycles, and improves compatibility across retail operations. Vendors are responding by expanding Android product portfolios, strengthening developer ecosystems, and integrating cloud-native business applications into next-generation payment terminals.

Cloud-Connected Commerce Integration Cloud-enabled POS platforms continue transforming enterprise operations, with cloud deployments increasing by approximately 36% and centralized device management reducing maintenance requirements by nearly 28%. Businesses are integrating payment processing, inventory management, customer loyalty, and analytics into unified operational platforms that improve visibility across multiple locations. As retailers modernize legacy infrastructure, technology providers are expanding SaaS offerings, strategic partnerships, and managed deployment services to accelerate enterprise migration while reducing IT complexity.

Contactless Payments Become Standard Contactless payment capability has become a baseline requirement, with over 90% of newly deployed POS terminals supporting NFC technology and nearly 72% of urban consumer transactions utilizing tap-to-pay or mobile wallet solutions. Financial institutions and merchants continue upgrading payment infrastructure following digital payment modernization initiatives and evolving security requirements. Manufacturers are accelerating production of multi-payment terminals featuring biometric authentication, QR code acceptance, and enhanced encryption to improve transaction speed, customer convenience, and operational resilience.

AI-Powered Operational Intelligence Artificial intelligence is transforming POS terminals into enterprise decision-support platforms. AI-enabled transaction analytics improve inventory forecasting accuracy by approximately 30%, while automated demand analysis reduces stock replenishment delays by nearly 22%. Rising labor costs and workforce shortages are encouraging retailers to automate pricing, checkout optimization, and customer engagement processes through intelligent POS ecosystems. Companies are expanding investments in predictive analytics, embedded AI software, and unified commerce platforms that enhance operational efficiency while creating recurring software and service revenue opportunities.

Fixed POS terminals remain the leading segment, accounting for approximately 57% of global installations, supported by their high processing capacity, seamless integration with enterprise resource planning (ERP) systems, and reliable operation in high-volume retail environments. Large supermarkets, department stores, pharmacies, and hospitality chains continue investing in fixed terminals because they support barcode scanners, receipt printers, cash drawers, and customer relationship management functions within a single ecosystem. Their scalability and long operational lifecycle make them the preferred choice for organized retail, particularly across the United States, Germany, and Japan. Vendors continue enhancing these systems with AI-powered analytics, cloud synchronization, and omnichannel payment capabilities to improve transaction visibility and operational efficiency. Mobile POS (mPOS) terminals represent the fastest-growing segment as businesses prioritize mobility, lower deployment costs, and flexible checkout experiences. Adoption among SMEs has increased by more than 30% over the past two years, while nearly 70% of new deployments support NFC-enabled contactless payments. Restaurants, pop-up stores, healthcare providers, and field-service businesses increasingly deploy tablet- and smartphone-based POS solutions to reduce queues and improve customer engagement. Technology providers are expanding Android-based devices, embedded payment applications, and cloud subscriptions to strengthen recurring software revenues while supporting enterprise digital transformation.

Retail remains the dominant application segment, representing nearly 40% of enterprise deployments because retailers require integrated inventory management, customer loyalty programs, omnichannel payment processing, and real-time sales analytics. Large retail chains continue replacing legacy checkout systems with cloud-enabled POS platforms that improve checkout speed by approximately 25% while supporting centralized store operations. Restaurant and hospitality applications also maintain strong demand as operators deploy tableside ordering, digital menu integration, and contactless payment solutions to improve customer experience and workforce productivity.

Healthcare is emerging as the fastest-growing application as hospitals, pharmacies, and diagnostic centers increasingly digitize patient billing and payment workflows. Mobile POS solutions reduce payment processing delays while improving patient convenience and operational transparency. Warehouse operators are integrating POS systems with inventory automation and logistics software, while entertainment venues continue adopting mobile payment terminals to reduce waiting times during peak events. Vendors are expanding industry-specific software partnerships and customized workflow solutions to strengthen adoption across specialized business environments.

