Reports

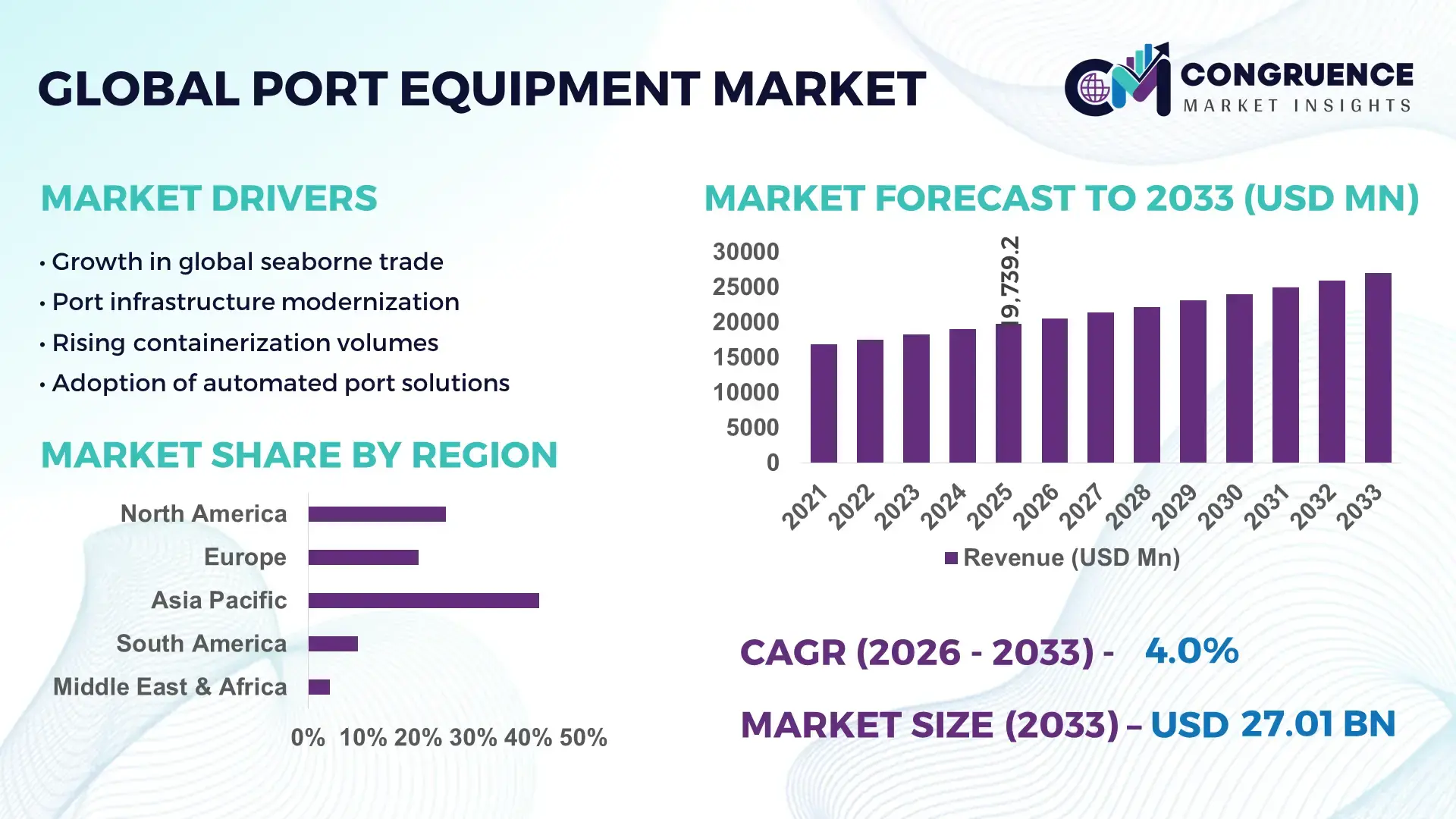

The Global Port Equipment Market was valued at USD 19,739.2 Million in 2025 and is anticipated to reach a value of USD 27,014.45 Million by 2033, expanding at a CAGR of 4% between 2026 and 2033. This growth is primarily driven by increasing global trade activities, port modernization initiatives, and rising automation in cargo handling operations.

