Reports

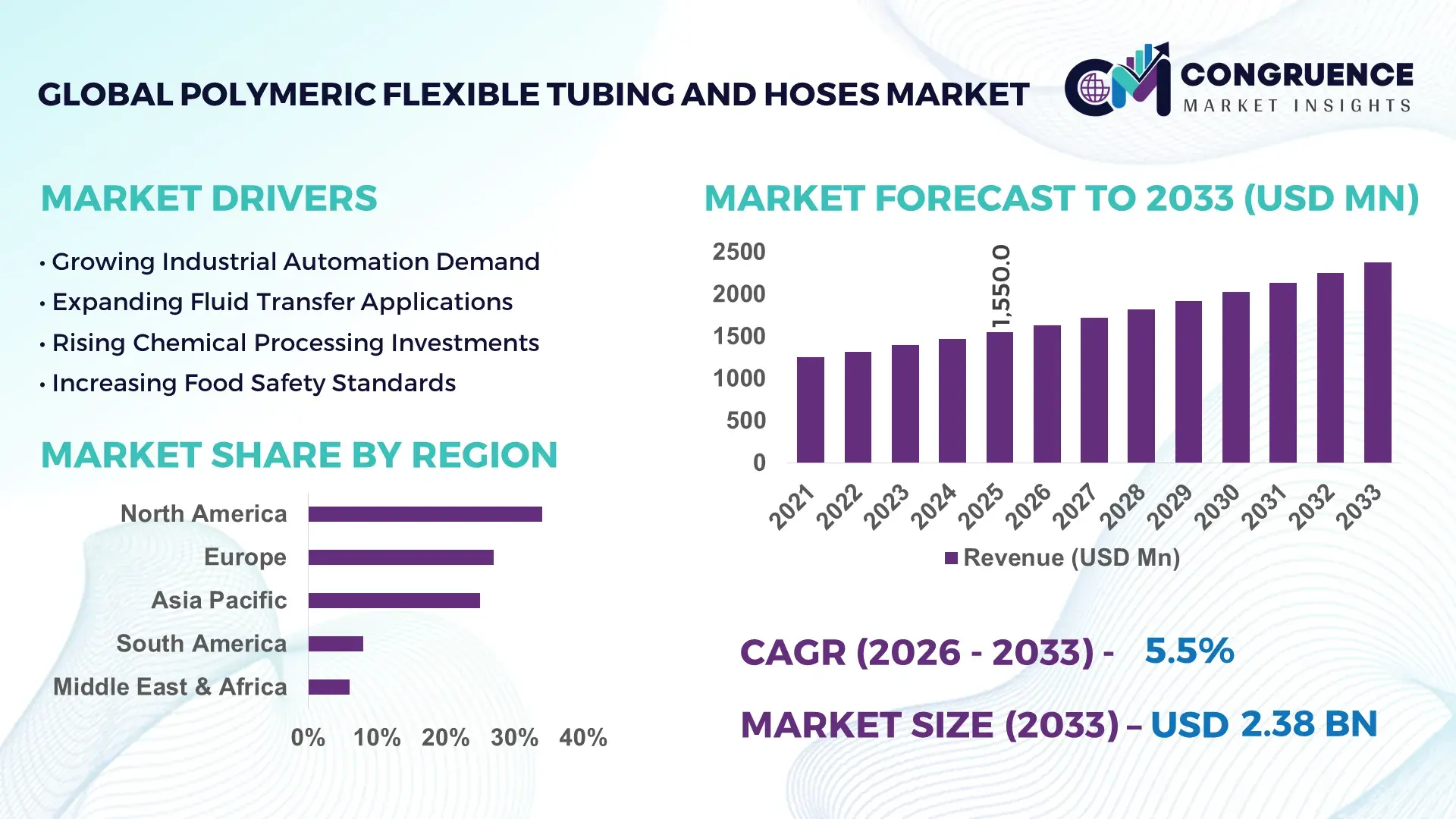

The Global Polymeric Flexible Tubing and Hoses Market was valued at USD 1,550.0 Million in 2025 and is anticipated to reach a value of USD 2,378.8 Million by 2033 expanding at a CAGR of 5.5% between 2026 and 2033. Growth is being accelerated by rising deployment of high-performance polymer hoses in automotive fluid management, semiconductor manufacturing, food processing, and industrial automation systems requiring corrosion-resistant and lightweight transfer solutions.