Large enterprises remain the dominant buyer group, accounting for approximately 65% of enterprise POS deployments because multinational retailers, hospitality groups, healthcare networks, and supermarket chains require integrated payment infrastructure across hundreds or thousands of locations. These organizations prioritize centralized device management, cybersecurity, AI-powered analytics, and enterprise-grade cloud integration. More than 75% of large retail organizations now deploy connected POS platforms linked with inventory, CRM, and financial management systems. Technology vendors continue strengthening long-term contracts and managed service offerings to improve lifecycle support and operational continuity. Small and medium enterprises (SMEs) represent the fastest-growing end-user segment as subscription-based cloud POS platforms significantly reduce upfront investment requirements. SME adoption has increased by approximately 30% with expanding digital payment ecosystems, particularly across India, Brazil, and Southeast Asia. Businesses increasingly prefer Android-based smart terminals with integrated payment acceptance, inventory management, and customer engagement features. Vendors are responding through flexible pricing models, fintech partnerships, and bundled software subscriptions that improve affordability while expanding recurring service revenue.

North America accounted for the largest market share at 36.8% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 9.4% between 2026 and 2033.

North America maintains the leading position in the POS Machines Market through its mature digital payment ecosystem, widespread enterprise retail infrastructure, and high penetration of cloud-based business management platforms. The region accounts for 36.8% of global demand, supported by rapid replacement of legacy payment terminals with AI-enabled smart POS systems. More than 82% of organized retailers have integrated contactless payment capabilities into their checkout infrastructure, while enterprise investments increasingly focus on unified commerce platforms combining payments, inventory management, and customer analytics. Financial institutions and payment technology providers continue expanding strategic collaborations to accelerate secure payment processing, while large retailers prioritize software-driven terminal upgrades that improve operational visibility and reduce store-level management complexity.

United States Market Outlook: The United States remains the largest national market due to its extensive retail network, advanced payment infrastructure, and strong enterprise technology spending. More than 9 million merchant locations utilize electronic payment acceptance, while large retailers continue deploying AI-powered POS platforms supporting omnichannel operations. Continuous investment in payment security, cloud integration, and customer analytics enables businesses to improve transaction efficiency and operational resilience, reinforcing the country's leadership in next-generation payment technology deployment.

Europe continues strengthening its market position through payment security modernization, digital banking expansion, and widespread adoption of contactless transactions across retail and hospitality sectors. The region represents approximately 27.4% of global market activity, supported by strong compliance with electronic payment standards and increasing deployment of cloud-connected POS infrastructure. More than 75% of payment terminals support NFC-enabled transactions, while retailers continue integrating digital invoicing and inventory management capabilities into unified commerce platforms. Technology providers are expanding software partnerships and managed service offerings to simplify regulatory compliance while improving operational scalability for multi-country retail enterprises.

Germany Market Outlook: Germany serves as Europe's strategic technology hub for enterprise retail modernization and industrial payment infrastructure. Large retail chains continue replacing conventional checkout systems with intelligent POS platforms supporting centralized device management and real-time business analytics. Approximately 68% of organized retailers have completed significant payment terminal modernization initiatives, enabling stronger integration between physical stores, e-commerce operations, and enterprise resource planning systems while improving customer transaction efficiency.

Asia-Pacific represents the fastest-evolving regional market as merchant digitization, expanding organized retail, and large-scale electronics manufacturing continue accelerating POS deployment. The region contributes nearly 25.6% of global market demand while recording the highest installation momentum across small businesses and enterprise retailers. More than 70% of newly registered merchants in several major economies now accept digital payments, encouraging rapid adoption of Android-based smart terminals. Local manufacturers continue increasing production capacity while fintech companies strengthen payment ecosystems through integrated software platforms, enabling broader deployment across retail, hospitality, transportation, and healthcare sectors.

