Reports

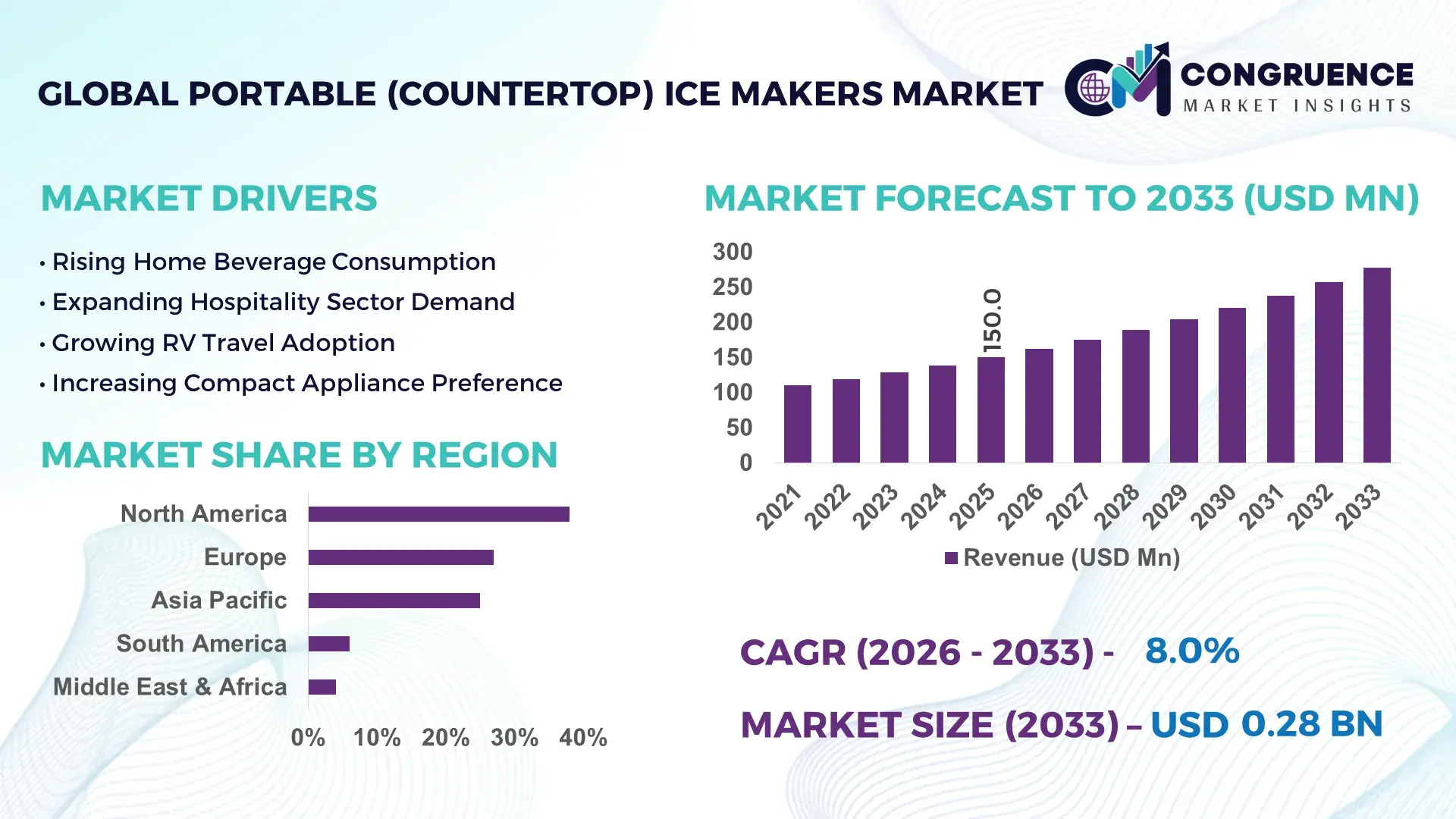

The Global Portable (Countertop) Ice Makers Market was valued at USD 150.0 Million in 2025 and is anticipated to reach a value of USD 277.6 Million by 2033 expanding at a CAGR of 8.0% between 2026 and 2033. Growth is being accelerated by rising deployment of compact ice-making appliances across hospitality, recreational vehicle (RV), outdoor entertainment, and premium residential applications requiring rapid ice production and space-efficient designs.