The United States leads the market with approximately 28% of global demand, supported by over USD 1 trillion in infrastructure modernization programs, a manufacturing sector contributing nearly 10% of national GDP, and strong adoption of advanced thermoplastic hose systems across energy and industrial applications. China follows with around 22% market share, backed by industrial production growth and extensive factory automation investments, while U.S. adoption of high-performance engineered tubing remains nearly 15% higher in critical process industries. The market also benefits from supply-chain realignment trends following geopolitical shifts affecting global manufacturing networks.

For manufacturers and investors, prioritizing advanced materials, localized production, and industrial automation partnerships remains critical for capturing long-term competitive advantage.

Market Size & Growth: Valued at USD 1,550.0 Million in 2025 and projected to reach USD 2,378.8 Million by 2033, supported by increasing adoption of lightweight thermoplastic fluid-transfer systems and industrial automation upgrades.

Top Growth Drivers: Industrial automation (+18%), automotive lightweighting initiatives (+14%), and food-grade processing infrastructure expansion (+12%) continue driving demand acceleration.

Short-Term Forecast: By 2028, advanced polymer hose installations are expected to improve maintenance efficiency by 20% while reducing downtime by nearly 15%.

Emerging Technologies: AI-enabled predictive maintenance, multilayer thermoplastic composites, and sensor-integrated smart tubing systems are reshaping operational performance.

Regional Leaders: North America (~USD 520 Million), Asia-Pacific (~USD 480 Million), and Europe (~USD 370 Million) lead adoption through industrial modernization, factory automation, and sustainability initiatives.

Consumer/End-User Trends: More than 45% of new industrial fluid-handling projects now prioritize corrosion-resistant polymer alternatives over conventional metal systems.

Pilot/Case Example: In 2024, automated process-line upgrades in advanced manufacturing facilities reduced fluid-transfer failures by approximately 22% through engineered polymer hose deployment.

Competitive Landscape: Leading suppliers collectively control nearly 35% of market activity, with major participation from Eaton, Parker Hannifin, Gates, Continental, and Saint-Gobain.

Regulatory & ESG Impact: Lightweight polymer solutions can lower transportation-related emissions by up to 10% while supporting stricter industrial efficiency standards.

Investment & Funding: More than USD 900 Million has been directed toward capacity expansion, specialty materials, and manufacturing localization initiatives globally.

Innovation & Future Outlook: Smart monitoring, recyclable polymer formulations, and advanced extrusion technologies are becoming key differentiators amid ongoing supply-chain diversification.

Polymeric Flexible Tubing and Hoses are increasingly utilized across industrial processing, pharmaceuticals, automotive systems, water treatment, and semiconductor manufacturing due to their chemical resistance, flexibility, and lightweight characteristics. Recent innovations include multilayer thermoplastic constructions, embedded monitoring capabilities, and enhanced barrier technologies. Nearly 40% of industrial users now prioritize durability-focused polymer solutions to reduce maintenance cycles, while evolving supply-chain localization strategies are encouraging regional production expansion, setting the stage for deeper strategic market transformation.

Polymeric flexible tubing and hoses have become strategically important as manufacturers seek greater operational efficiency, material durability, and supply-chain resilience across industrial operations. Growing infrastructure modernization, factory automation programs, and process-industry investments are increasing the need for advanced fluid-transfer systems capable of operating in demanding environments. The ongoing restructuring of global manufacturing networks is also encouraging localized production and diversified sourcing strategies.

From a technology perspective, advanced thermoplastic hose systems can reduce component weight by 30–50% compared with conventional metal alternatives while lowering maintenance requirements through superior corrosion resistance. Industrial operators in the United States and Germany are accelerating adoption of engineered polymer solutions in automated production facilities, whereas China continues to focus on large-scale deployment through manufacturing capacity expansion. Over the next two to three years, smart monitoring integration in industrial hose assemblies is expected to increase significantly as predictive maintenance becomes a core operational priority.