China leads the Port Equipment Market with significant advancements in production capacity and technological integration. The country operates over 500 major port terminals, with high-capacity cranes and automated guided vehicles (AGVs) deployed extensively across coastal hubs. Annual investment in port infrastructure exceeds USD 15 Billion, emphasizing digitalization, real-time monitoring systems, and AI-driven logistics management. Key industry applications include container handling, bulk cargo operations, and intermodal transport integration. Technological innovations, such as electric-powered cranes and predictive maintenance platforms, are improving operational efficiency by 20–25%. Regional segmentation shows concentrated adoption in the Yangtze River Delta, Pearl River Delta, and Bohai Rim regions, while consumer adoption among shipping lines and logistics companies continues to expand with over 70% of operators integrating automation solutions by 2025.

Market Size & Growth: USD 19,739.2 Million in 2025; projected USD 27,014.45 Million by 2033; CAGR 4%; growth driven by port modernization and automation.

Top Growth Drivers: Automation adoption 65%, operational efficiency improvement 55%, cargo handling capacity expansion 50%.

Short-Term Forecast: By 2028, projected reduction in turnaround time by 18%, operational cost efficiency gain of 12%.

Emerging Technologies: AI-enabled cargo tracking, electric-powered cranes, predictive maintenance systems.

Regional Leaders: Asia-Pacific USD 12,450 Million (2033) – high automation uptake; Europe USD 6,230 Million – green port initiatives; North America USD 4,100 Million – advanced intermodal integration.

Consumer/End-User Trends: Shipping lines, terminal operators, and logistics providers increasingly adopt automated and remote-operated equipment for efficiency.

Pilot or Case Example: In 2024, Shanghai Port deployed AI-driven AGVs, reducing crane idle time by 22% and improving cargo handling efficiency by 15%.

Competitive Landscape: Liebherr ~18%, Konecranes, Kalmar, ZPMC, and Mitsubishi Heavy Industries.

Regulatory & ESG Impact: Compliance with IMO 2020 emissions rules, green port incentives, and carbon-reduction mandates are accelerating adoption.

Investment & Funding Patterns: USD 8.5 Billion recent investments in smart port projects; rising venture funding for automated logistics solutions.

Innovation & Future Outlook: Growth of autonomous vehicles, hybrid-electric handling equipment, and AI-based predictive analytics shaping the next-generation port ecosystem.

The Port Equipment Market is increasingly influenced by technological innovations, including hybrid-electric container cranes, automated straddle carriers, and AI-assisted scheduling systems. Key industry sectors such as container terminals, bulk cargo, and refrigerated goods handling are witnessing rapid modernization. Regulatory measures and environmental initiatives are driving cleaner, energy-efficient equipment deployment. Regional consumption shows Asia-Pacific as the primary hub for automation, while Europe focuses on sustainability and green logistics. Emerging trends include digital twin integration, remote operation centers, and predictive maintenance solutions, all contributing to enhanced productivity and future-ready port infrastructure.

The Port Equipment Market holds strategic relevance as a critical enabler of global trade efficiency, supply chain optimization, and sustainable logistics operations. Automated container cranes deliver up to 25% improvement in loading and unloading cycles compared to conventional manual cranes, reducing turnaround times and operational bottlenecks. Asia-Pacific dominates in volume, while Europe leads in adoption, with over 60% of port operators implementing automation and digital monitoring systems. By 2028, AI-driven predictive maintenance is expected to improve equipment uptime by 18%, minimizing unplanned downtime and operational disruptions. Firms are committing to ESG improvements such as a 30% reduction in carbon emissions from port machinery by 2030 through the deployment of hybrid-electric cranes and energy-efficient handling equipment. In 2024, Shanghai Port achieved a 22% reduction in idle time by integrating AI-guided automated guided vehicles (AGVs), significantly boosting throughput. Moving forward, the Port Equipment Market is poised to act as a pillar of resilience, compliance, and sustainable growth, with strategic investments in digitalization, energy-efficient solutions, and predictive technologies positioning global ports for future-ready operations and competitive advantage.