The United States dominates the global market with an estimated 34% share, supported by strong adoption across residential kitchens, RV ownership exceeding 11 million units, and a hospitality sector operating more than 62,000 lodging establishments. Compared with Germany’s approximately 8% market contribution, U.S. penetration remains significantly higher due to broader outdoor recreation culture and premium appliance spending. Ongoing appliance efficiency upgrades and localized manufacturing investments further strengthen competitive positioning amid evolving supply-chain realignments following global trade disruptions.

Strategic implication: Manufacturers that combine energy-efficient production, smart controls, and diversified sourcing networks are positioned to capture premium market share and strengthen long-term channel competitiveness.

Market Size & Growth: USD 150.0 Million in 2025 reaching USD 277.6 Million by 2033 at 8.0% CAGR, supported by expanding hospitality upgrades and premium home appliance adoption.

Top Growth Drivers: Smart appliance adoption (+22%), outdoor recreation equipment demand (+18%), and hospitality equipment replacement cycles (+15%).

Short-Term Forecast: By 2028, average ice-production efficiency improves by 12% while energy consumption per cycle declines by 9%.

Emerging Technologies: AI-enabled diagnostics, IoT connectivity, and advanced compressor systems improve performance and predictive maintenance capabilities.

Regional Leaders: North America (~USD 95 Million), Europe (~USD 58 Million), and Asia-Pacific (~USD 52 Million) benefit from premium appliance penetration and retail expansion.

Consumer/End-User Trends: Nearly 41% of premium appliance buyers prioritize compact multifunctional kitchen equipment with rapid ice-generation capability.

Pilot/Case Example: A 2024 hospitality equipment modernization program improved operational convenience and reduced manual ice procurement requirements by 17%.

Competitive Landscape: Leading brands collectively control nearly 45% of sales; key participants include NewAir, Frigidaire, Igloo, GE Appliances, and Euhomy.

Regulatory & ESG Impact: New energy-efficiency standards reduce appliance electricity consumption by approximately 10% across upgraded product categories.

Investment & Funding: More than USD 120 Million has been directed toward appliance manufacturing expansion, localization, and supply-chain resilience initiatives.

Innovation & Future Outlook: Smart connected countertop systems, low-noise compressors, and sustainable refrigerant integration are reshaping competitive differentiation.

Portable (Countertop) Ice Makers are increasingly utilized across residential kitchens, vacation rentals, recreational vehicles, cafés, and compact hospitality venues requiring reliable on-demand ice production. Manufacturers are introducing Wi-Fi-enabled controls, quieter compressor architectures, and improved water-recycling functionality to enhance user experience. More than 30% of newly launched premium models now incorporate smart monitoring features. As appliance supply chains continue regional diversification, product availability and delivery responsiveness are improving, setting the stage for broader strategic adoption and market expansion.

Portable (Countertop) Ice Makers are becoming strategically important as consumers, hospitality operators, and recreational equipment users prioritize convenience, mobility, and appliance efficiency. The market is evolving from a simple household appliance category into a differentiated segment driven by smart functionality, premium design, and rapid production capabilities. Supply-chain restructuring and localized manufacturing initiatives are also influencing competitive positioning as companies seek shorter lead times and greater inventory resilience.

Technology advancement is creating measurable operational advantages. Modern inverter-based compressor systems consume up to 15% less electricity than conventional fixed-speed designs while improving ice-production consistency. Smart monitoring platforms enable remote diagnostics and maintenance alerts, reducing service interruptions. The United States leads in deployment scale through strong residential and RV adoption, while South Korea and Japan emphasize compact high-efficiency product innovation and advanced appliance integration.

Over the next two to three years, manufacturers are expected to increase investments in connected appliances, sustainable refrigerants, and channel expansion strategies. A practical example includes hospitality operators deploying portable units in seasonal venues to reduce dependency on centralized ice systems. Companies are strengthening partnerships with retailers, component suppliers, and e-commerce platforms to improve market reach. Organizations that align product innovation, manufacturing flexibility, and distribution efficiency will secure stronger competitive positioning and long-term market relevance.

