Reports

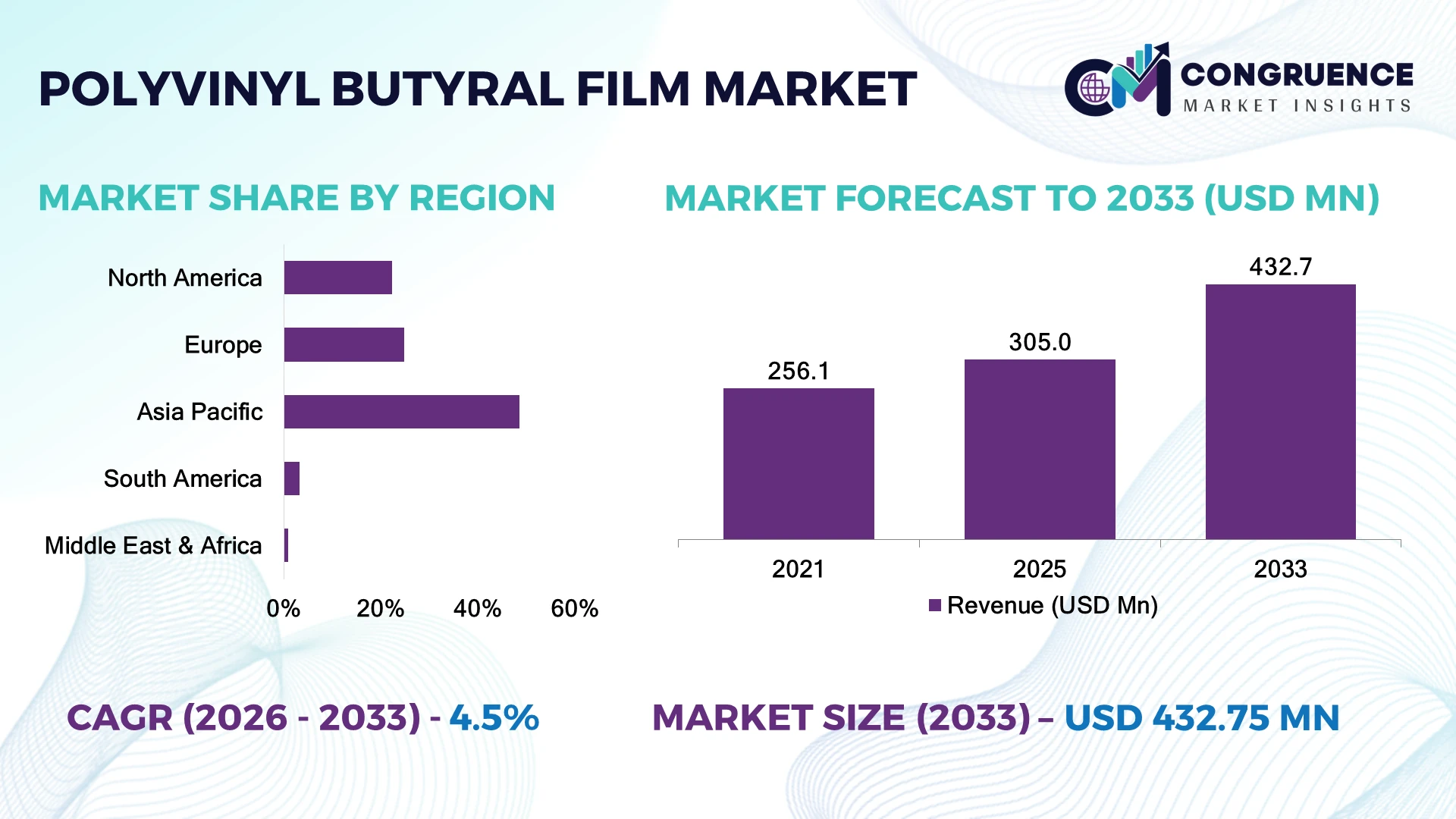

The Global Polyvinyl Butyral Film Market was valued at USD 305.0 Million in 2025 and is anticipated to reach a value of USD 432.7 Million by 2033 expanding at a CAGR of 4.5% between 2026 and 2033. Growth is primarily driven by expanding laminated safety glass production for electric vehicles, solar photovoltaic modules, and high-performance architectural glazing requiring superior impact resistance and acoustic insulation.

China leads the global market with approximately 38% of production capacity, supported by investments exceeding USD 2 billion across advanced glass manufacturing clusters serving automotive, construction, and photovoltaic industries. Compared with Germany's high-value specialty production, China delivers significantly higher manufacturing volumes, while over 62% of newly installed photovoltaic modules increasingly incorporate advanced encapsulation and protective interlayer technologies amid global clean-energy expansion.

Manufacturers are strengthening regional production networks and premium material portfolios to secure long-term supply resilience and competitive differentiation across automotive, construction, and renewable energy value chains.

Market Size & Growth: USD 305.0 Million in 2025, reaching USD 432.7 Million by 2033 at 4.5% CAGR, supported by expanding EV glazing and solar module production.

Top Growth Drivers: Automotive laminated glass demand (+18%), photovoltaic installations (+21%), and green building adoption (+15%) continue accelerating market expansion.

Short-Term Forecast: By 2028, manufacturing waste is projected to decline by nearly 12% through advanced extrusion automation and process optimization.

Emerging Technologies: AI-driven quality inspection, multilayer extrusion, and advanced acoustic PVB films improve consistency, durability, and production efficiency.

Regional Leaders: Asia Pacific approaches USD 180 Million, Europe exceeds USD 110 Million, and North America nears USD 82 Million with localized manufacturing expansion.

Consumer/End-User Trends: More than 65% of premium passenger vehicles now incorporate laminated glazing for enhanced safety and cabin comfort.

Pilot/Case Example: In 2024, a smart automotive glass manufacturing upgrade improved inspection accuracy by approximately 20% while reducing production defects.

Competitive Landscape: Eastman controls roughly 17% market share alongside Kuraray, Sekisui Chemical, EVERLAM, and Chang Chun Group.

Regulatory & ESG Impact: Tougher vehicle safety and energy-efficiency regulations contribute to approximately 14% higher adoption of advanced laminated glazing solutions.

Investment & Funding: More than USD 900 Million has been committed toward capacity expansion, strategic partnerships, and advanced film manufacturing across Asia and Europe.

Innovation & Future Outlook: High-performance acoustic, UV-resistant, and recyclable PVB films are strengthening product differentiation as regional supply chains continue evolving.

Polyvinyl Butyral Film is gaining stronger adoption across automotive glazing, photovoltaic modules, and energy-efficient architectural glass as manufacturers prioritize durability and safety performance. Advanced multilayer film technologies and precision extrusion are improving product consistency, while nearly 22% of new premium glazing solutions incorporate enhanced acoustic functionality. Regional supply-chain diversification and stricter safety regulations continue encouraging localized production and material innovation, setting the stage for broader strategic market developments.

The Polyvinyl Butyral Film Market has become strategically important as automotive electrification, renewable energy deployment, and sustainable construction reshape material procurement priorities worldwide. Companies are strengthening regional manufacturing footprints while reducing dependence on single-country sourcing to improve operational resilience and delivery reliability. Regulatory emphasis on safer laminated glass and energy-efficient buildings is also accelerating long-term procurement commitments.

Modern multilayer extrusion technology delivers approximately 15% higher production efficiency and reduces material waste by nearly 10% compared with conventional processing systems, allowing manufacturers to improve quality consistency while lowering operational costs. Asia Pacific continues leading large-scale production and capacity expansion, whereas Europe focuses on premium acoustic and specialty interlayer innovations for high-performance automotive and architectural applications. During the next two to three years, automation adoption across advanced film production facilities is expected to exceed 55%, improving throughput and quality assurance.

Several producers are expanding localized manufacturing facilities near automotive and photovoltaic hubs while forming technology partnerships with glass processors to shorten delivery cycles and strengthen customer integration. These operational strategies enhance competitive positioning, improve supply-chain flexibility, and establish a durable foundation for long-term industrial leadership across global end-use sectors.

Expanding production of electric vehicles, solar photovoltaic modules, and energy-efficient buildings is accelerating demand for advanced polyvinyl butyral films with superior impact resistance and optical clarity. More than 70% of automotive windshields globally already use laminated safety glass, while over 60% of newly installed building façades in developed economies incorporate laminated glazing for safety and acoustic performance. China's continued investment in electric vehicle manufacturing and photovoltaic capacity is strengthening downstream demand for advanced interlayer materials. This structural shift is encouraging manufacturers to expand specialty film production, introduce high-acoustic and UV-resistant grades, and establish long-term supply agreements with automotive OEMs and architectural glass processors, improving product differentiation and operational resilience.

Polyvinyl alcohol and plasticizer availability remains closely linked to petrochemical feedstock pricing, creating persistent cost uncertainty for film manufacturers. Feedstock prices have experienced fluctuations exceeding 18% during recent supply-chain disruptions, while logistics costs in several international trade corridors increased by nearly 14% during periods of shipping constraints. Japan and China continue supplying a significant share of specialty raw materials, increasing procurement concentration for global manufacturers. Companies are responding by qualifying multiple suppliers, increasing localized sourcing, and negotiating long-term procurement contracts to stabilize production costs. Strengthening regional supply networks has become a strategic priority for protecting manufacturing continuity and improving pricing competitiveness.

Next-generation laminated glass applications are creating new value opportunities beyond conventional automotive glazing. More than 30% of premium commercial buildings now integrate high-performance glazing technologies that improve energy efficiency and occupant comfort, while smart glass installations continue expanding across infrastructure projects. Germany is accelerating sustainable building initiatives that encourage adoption of advanced laminated glazing systems with improved thermal and acoustic characteristics. Manufacturers are investing in recyclable interlayer technologies, multifunctional films, and precision extrusion platforms while collaborating with photovoltaic module producers and specialty glass fabricators. Developing lightweight, high-durability films capable of supporting smart building integration provides a strong competitive advantage and unlocks premium application segments.

Maintaining consistent optical performance and adhesion properties across large-scale production remains a significant operational challenge as product specifications become increasingly demanding. Premium automotive glazing applications typically require defect rates below 1%, while automated inspection systems can improve quality detection accuracy by approximately 20%. The United States continues increasing quality and traceability requirements for automotive safety components, placing greater pressure on production control systems. Manufacturers must invest in digital quality monitoring, advanced process automation, workforce training, and predictive maintenance to achieve stable high-volume output. Successfully integrating these capabilities will determine long-term competitiveness, customer retention, and qualification for high-value automotive and architectural glazing programs.

High-Performance Automotive Glazing: Automotive OEMs are rapidly shifting toward acoustic and lightweight laminated glazing, with more than 68% of premium passenger vehicles incorporating advanced PVB interlayers and nearly 24% higher adoption in electric vehicle platforms. Stricter vehicle safety standards and lightweight design targets are accelerating product upgrades. Manufacturers are expanding dedicated automotive production lines, increasing automation, and strengthening long-term partnerships with laminated glass fabricators to improve delivery speed and production flexibility.

Localized Manufacturing Expansion: Supply-chain diversification continues reshaping production strategies as over 42% of manufacturers increase regional sourcing and nearly 30% expand localized converting operations to reduce logistics risks. Ongoing trade policy adjustments and transportation disruptions are encouraging companies to shorten procurement cycles and establish manufacturing closer to automotive and construction clusters. Enterprises are restructuring supplier networks while investing in digital inventory planning to improve operational resilience and reduce lead-time variability.

Advanced Functional Film Development: Demand for UV-resistant, acoustic, and solar-control PVB films is strengthening across architectural and photovoltaic applications. Approximately 36% of newly launched specialty glazing products now integrate multifunctional interlayers, while automated optical inspection has improved production accuracy by nearly 18%. Companies are accelerating product development, scaling precision extrusion technologies, and collaborating with glass processors to deliver differentiated high-value performance solutions for commercial infrastructure projects.

Circular Material Processing: Sustainability initiatives are increasing recycled material utilization, with nearly 28% of manufacturers investing in closed-loop recovery systems and approximately 22% improving production waste recovery through advanced processing technologies. Environmental compliance requirements and customer sustainability targets are encouraging broader adoption of recyclable interlayer solutions. Producers are modernizing manufacturing facilities, integrating resource-efficient operations, and developing circular production models that lower material losses while strengthening long-term competitiveness.

Standard PVB Film dominates the market with approximately 61% share due to its established use in automotive windshields and architectural laminated glass. Its excellent adhesion, optical clarity, and cost efficiency continue supporting large-scale deployment across mature manufacturing ecosystems. Acoustic PVB Film represents the fastest-growing segment as vehicle manufacturers increasingly prioritize cabin noise reduction and premium passenger comfort. UV-resistant PVB Film is also gaining momentum through expanding photovoltaic installations and energy-efficient glazing projects where long-term durability is becoming increasingly important. Colored and specialty functional PVB films continue serving niche applications including decorative glazing, security installations, and advanced infrastructure projects. Manufacturers are expanding premium product portfolios through multilayer structures, customized formulations, and enhanced processing technologies to capture higher-value applications. Investment priorities are steadily shifting toward differentiated films capable of delivering multiple functional properties while maintaining compatibility with high-speed glass lamination processes.

Automotive laminated glass remains the leading application, accounting for approximately 56% of total demand due to continuous vehicle production and increasingly stringent occupant safety requirements. Architectural laminated glass represents the second-largest application, supported by rising investments in energy-efficient commercial buildings and public infrastructure. Photovoltaic modules are emerging as the fastest-growing application as advanced encapsulation and protective glazing become increasingly important for long-term panel reliability. Security glazing, hurricane-resistant windows, and specialty transportation applications continue expanding as infrastructure modernization creates new demand for impact-resistant laminated glass. Nearly 35% of newly developed commercial glazing projects now integrate multifunctional laminated glass systems, while automated lamination processes have improved manufacturing throughput by approximately 16%. Companies are expanding production capacity, strengthening relationships with glass processors, and optimizing product portfolios to serve rapidly evolving end-use requirements across multiple industries.

The automotive industry accounts for approximately 52% of total Polyvinyl Butyral Film consumption, driven by continuous demand for laminated windshields, panoramic roofs, and advanced side glazing systems. Construction is the second-largest end-user owing to expanding investments in commercial buildings, airports, hospitals, and sustainable infrastructure. The renewable energy sector represents the fastest-growing end-user group as solar module manufacturers increase deployment of protective laminated glass for enhanced operational durability. Transportation infrastructure, industrial manufacturing, and specialty security applications continue expanding their procurement volumes as operational standards become increasingly performance-driven. More than 40% of manufacturers are introducing customized product grades tailored to specific end-user performance requirements, while nearly 26% have expanded collaborative development programs with downstream glass processors. Companies are strengthening application-specific product strategies, pricing models, and technical support capabilities to improve long-term customer retention and competitive positioning.

Asia-Pacific accounted for the largest market share at 48.6% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 5.2% between 2026 and 2033.

North America represents approximately 22.4% of the global Polyvinyl Butyral Film Market, supported by advanced automotive manufacturing, modern architectural construction, and expanding photovoltaic installations. Premium laminated glazing adoption continues increasing across electric vehicles and commercial infrastructure projects requiring enhanced safety, acoustic performance, and UV protection. More than 65% of newly introduced premium passenger vehicles utilize advanced laminated glass configurations. Manufacturers are expanding localized film conversion capacity while strengthening partnerships with automotive glass suppliers to improve delivery performance and reduce procurement risk. Automation investments have improved production consistency by nearly 18%, supporting higher-value specialty film manufacturing. Enterprise demand continues shifting toward customized interlayer solutions with greater optical clarity and durability, reinforcing the region's position in premium application development.

United States Market Outlook: The United States remains the largest national market due to its extensive automotive production, advanced building standards, and growing investment in renewable energy infrastructure. More than 70% of domestic automotive laminated glass production utilizes high-performance interlayer technologies, while manufacturers continue expanding regional supply capabilities through automated production lines and long-term OEM partnerships. Strong product certification requirements and continuous investment in advanced glazing technologies further strengthen industrial competitiveness.

Europe accounts for approximately 24.8% of global market demand, supported by stringent building regulations, premium automotive manufacturing, and increasing adoption of energy-efficient glazing systems. Architectural modernization programs and sustainable infrastructure investments continue driving specification of laminated safety glass with enhanced acoustic and solar-control performance. Nearly 58% of newly completed commercial buildings integrate advanced laminated glazing technologies for energy optimization and occupant protection. Producers are investing in specialty interlayer development, recyclable material technologies, and precision manufacturing systems while expanding collaboration with regional glass processors. High-performance product differentiation and environmental compliance continue shaping purchasing decisions across automotive and construction industries.

Germany Market Outlook: Germany leads the European market through its strong automotive manufacturing ecosystem, advanced engineering capabilities, and premium architectural glass production. Approximately 40% of regional specialty automotive glazing development is concentrated within Germany, where manufacturers continue investing in acoustic and multifunctional laminated glass technologies. Continuous modernization of industrial production facilities supports higher operational efficiency and accelerated commercialization of advanced interlayer products.

Asia-Pacific contributes approximately 48.6% of global market demand and remains the world's largest manufacturing hub for Polyvinyl Butyral Film. Extensive automotive production, expanding photovoltaic deployment, and rapid commercial construction continue strengthening downstream consumption of laminated glass materials. More than 55% of global laminated automotive glass production is concentrated within the region, while production capacity expansion exceeds 20% across several industrial clusters. Companies continue commissioning integrated manufacturing facilities, optimizing production efficiency, and expanding export-oriented operations to strengthen global supply reliability. Large-scale manufacturing, competitive production economics, and vertically integrated value chains provide significant operational advantages for regional producers.

China Market Outlook: China dominates the regional market through its extensive automotive manufacturing, photovoltaic module production, and architectural glass industry. The country accounts for roughly 38% of global Polyvinyl Butyral Film manufacturing capacity, supported by integrated industrial parks and advanced processing infrastructure. Continuous investment in intelligent manufacturing, export expansion, and specialty film production enables domestic manufacturers to strengthen both local demand fulfillment and international market competitiveness.

South America accounts for approximately 3.2% of the global market, supported by expanding transportation infrastructure, commercial construction, and gradual modernization of automotive manufacturing. Demand continues increasing for laminated safety glass across public infrastructure and high-rise developments emphasizing occupant protection and durability. More than 28% of recent commercial construction projects specify laminated glazing for enhanced structural safety and environmental performance. Regional manufacturers are improving distribution networks, expanding converter partnerships, and increasing localized inventory to shorten supply cycles. Infrastructure funding and industrial modernization continue supporting gradual market expansion despite logistics limitations and import dependence for certain specialty materials.

Brazil Market Outlook: Brazil represents the largest market within South America due to its established automotive manufacturing base and expanding commercial construction sector. Automotive production clusters continue increasing procurement of laminated glazing components, while investments in logistics and industrial modernization improve operational efficiency. Growing adoption of advanced safety standards is encouraging greater use of premium laminated glass technologies across transportation and infrastructure applications.

Middle East & Africa represents approximately 1.0% of global demand, supported by major commercial developments, transport infrastructure projects, and premium real estate investments. Increasing specification of laminated safety glass for airports, commercial towers, healthcare facilities, and hospitality projects is strengthening demand for high-performance interlayer materials. More than 35% of landmark commercial developments in the Gulf region now incorporate advanced laminated glazing systems for safety and energy efficiency. Companies are expanding regional distribution partnerships, strengthening technical support capabilities, and improving localized product availability to meet evolving project requirements. Continued infrastructure modernization is enhancing long-term demand across premium construction applications.

Saudi Arabia Market Outlook: Saudi Arabia leads regional demand through extensive infrastructure development, large-scale urban transformation initiatives, and significant commercial construction investment. Advanced glazing technologies are increasingly specified across mixed-use developments, transportation hubs, and public infrastructure projects, with premium laminated glass adoption rising by approximately 25% in newly approved flagship developments. Continued investment in smart city infrastructure and sustainable construction strengthens long-term opportunities for Polyvinyl Butyral Film suppliers.

The Polyvinyl Butyral Film Market is led by Kuraray, Eastman Chemical Company, Sekisui Chemical, EVERLAM, and Chang Chun Group, with global technology leaders competing against cost-focused Asian manufacturers and regional specialty suppliers. The top five companies collectively control approximately 68% of global market share through integrated manufacturing, proprietary resin technologies, and long-term automotive glass partnerships. Competition centers on optical performance, production efficiency, customized formulations, and supply reliability rather than price alone. Advanced manufacturing has improved production efficiency by nearly 18%, while premium acoustic and UV-resistant films command pricing premiums of 12–20%. Companies continue strengthening positions through capacity expansion, vertical integration, product innovation, and strategic partnerships with automotive OEMs and architectural glass processors. The competitive landscape is shifting toward specialty high-performance films, sustainable formulations, and localized manufacturing to strengthen supply resilience. High capital requirements, demanding quality certifications, and customer qualification cycles remain major entry barriers. Success depends on technological differentiation, consistent product quality, global supply capability, and deep customer integration.