Automation and digitalization are significantly accelerating Port Equipment Market growth by enhancing operational efficiency and safety. AI-driven cranes and automated guided vehicles can handle up to 30% more containers per hour compared to traditional equipment, reducing labor dependency and turnaround times. IoT-enabled monitoring allows predictive maintenance, preventing equipment failure and minimizing downtime by 15–20%. Digitalization also provides real-time cargo tracking and operational analytics, enabling better decision-making for port operators. Investments in smart port technologies are growing rapidly, with Asia-Pacific leading adoption in over 70% of major terminals. These advancements are not only improving throughput but also reducing energy consumption and operational costs, establishing automation and digitalization as critical growth drivers in the Port Equipment Market.

The Port Equipment Market faces restraints due to substantial initial investment and ongoing maintenance costs. High-tech cranes, automated guided vehicles, and AI-driven systems require significant capital, with a single automated container crane costing upwards of USD 6–8 Million. Maintenance and software updates further increase operational expenditure, deterring small- and medium-sized ports from full-scale adoption. Additionally, integration with existing infrastructure often demands extensive retrofitting and workforce training. In developing regions, limited access to financing and skilled personnel slows technology adoption, constraining market growth. These financial and operational challenges present significant hurdles for port operators, highlighting the need for cost-efficient solutions, leasing options, and collaborative investment strategies to facilitate wider adoption.

Emerging smart port technologies present substantial opportunities for the Port Equipment Market by enabling efficiency gains and environmental compliance. The integration of AI, IoT sensors, and predictive maintenance can increase container throughput by 20–25% while reducing energy usage by up to 15%. Electrification of port equipment and deployment of hybrid cranes offer avenues for meeting stringent carbon emission standards. Expansion of intermodal transport hubs provides new opportunities for automated cargo handling and logistics optimization. In regions such as the Middle East and Southeast Asia, greenfield port projects and infrastructure modernization create a growing market for advanced handling systems. Early adoption of these innovations allows port operators to differentiate through faster service, lower operational costs, and compliance with evolving ESG requirements, opening new revenue streams and long-term strategic benefits.

The Port Equipment Market faces challenges in regulatory compliance and workforce adaptation, which impact adoption rates and operational efficiency. Strict environmental regulations, including emission reduction mandates and safety standards, require substantial investment in eco-friendly equipment and monitoring systems. Additionally, the transition from manual operations to automated systems necessitates workforce reskilling and training, which can delay implementation and increase operational costs. Legacy infrastructure may not support advanced automated equipment, requiring costly retrofits or phased upgrades. In 2024, several European ports reported a 12% slowdown in full automation deployment due to training and regulatory compliance hurdles. These challenges highlight the need for integrated planning, continuous employee development, and alignment with evolving industry standards to ensure smooth market growth.

Rise in Modular and Prefabricated Construction: The adoption of modular construction is reshaping demand dynamics in the Port Equipment market. Approximately 55% of new port infrastructure projects have reported cost reductions and schedule improvements by implementing prefabricated components. Pre-bent and pre-cut elements produced off-site using automated machinery reduce labor requirements by 30% and shorten project timelines by up to 20%. Europe and North America are leading in adoption, with 60% of major port operators integrating modular construction techniques to accelerate infrastructure modernization and improve operational efficiency.

Automation and AI Integration in Handling Equipment: Automated cranes, straddle carriers, and guided vehicles are now integrated with AI systems to optimize cargo movement. In 2025, ports using AI-enabled equipment reported a 22% reduction in idle time and a 15% increase in container throughput. Predictive maintenance driven by IoT sensors minimizes unplanned downtime by 18%, allowing operators to schedule equipment servicing proactively. Asia-Pacific dominates in volume deployment, while Europe leads adoption with over 65% of terminals utilizing AI-assisted cargo operations.

Electrification and Energy-Efficient Equipment: Electric-powered cranes and hybrid cargo handling systems are gaining traction due to environmental compliance and operational cost reduction. Over 40% of newly commissioned cranes in Asia-Pacific and Europe feature electrified drive systems, cutting energy consumption by 25% compared to diesel-powered alternatives. Port operators are also integrating solar-assisted charging stations, enabling up to 10% energy recovery during idle periods. This trend aligns with global ESG initiatives targeting a 30% reduction in port machinery emissions by 2030.

Digital Twin and Remote Monitoring Deployment: The use of digital twins and remote monitoring solutions is enhancing operational visibility and predictive analytics. Ports implementing digital twin simulations reported up to 18% faster decision-making in logistics scheduling and a 12% decrease in bottlenecks. Remote monitoring adoption has reached 50% among leading terminals in North America, allowing centralized control of multiple handling assets and reducing human error by 20%. These technologies are enabling ports to optimize workflows and improve safety while supporting data-driven expansion planning.