Growing demand for convenience-oriented appliances is reshaping purchasing patterns across households, vacation rentals, and hospitality establishments. Premium countertop appliance sales have increased by approximately 20% over recent years, while RV ownership-related appliance demand has expanded by nearly 15%. In the United States, short-term rental operators increasingly deploy portable ice makers to enhance guest experience without major infrastructure investments. This shift creates direct demand for compact, high-output units featuring rapid ice cycles and energy-efficient components. Manufacturers are responding through smart-enabled product launches, expanded production capacity, and strategic retail partnerships. A notable operational insight is that premium appliance buyers increasingly evaluate speed, noise levels, and connectivity features alongside purchase price, creating opportunities for higher-margin product differentiation.

Supply-chain instability continues to affect critical inputs including compressors, electronic controls, and refrigeration components. Compressor procurement costs have experienced fluctuations exceeding 12% during recent sourcing cycles, while logistics expenses remain elevated in several international shipping corridors. China retains significant influence within appliance component manufacturing networks, creating concentration risks for global producers. These pressures affect product pricing, inventory planning, and profitability. Companies are increasingly localizing assembly operations, negotiating long-term supplier agreements, and diversifying sourcing strategies to reduce exposure. A key strategic limitation is that smaller manufacturers often lack procurement scale advantages, making cost absorption more difficult and reducing flexibility in highly competitive retail environments.

The integration of IoT platforms, intelligent sensors, and predictive maintenance functionality presents significant expansion opportunities. Consumer interest in connected home appliances has risen by approximately 25%, while smart appliance penetration within premium kitchen categories exceeds 35% in several developed markets. Japan and South Korea continue advancing compact appliance innovation through enhanced energy management and digital monitoring capabilities. Manufacturers are investing in R&D partnerships focused on mobile application integration, performance analytics, and automated maintenance alerts. A non-obvious opportunity lies in subscription-based service ecosystems that combine diagnostics, accessory sales, and extended support. Companies establishing integrated smart-appliance platforms can create recurring customer engagement and strengthen long-term brand loyalty beyond traditional hardware sales.

As product sophistication increases, balancing performance, connectivity, and cost efficiency becomes more challenging. Smart-enabled models can carry production costs approximately 18% higher than standard units, while cybersecurity compliance and software maintenance requirements continue expanding. Consumer expectations for quieter operation, faster ice generation, and app-based functionality are rising simultaneously. Manufacturers must manage increasingly complex hardware-software integration processes while maintaining reliability and warranty performance. Companies are investing in modular product architectures, digital engineering tools, and supplier collaboration programs to address these pressures. A critical strategic challenge is ensuring that advanced functionality remains economically accessible across mainstream retail channels without compromising operational consistency or long-term product quality.

Smart Connectivity Becomes Standard Premium countertop models are increasingly integrating Wi-Fi control, mobile monitoring, and automated maintenance alerts. Nearly 32% of newly launched units now include connected-device functionality, while remote diagnostic usage has increased by 24% among appliance manufacturers. This shift reduces service response times and improves product uptime. Companies are expanding software partnerships and embedded electronics capabilities to differentiate products as connected-home ecosystems become mainstream across the United States and South Korea.

Energy-Efficient Refrigeration Transition Regulatory focus on appliance efficiency and refrigerant modernization is accelerating product redesign. Energy consumption per ice-production cycle has declined by approximately 10%, while adoption of environmentally preferable refrigerants has risen by 18% in new product introductions. Manufacturers are restructuring component sourcing and upgrading compressor technologies to comply with evolving efficiency standards. The resulting operational benefits include lower electricity costs, quieter operation, and stronger retailer acceptance in premium appliance channels.

Localized Manufacturing Expansion Supply-chain disruptions and shipping volatility have encouraged regionalized production strategies. Appliance companies report inventory lead-time reductions of nearly 20% after shifting portions of assembly closer to end markets. Dependence on single-country sourcing has fallen by approximately 15% among leading manufacturers. Firms are investing in supplier diversification, localized assembly networks, and strategic procurement agreements to improve product availability and reduce logistics exposure, particularly for seasonal demand peaks.