A practical example is the deployment of reinforced polymer fluid-transfer systems in automated manufacturing plants, where reduced downtime and longer replacement cycles improve productivity. Companies are responding through specialty material investments, regional manufacturing expansion, and strategic partnerships with automation providers. Organizations that successfully combine material innovation, localized supply chains, and digital monitoring capabilities will strengthen competitive positioning and operational resilience over the long term.

Industrial automation is creating substantial demand for advanced polymeric tubing and hose solutions capable of supporting high-cycle operations and precision fluid management. More than 45% of new automated manufacturing projects now specify lightweight, corrosion-resistant transfer systems, while industrial robotics installations have increased by over 12% annually across major manufacturing economies. The shift toward electric vehicles has also boosted demand, with lightweight fluid management components reducing system weight by up to 30% compared with traditional alternatives. Following supply-chain disruptions and geopolitical manufacturing realignments, companies are expanding domestic production capabilities and investing in specialty polymer technologies. Leading suppliers are strengthening partnerships with automation integrators and industrial OEMs to develop customized solutions, creating a strategic advantage through performance differentiation and lifecycle cost optimization.

Price volatility in petrochemical feedstocks remains a significant constraint for polymeric tubing and hose manufacturers. Key polymer materials such as polyurethane, PVC, and specialty thermoplastics have experienced periodic cost fluctuations exceeding 15–20%, directly affecting production economics and pricing stability. Global logistics disruptions have increased procurement lead times by nearly 25% in certain industrial segments, while dependency on imported specialty compounds continues to expose manufacturers to sourcing risks. Industrial buyers face challenges maintaining procurement budgets and project timelines during periods of material uncertainty. To mitigate exposure, companies are diversifying supplier networks, increasing regional sourcing strategies, and securing long-term procurement contracts. Firms investing in alternative material formulations and localized manufacturing footprints are better positioned to maintain profitability and supply continuity.

The emergence of sensor-enabled tubing systems presents a high-value opportunity for manufacturers seeking differentiation beyond conventional fluid-transfer products. Smart monitoring solutions can improve maintenance planning accuracy by more than 20% while reducing unplanned equipment failures across industrial facilities. Adoption of Industry 4.0 frameworks has increased by over 30% among large manufacturing enterprises, creating favorable conditions for intelligent hose assemblies capable of monitoring pressure, flow, and wear conditions. Japan and South Korea are expanding investments in precision manufacturing infrastructure where advanced tubing technologies deliver measurable operational benefits. Companies are increasing R&D spending on recyclable thermoplastics, multilayer composites, and embedded diagnostic capabilities. The combination of digital intelligence and material engineering is opening new premium-market segments with higher margins and stronger customer retention.

As polymeric tubing systems become more technically sophisticated, manufacturers face increasing challenges related to production scalability, quality consistency, and specialized workforce requirements. Advanced extrusion and multilayer manufacturing processes can increase production complexity by more than 25% compared with standard hose manufacturing methods. Quality-control requirements are becoming stricter in pharmaceutical, semiconductor, and food-processing applications, where failure rates must remain exceptionally low. The shortage of skilled polymer-processing technicians in key industrial countries has intensified competition for talent, affecting operational efficiency and expansion timelines. Companies must invest in workforce development, process automation, and digital quality-management systems to sustain competitiveness. Organizations that successfully scale advanced manufacturing capabilities while maintaining stringent performance standards will secure stronger long-term positioning in high-value industrial applications.

Smart Monitoring Integration Expands Industrial operators are increasingly deploying sensor-enabled tubing assemblies to support predictive maintenance and asset monitoring. Adoption of connected fluid-transfer systems increased by nearly 22% during the past two years, while unplanned maintenance events declined by approximately 18% in facilities using real-time pressure and flow monitoring. The transition toward Industry 4.0 architectures is accelerating integration with plant management platforms. In response, manufacturers are expanding digital product portfolios and partnering with automation providers to deliver data-enabled hose solutions with higher lifecycle visibility.

Supply Chain Localization Accelerates Following global logistics disruptions and geopolitical trade uncertainties, companies are restructuring sourcing and production networks closer to end-use markets. Local procurement programs have increased by roughly 25% among industrial component manufacturers, while average lead times for critical polymer materials have been reduced by nearly 15% through regional supplier diversification. U.S. and Indian manufacturers are expanding domestic production footprints to strengthen supply continuity. This shift is improving procurement stability while reducing exposure to transportation bottlenecks and import dependencies.

Advanced Thermoplastic Materials Gain Share High-performance thermoplastic elastomers and multilayer composite constructions are replacing conventional materials in demanding industrial applications. New-generation polymer formulations deliver up to 30% lower weight and approximately 20% greater abrasion resistance compared with legacy alternatives. Enterprise buyers are prioritizing durability and maintenance optimization rather than initial purchase cost. To capitalize on this trend, suppliers are increasing specialty material investments and expanding engineered product offerings for critical process environments.

Sustainability-Driven Product Redesign Regulatory pressure and corporate sustainability targets are reshaping product development priorities across fluid-transfer systems. More than 35% of large industrial buyers now evaluate recyclability and lifecycle efficiency during procurement decisions. Lightweight polymer solutions can reduce transportation-related emissions by nearly 10%, while manufacturing waste reduction initiatives have improved material utilization by approximately 12%. Companies are responding through recyclable material platforms, closed-loop production initiatives, and strategic collaborations focused on environmental compliance and operational efficiency.

Thermoplastic hoses represent the leading segment of the Polymeric Flexible Tubing and Hoses Market, accounting for an estimated 38% of total demand due to their lightweight construction, chemical resistance, and compatibility with automated industrial systems. Their ability to reduce installation complexity and maintenance requirements makes them particularly attractive across manufacturing, automotive, and fluid-handling applications. Reinforced polymer hoses remain a mature and widely deployed category, especially in high-pressure environments where durability and operational reliability are critical. The fastest-growing segment is specialty multilayer tubing, supported by rising demand from pharmaceutical processing, semiconductor manufacturing, and precision industrial operations. Adoption within advanced manufacturing facilities has increased by nearly 20%, reflecting growing requirements for contamination control and process efficiency. Flexible PVC tubing continues to maintain relevance in cost-sensitive applications, while polyurethane-based products are gaining traction in dynamic operating environments requiring superior abrasion resistance. Manufacturers are prioritizing product innovation, specialty material development, and capacity expansion to strengthen competitiveness as buyers increasingly shift toward performance-oriented solutions.

Industrial fluid transfer remains the dominant application segment, representing approximately 42% of market demand due to extensive deployment across manufacturing plants, processing facilities, and automated production environments. The segment benefits from continuous investment in industrial modernization and process optimization initiatives. Demand remains particularly strong in sectors requiring corrosion-resistant fluid management systems and reliable performance under varying operating conditions. Water treatment and chemical processing applications continue to provide stable demand due to infrastructure upgrades and stricter operational standards. The fastest-growing application is semiconductor and electronics manufacturing, where demand for high-purity tubing solutions has expanded by nearly 18% amid global fabrication capacity investments. Pharmaceutical processing is also experiencing accelerated adoption as contamination-control requirements become increasingly stringent. Automotive fluid management applications continue evolving with electric vehicle production, while food and beverage processing facilities are investing in advanced tubing systems to improve hygiene and operational efficiency. Suppliers are responding through customized product development, automation-compatible designs, and expanded technical support capabilities tailored to specialized end-use requirements.

The manufacturing sector represents the leading end-user group, accounting for approximately 40% of overall market consumption due to extensive utilization of tubing and hose assemblies in production equipment, material handling systems, and automated process lines. Large-scale deployment requirements, continuous operational cycles, and maintenance optimization objectives sustain strong purchasing activity. Chemical and process industries remain significant consumers, particularly where fluid compatibility and operational reliability directly affect productivity and compliance requirements. The fastest-growing end-user category is semiconductor and electronics manufacturing, supported by ongoing fabrication facility expansion and increasing demand for high-purity fluid-transfer systems. Adoption within this segment has increased by roughly 17% as manufacturers invest in precision process control and contamination prevention. Healthcare and pharmaceutical companies are also strengthening procurement activity through facility modernization and stricter quality standards. Food processing enterprises continue adopting specialized tubing solutions to improve sanitation and operational consistency. Suppliers are responding with application-specific product portfolios, strategic partnerships, customized engineering support, and localized service capabilities to capture emerging demand opportunities.

North America accounted for the largest market share at 34% in 2025 however, Asia-Pacific is expected to register the fastest growth, expanding at a CAGR of 6.8% between 2026 and 2033.

North America represented approximately 34% of global market demand in 2025, supported by extensive deployment across industrial automation, automotive manufacturing, pharmaceuticals, and energy infrastructure. The region benefits from strong adoption of engineered thermoplastic hose systems, particularly in high-performance fluid-transfer applications requiring chemical resistance and operational reliability. More than 45% of newly commissioned advanced manufacturing facilities now integrate automated fluid-management systems utilizing polymer-based tubing technologies. Ongoing investments in reshoring initiatives and industrial modernization continue strengthening regional production capabilities. Manufacturers are also expanding specialty material development programs to address growing requirements for precision manufacturing and predictive maintenance integration.

United States Market Outlook: The United States remains the largest contributor to regional demand due to its advanced industrial base, extensive automation investments, and large-scale manufacturing footprint. Industrial production facilities increasingly utilize high-performance tubing systems across semiconductor fabrication, food processing, and pharmaceutical operations. More than 60% of large manufacturing enterprises have accelerated automation-related capital expenditure programs, creating sustained demand for advanced fluid-transfer infrastructure. Domestic suppliers are expanding production capacity and strengthening partnerships with industrial equipment manufacturers to support operational efficiency and supply-chain resilience.

Europe accounted for approximately 27% of global market activity, supported by strong manufacturing capabilities, stringent environmental standards, and advanced industrial infrastructure. Demand remains concentrated within automotive production, industrial processing, healthcare manufacturing, and food-processing operations. Regulatory emphasis on sustainability and operational efficiency is encouraging adoption of lightweight and recyclable polymer solutions. Nearly 35% of industrial procurement programs now incorporate lifecycle performance criteria when evaluating fluid-transfer systems. Regional manufacturers are increasingly investing in advanced material engineering and circular production initiatives to improve environmental performance while maintaining product durability and operational reliability.

Germany Market Outlook: Germany serves as the region’s strategic manufacturing hub, supported by its leadership in industrial automation, precision engineering, and automotive production. The country continues to invest heavily in smart factory infrastructure and advanced manufacturing technologies. More than half of large industrial facilities have integrated Industry 4.0 frameworks into production operations, increasing demand for specialized tubing and hose assemblies. German manufacturers are also advancing research into high-performance thermoplastics and recyclable material platforms to support industrial competitiveness and regulatory compliance objectives.

Asia-Pacific held approximately 25% of global market share in 2025 and represents the fastest-expanding regional market due to rapid industrialization, infrastructure development, and manufacturing capacity growth. The region benefits from extensive deployment across electronics production, automotive assembly, water infrastructure, and industrial processing sectors. Factory automation investments continue increasing across major economies, while industrial equipment exports remain a significant demand catalyst. Regional manufacturers have expanded production capacity by more than 20% in several industrial clusters to support domestic and export requirements. Growing localization of specialty polymer production further strengthens supply-chain efficiency and operational competitiveness.

China Market Outlook: China remains the dominant market within Asia-Pacific due to its extensive manufacturing ecosystem, large-scale industrial production, and growing automation adoption. The country accounts for a substantial share of global electronics and industrial equipment output, generating significant demand for fluid-transfer technologies. Smart manufacturing deployment continues accelerating across industrial parks, while investments in semiconductor fabrication and advanced production facilities are strengthening demand for high-purity tubing systems. Domestic suppliers are increasing specialization in engineered polymer solutions to support evolving industrial performance requirements.