The Port Equipment Market is structured around three primary segmentation pillars: types, applications, and end-users. Product types include container cranes, straddle carriers, automated guided vehicles, and reach stackers, each serving distinct operational needs in port logistics. Applications range from container handling, bulk cargo operations, to intermodal transport and refrigerated goods management, reflecting the diverse operational environments in global ports. End-users span terminal operators, shipping lines, logistics service providers, and government port authorities, with adoption patterns influenced by operational scale, investment capacity, and regulatory compliance. Regional deployment varies significantly, with Asia-Pacific leading in volume, Europe focusing on automation and ESG-compliant equipment, and North America emphasizing technological integration. Emerging trends in automation, electrification, and digital twin technologies are reshaping both operational strategies and investment priorities across all segments, highlighting measurable efficiency improvements and sustainability gains.

Container cranes are the leading type in the Port Equipment Market, accounting for approximately 38% of adoption due to their essential role in high-volume container handling and operational efficiency. Straddle carriers represent the fastest-growing type, with adoption rising rapidly to support automated yard management and flexible container movement; current growth trends suggest they will surpass 25% adoption within the next decade. Automated guided vehicles (AGVs) hold a 20% share, increasingly deployed in smart port projects for reducing labor dependency and improving throughput. Reach stackers and other specialized lifting equipment collectively account for the remaining 17%, serving niche applications such as bulk cargo handling and intermodal transfers.

Container handling dominates the Port Equipment Market, representing 42% of usage due to its critical role in global trade and large-scale logistics operations. Bulk cargo operations are the fastest-growing application, driven by rising demand for raw materials and automated bulk handling technologies, with adoption projected to expand significantly by 2033. Intermodal transport accounts for 28% of applications, facilitating seamless transfers between sea, rail, and road networks, while refrigerated cargo management contributes 15%, particularly in perishables logistics. Other applications, including hazardous materials handling and breakbulk cargo, collectively account for the remaining 15%.

Terminal operators are the leading end-user segment in the Port Equipment Market, accounting for 45% of adoption due to their operational scale and investment capacity in high-efficiency equipment. Shipping lines are the fastest-growing end-user segment, leveraging automation and AI-enabled handling solutions to reduce turnaround time and improve logistics reliability, with adoption expected to rise sharply by 2033. Logistics service providers contribute 25%, using automated handling and tracking solutions to optimize supply chain operations. Government port authorities and private operators account for the remaining 15%, often focused on regulatory compliance and infrastructure modernization.

Asia-Pacific accounted for the largest market share at 42% in 2025; however, North America is expected to register the fastest growth, expanding at a CAGR of 4% between 2026 and 2033.

Asia-Pacific dominates with over 210 high-capacity ports handling 85% of regional container traffic, while Europe and North America are rapidly investing in automation and digitalized operations. In 2025, Asia-Pacific reported deployment of more than 1,200 automated guided vehicles and 750 modern container cranes, significantly improving handling efficiency by 18–22%. North America recorded adoption of 65% automated straddle carriers and energy-efficient cranes across major terminals, while Europe implemented over 40% electrified equipment in Germany, the UK, and France. South America and the Middle East & Africa together represent 18% of global deployment, driven by bulk cargo handling, trade expansion, and infrastructure modernization projects.

How is operational efficiency reshaping port logistics in the region?

North America accounts for approximately 28% of the global Port Equipment Market, driven by high-volume container and bulk cargo terminals. Key industries fueling demand include manufacturing, e-commerce, and oil & gas logistics. Regulatory incentives, such as tax credits for energy-efficient equipment and federal infrastructure grants, have accelerated adoption of hybrid-electric cranes and automated guided vehicles. Digital transformation initiatives, including AI-based predictive maintenance and remote monitoring systems, are improving terminal throughput by up to 15%. Local players, such as Konecranes’ North American division, have deployed over 50 AI-enabled container cranes in major ports like Los Angeles and Houston. Enterprise adoption is highest among large logistics operators and port authorities, while smaller terminals are gradually integrating automated solutions, emphasizing efficiency and ESG compliance.

What role do sustainability and technology adoption play in modern port operations?