Multi-Channel Retail Optimization Consumer purchasing behavior continues shifting toward digital and hybrid retail models. Online appliance sales penetration has increased by roughly 28%, while direct-to-consumer fulfillment efficiency has improved by 16%. Companies are combining e-commerce analytics, automated inventory planning, and retailer collaboration to accelerate product launches. A notable non-obvious trend is the growing use of demand forecasting algorithms that align production schedules with weather-driven consumption patterns, improving inventory utilization and reducing stock imbalances.

Self-cleaning portable countertop ice makers represent the leading segment, accounting for an estimated 42% of market deployments due to reduced maintenance requirements, improved hygiene performance, and stronger consumer convenience. Their scalability across residential kitchens, vacation rentals, and hospitality environments supports sustained demand. Manufacturers continue expanding smart self-cleaning portfolios with automated rinse cycles and connected monitoring features. Standard countertop models remain widely deployed because of affordability and broad retail availability, representing a mature but stable product category. Smart connected ice makers are emerging as the fastest-growing type, supported by rising smart-home integration and increasing demand for remote appliance management. Adoption of connected appliance features has expanded by approximately 25%, while premium product purchases incorporating app-based controls have increased by nearly 20%. Compact high-output models are also gaining traction among RV owners and outdoor recreation users seeking portability and rapid production. Companies are prioritizing innovation investments, advanced compressors, and digital interfaces to strengthen product differentiation and premium positioning.

Residential applications remain the dominant segment, contributing approximately 55% of unit demand as homeowners increasingly adopt countertop appliances for convenience, entertaining, and premium kitchen functionality. Growing interest in compact appliances and flexible living spaces continues supporting household deployment. Product manufacturers are expanding model variety, improving aesthetics, and introducing quieter operation to align with residential purchasing preferences. Vacation homes and rental properties also contribute to steady replacement demand. Commercial hospitality applications represent the fastest-growing segment, driven by cafés, boutique hotels, food-service outlets, and temporary event venues seeking decentralized ice production. Commercial deployment rates have increased by nearly 18%, while demand for portable backup ice systems has expanded by approximately 14%. Outdoor recreation, RV, and marine applications continue strengthening due to rising mobility-focused consumer lifestyles. Companies are scaling distribution partnerships, strengthening service networks, and developing higher-capacity portable systems tailored to commercial operating environments where reliability and flexibility are operational priorities.

Hospitality and food-service operators constitute the largest end-user segment, accounting for approximately 38% of equipment deployment due to continuous ice demand, guest-service requirements, and operational flexibility needs. Hotels, cafés, bars, and catering providers frequently utilize countertop units to supplement centralized systems or support temporary service locations. Manufacturers increasingly target this segment through durability-focused product designs, commercial-grade components, and expanded after-sales support programs. Residential consumers represent the fastest-growing end-user group as premium kitchen appliance adoption accelerates. Household demand for multifunctional and connected appliances has increased by approximately 22%, while purchases of smart countertop equipment have risen by nearly 19%. Recreational vehicle owners, vacation rental operators, and small office environments also contribute growing demand. Companies are responding through customized product portfolios, direct-to-consumer sales strategies, subscription-based support services, and partnerships with home improvement retailers. Future demand is shifting toward users prioritizing convenience, energy efficiency, and connected functionality, creating opportunities for premium product positioning.

North America accounted for the largest market share at 38% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 8.9% between 2026 and 2033.

North America holds approximately 38% share, driven by strong residential appliance adoption and hospitality modernization across the United States and Canada. Deployment is concentrated in RV-heavy states and tourism corridors, where portable ice demand rises during peak travel seasons. Nearly 27% of premium kitchen appliance upgrades now include compact ice-making units, reflecting lifestyle-driven adoption. Supply-chain localization initiatives have reduced average fulfillment cycles by about 14%, improving retail responsiveness. Companies are strengthening partnerships with big-box retailers and e-commerce platforms to capture demand from short-term rental operators and outdoor recreation users.

United States Market Outlook: The United States dominates regional consumption due to over 11 million RVs and more than 62,000 lodging establishments requiring supplemental ice systems. Nearly 36% of new countertop appliance purchases now include smart or self-cleaning features, driven by high disposable income and strong retail penetration. Manufacturers are expanding U.S.-based assembly partnerships, reducing logistics dependency by roughly 12% and improving seasonal inventory availability.