Eastman Chemical Company

Sekisui Chemical Co., Ltd.

EVERLAM NV

Chang Chun Group

Kingboard Chemical Holdings Ltd.

Huakai Plastic (Chongqing) Co., Ltd.

Zhejiang Decent Plastic Co., Ltd.

Jiangsu Daruihengte Technology Co., Ltd.

Wuhan Honghui New Material Co., Ltd.

Tiantai Kanglai Industrial Co., Ltd.

Rehone Plastic Products Co., Ltd.

Precision multilayer extrusion, AI-enabled optical inspection, and advanced resin compounding define current technology leadership across the Polyvinyl Butyral Film Market. Automated inline inspection improves defect detection by approximately 20%, while digital process control enhances production consistency by nearly 15%. More than 60% of newly commissioned premium production lines now incorporate intelligent monitoring systems, enabling manufacturers to reduce waste and maintain tighter thickness tolerances required by automotive and architectural customers.

High-acoustic, UV-resistant, and recyclable PVB formulations are replacing conventional standard interlayers across premium applications. Compared with legacy production systems, next-generation extrusion platforms improve throughput by approximately 18% while reducing material losses by nearly 10%. Global technology leaders benefit most through differentiated product portfolios, whereas regional manufacturers increasingly compete by upgrading automation and expanding specialty film capabilities. Integration with digital quality management platforms is becoming a competitive requirement rather than an operational advantage.

Between 2026 and 2028, manufacturers are expected to accelerate deployment of predictive maintenance, closed-loop process control, and sustainable material technologies. Wider adoption of recyclable interlayer formulations and AI-assisted manufacturing will strengthen operational flexibility, shorten production cycles, improve certification compliance, and create stronger competitive positioning across automotive, photovoltaic, and advanced architectural glazing markets.

March 2024 – Kuraray announced a US$410 million investment to construct a new EVAL™ production facility in Singapore with an initial capacity of 18,000 tons per year, strengthening long-term supply capabilities and manufacturing resilience across Asia. Source: www.kuraray.com

November 2024 – Kuraray secured ISCC PLUS certification across multiple European and U.S. production sites, establishing a certified supply chain for PVB resin and related materials while expanding sustainable product offerings for industrial customers. Source: www.kuraray.com

June 2025 – Kuraray announced expansion of optical-use Poval film production facilities to support growing demand from larger display applications, reinforcing manufacturing scalability and strengthening advanced film production capabilities.

June 2025 – Kuraray introduced fully transparent MOWITAL® PVB adhesive films for industrial lamination in glass, composites, and lightweight components, expanding high-performance application opportunities with processing temperatures as low as 140°C and enhanced recycling compatibility.

This report provides comprehensive analysis of the Polyvinyl Butyral Film Market across major product types, applications, end-users, and regional markets between 2026 and 2033. It evaluates demand distribution across automotive, architectural, photovoltaic, and specialty applications while assessing evolving adoption patterns, manufacturing trends, technology integration, and competitive positioning. The study covers North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, representing virtually all global consumption and production activity. More than 12 leading industry participants are assessed alongside emerging manufacturers and specialty suppliers.

The report delivers strategic insights into production technologies, supply-chain developments, sustainability initiatives, product innovation, and regional investment priorities. It highlights deployment trends, operational shifts, market concentration, and evolving customer requirements to support expansion planning, partnership evaluation, product development, competitive benchmarking, and long-term investment decisions. The analysis also identifies emerging niche opportunities, technology adoption patterns, and changing procurement strategies influencing future market direction.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 305.0 Million |

| Market Revenue (2033) | USD 432.7 Million |

| CAGR (2026–2033) | 4.5% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Companies Profiled | Kuraray Co., Ltd.; Eastman Chemical Company; Sekisui Chemical Co., Ltd.; EVERLAM NV; Chang Chun Group; Kingboard Chemical Holdings Ltd.; Huakai Plastic (Chongqing) Co., Ltd.; Zhejiang Decent Plastic Co., Ltd.; Jiangsu Daruihengte Technology Co., Ltd.; Wuhan Honghui New Material Co., Ltd.; Tiantai Kanglai Industrial Co., Ltd.; Rehone Plastic Products Co., Ltd. |

| Customization & Pricing | Available on Request (10% Customization Free) |