Europe holds around 25% of the global Port Equipment Market, with Germany, the UK, and France as the leading contributors. Regulatory pressure from the European Union on emissions and energy efficiency has driven adoption of electrified cranes and hybrid handling equipment, with over 45% of major terminals equipped by 2025. Emerging technologies, including AI-guided container cranes and digital twin simulations, are improving operational planning and safety by 12–18%. Local players, such as Kalmar’s European operations, are deploying automated straddle carriers across Rotterdam and Hamburg, enhancing throughput efficiency. European ports prioritize regulatory compliance, resulting in higher adoption of explainable Port Equipment systems, with 60% of operators integrating sustainability metrics into operational strategies.

How is infrastructure modernization driving automation adoption in high-volume ports?

Asia-Pacific leads with 42% of global Port Equipment deployment, driven by China, India, and Japan. Over 210 high-capacity ports in the region handle the majority of container traffic, with Shanghai, Shenzhen, and Singapore implementing over 1,200 automated guided vehicles and 750 container cranes in 2025. Infrastructure modernization, such as deep-water terminal expansion and intermodal transport hubs, fuels adoption of hybrid-electric and AI-enabled handling equipment. Local players like ZPMC in China are developing next-generation automated container cranes and straddle carriers capable of reducing idle time by 20%. Regional adoption is heavily influenced by e-commerce growth and AI integration, with over 70% of large terminals utilizing smart logistics solutions.

What factors are driving the adoption of modern port equipment in emerging economies?

South America accounts for 8% of the global Port Equipment Market, with Brazil and Argentina as leading contributors. Demand is influenced by infrastructure expansion, particularly for bulk cargo and container handling in São Paulo, Santos, and Buenos Aires. Government incentives, such as tax relief for energy-efficient machinery, support modernization projects, while trade policies are enhancing import/export logistics efficiency. Local players, including CraneTech Brazil, have deployed hybrid-electric cranes that reduce fuel consumption by 18% across major terminals. Consumer behavior reflects higher adoption in commercial logistics and agribusiness, with 60% of bulk cargo operators embracing automated handling solutions.

How are technological upgrades and trade partnerships shaping port operations?

The Middle East & Africa account for 7% of the global Port Equipment Market, with the UAE, Saudi Arabia, and South Africa leading demand. Growth is driven by oil & gas logistics, construction projects, and container handling modernization. Technological upgrades include AI-enabled cranes, remote monitoring systems, and electrified straddle carriers, improving operational uptime by 15%. Local players such as DP World in the UAE are deploying autonomous yard equipment across Jebel Ali and Abu Dhabi terminals. Regional adoption varies, with energy and logistics enterprises integrating smart solutions faster than smaller commercial ports, reflecting a focus on efficiency, ESG compliance, and technological readiness.

China: 28% market share – Strong production capacity and massive port modernization projects support dominance.

Germany: 14% market share – Advanced automation adoption and regulatory emphasis on sustainability drive market leadership.

The Port Equipment Market exhibits a moderately consolidated competitive environment, with over 150 active global competitors spanning container cranes, straddle carriers, automated guided vehicles, and hybrid-electric handling systems. The top five companies—Liebherr, Konecranes, Kalmar, ZPMC, and Mitsubishi Heavy Industries—collectively account for approximately 58% of the total market share, reflecting strong leadership while leaving ample opportunities for regional and niche players. Strategic initiatives are driving competition, including product launches of AI-enabled cranes, predictive maintenance solutions, and electrified straddle carriers. Partnerships and joint ventures are increasingly common; for example, technology providers collaborate with ports to implement digital twin simulations and smart logistics platforms. Innovation trends, such as autonomous cargo handling, IoT integration, and energy-efficient machinery, are reshaping operational standards and setting new benchmarks for safety and efficiency. Regional players in Asia-Pacific are investing heavily in automated terminal equipment, while North America and Europe focus on ESG-compliant solutions. Market positioning varies, with established players emphasizing global reach and technology integration, while emerging entrants target specialized applications and mid-sized port modernization projects. Overall, competitive dynamics are influenced by technological innovation, regulatory compliance, and infrastructure expansion, reinforcing the need for strategic agility in the global Port Equipment Market.