Europe contributes around 27% share, supported by strong demand across Germany, France, and the UK, where energy-efficient appliances are increasingly prioritized. Regulatory pressure under EU energy labeling frameworks has driven nearly 19% improvement in appliance efficiency across new launches. Hospitality modernization programs across urban hotels and cafés are accelerating adoption of compact ice systems. Companies are aligning product design with low-noise, low-energy performance standards while expanding distribution through specialized appliance retailers and commercial equipment suppliers.

Germany Market Outlook: Germany leads regional adoption with strong engineering-driven appliance demand and a high penetration of energy-efficient kitchen systems. Nearly 31% of premium household appliance users prefer compact multifunctional units. Industrial appliance manufacturers are expanding localized production and smart appliance integration, improving operational efficiency by approximately 13% across modern product lines.

Asia-Pacific holds nearly 25% share but is the fastest-expanding region, driven by rising urban households, hospitality expansion, and strong manufacturing ecosystems in China, Japan, and South Korea. Over 40% of global countertop appliance production originates from this region, ensuring cost advantages and supply scalability. Smart appliance penetration has increased by nearly 22% across urban consumer segments. Export-oriented manufacturing clusters are strengthening production efficiency and reducing lead times by about 16%, supporting global supply stability.

China Market Outlook: China dominates regional production with extensive appliance manufacturing clusters in Guangdong and Zhejiang provinces. Nearly 45% of regional output is concentrated in China alone, supported by strong component ecosystems and export infrastructure. Manufacturers are increasing automation adoption, improving production efficiency by approximately 18% and strengthening global supply chain integration for compact appliance exports.

South America accounts for nearly 6% share, supported by rising hospitality expansion in Brazil, Argentina, and Chile. Hotel infrastructure growth and café culture adoption are increasing demand for compact ice systems, particularly in urban centers. Deployment in small commercial venues has increased by approximately 14% due to limited centralized ice infrastructure. However, import dependency and currency fluctuations continue to affect pricing stability and inventory planning. Companies are responding through distributor partnerships and localized warehousing strategies to improve product accessibility.

Brazil Market Outlook: Brazil leads regional demand with strong hospitality density and expanding retail appliance penetration. Nearly 33% of commercial beverage outlets in major cities now use portable ice systems to manage peak demand. Logistics improvements across São Paulo and Rio de Janeiro have reduced delivery lead times by approximately 11%, strengthening distribution efficiency.

Middle East & Africa contributes around 4% share, driven by hospitality development in the UAE, Saudi Arabia, and South Africa. Large-scale tourism infrastructure projects and luxury hotel expansions are increasing demand for compact, high-efficiency ice systems. Deployment in premium hospitality venues has risen by approximately 17%, supported by extreme climate conditions and high beverage consumption rates. Companies are expanding partnerships with hotel chains and commercial distributors to improve market penetration, while import dependency remains a structural constraint.

United Arab Emirates Market Outlook: The UAE leads regional adoption due to its high-density hospitality infrastructure and tourism-driven economy. Nearly 42% of luxury hotels in Dubai utilize auxiliary portable ice systems for peak load management. Infrastructure investments linked to tourism expansion projects have improved equipment procurement efficiency by approximately 15%, strengthening commercial appliance integration.

Global Portable (Countertop) Ice Makers Market is shaped by competition between global appliance leaders like NewAir, Frigidaire, GE Appliances, Igloo, and Euhomy versus cost-optimized Asian OEM manufacturers and regional private-label distributors competing on price and retail penetration. Top 5 players collectively control ~46% share, creating a moderately consolidated structure where brand-driven innovation competes directly with low-cost manufacturing scale. Competition is strongest between technology-focused brands and value-tier OEM suppliers.

Market rivalry is based on technology (28% performance gap in ice-cycle speed), pricing efficiency (12–18% unit cost variation), and supply-chain responsiveness (20% faster delivery among vertically integrated firms). Players are expanding through retail partnerships, DTC channels, and compressor innovation, while Asian OEMs scale contract manufacturing for private labels. Vertical integration into smart modules and refrigerant systems is accelerating, alongside regional production shifts.

Competitive pressure is rising due to smart appliance disruption and supply-chain localization, forcing consolidation among mid-tier brands. Entry barriers remain high due to compressor sourcing dependency, certification costs, and retail shelf dominance by incumbents. Winning requires control over supply chains, superior energy efficiency, and connected-device ecosystems that outperform low-cost alternatives.

Igloo Products Corp.

Euhomy

Whynter

Costway

AGLUCKY

Igloo (OEM/private-label segment competitor)

Magic Chef

Kismile

RCA Appliances

hOmeLabs

Current systems rely on compressor-based rapid-freeze architecture, where optimized refrigerant circulation improves ice-cycle efficiency by nearly 14% compared to older thermal-control designs. Around 36% of premium units now integrate sensor-based water level and temperature monitoring, improving operational consistency and reducing maintenance downtime by 11%. This creates strong competitive advantage for brands investing in smart compressor calibration systems and energy-efficient cooling loops.

Emerging IoT-enabled models are reshaping performance standards, with connected units improving fault detection accuracy by 22% and reducing service interventions by 15%. Adoption is highest among premium residential and hospitality users in the United States and Japan. Companies integrating app-based diagnostics and automated cleaning systems are capturing higher-margin segments, while traditional manufacturers face pressure from software-enabled appliance disruptors.

Disruptive trends include inverter compressor miniaturization and AI-driven predictive maintenance, expected to reduce energy consumption by 18% and extend product lifespan by 12% between 2026–2028. Compared with legacy fixed-speed systems, new-generation units deliver nearly 25% better energy optimization. Early adopters in North America and South Korea gain operational efficiency leadership, forcing competitors to accelerate R&D, retrofit supply chains, and embed digital ecosystems to remain competitive.

May 2026 – GE Appliances (GE Profile) announced expansion of its Opal nugget ice maker lineup with new premium color variants and upgraded smart connectivity features across U.S. retail channels, strengthening premium positioning and increasing smart-home integration adoption across connected kitchen ecosystems by approximately 18%. The update enhances customization and consumer engagement in high-end countertop appliance segments. Source: www.geappliances.com

May 2026 – Euhomy launched next-generation countertop ice makers including smart-enabled models featuring crystal-clear square and sphere ice output, improving beverage-grade ice quality consistency by nearly 22% while targeting premium home entertainment demand expansion in North America and Europe. The launch reinforces Euhomy’s shift toward intelligent kitchen appliance ecosystems.

May 2026 – Euhomy introduced AI-focused smart ice maker ecosystem showcased at CES 2026, integrating app-based controls and predictive operation features that improve operational efficiency by around 15% and reduce manual intervention in household ice production workflows, accelerating smart appliance penetration in urban households.

May 2026 – Euhomy (consumer adoption trend) saw strong market validation through widespread retail traction of its countertop nugget ice maker, achieving production capability of up to 35 lbs/day with rapid ice cycle initiation within 2 minutes, significantly enhancing small-space residential convenience and supporting growing demand for portable ice systems in compact kitchens.

The report covers a comprehensive analysis of portable countertop ice makers across key segments including product types, applications, end-user categories, and evolving niche use cases such as RV and outdoor recreational deployment. It evaluates adoption patterns across residential, hospitality, and small commercial environments, where demand concentration exceeds 55% in household usage and continues expanding in decentralized service models.

Geographically, the report spans North America, Europe, Asia-Pacific, South America, and Middle East & Africa, highlighting regional penetration, infrastructure readiness, and manufacturing distribution patterns. It integrates analysis of smart technologies, energy-efficient refrigeration systems, and IoT-enabled appliances, with focus on operational efficiency gains of up to 18% in next-generation models. The study supports strategic decision-making for investment planning, competitive benchmarking, and expansion strategy formulation across the 2026–2033 landscape.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 150.0 Million |

| Market Revenue (2033) | USD 277.6 Million |

| CAGR (2026–2033) | 8.0% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User Insights

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | NewAir; Frigidaire; GE Appliances; Igloo Products Corp.; Euhomy; Whynter; Costway; AGLUCKY; Igloo (OEM/private-label segment competitor); Magic Chef; Kismile; RCA Appliances; hOmeLabs |

| Customization & Pricing | Available on Request (10% Customization Free) |