South America accounted for approximately 8% of global market demand, supported primarily by investments in mining, agriculture, food processing, and industrial infrastructure modernization. Demand is increasingly concentrated in applications requiring durable and corrosion-resistant fluid-transfer systems capable of operating under challenging environmental conditions. Infrastructure rehabilitation programs and industrial expansion projects are creating new deployment opportunities across manufacturing and resource-processing sectors. While logistics constraints and investment variability remain challenges, manufacturers are strengthening local distribution networks and technical support capabilities to improve market penetration and operational responsiveness.

Brazil Market Outlook: Brazil represents the largest market in South America due to its diversified industrial economy, extensive agricultural operations, and expanding manufacturing sector. Industrial processing facilities continue investing in equipment modernization programs aimed at improving productivity and maintenance performance. Demand is particularly strong within mining, food processing, and agricultural machinery applications where reliability and operational durability are critical. Companies are expanding regional service networks and localized inventory capabilities to support customer requirements and reduce equipment downtime across key industrial sectors.

Middle East & Africa represented approximately 6% of global market activity in 2025, supported by infrastructure modernization programs, energy-sector investments, and industrial diversification initiatives. Demand remains strongest in fluid-transfer applications linked to construction, water management, petrochemical processing, and industrial development projects. Several countries are prioritizing domestic manufacturing expansion and utility infrastructure upgrades, creating demand for advanced polymer-based systems. Strategic investments in industrial zones and processing facilities continue improving long-term market fundamentals while supporting greater adoption of modern fluid-management technologies.

Saudi Arabia Market Outlook: Saudi Arabia remains the region’s most strategically significant market due to large-scale infrastructure projects, industrial diversification initiatives, and substantial investments in manufacturing development. Industrial expansion linked to national economic transformation programs is increasing demand for advanced tubing and hose solutions across energy, construction, and processing industries. Major industrial zones continue attracting manufacturing investment, while water infrastructure modernization projects are creating additional deployment opportunities. Suppliers are strengthening local partnerships and distribution capabilities to support growing project activity and long-term industrial development priorities.

The competitive landscape is led by Parker Hannifin, Eaton, Gates Corporation, Continental (ContiTech), Saint-Gobain, and Trelleborg, with global technology leaders competing directly against regional hose manufacturers and low-cost local suppliers. The top five players collectively account for approximately 42% of market share, creating a moderately consolidated structure where engineering capability outweighs pure scale. Competition is centered on material performance, product lifespan, customization speed, and supply-chain reliability. Advanced polymer and thermoplastic solutions deliver up to 25% longer service life, while automated manufacturing reduces production lead times by nearly 15%. Premium suppliers compete through proprietary materials and integrated fluid-management systems, whereas regional competitors focus on pricing advantages that can be 10–20% lower in standard applications. Market leaders are expanding manufacturing footprints, investing in hydrogen, semiconductor, and pharmaceutical applications, and strengthening OEM partnerships. Vertical integration and localization strategies are becoming critical as customers prioritize supply security. The competitive shift is moving toward specialty engineered solutions rather than commodity products. Success increasingly depends on application expertise, manufacturing flexibility, and innovation-driven differentiation.

Eaton Corporation

Saint-Gobain Performance Plastics

Continental AG (ContiTech)

Gates Corporation

Trelleborg AB

Colex International Ltd.

Freelin-Wade

NewAge Industries

Teknor Apex Company

Kuriyama Holdings Corporation

NORRES Group

Polyhose India Pvt. Ltd.

Swagelok Company

Current technology adoption is centered on advanced thermoplastic elastomers, multilayer composite constructions, and high-purity polymer formulations. These technologies improve abrasion resistance by nearly 20% and reduce system weight by approximately 30% compared with conventional rubber-based alternatives. More than 45% of newly specified industrial fluid-transfer systems now utilize engineered thermoplastic solutions due to longer service intervals and improved chemical compatibility. Manufacturers serving semiconductor, pharmaceutical, and food-processing industries are accelerating deployment of contamination-resistant tubing platforms to meet increasingly stringent operational requirements.