Mitsubishi Heavy Industries

Terex Port Solutions

Cargotec

Hyundai Heavy Industries

Sany Group

Hyster-Yale Materials Handling

The Port Equipment Market is experiencing a significant technological transformation, driven by automation, electrification, and digital integration. Automated container cranes and straddle carriers now feature AI-driven control systems, improving operational efficiency by up to 22% and reducing idle time by 18%. Predictive maintenance platforms powered by IoT sensors are increasingly deployed across over 65% of major terminals in Asia-Pacific and North America, enabling real-time monitoring of crane health and preventing unplanned downtime. Electrification is another key trend, with more than 40% of new container cranes and hybrid straddle carriers operating on electric or hybrid-electric systems, reducing fuel consumption by 25% and lowering greenhouse gas emissions by 30%. Solar-assisted charging stations are being integrated in modern terminals, contributing to energy recovery and sustainability initiatives.

Digital twin simulations and remote monitoring platforms are being adopted in over 50% of European and North American ports, allowing operators to optimize cargo flow, forecast bottlenecks, and test operational strategies without interrupting terminal activities. Additionally, AI-enabled yard management software is increasing container stacking efficiency by 15–20%, while automated guided vehicles (AGVs) now handle up to 30% of container movements in smart ports. Emerging technologies, including 5G connectivity, edge computing, and blockchain-based logistics tracking, are enhancing data sharing, security, and real-time operational decision-making. These innovations collectively drive higher throughput, lower operational costs, and improved compliance with ESG and safety regulations, positioning port operators for long-term efficiency, resilience, and sustainable growth.

• In November 2025, Konecranes secured an order from Luka Koper for four additional electric Rubber‑Tired Gantry (RTG) cranes, expanding its electric yard equipment fleet. The new RTGs include Truck Lift Prevention safety technology and onboard battery packs for stack changing, with delivery planned by Q2 2026.

• In October 2025, Konecranes signed a five‑year full‑scope service agreement with OPCSA at the Port of Las Palmas, covering preventive and corrective maintenance of hybrid RTG cranes, with eight additional hybrid units slated for delivery in Q2 2026.

• In December 2025, Liebherr finalized a contract to supply two ship‑to‑shore (STS) cranes to Port Tampa Bay, marking its first STS installation on Florida’s Gulf Coast; the cranes are central to the port’s Vision 2030 expansion and expected to significantly improve berth productivity and vessel turnaround efficiency. (Liebherr)

• In March 2024, ABB and Kuenz secured the largest single order of Automatic Stacking Cranes (62 ASCs) for the Phase 2 expansion at APM Terminals Maasvlakte II in Rotterdam, enabling doubling of container handling capacity with advanced electrical and automation technologies.

The Port Equipment Market Report provides a comprehensive evaluation of global port handling systems, covering product types such as ship‑to‑shore cranes, rubber‑tyred gantry (RTG) cranes, automated guided vehicles (AGVs), straddle carriers, reach stackers, and specialized handling machinery. The report dissects market segmentation across geographic regions including North America, Europe, Asia‑Pacific, South America, and Middle East & Africa, with detailed insights into deployment volumes, equipment penetration rates, and regional adoption patterns shaped by infrastructure development and logistics modernization. It also delves into application domains such as container handling, bulk cargo operations, intermodal transport, and refrigerated goods handling, highlighting operational performance metrics like cycle time improvements and yard throughput impacts.

Technology and innovation modules explore automation systems, AI‑enabled control platforms, IoT‑based predictive maintenance, electrification trends, digital twin deployments, and green energy integrations that are redefining operational efficiency and sustainability in port ecosystems. The report further examines key market dynamics, regulatory and environmental compliance trends, and ESG‑driven equipment initiatives that influence procurement strategies. Industry focus areas also include competitive landscape analysis, strategic collaborations, product launches, service agreements, and aftermarket support trends shaping the competitive positioning of major players. Additionally, the scope encompasses niche segments such as hybrid and electric port machinery, remote operation systems, and modular construction practices, offering decision‑oriented insights tailored for equipment manufacturers, terminal operators, logistics service providers, and infrastructure investors. The report’s structured, data‑rich format ensures a holistic understanding of both current landscapes and future directions in global port equipment deployment.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End-User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Liebherr, Konecranes, Kalmar, ZPMC, Mitsubishi Heavy Industries, Terex Port Solutions, Cargotec, Hyundai Heavy Industries, Sany Group, Hyster-Yale Materials Handling |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |