Reports

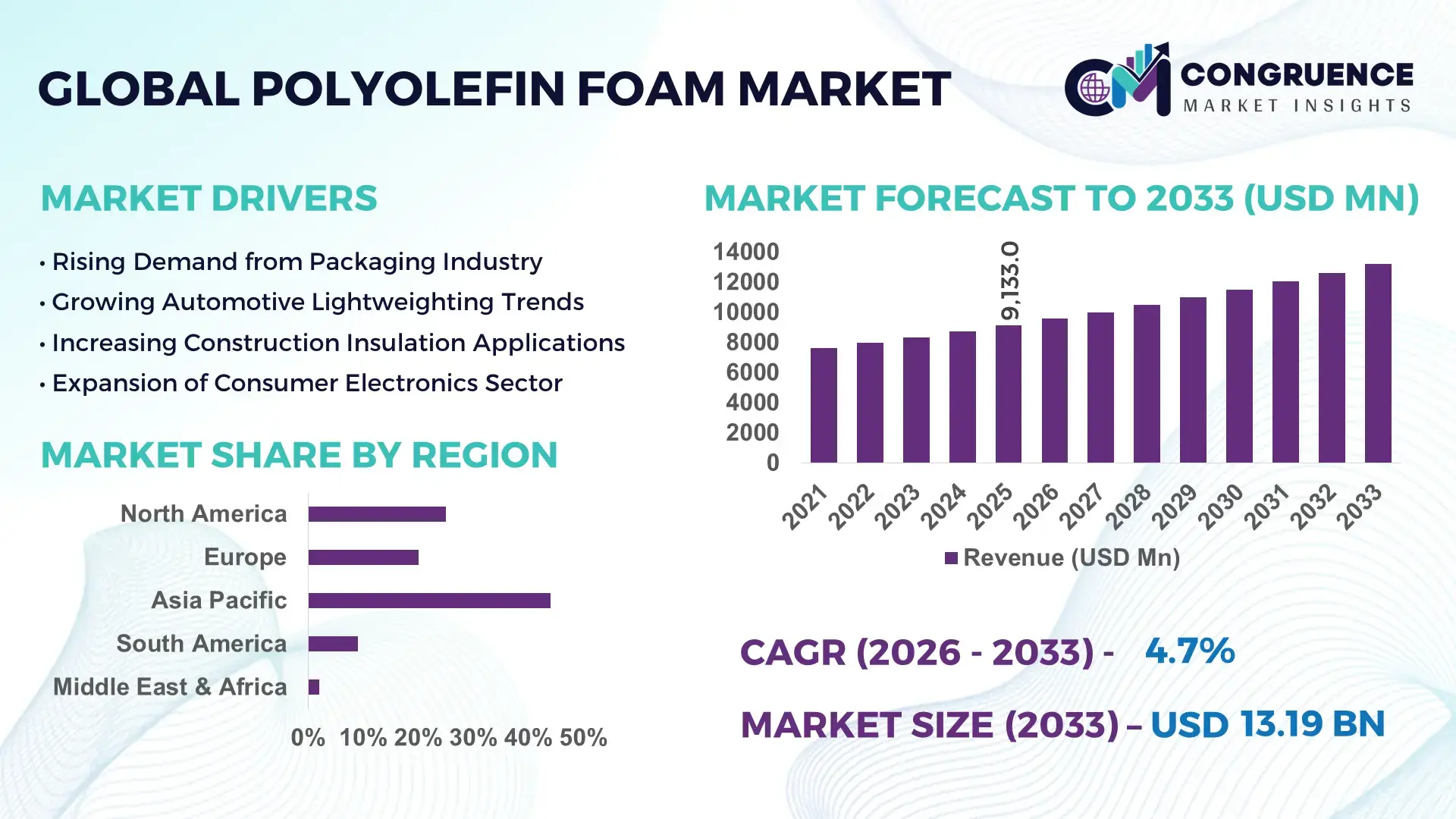

The Global Polyolefin Foam Market was valued at USD 9133 Million in 2025 and is anticipated to reach a value of USD 13188.24 Million by 2033 expanding at a CAGR of 4.7% between 2026 and 2033. This growth is primarily driven by increasing demand for lightweight, durable, and recyclable foam materials across automotive, packaging, and construction sectors.

China stands at the forefront of the polyolefin foam market with extensive production infrastructure and large-scale industrial integration. The country operates over 250 advanced foam manufacturing facilities, with annual polyolefin resin consumption exceeding 20 million tons for foam applications alone. Significant investments in automated extrusion and cross-linking technologies have enabled high-volume production of polyethylene (PE) and polypropylene (PP) foams for automotive insulation and protective packaging. Approximately 35% of domestic foam output is utilized in the automotive sector, while nearly 28% supports electronics packaging. Rapid adoption of closed-cell foam technologies and government-backed industrial upgrades have enhanced product quality and export competitiveness, particularly in Asia-Pacific and European supply chains.

Market Size & Growth: Valued at USD 9133 Million in 2025, projected to reach USD 13188.24 Million by 2033 at 4.7% CAGR, driven by rising demand for lightweight insulation materials.

Top Growth Drivers: Automotive lightweighting adoption (42%), protective packaging demand increase (36%), construction insulation efficiency gains (29%).

Short-Term Forecast: By 2028, advanced foam processing technologies are expected to improve material efficiency by 18% and reduce waste by 12%.

Emerging Technologies: Electron-beam cross-linking, biodegradable polyolefin blends, and high-density extrusion foaming innovations.

Regional Leaders: Asia-Pacific to reach USD 5.6 Billion by 2033 with strong manufacturing demand; North America USD 3.4 Billion driven by packaging innovation; Europe USD 2.9 Billion with sustainability-focused adoption.

Consumer/End-User Trends: Automotive and electronics sectors account for over 60% combined usage, with increasing preference for recyclable foam solutions.

Pilot or Case Example: In 2024, a Japanese manufacturer improved thermal insulation efficiency by 22% using cross-linked polyolefin foam in EV battery systems.

Competitive Landscape: Market leader holds approximately 18% share, followed by major global producers and regional manufacturers expanding capacity.

Regulatory & ESG Impact: Increasing compliance with recyclable material mandates and reduction of VOC emissions across manufacturing processes.

Investment & Funding Patterns: Over USD 2 Billion invested globally in foam processing technologies and sustainable material development since 2023.

Innovation & Future Outlook: Growth in bio-based polyolefin foams and integration with smart insulation systems are shaping future market expansion.

Polyolefin foam market growth is significantly influenced by key sectors such as automotive, packaging, and construction, contributing approximately 35%, 30%, and 20% respectively to total demand. Recent innovations include the development of low-density, high-strength foams that reduce material usage by up to 15% while maintaining structural integrity. Environmental regulations promoting recyclable materials have accelerated the shift toward eco-friendly foam variants, particularly in Europe and North America. Consumption patterns show strong growth in Asia-Pacific due to industrial expansion, while developed regions focus on high-performance and sustainable foam solutions. Emerging trends include the integration of antimicrobial properties in packaging foams and increased adoption in electric vehicle thermal management systems.

The polyolefin foam market holds strategic importance due to its critical role in lightweight manufacturing, energy-efficient insulation, and protective packaging solutions across multiple industries. Advanced cross-linked polyolefin foam technology delivers up to 25% higher thermal insulation performance compared to traditional polyurethane foam, enabling enhanced energy efficiency in construction and automotive applications. Asia-Pacific dominates in production volume, while Europe leads in sustainable adoption with over 48% of manufacturers integrating recyclable foam materials into their product lines.

In the short term, by 2028, AI-driven process optimization in foam extrusion is expected to reduce material wastage by nearly 15% while improving production efficiency by 20%. Companies are aligning with ESG commitments by targeting up to 30% recyclability improvements in foam materials by 2030, supported by regulatory mandates on plastic waste reduction. A notable micro-scenario occurred in 2024, where a South Korean manufacturer achieved a 19% reduction in production energy consumption through automated extrusion line upgrades and real-time monitoring systems.