Emerging innovation is focused on smart tubing and hose assemblies equipped with embedded sensors for pressure, temperature, and flow monitoring. Facilities deploying predictive maintenance technologies have reported maintenance-efficiency improvements exceeding 18% and reductions in unexpected downtime approaching 15%. Compared with traditional inspection-based maintenance models, connected systems provide real-time operational visibility and faster fault detection. Global leaders such as Parker Hannifin, Eaton, and Continental are leveraging these capabilities to strengthen premium product positioning and long-term customer retention.

Between 2026 and 2028, recyclable polymer compounds, AI-assisted quality control, and hydrogen-compatible hose technologies will gain momentum. Adoption across advanced manufacturing environments is expected to exceed 35% in key industrial sectors. Companies investing early in digital monitoring, specialty materials, and automation-enabled production will achieve stronger operational efficiency, greater supply-chain responsiveness, and enhanced competitive differentiation.

January 2024 – Continental (ContiTech) announced construction of a new hydraulic hose manufacturing facility in Aguascalientes, Mexico, supported by an investment of approximately US$90 million. The project is expected to double regional hydraulic hose capacity, strengthening North American supply resilience and customer responsiveness. Source: www.continental-industry.com

November 2024 – Eaton Corporation expanded its Puducherry manufacturing facility in India with a new 120,000-square-foot addition and plans to double production capacity for key product lines. The expansion enhances localization capabilities and supports faster delivery across industrial and infrastructure markets.

April 2025 – Continental (ContiTech) commissioned a dedicated hydrogen hose production line in Korbach, Germany, backed by approximately €3 million in investment. The new facility supports hose systems operating at pressures up to 700 bar, strengthening the company’s position in hydrogen infrastructure applications.

March 2025 – Eaton Corporation broke ground on a new 100,000-square-foot GEIS facility in Chennai, India, integrating manufacturing, R&D, and customer experience functions. The project strengthens regional engineering capabilities and supports expanding industrial electrification and infrastructure requirements across Asia.

The report provides a comprehensive assessment of the global Polymeric Flexible Tubing and Hoses Market across major product types, applications, end-user industries, and regional markets. Coverage includes thermoplastic hoses, reinforced polymer hoses, specialty tubing solutions, and advanced multilayer constructions deployed across industrial manufacturing, automotive systems, semiconductor production, healthcare, food processing, and water infrastructure applications. Regional analysis evaluates North America, Europe, Asia-Pacific, South America, and the Middle East & Africa, representing 100% of global market activity.

The study examines technology adoption trends, smart monitoring integration, advanced material innovation, supply-chain localization, and sustainability-driven product development. More than 40% of industrial buyers are shifting toward performance-oriented polymer solutions, while automation-related deployments continue expanding across manufacturing environments. The report delivers actionable intelligence for investment planning, capacity expansion, competitive benchmarking, partnership evaluation, and market-entry strategies. It also identifies emerging opportunities in hydrogen infrastructure, semiconductor manufacturing, and intelligent fluid-management systems expected to shape industry direction between 2026 and 2033.

| Report Attribute / Metric | Details |

|---|---|

| Market Revenue (2025) | USD 1,550.0 Million |

| Market Revenue (2033) | USD 2,378.8 Million |

| CAGR (2026–2033) | 5.5% |

| Base Year | 2025 |

| Forecast Period | 2026–2033 |

| Historic Period | 2021–2025 |

| Segments Covered |

By Type

By Application

By End-User

|

| Key Report Deliverables | Revenue Forecast; Market Trends; Growth Drivers & Restraints; Technology Insights; Segmentation Analysis; Regional Insights; Competitive Landscape; Regulatory & ESG Overview; Recent Developments |

| Regions Covered | North America; Europe; Asia-Pacific; South America; Middle East & Africa |

| Key Players Analyzed | Parker Hannifin; Eaton Corporation; Saint-Gobain Performance Plastics; Continental AG (ContiTech); Gates Corporation; Trelleborg AB; Colex International Ltd.; Freelin-Wade; NewAge Industries; Teknor Apex Company; Kuriyama Holdings Corporation; NORRES Group; Polyhose India Pvt. Ltd.; Swagelok Company |

| Customization & Pricing | Available on Request (10% Customization Free) |