China Market Outlook: China remains the region's largest market through its advanced digital payment ecosystem, extensive POS manufacturing capabilities, and strong enterprise retail modernization. Domestic manufacturers supply a significant share of global smart POS hardware, while over 85% of urban retail transactions are supported by digital payment methods. Companies continue investing in AI-enabled payment terminals, cloud software integration, and intelligent retail automation to strengthen both domestic deployment and international competitiveness.

South America is experiencing steady POS deployment as financial inclusion initiatives and expanding digital payment ecosystems encourage merchant modernization across retail and service industries. The region accounts for approximately 5.8% of global market activity, with small and medium-sized businesses increasingly replacing cash-based operations with connected payment terminals. Contactless transaction volumes have increased by nearly 40% over recent years, while fintech partnerships continue improving payment accessibility for independent merchants. Infrastructure disparities remain across rural markets, yet technology providers are expanding affordable subscription models and localized payment solutions to strengthen long-term deployment.

Brazil Market Outlook: Brazil leads the regional market through its rapidly expanding fintech sector, large retail industry, and widespread adoption of instant digital payments. More than 65% of small merchants now utilize electronic payment terminals integrated with inventory and business management applications. Payment providers continue expanding cloud-enabled POS solutions and embedded financial services, allowing businesses to improve transaction efficiency while strengthening customer engagement across urban and semi-urban commercial centers.

The Middle East & Africa market continues advancing through smart city investments, banking modernization, and government-led cashless payment initiatives. The region contributes approximately 4.4% of global market demand while accelerating deployment across retail, hospitality, transportation, and tourism sectors. Digital payment acceptance has increased by nearly 35% among organized merchants, supported by expanding financial technology ecosystems and upgraded payment infrastructure. Technology vendors are strengthening regional partnerships, establishing local distribution networks, and introducing cloud-based POS platforms that simplify deployment while supporting secure electronic payment acceptance.

United Arab Emirates Market Outlook: The United Arab Emirates remains the region's technology leader due to its advanced digital economy, strong tourism industry, and government-backed smart commerce initiatives. More than 90% of organized retailers support contactless payment acceptance, while hospitality operators continue investing in integrated POS platforms that combine payment processing, customer engagement, and operational analytics. Continuous investment in digital infrastructure and enterprise modernization positions the country as a regional benchmark for advanced payment technology deployment.

The POS Machines Market is characterized by competition between global payment technology leaders such as Ingenico, Verifone, PAX Technology, NCR Voyix, Diebold Nixdorf, and Toshiba Tec and regional manufacturers offering cost-optimized Android-based terminals. The top five companies collectively account for approximately 58% of the global market, reflecting moderate consolidation with strong enterprise influence. Competition centers on software integration, payment security, cloud connectivity, and total ownership cost rather than hardware alone. Android-based smart POS deployments have increased by over 45%, while cloud-enabled platforms reduce maintenance costs by nearly 28%, shifting competitive priorities toward software ecosystems. Leading vendors continue expanding through fintech partnerships, AI-enabled terminal innovation, regional manufacturing, and managed payment services, whereas regional suppliers compete aggressively on pricing and localization. PCI DSS compliance requirements and payment certification remain significant entry barriers. Companies that combine secure payment infrastructure, scalable software, rapid product innovation, and global service capabilities are best positioned to outperform established competitors.

Verifone

PAX Technology

NCR Voyix

Diebold Nixdorf

Toshiba Tec Corporation

Newland Payment Technology

Castles Technology

Posiflex Technology

SUNMI Technology

BBPOS

SZZT Electronics

Fujitsu Limited

Panasonic Connect

Android-based smart POS platforms have become the dominant technology trend, replacing proprietary operating systems with open application ecosystems that support payment acceptance, inventory management, customer engagement, and business analytics through a single interface. More than 55% of newly deployed smart terminals now utilize Android architectures, while cloud-native software reduces system maintenance requirements by approximately 30% through centralized updates and remote device management. Retailers benefit from faster application deployment and simplified integration with enterprise business platforms.

Artificial intelligence, cloud computing, biometric authentication, NFC payments, SoftPOS technology, and edge analytics are reshaping payment infrastructure. AI-powered analytics improve inventory forecasting accuracy by nearly 30%, while biometric authentication reduces payment verification time by approximately 20% compared with traditional PIN-based transactions. More than 70% of newly installed enterprise terminals support contactless payment functionality, enabling higher transaction throughput and stronger customer experience. Large retailers and hospitality operators gain the greatest competitive advantage by integrating payment, loyalty, and operational intelligence within unified commerce platforms.

Between 2026 and 2028, software-defined POS ecosystems will increasingly replace hardware-centric business models. Embedded AI assistants, real-time fraud detection, digital identity verification, and API-driven payment orchestration will strengthen enterprise automation. Vendors investing in cloud-native architectures, cybersecurity, and intelligent software ecosystems will improve operational scalability, reduce deployment complexity, accelerate feature delivery, and strengthen long-term customer retention as payment infrastructure becomes increasingly service-oriented.

February 2025 – Ingenico introduced the AXIUM CX9000, an Android 14-based all-in-one POS platform integrating payment acceptance, checkout, and inventory management into a single device. The platform supports PCI and EMV V3 compliance, improving operational efficiency and simplifying enterprise retail deployments. Source: www.ingenico.com

March 2025 – Ingenico expanded the commercial rollout of the AXIUM CX9000 across international retail markets, emphasizing integrated business services and enhanced checkout performance. The solution consolidates multiple retail functions into one platform, reducing counter-space requirements while improving store productivity.

July 2025 – NCR Voyix retained its global leadership in self-checkout technology, achieving approximately 22% of worldwide self-checkout shipments during 2024. The milestone reinforces the company's position in enterprise retail automation and strengthens its competitive advantage in intelligent checkout solutions.

June 2024 – PAX Technology, Verifone, Diebold Nixdorf, Castles Technology, and other leading vendors expanded investments in virtual and cloud-connected POS ecosystems as merchants accelerated digital payment modernization. Enterprise demand increasingly shifted toward software-enabled payment platforms supporting centralized management and omnichannel commerce.

The report provides a comprehensive assessment of the global POS Machines Market across hardware platforms, software integration, enterprise deployment strategies, and evolving payment technologies. It evaluates market performance by type (Fixed POS and Mobile POS), application (Retail, Restaurant, Hospitality, Healthcare, Warehouse, Entertainment, and Others), and end-user (Large Enterprises and SMEs) while delivering detailed analysis across North America, Europe, Asia-Pacific, South America, and the Middle East & Africa. More than 70% of current enterprise deployments incorporate contactless payment capability, while Android-based smart terminals continue expanding across multiple industry verticals.

The study examines competitive positioning, technology adoption, digital payment infrastructure, AI-enabled analytics, cloud-native POS platforms, cybersecurity developments, and unified commerce ecosystems. It also evaluates deployment patterns, investment priorities, enterprise modernization strategies, regional demand distribution, and emerging business opportunities between 2026 and 2033. Strategic insights support product development, market expansion, partnership evaluation, competitive benchmarking, technology investment, and long-term decision-making for manufacturers, payment providers, investors, distributors, and enterprise customers.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,232.0 Million |

| Market Revenue (2033) | USD 2,263.5 Million |

| CAGR (2026–2033) | 7.9% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Ingenico; Verifone; PAX Technology; NCR Voyix; Diebold Nixdorf; Toshiba Tec Corporation; Newland Payment Technology; Castles Technology; Posiflex Technology; SUNMI Technology; BBPOS; SZZT Electronics; Fujitsu Limited; Panasonic Connect |

| Customization & Pricing | Available on Request (10% Customization Free) |