The market is increasingly shaped by the integration of sustainable raw materials, digitized manufacturing, and advanced material science innovations. Polyolefin foam is positioned as a critical component in next-generation automotive and construction solutions, reinforcing its role as a pillar of industrial resilience, regulatory compliance, and long-term sustainable growth.

The increasing emphasis on vehicle weight reduction to improve fuel efficiency and reduce emissions is a major driver for the polyolefin foam market. Polyolefin foams are up to 30% lighter than conventional materials used in automotive interiors and insulation, contributing significantly to overall vehicle efficiency. In electric vehicles, lightweight materials enhance battery performance and extend driving range, making polyolefin foam an essential component in thermal insulation and vibration damping applications. Automotive manufacturers are incorporating foam materials in door panels, headliners, and seating systems, with usage increasing by over 20% in recent vehicle models. Additionally, regulatory mandates on emission reduction are accelerating the adoption of lightweight materials, further boosting demand. The combination of performance benefits, cost efficiency, and recyclability positions polyolefin foam as a key material in next-generation automotive design and manufacturing.

The polyolefin foam market faces significant challenges due to volatility in raw material prices, particularly polyethylene and polypropylene resins derived from petrochemical sources. Price fluctuations of up to 15–20% annually impact production costs and profit margins for manufacturers. These variations are influenced by crude oil price instability, supply chain disruptions, and geopolitical factors affecting petrochemical production. Manufacturers often struggle to maintain consistent pricing strategies, leading to reduced competitiveness in price-sensitive markets such as packaging. Smaller producers are particularly vulnerable, as they lack the financial flexibility to absorb cost increases. Additionally, dependency on fossil-based raw materials raises concerns about long-term sustainability, further complicating procurement strategies. These factors collectively hinder stable growth and create uncertainty in the market environment.

The growing focus on sustainability presents significant opportunities for the polyolefin foam market, particularly through the development of recyclable and bio-based foam materials. Innovations in eco-friendly polyolefin blends have enabled manufacturers to produce foams with up to 40% recycled content without compromising performance. This aligns with global environmental regulations and corporate sustainability goals. Demand for sustainable packaging solutions is increasing rapidly, with over 60% of companies actively seeking recyclable alternatives to traditional plastics. Polyolefin foam’s ability to be reused and reprocessed makes it an attractive option for circular economy initiatives. Additionally, advancements in biodegradable additives and low-emission manufacturing processes are opening new avenues in environmentally conscious markets. These innovations are expected to expand application areas and attract investment in green material technologies.

Despite its recyclability potential, the polyolefin foam market faces challenges related to complex recycling processes and stringent environmental regulations. Cross-linked polyolefin foams, widely used for their durability, are difficult to recycle due to their chemical structure, limiting large-scale reuse. This creates compliance challenges in regions with strict plastic waste management laws. Additionally, regulatory requirements for reduced carbon emissions and waste generation are increasing operational costs for manufacturers. Implementing advanced recycling technologies and sustainable production processes often requires substantial capital investment, which can be a barrier for small and medium enterprises. Furthermore, lack of standardized recycling infrastructure in many regions restricts the effective collection and processing of foam waste. These challenges necessitate continuous innovation and collaboration across the value chain to ensure regulatory compliance and sustainable growth.

• Accelerated adoption of lightweight automotive insulation materials: The automotive sector is witnessing a measurable shift toward polyolefin foam, with over 48% of manufacturers integrating lightweight foam components into vehicle interiors and insulation systems. Polyolefin foam reduces vehicle weight by approximately 25–30%, directly improving fuel efficiency and electric vehicle battery performance. Around 35% of EV manufacturers now utilize cross-linked polyolefin foams for thermal management and vibration control. This trend is further reinforced by regulatory mandates targeting emission reductions, pushing automakers to replace heavier traditional materials with advanced foam alternatives across dashboards, seating, and door panels.

• Expansion of sustainable and recyclable foam solutions: Sustainability-driven innovation is reshaping the polyolefin foam market, with nearly 62% of packaging companies transitioning toward recyclable or reusable foam materials. New formulations incorporating up to 40% recycled content are being widely adopted without compromising durability or cushioning performance. Additionally, over 50% of European manufacturers have introduced low-VOC and eco-certified foam products to meet strict environmental standards. The push toward circular economy practices has increased demand for closed-loop recycling systems, particularly in high-volume industries such as electronics and consumer goods packaging.

• Growth in electronics and protective packaging demand: The electronics sector accounts for approximately 28% of total polyolefin foam usage, driven by rising demand for shock-absorbing and anti-static packaging materials. With global consumer electronics production increasing by over 12% annually, manufacturers are prioritizing high-performance foam packaging that reduces product damage rates by up to 20%. Anti-static polyolefin foam solutions are now used by nearly 45% of semiconductor packaging facilities, ensuring protection against electrostatic discharge during transportation and storage. This trend is particularly strong in Asia-Pacific manufacturing hubs.

• Rise in modular and prefabricated construction applications: The adoption of modular construction practices is transforming demand for polyolefin foam in insulation and structural applications. Approximately 55% of new construction projects report cost savings when using prefabricated components integrated with precision-cut foam insulation. These materials improve thermal efficiency by up to 18% and reduce installation time by nearly 30%. Demand for pre-engineered foam panels is increasing rapidly in North America and Europe, where over 40% of large-scale commercial projects now incorporate modular building techniques to enhance efficiency and reduce labor dependency.

The polyolefin foam market is segmented based on type, application, and end-user industries, each contributing distinctively to overall demand patterns. Polyethylene (PE) and polypropylene (PP) foams dominate the product landscape due to their superior flexibility, thermal insulation, and moisture resistance. Application-wise, automotive and packaging sectors collectively account for over 65% of total consumption, driven by increasing demand for lightweight and protective materials. In terms of end-users, automotive manufacturers, construction firms, and electronics producers represent the core demand base, with rising adoption of high-performance foam materials for energy efficiency and product protection. Regional segmentation reveals strong consumption in Asia-Pacific due to manufacturing expansion, while Europe and North America emphasize sustainable and high-specification foam solutions.

Polyethylene (PE) foam remains the leading segment, accounting for approximately 52% of total adoption due to its excellent cushioning properties, low density, and cost-effectiveness. It is widely used in packaging and automotive insulation, where flexibility and shock absorption are critical. Polypropylene (PP) foam holds around 30% share, offering higher temperature resistance and structural strength, making it suitable for automotive and industrial applications. However, cross-linked polyolefin foam is emerging as the fastest-growing segment, expanding at an estimated CAGR of 6.2%, driven by its superior durability, closed-cell structure, and enhanced thermal insulation capabilities.

Other foam types, including expanded polyolefin and specialty blends, collectively contribute approximately 18% of the market, serving niche applications such as medical packaging and high-performance insulation systems. These materials are gaining attention for their ability to combine lightweight properties with enhanced chemical resistance.

Automotive applications dominate the polyolefin foam market, accounting for nearly 38% of total usage due to the increasing need for lightweight materials in vehicle manufacturing. Polyolefin foam is extensively used in seating, door panels, and thermal insulation systems, contributing to improved fuel efficiency and passenger comfort. Packaging applications follow with approximately 32% share, driven by the demand for protective and anti-static materials in electronics and consumer goods industries.

Construction is the fastest-growing application segment, expanding at an estimated CAGR of 5.8%, supported by rising demand for energy-efficient building materials and insulation solutions. Polyolefin foam enhances thermal performance and moisture resistance in residential and commercial buildings. Other applications, including sports equipment, footwear, and medical uses, collectively account for about 30% of market demand, reflecting diversified usage across industries.

The automotive industry leads as the primary end-user, contributing approximately 35% of total polyolefin foam demand, driven by the shift toward lightweight and energy-efficient vehicles. Foam materials are increasingly used in electric vehicles, with adoption rates exceeding 40% in battery insulation and interior components. The construction sector follows with around 27% share, leveraging polyolefin foam for thermal insulation and moisture protection in modern infrastructure projects.

The electronics industry is the fastest-growing end-user segment, expanding at an estimated CAGR of 6.5%, fueled by rising production of consumer electronics and the need for advanced protective packaging. Polyolefin foam usage in electronics packaging has increased by over 20% in recent years due to its anti-static and shock-absorbing properties. Other end-users, including healthcare, sports, and consumer goods, collectively contribute approximately 38% of demand, reflecting diverse application potential.

Region Asia-Pacific accounted for the largest market share at 46% in 2025 however, North America is expected to register the fastest growth, expanding at a CAGR of 5.6% between 2026 and 2033.

Asia-Pacific’s dominance is supported by high-volume manufacturing output exceeding 8.5 million tons of polyolefin foam annually, with China alone contributing over 52% of regional production capacity. Japan and South Korea collectively account for nearly 18% of advanced foam technology adoption, particularly in automotive and electronics applications. North America holds approximately 24% of the global market, driven by increased demand in packaging and EV manufacturing, while Europe contributes close to 21%, supported by sustainability-focused regulations and advanced insulation applications. South America and the Middle East & Africa together represent around 9%, with emerging infrastructure and industrial development projects driving incremental demand. Regional consumption patterns reveal that over 60% of total polyolefin foam usage is concentrated in industrial manufacturing hubs, while construction-related demand contributes nearly 25% globally.

North America accounts for approximately 24% of the global polyolefin foam market, supported by strong demand across automotive, packaging, and construction industries. The automotive sector alone contributes nearly 37% of regional consumption, driven by electric vehicle production and lightweight material requirements. Regulatory frameworks promoting energy efficiency and recyclable materials have led to over 45% of manufacturers adopting eco-friendly foam solutions. Technological advancements such as automated extrusion systems and digital process monitoring have improved production efficiency by nearly 20%. Local manufacturers are increasingly investing in innovation, with a U.S.-based producer recently expanding its cross-linked foam production capacity by 18% to meet rising EV demand. Consumer behavior reflects a strong preference for high-performance and sustainable materials, particularly in packaging and healthcare applications, where adoption rates exceed 50% among enterprises prioritizing environmental compliance and product safety.

Europe represents around 21% of the polyolefin foam market, with key countries such as Germany, the UK, and France driving regional demand. Germany alone accounts for nearly 32% of Europe’s consumption due to its robust automotive and industrial manufacturing base. Regulatory initiatives focused on reducing plastic waste and carbon emissions have led to over 55% of manufacturers adopting recyclable and low-VOC foam materials. The region is witnessing strong adoption of advanced insulation technologies, particularly in construction, where polyolefin foam improves energy efficiency by up to 20%. A leading European foam manufacturer recently introduced bio-based polyolefin foam products, increasing sustainable material usage by 28%. Consumer behavior in the region is heavily influenced by environmental awareness, with nearly 60% of businesses prioritizing compliance with sustainability standards and eco-certification requirements.

Asia-Pacific leads the polyolefin foam market in terms of volume, producing over 8.5 million tons annually, with China, India, and Japan as the top consuming countries. China contributes more than 50% of regional production, while India accounts for approximately 14% of consumption due to rapid infrastructure and manufacturing growth. The region’s strong industrial base supports widespread adoption across automotive, packaging, and electronics sectors, which together represent over 65% of demand. Technological innovation hubs in Japan and South Korea are advancing foam processing techniques, improving material performance by nearly 15%. A major regional manufacturer recently implemented automated foam extrusion lines, increasing output efficiency by 22%. Consumer behavior is driven by affordability and scalability, with over 70% of small and medium enterprises adopting cost-effective foam solutions for packaging and industrial applications.

South America accounts for approximately 5% of the global polyolefin foam market, with Brazil and Argentina serving as key contributors. Brazil represents nearly 60% of regional demand, supported by growth in automotive manufacturing and construction sectors. Infrastructure development projects have increased demand for insulation materials by over 18% in recent years. Government incentives promoting industrial expansion and trade policies supporting domestic manufacturing have encouraged the adoption of polyolefin foam solutions. A regional producer in Brazil recently expanded its production capacity by 12% to meet rising packaging demand. Consumer behavior in the region is influenced by cost sensitivity, with over 65% of businesses prioritizing affordable and durable materials for industrial and packaging applications.

The Middle East & Africa region holds approximately 4% of the global polyolefin foam market, driven by increasing demand in construction, oil & gas, and packaging industries. The UAE and South Africa are key growth countries, contributing nearly 40% and 25% of regional demand respectively. Infrastructure development projects, particularly in the Gulf region, have increased the use of insulation materials by over 20%. Technological modernization efforts, including the adoption of advanced foam processing equipment, have improved production efficiency by nearly 15%. Trade partnerships and regulatory initiatives promoting industrial diversification are further supporting market expansion. A local manufacturer in the UAE recently introduced high-density foam products tailored for construction insulation, improving thermal efficiency by 17%. Consumer behavior reflects a growing preference for durable and heat-resistant materials, particularly in construction and industrial applications.

China – 34% share in the Polyolefin Foam market, driven by high production capacity and large-scale industrial manufacturing integration.

United States – 18% share in the Polyolefin Foam market, supported by strong demand from automotive, packaging, and advanced material innovation sectors.

The polyolefin foam market exhibits a moderately fragmented structure with over 120 active global and regional competitors operating across production, processing, and distribution segments. The top five companies collectively account for approximately 38% of the total market share, indicating a competitive yet innovation-driven environment. Leading players are focusing on strategic initiatives such as capacity expansion, product innovation, and mergers to strengthen their market position.

In recent years, more than 25 major product launches have been recorded, primarily centered on recyclable and high-performance foam solutions. Partnerships between material suppliers and automotive manufacturers have increased by nearly 30%, enabling the development of customized foam applications for electric vehicles and lightweight components. Technological advancements such as electron-beam cross-linking and automated extrusion processes are being widely adopted, improving production efficiency by up to 20%.

Additionally, companies are investing heavily in sustainable material development, with over USD 2 billion allocated globally toward eco-friendly foam innovations since 2023. Regional players are also expanding their footprint through localized manufacturing facilities, particularly in Asia-Pacific, where production capacity has increased by over 15% in the past three years. This dynamic competitive landscape is characterized by continuous innovation, strategic collaborations, and a strong emphasis on sustainability.

Sekisui Chemical Co., Ltd.

JSP Corporation

BASF SE

Borealis AG

Armacell International S.A.

Zotefoams plc

Toray Industries, Inc.

Kaneka Corporation

Furukawa Electric Co., Ltd.

Rogers Corporation

Sealed Air Corporation

SABIC

Mitsui Chemicals, Inc.

Pregis LLC

Recticel NV

Technological advancements in the polyolefin foam market are increasingly centered on improving material performance, production efficiency, and sustainability outcomes. One of the most impactful innovations is electron-beam (e-beam) cross-linking technology, which enhances foam strength, ताप resistance, and durability by up to 25% compared to non-cross-linked alternatives. This process enables the production of uniform closed-cell structures, widely used in automotive insulation and high-performance packaging. Additionally, chemical cross-linking methods continue to evolve, offering improved density control and enabling manufacturers to produce ultra-lightweight foams with densities as low as 20–30 kg/m³.

Extrusion technology has also undergone significant transformation, with automated extrusion lines improving output consistency and reducing production defects by nearly 18%. Advanced extrusion systems now integrate real-time monitoring and AI-based quality control, allowing manufacturers to optimize temperature, pressure, and material flow parameters dynamically. These systems have demonstrated productivity improvements of up to 20% while minimizing material waste by approximately 12%.

Another key technological trend is the development of bio-based and recyclable polyolefin foams. Manufacturers are incorporating up to 40% recycled content into foam products without compromising mechanical strength or insulation performance. Innovations in additive technologies, such as nucleating agents and flame retardants, are enhancing foam properties, including fire resistance and thermal stability, making them suitable for construction and transportation applications.

Furthermore, digitalization and Industry 4.0 practices are reshaping production environments. Smart manufacturing systems equipped with IoT sensors are enabling predictive maintenance, reducing equipment downtime by nearly 15%. Emerging technologies such as 3D foam molding and precision cutting systems are also expanding customization capabilities, particularly in automotive and electronics sectors. These technological advancements collectively position polyolefin foam as a high-performance, sustainable material solution for diverse industrial applications.

• In March 2025, BASF SE expanded its sustainable materials portfolio by introducing advanced polyethylene-based foam solutions with improved recyclability and reduced environmental impact, aligning with circular economy goals and enhancing material efficiency in automotive and packaging applications. Source: www.basf.com

• In September 2024, Sekisui Chemical Co., Ltd. announced the expansion of its cross-linked polyolefin foam production capacity in Japan, increasing output by approximately 15% to meet rising demand from automotive and construction sectors. Source: www.sekisuichemical.com

• In January 2025, Zotefoams plc launched a new high-performance polyolefin foam grade designed for electric vehicle battery insulation, offering enhanced thermal resistance and reducing heat transfer by up to 20%. Source: www.zotefoams.com

• In July 2024, Armacell International S.A. introduced next-generation eco-friendly foam insulation products incorporating recycled content, improving sustainability performance while maintaining high durability for industrial and HVAC applications. Source: www.armacell.com

The Polyolefin Foam Market Report provides a comprehensive analysis of industry trends, segmentation structures, technological advancements, and regional dynamics shaping the global market landscape. The report covers multiple product types, including polyethylene foam, polypropylene foam, and cross-linked variants, which together account for over 80% of total product utilization across industries. It also evaluates application-specific demand patterns, with automotive, packaging, and construction sectors collectively contributing more than 65% of global consumption, while emerging applications in healthcare and electronics continue to expand their footprint.

Geographically, the report encompasses key regions such as Asia-Pacific, North America, Europe, South America, and the Middle East & Africa, offering detailed insights into regional production capacities, consumption trends, and industrial growth patterns. Asia-Pacific alone contributes over 45% of global production volume, supported by strong manufacturing ecosystems and infrastructure development.

The report further examines technological innovations, including advanced extrusion techniques, cross-linking technologies, and sustainable material development, highlighting their role in improving product efficiency and environmental compliance. It also includes analysis of supply chain dynamics, raw material sourcing, and production optimization strategies, with a focus on reducing waste and enhancing operational efficiency by up to 15%.

Additionally, the scope extends to end-user industries such as automotive, electronics, construction, and consumer goods, providing insights into adoption rates, usage patterns, and performance requirements. The report also addresses regulatory frameworks, sustainability initiatives, and emerging niche segments such as bio-based foams and high-performance insulation materials, offering a holistic view for strategic decision-making.

| Report Attribute/Metric | Report Details |

|---|---|

|

Market Revenue in 2025 |

USD V2025 Million |

|

Market Revenue in 2033 |

USD V2033 Million |

|

CAGR (2026 - 2033) |

4.7% |

|

Base Year |

2025 |

|

Forecast Period |

2026 - 2033 |

|

Historic Period |

2021 - 2025 |

|

Segments Covered |

By Types

By Application

By End User

|

|

Key Report Deliverable |

Revenue Forecast, Growth Trends, Market Dynamics, Segmental Overview, Regional and Country-wise Analysis, Competition Landscape |

|

Region Covered |

North America, Europe, Asia-Pacific, South America, Middle East, Africa |

|

Key Players Analyzed |

Sekisui Chemical Co., Ltd., JSP Corporation, BASF SE, Borealis AG, Armacell International S.A., Zotefoams plc, Toray Industries, Inc., Kaneka Corporation, Furukawa Electric Co., Ltd., Rogers Corporation, Sealed Air Corporation, SABIC, Mitsui Chemicals, Inc., Pregis LLC, Recticel NV |

|

Customization & Pricing |

Available on Request (10% Customization is Free) |